ACGL - Arch Capital: A Specialty Insurer With Further Upside Potential

2023-11-15 01:32:28 ET

Summary

- Arch Capital Group has seen its shares rally over 50% in the past year, benefiting from a strong underwriting profile and higher interest rates.

- Recent results have been strong, with the company earning $2.31 in adjusted EPS, beating expectations, and experiencing strong growth in net premiums written.

- The company's underwriting profit has increased significantly, and it has also seen benefits from rising interest rates.

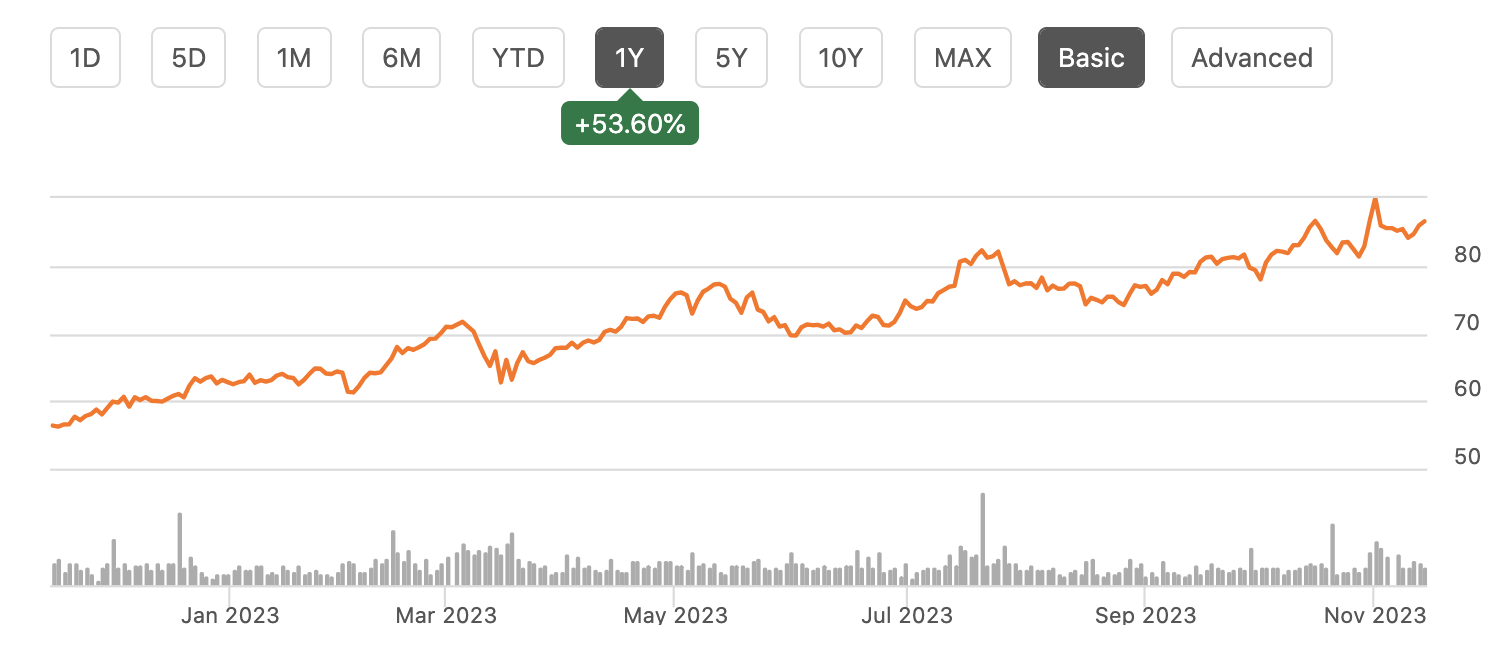

Shares of Arch Capital Group ( ACGL ) have been a tremendous performer, rallying over 50% the past year. This specialty insurer is benefitting from a strong underwriting profile as well as higher interest rates. Recent results have been especially strong, though there is likely to be some reversion in underwriting profitability over time. Still, with over $8 in earnings power and solid growth, the upside is not yet fully maxed out.

{kind=link}

In the company’s third quarter , Arch Capital earned $2.31 in adjusted EPS, beating consensus by $0.74, as underwriting results were spectacular. Arch generated net premiums written of 3.36 billion, up 23% from last year. This strong growth was driven by pricing gains, winning more policies from existing clients, and adding clients. Arch is achieving pricing gains north of 15%, in fact, on some policies. Higher inflation had weighed on insurance sector profits over the past year as it cost insurers more to settle claims, given increased cost to repair and replace property. That has resulted in a wave of price increases, which should improve future profitability.

