CNRFF - Arch Capital 2022 Annual Letter To Partners

Summary

- Arch Capital is a concentrated, long-only equity fund aiming to compound capital at an above-market rate.

- Our investments centered on the two worst-performing sectors of 2022 (technology and communication services) which were both down over 30% last year.

- Over the many years we plan on running the Arch Capital Limited Partnership, you can bet there will be more down years like 2022.

- We believe having investment flexibility gives us a higher chance of making rational decisions throughout all market environments.

| Arch Capital Investors Fund |

| S&P 500 Total Return Index |

| Returns Year To Date (2022) |

| (29.9%) |

| (18.1%) |

| Cumulative Returns Since Inception (2/1/21) |

| (32.4%) |

| 6.5% |

| *Fund returns are as of the end of Q4 2022 and net of realized and estimated fees. Returns may differ based on the timing of entry into the limited partnership. Contact archcapitalmanagement@gmail.com with any questions. |

Dear Limited Partners,

2022 was one of the worst years in the history of modern financial markets. The drawdown in the S&P 500 was the 7th sharpest of the past 100 years, with even worse results for bond investors as the Federal Reserve began its most aggressive interest rate hike campaign ever. These combined losses made it the worst year on record outside of the Great Depression for 60/40 portfolios, with the popular structure posting larger losses than the famed 1974 and 2008 bear markets [1] .

Unless you had exposure to the energy sector, it was tough to escape the carnage of 2022, as evidenced by the 33% decline of the tech-heavy NASDAQ 100 index. We certainly did not. In fact, our investments centered on the two worst-performing sectors of 2022 (technology and communication services) which were both down over 30% last year [2] . Ouch.

We begin this annual letter with some broader context because we want to highlight that drawdowns are not something you can avoid in financial markets. You can pretend to avoid them to appease investors (as the recent Bernie Madoff documentary highlights ever so starkly), or you can embrace volatility as the price of doing business. As a fund that invests on a multi-year time horizon with few worries about daily, weekly, or even quarterly price movements, we are comfortable holding stocks through bear markets. Over the many years we plan on running the Arch Capital Limited Partnership, you can bet there will be more down years like 2022.

Of course, our goal is not to lose you money. On a long enough time horizon, if we are right about the cash flow our portfolio companies will generate for shareholders and the competence of their respective management teams, the returns for our limited partners will take care of themselves. That is our north star.

For the rest of this letter, we are going to address three relevant topics for people interested in the fund: what we got wrong in 2022, what we got right, and where our focus lies as we march forward in 2023.

What We Got Wrong in 2022 (and what we can learn from it)

There were many things we got wrong in 2022. Frustratingly, a lot of our mistakes could have been avoided if we were more disciplined with our three main criteria when filtering investments (highlighted in our 2021 annual letter , which you can find on our website).

Our first mistake – and this is what accounted for the majority of the fund’s drawdown in 2022 – was our position sizing with stocks that traded at premium valuations. The stocks that contributed to the majority of the fund’s losses in 2022 (Spotify, Match Group, Wix.com, IAC) are generally companies where we are not betting on the durability of current cash flow but on the growth in free cash flow per share over the next few years.

We like the strategy of buying a stock with a time horizon of multiple years because it differentiates us from the majority of market participants who are basing their trading decisions on what will happen next quarter. Previously, our belief was that we should just ignore what could happen in the interim if we are confident in what the financials of a business will look like in the future.

We now believe this is an incomplete strategy and plan to remedy this mistake moving forward. Why? Because when you block out short-term risks and naively tell yourself you only care about the long-term, you can become blind to some obvious downside scenarios. This can then lead to foolishly sizing a position when, if you only did a little bit of analysis, you would have either kept the stock on your watchlist or made it a much smaller position size due to the likelihood of being able to buy shares at a 50% discount a few quarters later.

This does not mean we will now make investments based on quarterly trends with heavy portfolio turnover. But it does mean we will focus on near-term scenario planning to determine our position sizing. When risks start materializing for stocks with expensive earnings multiples, shares can start moving sharply downward, as we painfully experienced. Taking advantage of these price dislocations is much harder when you already sized the stock at 6%+ of your portfolio and much easier when it is 3% or less.

Another mistake we made in 2022 was a lack of discipline when identifying competent management teams. Based on our studying of businesses that produce durable above-market returns for shareholders, their management teams have three general qualities:

- They focus on building a culture that values all stakeholders, including shareholders.

- They spend money with return on invested capital ((ROIC)) and growth in free cash flow per share in mind.

- They are cost-disciplined both in good times and bad.

Within these three criteria, our largest miss was pairing our capital with management teams that have not shown to be cost-disciplined. This lack of discipline showed up in our underperforming stocks this year. Multiple times, we were able to identify these red flags, but either bought the stock anyways or failed to sell/trim our existing position. In the future, we are going to be more strict when deciding which management teams to trust our dollars with.

We will never completely avoid mistakes when making investments. But by analyzing what went wrong and why at the end of each year, we think we can continually improve our investment process.

