ARCH - Arch Resources: Cheap And Doing The Right Thing

2023-03-27 16:16:23 ET

Summary

- Arch Resources, Inc. is spending a modest amount on maintenance CapEx.

- Otherwise, it is committed to returning 50% of cash flow to shareholders through dividends.

- The other 50% gets returned through lumpy buyback programs.

- The immediate outlook is mixed, but given the Arch Resources valuation, there's some room for error or bad luck.

Arch Resources, Inc. ( ARCH ) produces thermal and metallurgical coal in the United States. The company trades at a market cap of around $2.27 billion and an enterprise value of $2.19 billion because it has a net cash position. Coal prices have declined some from their highs, but they're still above pre-pandemic levels.

Analyst estimates for earnings for next year have been adjusted back upwards since my last article and are now at $25 per share:

Cyclical, unfortunately, tends to get smashed in recessions. With all the banking turmoil, the probability of running into one soon is rising. However, as we'll get into later, Arch isn't spending on CapEx, and I believe that's a trend in the coal industry due to ESG pressures.

In the previous quarter, management said (emphasis mine):

we can buy back as much as a million shares, or maybe even slightly more, slightly more as we go through Q4.

Unfortunately, according to the latest earnings call , Arch only took out 690k shares:

As you can see, we clearly followed through on those expectations, deploying nearly $352 million during the quarter. That breaks down as follows; $192 million of dividends paid, $101 million to repurchase nearly 690,000 shares, and finally, $59 million to retire convertible bonds.

I would have loved to see them come through with a million. However, it is still 3.3% of their shares in one quarter. Not to mention, the company paid a 6% dividend in the same quarter and retired most of its convertibles. According to management, it was advantageous to prioritize taking out the convertibles because it would otherwise have resulted in buyback offsetting dilution:

That's principally because absent the steps we took to settle the bonds, we would have incurred additional dilution, stemming from the 2022 dividend payments because those payments result in an increase to the conversion rate for the convertible bond holders. That's why in a nutshell, we prioritize the settlement of the convertible bonds rather than share buybacks at the launch of the return program. We knew that in doing so we would not only reduce the diluted share count at the time of the bond repurchases, but that we would also avoid the additional dilution resulting from the dividend payments throughout the course of the year.

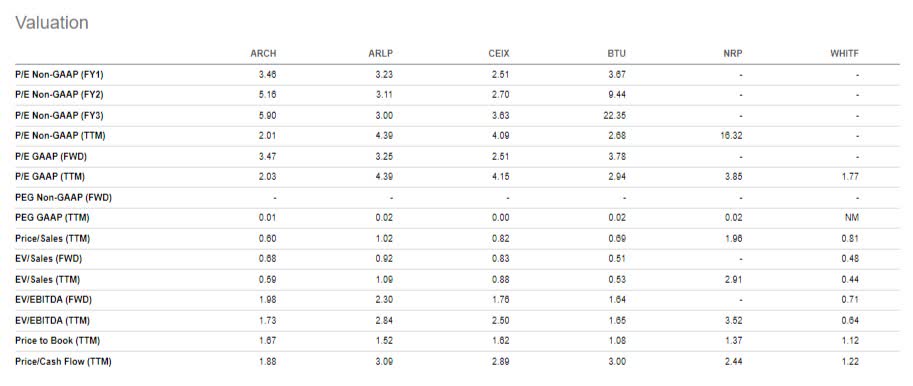

I have researched the valuations of various coal producers with similar market capitalizations using data from Seeking Alpha. These companies are primarily focused on either metallurgical or thermal coal production. Metallurgical coal is generally considered to have a longer-term future but is more susceptible to demand fluctuations due to the cyclical nature of the steel industry. On the other hand, thermal coal demand is steadier due to the stability of electricity demand.

Among these companies, Arch stands out as undervalued across several metrics. In my opinion, critical multiples such as P/Es, EV/EBITDA, and others generally point to Arch trading in line. Despite institutional investors deeming the coal sector uninvestable, I believe that coal companies' future cash flows are universally overly discounted. If prices don't plummet soon to stay there for a long time, investing in Arch or its competitors becomes significantly less risky due to the high levels of free cash flow and low debt.

{kind=link}

Where Arch stands out is on price to free cash flow. That's not a coincidence because the management still appears to be focused (and I love it) on returning cash flows to shareholders. There is no talk of investing for growth:

Before turning the call over for questions, I wanted to provide some brief comments on a few of the financial guidance items in the release. First, our capital spending this year will be in the range of $150 million to $160 million and consists entirely of maintenance capital with over 80% of that related to the Core Metallurgical segment. Despite the inflationary environment, we have maintained the capital guidance in line year-over-year.

The cash flow is still unencumbered by taxes due to substantial NOLs. Unfortunately, these are going to run out next year.

I mean, right now David, I think the way the program is set up for the allocation model, we're going to stick with 50% of the discretionary cash flow to dividends, it's very simple, people understand it. Absent working capital changes, it's very simple.

When talking about the lumpiness of buybacks, management is effectively saying we're going to return 100% of capital. Just not consistently every quarter:

David, it's a fairly simple formula, but as Paul said, we're going to -- because we paid the dividend in arrears and the way we pay it, it's going to be lumpy, but our general view is 10 quarters from now, when you look back over what's been paid out for the first 50 to second 50. They're going to be relatively equal, because again, it's just math.

One last comment from the call I wanted to highlight is the following:

Importantly, and as Paul noted, the coking coal books Asian waiting continues to increase as well. During the course of 2023, we signed first-time commitments with seven leading steel producers in Asia that we could easily foresee becoming stalwarts in our contract book long-term. That's important of course, because Asia is almost certain to be the primary growth driver for steel production over the next several decades. By becoming part of these steel producers coke making blends and demonstrating the tremendous value in use of our high quality coking coal products, we are building a strong, durable and beneficial outlet for our future metallurgical output.

This is setting up the long-term cash flows of the company. Cash flows the market isn't exactly giving much credit for, given the company is trading at ~3.5x forward earnings. Having said that, a recession is going to arrive sooner than later given the inverted yield curve and these banking tremors. But it seems to me the price and the balance sheet are good enough to get through one. There are other important factors apart from whether we see a recession soon. Just recently , Freeport received permission to restart another train at its LNG export terminal. This increases gas exports from the U.S. which tends to help coal prices.

For further details see:

Arch Resources: Cheap And Doing The Right Thing