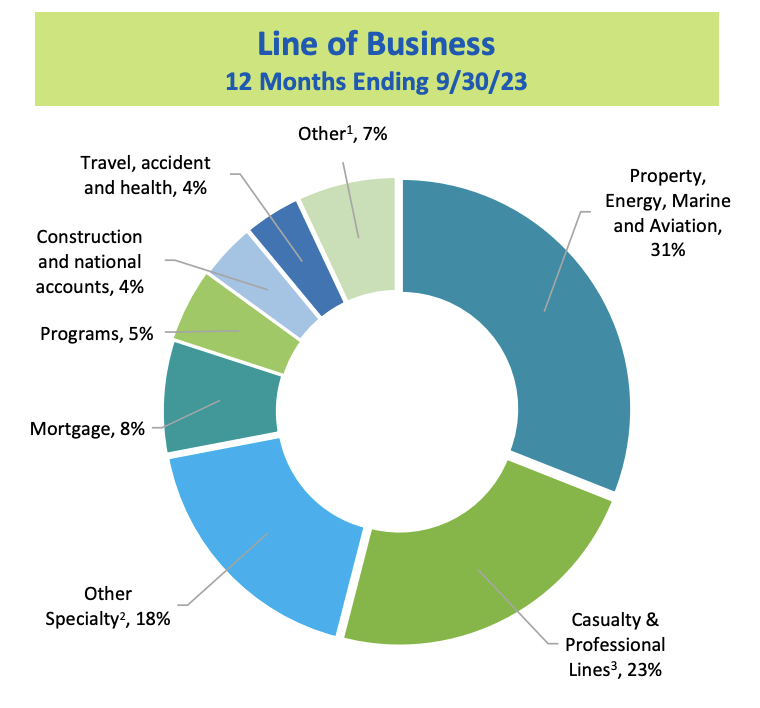

This “catch-up” is evidenced by the company’s combined ratio before catastrophes declined to 77% from 82.2% last year. Arch is essentially making $23 on every $100 of premiums it writes, a very wide margin. This is aided by the fact the company insures across a wide range of sectors, helping to diversify its exposures, and plays in niche sectors like aviation and marine that have fewer players and are less commoditized than sectors like auto insurance. Beyond sector, ACGL is also diversified across insurance types; over the past year, 49% of policies are reinsurance, 43% insurance, and 8% mortgages.

{kind=link}

Now, overall, Arch’s underwriting profit of $721 million last quarter was up 10x from $68 million last year. This includes both catastrophes and prior-year reserve adjustments. In Q3, Arch had net catastrophe losses of $180 million. Catastrophes were $551 million last year. In 2022, Hurricane Ian caused massive damages, leading to significant cat losses for the industry, and Arch was not spared from this. 2023 had minimal hurricane activity, by contrast. 2022 was worse-than-average season, but this year’s cat losses are likely to be better than the average we should expect. Because of the hurricane season, cat losses are typically concentrated in Q3. Due to this better quarter, year to date, they are down to $378 million from $719 million last year.

