ARCH - Arch Resources Delivers On Capital Returns

Summary

- Arch Resources had a tremendous 2022, generating over $1B in cash despite numerous headwinds.

- Going into 2023, coal pricing remains elevated and Arch is in a strong position to return capital to shareholders.

- I estimate 2023 free cash flow of $1.3B for Arch based on current coal prices, a yield of nearly 50%.

On February 16th, Arch Resources ( ARCH ) reported Q4-22 earnings , completing a year in which they generated over $1B of cash and transformed their balance sheet. A year ago, it seemed clear ARCH was on track to outperform street expectations, which they did handily despite coal volumes disappointing in 2022 due to poor rail service. So, what has changed for ARCH a year after KCA's prior write-up? ARCH's stock has appreciated 60% and paid out over $25 of dividends to shareholders, yet trades for approximately the same enterprise value thanks to substantial debt paydown and share repurchases.

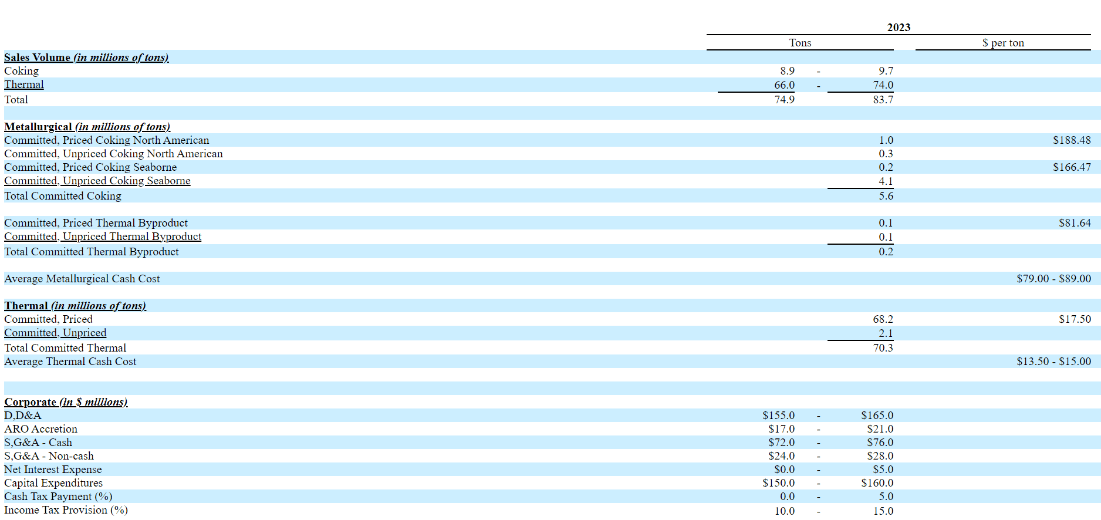

FY23 Outlook

{kind=link}

ARCH provided the above guidance for FY23, with both costs and volumes improving over the prior year. Using the midpoints, and assuming ARCH stock sells their unpriced tons for $220/ton (met) and $100/ton (thermal), we get the following estimates:

-

9.3*(215-84) + 70*(20-14.5) = $1.6B coal cash EBITDA

-

Less $300m (cash SG&A, CapEx, ARO funding, cash taxes)

-

$1.3B of FY23 Free Cash Flow ((FCF))

-

Current street estimates are for ~$700m of 2023 FCF

Meanwhile, ARCH has the following Enterprise Value (EV) build:

-

17.5m shares issued and outstanding (@$155) - $2.7B

-

Less $100m net cash

-

Asset Retirement Obligation ((ARO)) = funded

-

1.2m warrants @ $57 exercise less dividend payments = +$150m net impact

-

$60m net convertible outstanding offset by $62m " Capped Call " = neutral

-

Total $2.75B EV

-

1.3/2.75= 47% FCF yield

Return Profile

Assuming ARCH hits the above guidance, they have clearly communicated how they plan to proceed: 50% of cash returned via dividends and the remaining 50% for buybacks and debt reduction. $650m of cash dividends over 17.5m shares translates to a $37/share dividend for the year (ignoring repurchase impact), and $650m of share buybacks would be 20-25% of the outstanding shares near current prices.

Assuming buybacks at $200/share for some conservatism, ARCH would finish FY23 with about 14m shares outstanding. If met coal realizations significantly moderate to $150/ton and thermal earnings drop 50%, ARCH would likely earn $500-700m of FY24 FCF and have a 4x cash flow multiple if trading at $200/share. Cash taxes will be a headwind beginning in 2024, and I expect a 10-15% drag on cash flow based on Management comments on the Q4 call.

