MT - ArcelorMittal Has Become An Attractive Value Stock

2023-12-13 10:22:51 ET

Summary

- ArcelorMittal was characterized by highly cyclical performance in the past.

- However, the company has nearly eliminated its interest expense and has greatly reduced its share count thanks to its blowout earnings in the last three years.

- As a result, it has greatly improved its mid-cycle earnings per share.

- The company has a cheap valuation, trading at a low multiple of its expected earnings, and has promising growth prospects.

ArcelorMittal ( MT ) incurred the worst accident in its history on October 28 th , 2023, when it lost 46 of its employees in Kazakhstan. The stock shed 3% on that day. Since then, the stock has rallied 20% but it has still underperformed the S&P 500 by a wide margin over the last 12 months ( -5% vs. +16% ). In addition, the steel producer has an exceptionally cheap valuation, as it is trading at 5.5 times its expected earnings this year. Given also its promising growth prospects, the drastic reduction of its debt and its aggressive share repurchases, ArcelorMittal has become an attractive value stock.

Business overview

ArcelorMittal is one of the largest steel producers in the world, with operations in the Americas, Europe, Asia and Africa. It was founded in 1976 and is based in Luxembourg.

On October 28 th , 2023, ArcelorMittal experienced the worst accident in its history, in Kazakhstan. From the 252 employees who were working underground, 206 were safely evacuated but 46 people lost their lives. The company provided ample compensation to the families of the victims but, of course, the incident remains a disaster. This accident is a stern reminder of the risks related to mining operations.

On the bright side, due to this accident, ArcelorMittal initiated a comprehensive third-party audit of all its safety practices. The company will take a deep look in all its policies, standards, processes and procedures. As a result, it is likely to significantly improve its safety standards in the upcoming years. In other words, the accident was a tragic event but the worse seems to be behind the company.

Most investors avoid ArcelorMittal for its highly cyclical performance record. As a steel producer, the company is inevitably sensitive to the cycles of the price of steel. To be sure, ArcelorMittal has posted material losses in 5 of the last 10 years. Investors should generally avoid stocks with highly cyclical and unreliable performance.

However, ArcelorMittal seems to have greatly improved and smoothened its performance. When the global economy began to recover from the coronavirus crisis, the demand for steel rebounded strongly while global supply was limited due to supply chain disruptions. As a result, the price of steel skyrocketed to an all-time high in late 2021. Even better, while the price of steel has moderated, it remains above historical average prices thanks to the sustained demand for steel. Investors should be aware that steel is a critical component in wind power projects and other green energy projects, which have greatly increased in the last three years.

Thanks to the secular tailwind from the boom in clean energy projects, ArcelorMittal has enjoyed blowout profits in the last three years. It switched from a loss per share of -$0.64 in 2020 to all-time high earnings per share of $13.41 in 2021 and posted earnings per share of $11.39 in 2022. To provide a perspective, the sum of the earnings of ArcelorMittal in 2021 and 2022 is almost equal to its current stock price.

As the price of steel has moderated this year, ArcelorMittal is expected by analysts to earn “only” $4.68 per share this year. Notably, the stock is trading at only 5.5 times its expected earnings. More importantly, the company has taken full advantage of its blowout earnings in the last three years and thus it has permanently boosted its mid-cycle earnings per share.