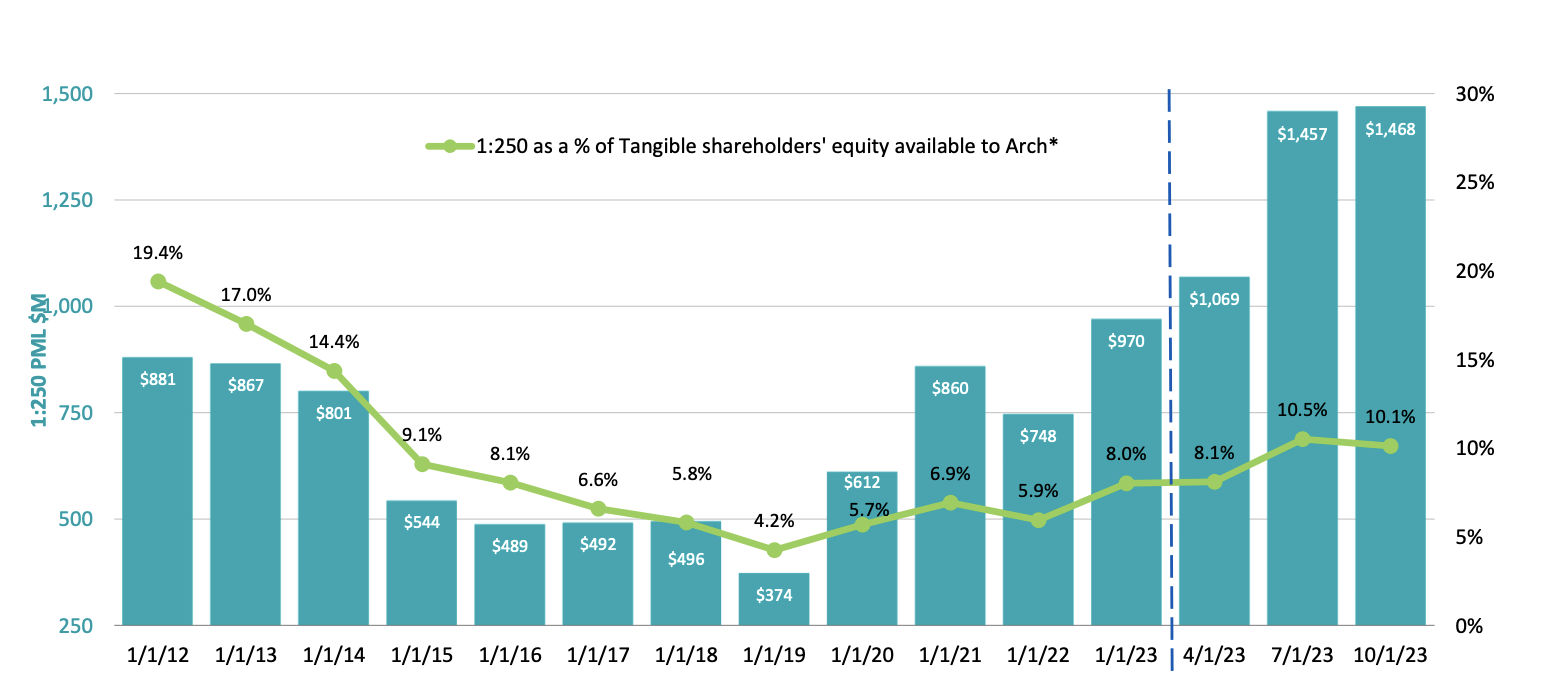

To measure catastrophe exposure, insurers look at 1:250 losses. This measures how large losses would be if a 1 in 250-year event were to occur. For Arch, that would cause about $1.5 billion in losses or about 10% of its shareholder’s equity. This share has ticked up since 2019 as cat-related policies have become more expensive, creating more profit margin. As such, Arch has reallocated capital towards this segment; still at 10% of equity, such losses would be manageable, though painful, and are much lower than levels from 10 years ago as a share of equity. Last year’s, Hurricane Ian was about 70% as bad as 250-year event, and the company managed through it relatively well. After all, it still turned an underwriting profit last year of $68 million. Given how bad Ian was, to still turn a profit speaks to the robustness of Arch’s underwriting. Bad storms will reduce profits significantly, but they are not solvency-threatening events.

{kind=link}

On top of lighter catastrophes, ACGL has also seen benefits from favorable developments on prior years’ reserves of $152 million. It can take time for claims on policies to materialize. Until a claim is filed or its insured exposure ceases, it is impossible to know the exact profits of each policy. As such, Arch, like other insurers, uses actuarial and modeled assumptions to estimate profits. These assumptions are periodically reviewed, and as more data is received, they are refined to better estimate profits with reserves added or removed. When ACGL completed this exercise, it found it had $152 million more set aside than necessary; in other words, policies have been outperforming expectations, good news for shareholders.

Drilling deeper into results, in its insurance segment, its adjusted combined ratio improved to 89.1% from 89.5%. Cats contributed a further 2.6% from 13.4% last year, due to Hurricane Ian. Net premiums written rose by 11.2% in this segment.

Its reinsurance unit swung to a $310 million profit from a $197 million loss as its catastrophe losses were just 9.3% from 39.1%. More of its catastrophe exposure sits here vs its insurance unit. Its adjusted combined ratio was 73.5% from 85.5% last year. Premiums surged 45% to $1.56 billion as it retained 73% of gross policies from 66% last year. Rate increases and mix shifts are also helping support underwriting profits. After Ian, some insurers have pulled back, and Arch has been allocating more capital to this segment, enjoying better pricing power given the lack of competition.

Finally, Arch has a smaller mortgage unit, which provides private mortgage insurance. In the US, its insurance mortgage balances beyond the 80% of the purchase price that Fannie and Freddie do, as well as operate in foreign markets like Australia. Here, it had 33.5% of favorable reserve adjustments, bringing its combined ratio to below 5%. Excluding this, it was 38%, which is still incredibly low, considering 17% of this is the cost to do underwriting on policies, have employees to process claims, etc.