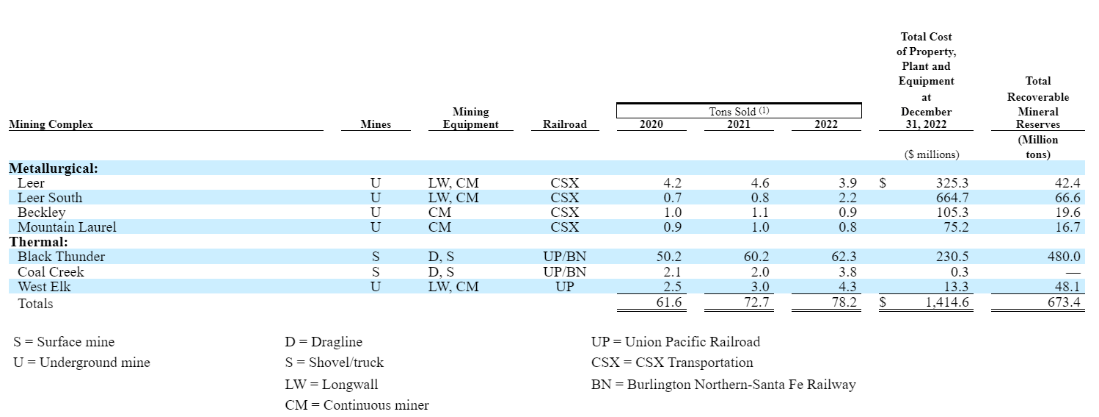

The upside case is obvious if pricing remains strong or increases - $200-300 longer-term realizations on met coal will allow ARCH to buy back the majority of their shares in the next 3-5 years if the stock does not re-rate significantly higher, and dividends will become more substantial if the share count decreases swiftly. ARCH's 145m tons of met coal reserves and substantial remaining thermal asset base could produce many multiples of their current EV even at significantly reduced prices:

{kind=link}

This reserve base was actually revised UP over 6m tons from FY21 due to substantial increases in the recoverable coal at Leer South, even after accounting for FY22 production. Higher met prices come with the added bonus of making production more economical for longer.

Risks/Common Concerns

1. Didn't ARCH guide to much lower costs and much higher production in 2022? Why trust them now?

They guided to nearly 10m tons of met sales (7.83m actual) and 75m tons of thermal (70.44m actual) last year before missing both due to rail performance and labor challenges, while also overshooting their cost expectations with volumes down and inflationary pressures. Hopefully, the new guidance better captures these prior headwinds, aided by Curtis Bay remaining open after being closed for the majority of 2022 . Rail service was significantly better in Q4 for met and YTD Q1, an encouraging sign. ARCH dealt with more rail issues than peers, so there may even be more upside for them in 2022 as they have more room to improve on prior performance.

2. Coal prices are going to collapse, yes? Have you looked at a natural gas chart lately?

ARCH would need to completely halt thermal operations and realize met prices close to $100/ton for cash flow to turn negative. Even in the depths of Covid, met coal prices held above $100/ton. Results will depend on spot pricing, given ARCH doesn't contract the majority of their met tons, but almost all their thermal book is priced for 2023. Met coal has been strong in the face of a weak 2022 steel market , so unlike thermal coal , I think pricing will prove more resilient than some expect.

3. ARCH trades at a 2x multiple of cash flow, just like last year. This stock isn't going to re-rate.

The key question for incremental buyers at $155 is - will the stock continue to trade at a 2x cash flow multiple if earnings contract, or is significant regression baked into the current price. As stated above, the stock currently trades at a 4x multiple of street estimates, but a 2x multiple of my estimates based on company guidance. A 2x multiple of street estimates ($700m) would push the share price back towards $100.

Here's my key takeaway: as long as ARCH persists in trading at a 2x multiple of cash flow and continues their policy of buying back shares with half their cash flow, they can continue to reduce outstanding shares 20-25% per year. This would result in ARCH having 4-5m shares outstanding in 5 years. Even if FCF contracts to $500m in year 5, ARCH would pay a $50-60/share annual dividend and trade at $200-250/share at a 2x multiple. You probably need a strong belief that long-term met coal pricing will remain under $150/ton to think the above scenario won't work out well for long-term investors.

4. ARCH is fine but (insert other coal stock) trades at a more attractive cash flow multiple.

When searching for a reason not to own ARCH, perhaps the best would be finding a more attractive coal producer. I prefer ARCH for its majority Met exposure, history of capital returns, Management, US asset base, and low-cost profile. I don't shy away from other analysis, but rather encourage each investor to review the alternatives that exist before investing in ARCH.

-

It seems as though more people are constructive on Peabody Energy ( BTU ) than any other name in the coal space, and plenty of bullish pitches are available for your perusal . The stock is up more than 20x from Covid lows and has done very well for holders. My reasons for caution with BTU center on Management, surety overhangs, declining Newcastle coal prices, and Australian government pressures, though many have gotten comfortable with these. Surety renegotiation may prove to be a catalyst in the near future.