What We Got Right in 2022 (and what we can learn from it)

So far, this letter has sounded negative. But there were things we got right in 2022, and we are very optimistic about what things will hold in 2023 and beyond if we keep implementing our strategy.

The most important thing we got right in 2022 was avoiding bullshit, plain and simple. What do we mean by this? Well, last year that meant a lot of things:

- We didn’t put the portfolio on margin (the investing term for taking out a loan to buy stocks). Using margin might make our returns look great during periods when the market is soaring, but would set us up for failure during bear markets like today.

- We passed on investing in companies with too much debt. Debt is not something we avoid completely. In fact, we thought very highly of our portfolio companies that took out extremely low-cost debt in 2020 and 2021 and are now returning that cash to shareholders at high free cash flow yields. However, companies with high leverage ratios in cyclical industries present great risks for permanent losses of capital, making them easy for us to pass on. There were plenty examples of this in 2022.

- We passed on hyped-up ideas that were deemed the “next big thing” like cryptocurrencies, NFTs, electric vehicles, the space economy, or SPACs. Our investment process is based on cash flow, growth, and management teams, not half-baked ideas with unsustainable – or in some cases non-existent – business models.

- We avoided management teams that commit fraud. The last few years have been deemed the “golden age of fraud” by many market participants, which we agree with. Plenty of frauds have been exposed in 2022, and plenty more will likely get revealed in 2023. We will do our best to avoid investing in these businesses by studying the techniques of fraudsters and how they tend to act/run their companies. Beyond fraud, we are also trying to identify red flags for management teams that are dishonest and/or misleading about their operations. These executives typically have the sole goal of enriching themselves, many times at the expense of shareholders. These are not the people we want to pair our capital with.

When running a portfolio, the most important thing is to minimize permanent losses of capital. This is true no matter if you are investing $1,000 or $100 billion. A permanent loss does not mean from short-term price movements, but from having to take a realized loss on an investment, either due to bankruptcy or forced selling. This year, many investors learned this the hard way.

Keeping our heads on straight through both bull and bear markets and having a conservative approach to portfolio management is the best strategy we know of for avoiding permanent losses.

Why is avoiding a permanent loss so vital? Because of the math of how percent losses work. From a Zacks investment blog [3] :

“The math of percentages shows that as losses get larger, the return necessary to recover to break-even increases at a much faster rate. A loss of 10 percent necessitates an 11 percent gain to recover. Increase that loss to 25 percent and it takes a 33 percent gain to get back to break even. A 50 percent loss requires a 100 percent gain to recover and an 80 percent loss necessitates 500 percent in gains to get back to where the investment value started.”

Second, another thing we got right in 2022 was having a balance between letting our successful investments appreciate in value and deciding to sell winners when forward returns were significantly reduced. We believe tons of investors hold themselves back by either leaning too much into the “I’ll never sell anything” camp or the “I’m going to sell anywhere above my price target” camp.

Yes, it would be ideal if we could just buy a stock at an attractive valuation and let it compound at 15% a year indefinitely. But that is not how investing works in reality. If a stock we own is up a significant amount in a short time period, which lowers forward expected returns, we will sell and deploy it into another opportunity we think has higher expected returns. This was perhaps our largest success in 2022 as we were able to sell a few strong performers like Sprouts Farmers Market and Harbor Diversified, sit on the cash, and then buy some stocks (in some cases the same stocks) that had fallen during the bear market to what we think were attractive prices.

The returns from these new purchases have not shown up in our consolidated performance yet, but we were very excited to purchase stakes in some high-quality businesses at dislocated prices.

Lastly, a small thing we got right in 2022 was implementing tax loss harvesting when appropriate. While simply a loophole set up by the U.S. government, using this tool increases the value we can provide to investors, which at the end of the day is the only goal we have. In the future, you can expect us to realize tax losses when appropriate in order to increase after-tax returns for limited partners.

Our focus for 2023

In 2023, there are two things we will be focused on outside of managing the existing portfolio.

First, we want to start building up a watchlist of the few dozen or so highest-quality businesses in the world. These are businesses that have clear and durable competitive advantages combined with competent management teams (among other criteria) that we would love to own at the right price.

Previously, we would take a look at these businesses and find things we liked, but then a lot of the time would end up discarding them due to valuation concerns. Now, instead of just immediately stopping our research when it is clear the valuation is going to keep us from taking a position today, we want to finish our analysis and then figure out at what stock price we would be willing to buy shares. This includes making a formal internal report, scenario planning, and logging our final decision on the watchlist.

Our hope is that over the next few years, we can compile a watchlist of 30 - 40 high-quality businesses we would love to own at the right price. Then, whenever one of these businesses enters into our predetermined buying range, we will be able to easily compare them to our least favorite existing holding and decide whether it belongs in or out of the fund at that time.

Price dislocations in individual stocks can sometimes happen quickly, with only a few weeks or even days to act. If you try to rush through the formal research, it can lead to irrational decision-making, the potential of which is already going to be elevated during bouts of volatility. We think performing the research first and then determining what price we would pay will lead to better decision-making than letting price movements dictate what stocks we research.