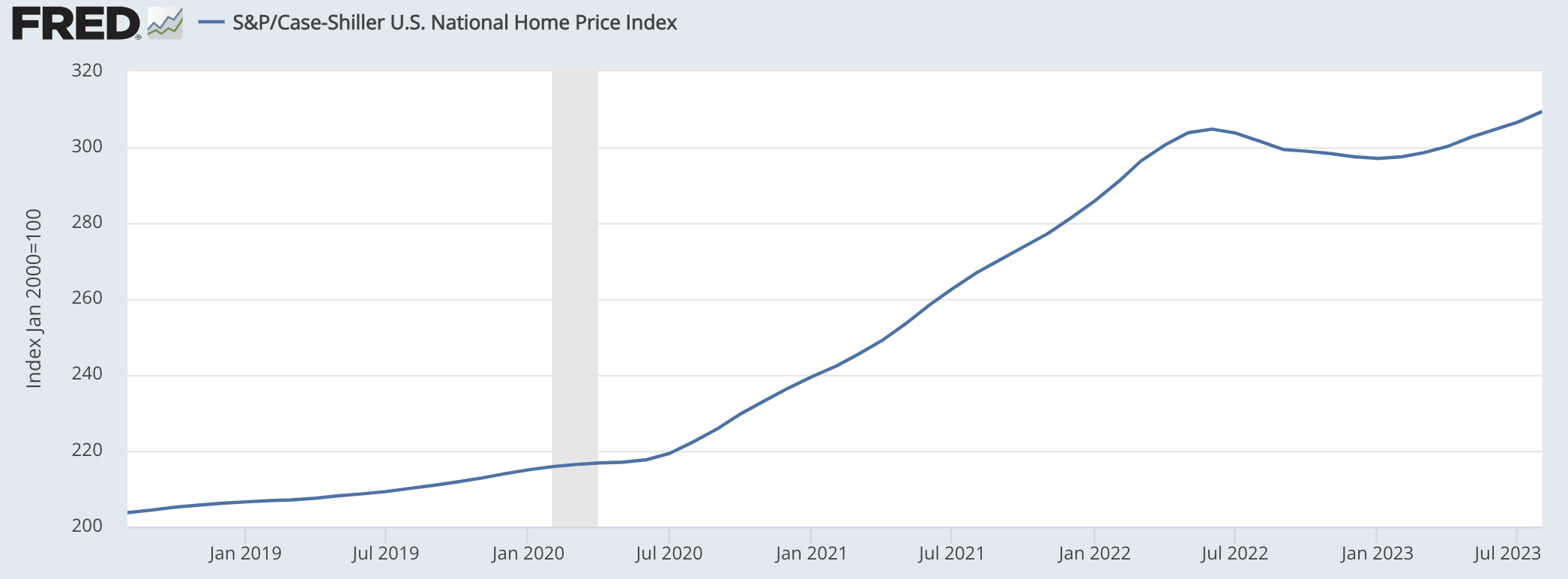

As I have written on pure-play mortgage insurers like Radian ( RDN ), this business is incredibly profitable right now because home prices have risen so much. Home prices have risen by more than 20% since the end of 2020, so even if an owner cannot afford the mortgage, they can sell their house for more than the mortgage balance and pay it off with no losses for ACGL. This business only struggles when people default and home prices are lower. Given both buoyant prices and a low unemployment rate, this business is incredibly profitable. I was glad to see Arch add exposure here via a small, bolt-on acquisition .