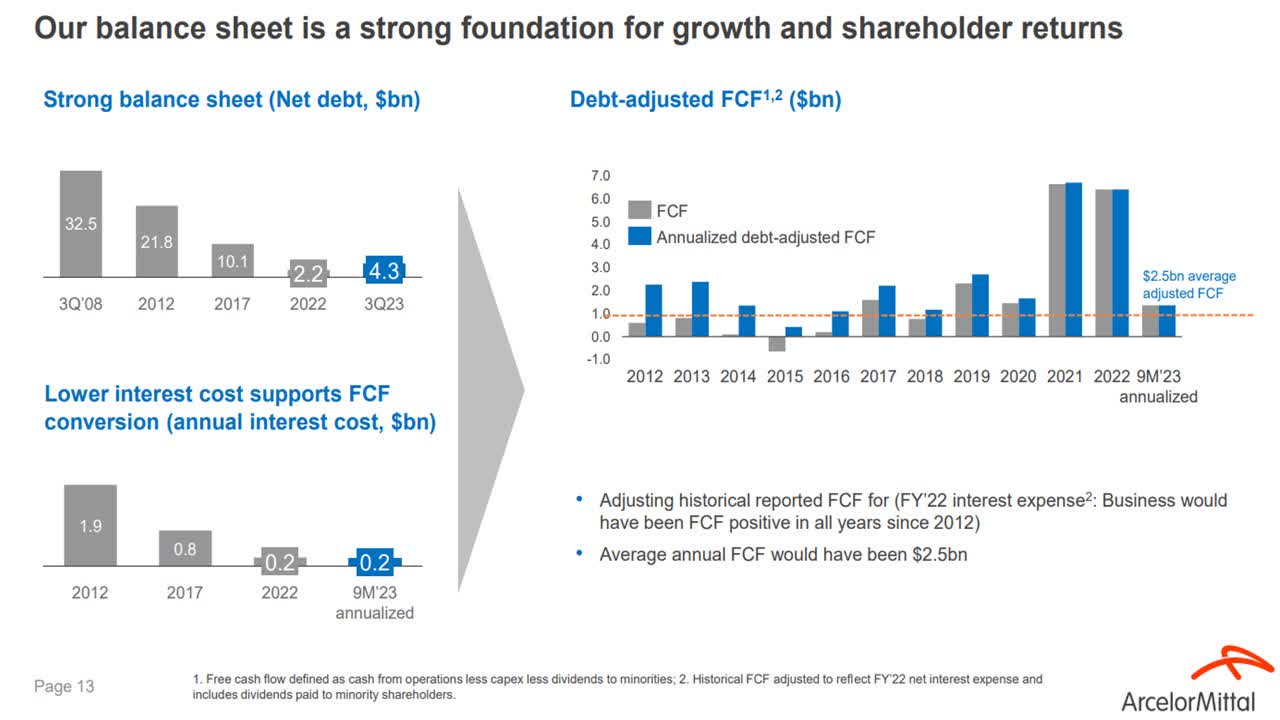

ArcelorMittal has drastically reduced its net debt, from $21.8 billion in 2012 to $4.3 billion now. As a result, it has nearly eliminated its net interest expense, from $1.9 billion in 2012 to $0.2 billion now.

{kind=link}

Source: Investor Presentation

If the annual free cash flow of ArcelorMittal is adjusted according to the current interest expense of the company, then the free cash flow becomes positive in every single year over the last decade. As shown in the above chart, the 10-year average adjusted free cash flow is $2.5 billion ($2.97 per share at the current share count).

Moreover, ArcelorMittal has been repurchasing its shares at an aggressive pace in the last three years thanks to its extraordinary earnings. As a result, the company has reduced the number of its outstanding shares by 32% over the last three years. Furthermore, it still has a repurchase program for another 78 million shares. This number of shares corresponds to 9% of the current share count. Overall, thanks to the extremely aggressive reduction of its interest expense and its material share repurchases, ArcelorMittal has greatly improved its mid-cycle free cash flow (and earnings) per share. Therefore, investors should not evaluate the stock based on its past earnings per share.

It is also important to note that ArcelorMittal enjoys a strong secular tailwind. Steel is a vital component in clean energy projects, which have been booming in the last three years. The company also benefits from strong population growth and improving living standards in emerging markets.

{kind=link}

Source: Investor Presentation

As a result, ArcelorMittal expects the ex-China global demand for steel to grow 35% over the next decade. Therefore, the price of steel has good chances of remaining elevated for the foreseeable future. Given also its current investment projects, ArcelorMittal expects to grow its EBITDA by $1.3 billion in the upcoming years. It thus implies ~17% growth of EBITDA, given the EBITDA of $7.5 billion in the last 12 months.

Valuation

Given the exceptionally high earnings per share of ArcelorMittal in the last three years, it is somewhat hard to predict how much the company can grow its earnings per share in the upcoming years. Analysts expect the earnings per share of the company to temporarily dip 15% next year, from $4.68 in 2023 to $3.99, but then grow to $6.00 thanks to the secular tailwind from the boom in clean energy projects and the investment program of the company.

It is critical to realize that the stock is trading at an extremely cheap valuation level. More precisely, it is trading at only 5.5 times its expected earnings this year, 6.5 times its expected earnings in 2024 and 4.3 times its expected earnings in 2025. Given also the rock-solid balance sheet of ArcelorMittal, its valuation is markedly cheap. Interest expense consumes just 4% of operating income while net debt is standing at $4.3 billion , which is approximately equal to the annual earnings and just 20% of the market capitalization of the stock.

It is also important to note that the exceptionally cheap valuation level of ArcelorMittal greatly enhances the value of its share repurchases. The longer ArcelorMittal remains cheaply valued the more shares it will be able to repurchase with a given amount of earnings. For instance, as ArcelorMittal is trading at 6.5 times its expected earnings in 2024, it will be able to repurchase up to 15% (=1/6.5) of its shares with its earnings.

Final thoughts

I have always dismissed ArcelorMittal due to the cyclical nature of its business and its high debt load until 2020. However, the company has changed course. The secular boom of green energy projects is likely to reduce the cyclicality of the global demand for steel. In addition, the company took full advantage of its blowout earnings in the last three years and drastically reduced its interest expense and its share count. As a result, it has greatly improved its mid-cycle earnings per share. Given also its depressed valuation level and its promising growth prospects, ArcelorMittal is a highly attractive value stock.

For further details see:

ArcelorMittal Has Become An Attractive Value Stock