ARCH - Arch Resources: Good Valuation And 100% Of Free Cash Flow Being Returned To Shareholders

2023-12-05 15:13:14 ET

Summary

- Arch Resources has seen a strong performance lately due to a rebound in coking coal prices.

- Q3 financials were slightly weaker compared to Q2, but improvements are expected in Q4 and 2024.

- The stock is attractively priced, with the free cash flow yield estimated to be roughly 15-20% for both 2023 and 2024.

Investment Thesis

I covered the coal mining company Arch Resources ( ARCH ) during the summer of this year, I also added the stock to the portfolio a few days after the publication, as mentioned in the comment section of that article.

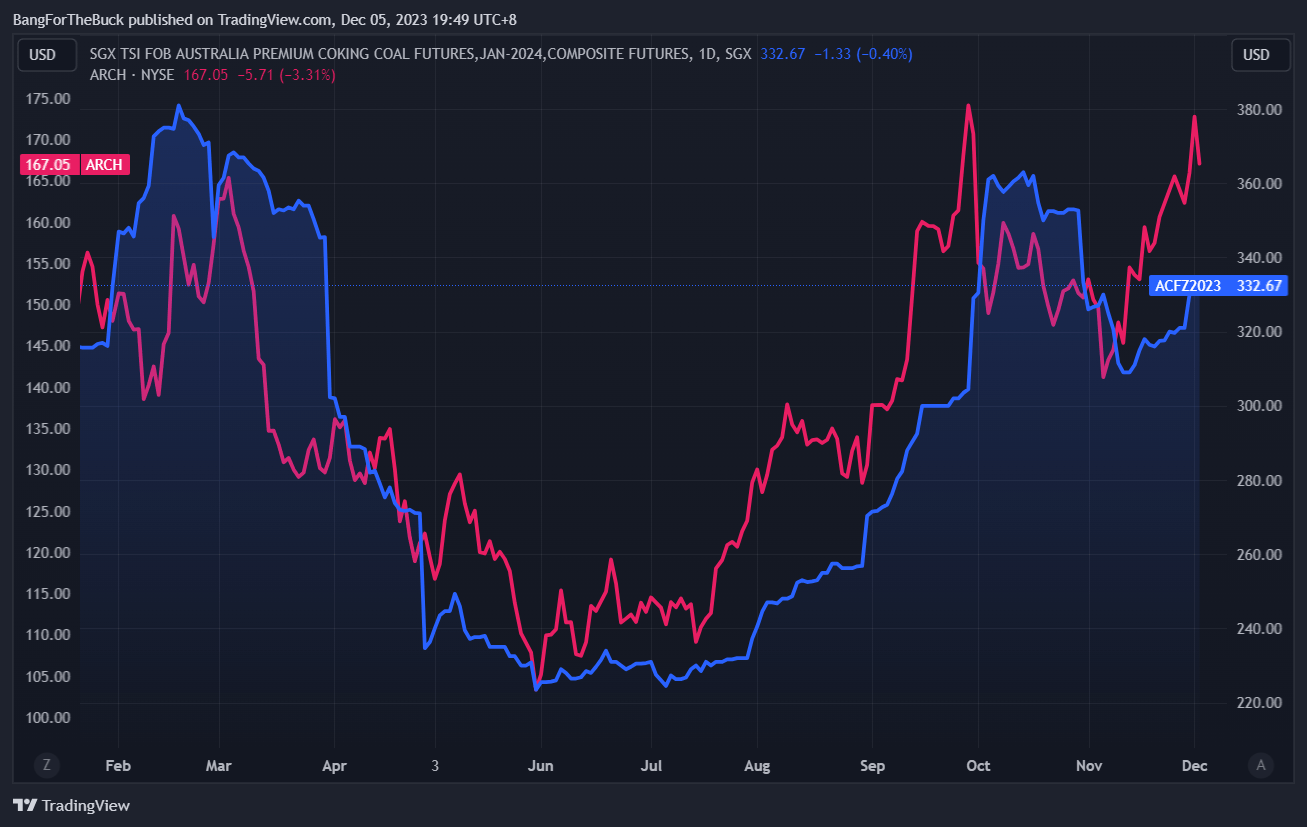

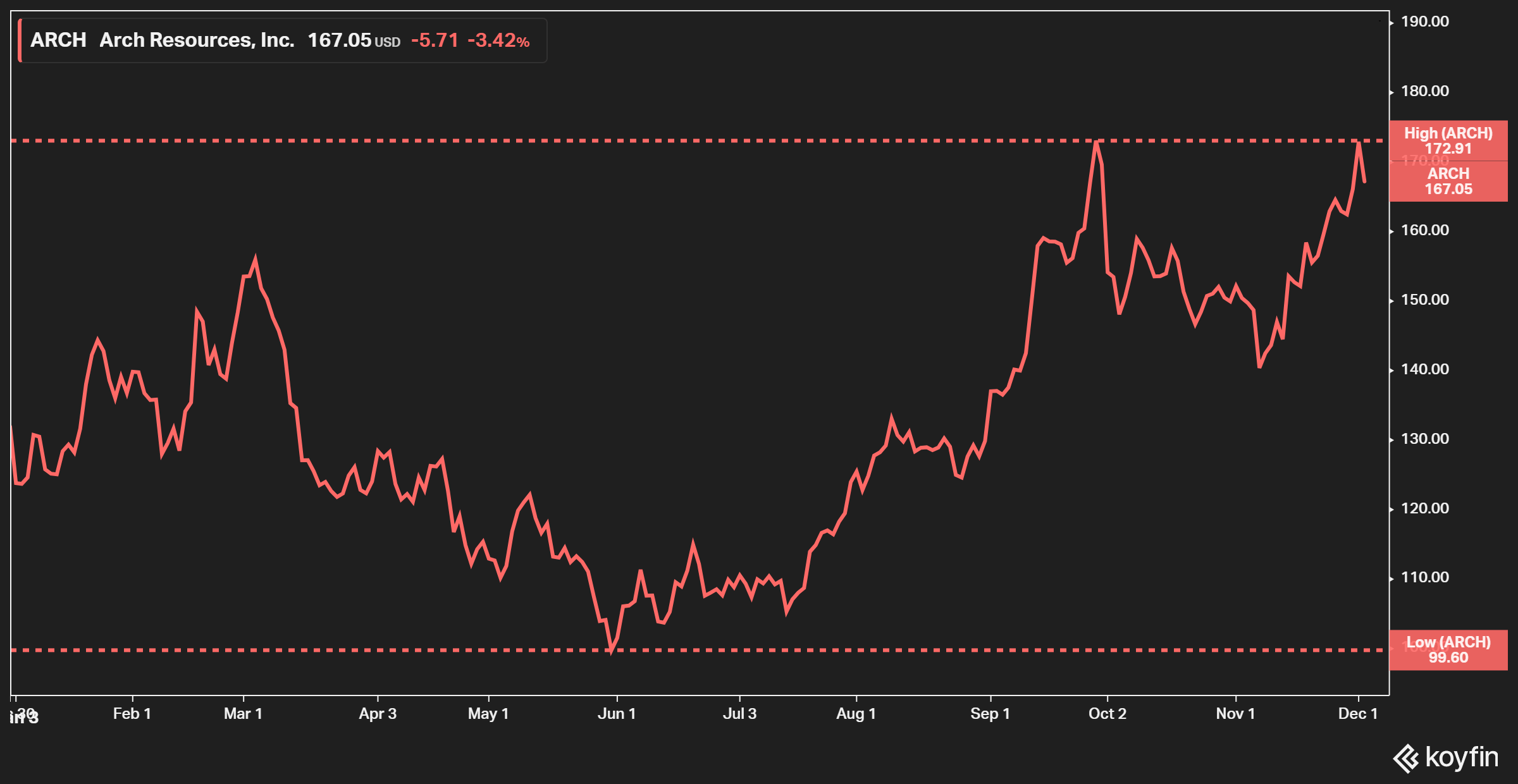

Arch has had a strong performance since the lows this year, which is primarily due to a very healthy rebound in coking coal prices.