{kind=link}

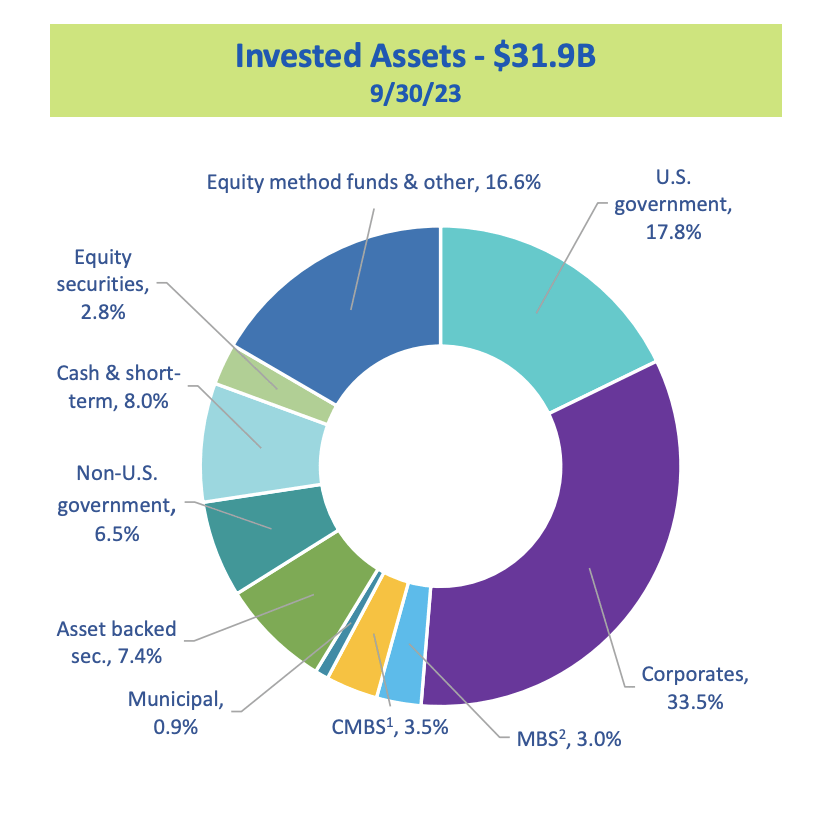

Beyond strong underwriting, Arch is benefitting from higher interest rates on its investment portfolio. Net investment income in Q3 more than doubled from $129 to $269 million. Equity method income was a further $59 million. The $32 billion investment portfolio’s after-tax yield has risen to 3.18% from 1.46% last year.

As you can see below, this is a diversified, high-quality portfolio, primarily in fixed income. 45% of its fixed maturity portfolio is US government or “AAA” rated. A further 28.5% are A or higher. Arch takes a bit more underwriting risk, via its reinsurance arm, than some peers and accordingly maintains a low-risk, highly liquid investment portfolio.

{kind=link}

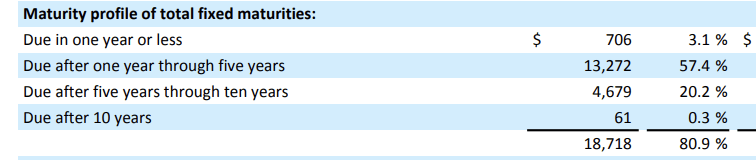

This portfolio is benefitting from higher rates as it reinvests bonds bought when rates were much lower into those with today’s yields. Most of its portfolio matures in 1-5 years, and so assuming the forward curve plays out, net investment income should gradually rise. On top of this, the remaining 19% of its fixed income portfolio are mortgage and asset-backed securities, which amortize, meaning that each month they repay some principal, which can be invested at higher yields.

{kind=link}

ACGL is also growing as net premiums written exceed the claims it is paying out. Insurance reserves are up $2.55 billion to $21.8 billion so far this year. With these premiums, it can buy bonds at today’s high yields. In the past year, it has generated $4 billion in operating cash flow, which has deployed at over 5% on average, contributing to over 20% growth in its investment portfolio. ACGL generates a solid underwriting profit on policies it writes, and in the meantime, it now earns over 5% per year on incremental premiums, which combine to make the company extremely profitable.

Shares do trade at 2.2x book value of $38.62, but the company is also generating a 24.8% adjusted return on equity. That still translates to an 11.3% return on its market value. This is partly because the true present value of its insurance reserves liability is less than its accounting value, given the profits ACGL generates on its underwriting. This is also why P&C insurers in general trade at substantial book value premiums.

If we assume no more favorable developments on past reserves and that catastrophe losses over time average between Q3 2022’s difficult level and this year’s light level, ACGL has about $1.9-2.00 in quarterly earnings power or $7.70-8/year. That gives shares just a 10.8x multiple. However, investment income is also rising as interest rates are higher, which should conservatively be a $0.25-$0.40 tailwind. Additionally, with its strong premium growth, core earnings can continue to rise at least 10% as it deploys more capital and grows its investment portfolio.

Given these factors, I expect ACGL to generate at least $8.40 in earnings over the next year. As it does have reinsurance and catastrophe risks, shares will structurally have a lower multiple, but as it continues to generate profitable growth, I do look for its multiple to reach about 12x, providing upside to about $100 over the next year. Shares may not rise another 50%, but with at least 16% upside, I would continue to buy ACGL.

For further details see:

Arch Capital: A Specialty Insurer With Further Upside Potential