MT - ArcelorMittal S.A.: Attractive Price Point To Get In At Right Now

2023-07-14 19:47:45 ET

Summary

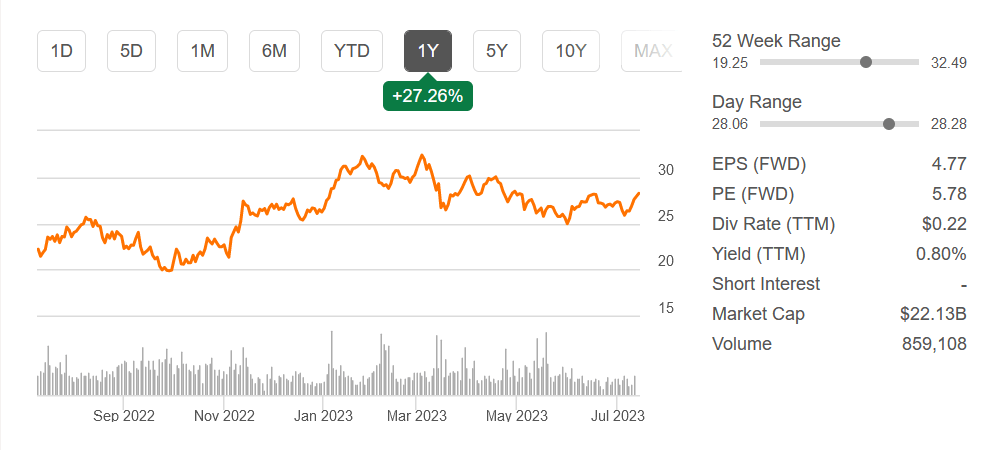

- ArcelorMittal S.A. has seen growth in steel consumption, leading to increased revenues and earnings, and has bought back a significant amount of shares, reducing shares outstanding by around 12% YoY.

- The company's Q1 2023 results showed a recovery in steel shipments and volumes, growing 12.7% QoQ, and a QoQ EPS increase from $0.3 in Q4 2022 to $1.28 in Q1 2023.

- ArcelorMittal is rated a buy due to its strong financial state, aggressive share buybacks are happening to boost investors' value.

Investment Summary

Steel-related companies can expect favorable conditions in the upcoming quarters and years, as the destocking phase appears to have concluded. This positive development has contributed to increased customer demand, resulting in a steady growth of both top and bottom lines for ArcelorMittal S.A ( MT ) throughout the first quarter and the beginning of 2023. Although the revenues and earnings have not yet reached the peak levels achieved in Q1 and Q2 of FY2022, MT has remained active in the market and implemented a substantial share buyback program.

MT adopts an investor-friendly strategy with a notable decrease of approximately 12% in shares outstanding YoY. This reduction serves as a primary method for the company to distribute earnings to shareholders, considering the relatively low dividend yield of around 0.22%. Moreover, MT is actively allocating substantial capital towards expanding its EBITDA, with an anticipated strategic capital expenditure of $4.2 billion from 2021 to 2024. Given the compelling current valuation, I find MT to be an attractive buy at present.

Shipments Increase As End Of Destocking Nears

A very important note to take from the last report was that destocking seems to be happening regarding steel. This has very positively affected the results for MT in the first quarter of 2023. They experience a recovery in the shipments and volumes, growing 12.7% QoQ.

Shipments (Earnings Presentation)

The coming quarters I think will be showcasing a similar trend of recovery as more and more manufacturers are becoming positive on the economic outlook. Seeing as steel plays such a vital role in our expansion of infrastructure and residential buildings, demand is rather persistent, but still goes in cycles depending on whether the economy is doing good or bad. The price of steel since December 2022 recovered very strongly, and I think both Q2 and Q3 for MT will show this in terms of revenues and earnings.

Steel Prices (IEA)

Fueling this growth seems to come from demand overseas, as the lack of steel plates supplied by Ukraine leaves an open void needing to be filled. Seeing as MT has an international presence it will in my opinion be easier for them to assert themselves successfully into these spaces and capture and satisfy demand. Some key markets they can serve will be Turkey, where reconstruction plans are underway after the devastating earthquakes that hit the country. Apart from that, looking at the Asia market, the easing of restrictions in China is helping with bringing a steady demand for steel as the economic environment here is beginning to once again rise.