Moving on to our second focus. In 2022, we want to put more time and effort into finding deep-value stocks for the fund. Over the last two years, two of our more successful investments have been from stocks that are clearly not the best businesses in the world but traded at extremely discounted prices. In the future, instead of having 10% of our investments in deep value, it might grow to 25%. There is no artificial target that we have set, but it is likely that we will have a higher percentage of the fund in deep-value stocks than we did in the past.

Both high-quality and deep-value investing can work. Ultimately, it doesn’t matter whether something is classified as growth or value, we are just trying to find stocks that can provide the best balance of risk and return potential for the fund. However, we believe having investment flexibility gives us a higher chance of making rational decisions throughout all market environments.

Simply put, there are periods when it is tough to find opportunities in high-quality investing (2021) and other periods when it is tough to find opportunities in deep value (2006). But rarely do these periods happen at the same time. In the future, it is easy to envision a multi-year period where valuations again reach a premium for high-quality stocks. If that was all we focused on, it is likely that we would make sub-optimal investing decisions during that time period. Looking for opportunities across the investing landscape should help us to find stocks to buy in all market environments.

All in all, 2022 was a mixed bag for the fund. In 2023, we plan to learn from our mistakes and continue to improve as investors, which will hopefully translate into adequate returns for our limited partners

If you are interested in learning more about the fund, head on over to our website. And, as always, contact us with any specific questions you may have.

Sincerely,

Brett, Brady, and Ryan

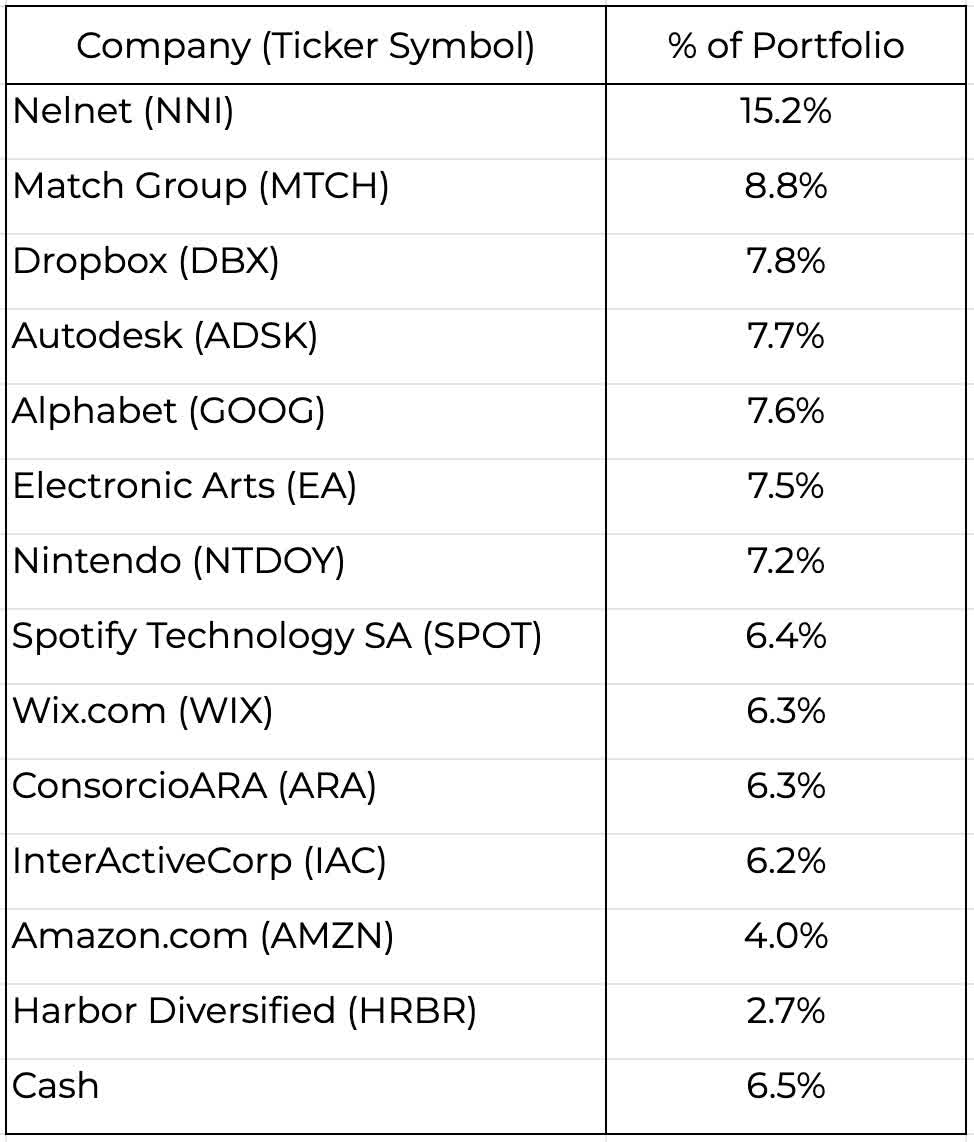

Fund holdings as of 1/23/2023

{kind=link}

Footnotes[1] 2022 Was One of the Worst Years Ever For Markets |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Arch Capital 2022 Annual Letter To Partners