-

The largest US Met producer is Alpha Metallurgical Resources ( AMR ), who has been profiled many times recently as well. AMR has higher costs than ARCH, but in an elevated pricing environment should earn more cash .

- There aren't many "growth" plays in coal, but the best mine project currently underway is owned by Warrior Met Coal ( HCC ) - Blue Creek. Their CapEx will be a drag on near-term cash flow, but the mine is expected to have some of the lowest costs and highest quality coal upon completion.

5. I see that ARCH is over 10% shorted, does someone know something?

ARCH's short interest has come down in 2022 and was a byproduct of their convertible note and capped call transactions. I would expect it to further decrease after these positions are unwound.

6. What if there is a significant mining accident at one of ARCH's properties?

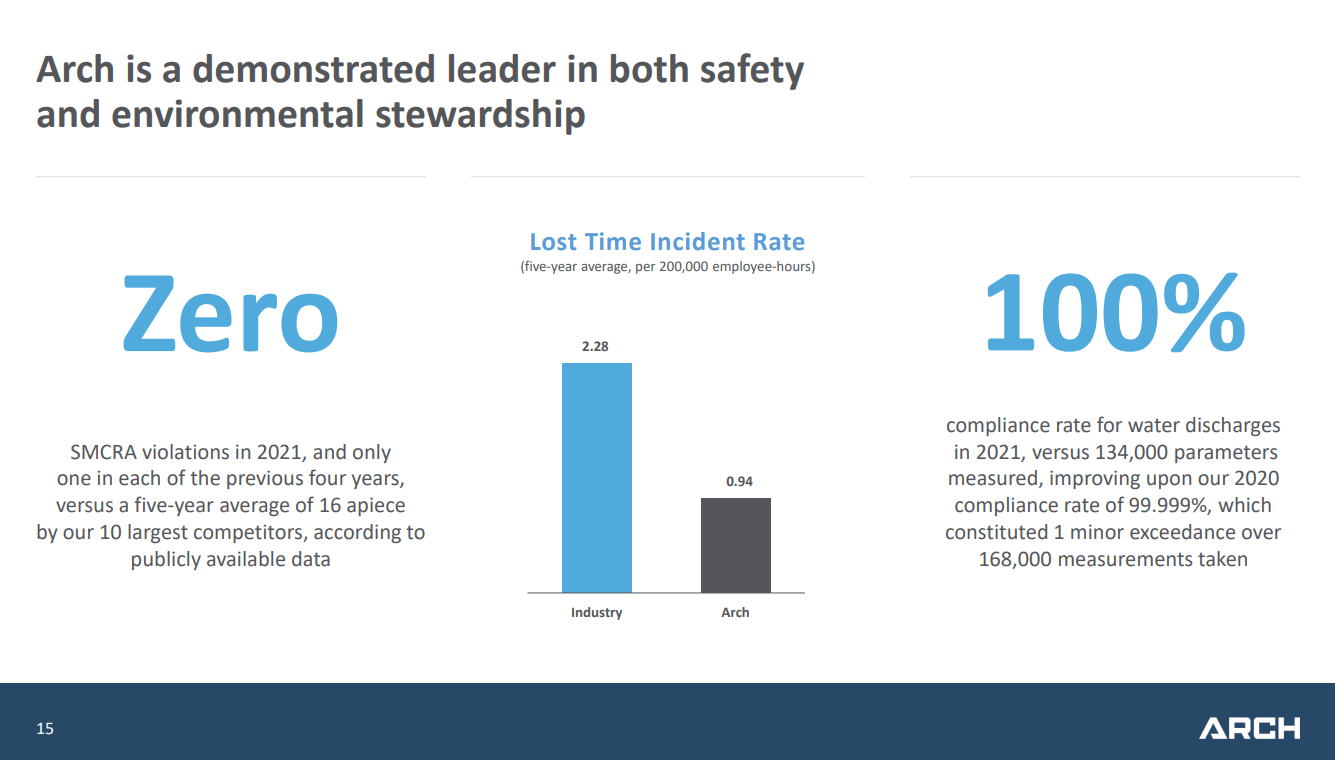

This is always a risk with mining businesses. ARCH boasts a fairly strong safety/environmental record , but accidents do happen.

{kind=link}

Conclusion

Arch Resources has delivered on expectations for significant capital returns, with the business well-capitalized and spewing cash. If the stock continues to trade at 2x cash flows, their capital allocation structure will allow them to repurchase half the outstanding shares every couple of years and significantly increase the dividends paid to remaining shareholders. I like their priorities and chances of significantly topping expectations in 2023, and I continue to be a very satisfied shareholder.

For further details see:

Arch Resources Delivers On Capital Returns