Figure 1 - Source: TradingView

{kind=link}

The company published its Q3 results in late October, which this article will partly be about, together with a focus on the attractive valuation.

Q3-23 Result

Arch reported $745M in revenues during Q3, adjusted EBITDA was $126M, and the net income was $74M. Despite a nice rebound in coking coal prices lately, the financials were slightly weaker compared to Q2. The company did downwardly revise the annual production guidance in early October, following some operational challenges at the Leer South Mine, so the slight weakness in Q3 was not a surprise.

As usual, the company did produce a fairly large amount of thermal coal in the quarter but given the much higher margin in the metallurgical ("MET") segment, the majority of adjusted EBITDA comes from the MET segment.

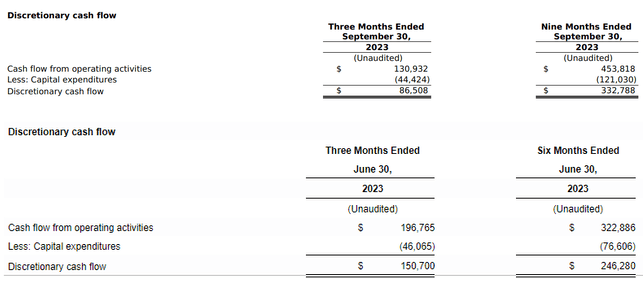

The free cash flow or discretionary cash flow in Q3 was $87M, that is down significantly compared to Q2's $151M. A somewhat lower production volume and higher costs in the quarter are part of the reason for a weaker free cash flow. The Q2 free cash flow was also boosted by some working capital adjustments, which were not present in Q3, that inflated the number slightly in Q2.

Figure 2 - Source: Arch Q2-23 & Q3-23 Press Releases

{kind=link}

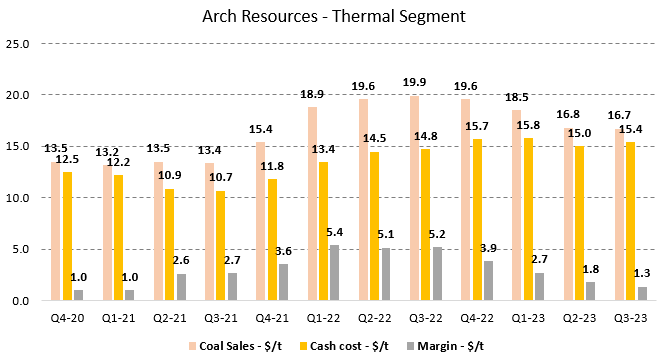

The margin in the thermal coal segment has continued to decline in Q3 compared to the prior quarter. The contribution to the bottom line from the thermal segment is quite low, but the recent weakness has had some impact on overall earnings and cash flows. We know the company has been dealing with some operational issues lately in both the thermal and MET segments, with the expectation of improvements in Q4 and 2024. So, I would not read too much into the decreasing margin.

Figure 3 - Source: Quarterly Reports

{kind=link}

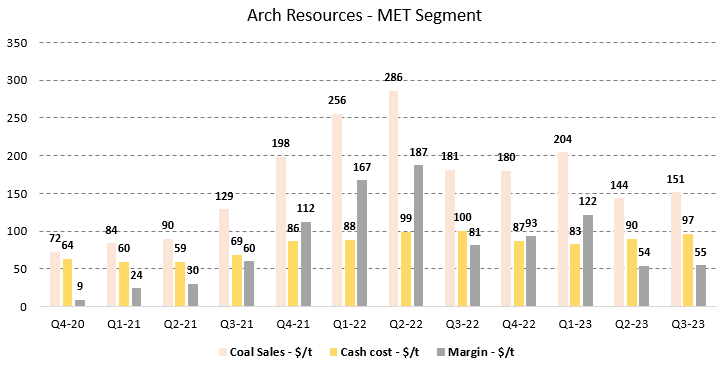

The MET segment did deliver a $55/t margin in the most recent quarter, which is a very marginal improvement compared to the prior quarter. However, that is still a relatively soft number compared to what we have seen over the last couple of years, and given where coking coal prices are currently trading, Q4 is likely to see a substantially improved margin.