Quarterly Result

The last quarter for MT showed the ability they have to quickly turn around and capture growth as the market they are in becomes more positive. On a QoQ basis, the EPS increased from $0.3 in Q4 2022 to $1.28 in Q1 2023.

Q1 Highlights (Earnings Report Q1)

The recovery of steel shipments accounted for a driving force in the growth of EBITDA on a QoQ basis, growing by 44.9%. This growth is great to see as the steel shipments didn't grow as much but still left a big impact on the bottom line. To me that indicates the company is very able to efficiently grow margins during upturns in the market sentiment. Besides that, there is a recovery in the prices for iron ore, over 26% compared to Q4 2022.

Iron Ore History (IEA)

As the price of iron ore recovers, so will likely the revenues for MT, as long as there aren't any issues with deliveries and production. In terms of future guidance for the market, MT sees positive in the short term, "Despite continued headwinds to real demand, the absence of any further destock is expected to support higher apparent demand in 2023 as compared to 2022. The Company's world ex-China apparent steel consumption ("ASC") growth forecast in 2023 as compared to 2022 (provided in February 2023) is for growth of +2.0% to +3.0%. The company maintains its previous guidance of steel shipments in 2023 to grow by ~5% vs. 2022".

In coming quarters this is what investors should be looking at, whether or not MT can efficiently grow their shipment volumes. If they can grow shipments above these estimates I think it could be a catalyst for the stock price, and we might see a valuation more in line with the materials sector which is 13. That would present a significant upside potential here as MT is valued at an FWD p/e of under 6 right now.

Upcoming Report

Estimates suggest that in Q2 of 2023 , MT will post a significant QoQ growth in terms of the EPS, $1.67 is the prediction. As I have mentioned throughout the article already, I think we will see an upward trend from now on in terms of the margins, which are being supported by stronger volumes and shipments, but also recovering steel prices.

In terms of margins in Q2 2023, I think anything under 8.2% will be a disappointment. A beat will mark the beginning of the growth cycle and entering into a position now would prove a great way to capture this momentum. Looking at the cash flows MT hinted in the last report that they expect the cash flows to largely outperform the results of Q1 for the remaining three quarters. With Q1 resulting in a neutral result, a surprise would provide more capital for MT to buy back shares, which is something I will be looking out for. The share price hasn't traded that richly in the last quarter, so I think MT would have been very good at being more aggressively buying shares. I would view that as a bullish sign and a factor to build more share price momentum.

Risks

The automotive, engineering, and construction industries, key consumers of steel, face macroeconomic uncertainties that could potentially lead to a slowdown in demand. Factors such as global trade tensions, changing government policies, and geopolitical events can affect these industries and, in turn, impact the prospects for steel manufacturers.

It is crucial for steel manufacturers to closely monitor and adapt to these evolving conditions to mitigate risks and seize opportunities. This may involve implementing efficient operational strategies, diversifying product offerings, and exploring new markets or sectors with growing demand. By proactively addressing these challenges, steel manufacturers can position themselves for long-term success in a dynamic and evolving global market. In terms of the position that MT holds right now, it's very strong in my opinion. A market cap of over $20 billion values them as one of the largest in the sector and industry. Leveraging this strength will be key to further growing both the top and bottom lines.

Valuation & Wrap Up

Right now the valuation for MT seems very appealing. The company does receive a quite low average p/e normally. It's usually somewhere between 3 and 7. Right now MT has a FWD multiple of 5.5 which I think presents a sound ratio between risk and reward right now that makes it an appealing buy. I think the coming quarters will show stronger revenues and earnings which will further fuel share price growth.

{kind=link}

The company is aggressively buying back shares to boost the value that shareholders are receiving. The financial state looks very solid what over $6 billion in cash and long-term debts of just over $8 billion. I don't think dilution is on the table and the risk that debt will hinder expansions and growth seems unlikely too. In conclusion, I am rating MT a buy right now.

For further details see:

ArcelorMittal S.A.: Attractive Price Point To Get In At Right Now