Figure 4 - Source: Quarterly Reports

{kind=link}

Valuation

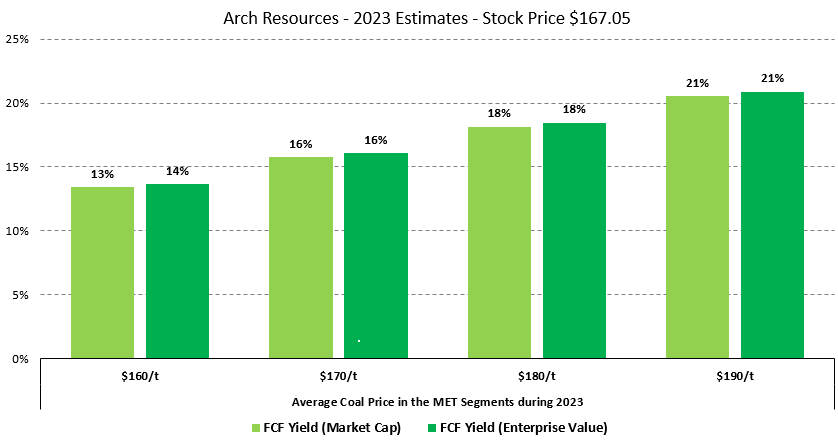

Arch Resources has had a few challenging quarters lately, with some operational issues in the various mines, that are expected to improve going forward. The weak coking coal prices during the summer have also impacted the annual result. Having said that, the stock price has had a nice rebound lately, and the valuation for 2023 continues to look very appealing, where the 2023 free cash flow yield is estimated to be around 16-18%.

Figure 5 - Source: My Estimates

{kind=link}

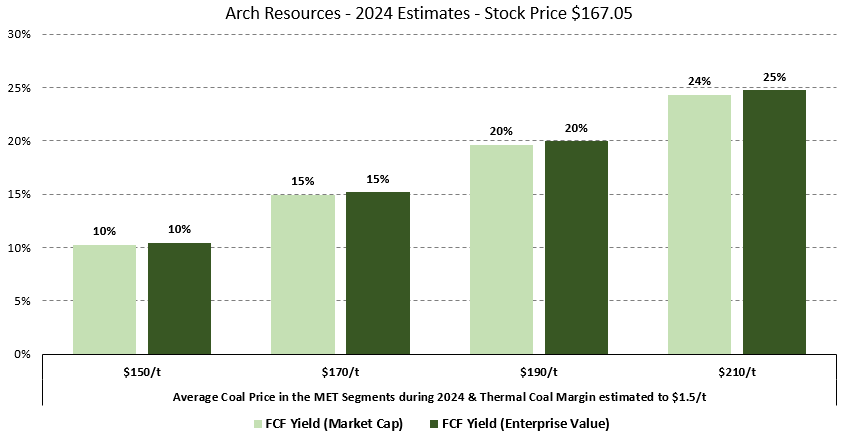

For 2024, in the thermal coal segment, I have assumed a 10% reduction in both the production volume and the margin compared to 2023. In the MET segment, I have instead assumed a 5% increase in the production volume, with costs unchanged compared to 2023. With those assumptions, we get the following valuations for Arch in 2024.

Figure 6 - Source: My Estimates

{kind=link}

The realized price for Arch in 2024 will depend on fluctuations in coking coal prices during the year, to some extent thermal prices as well, even if sales in that segment are made on slightly longer contracts. So, the 2024 valuation will primarily be based on how aggressive you want to be regarding coking coal prices going forward, but I do think a free cash flow yield in the 15-20% range is not an overly aggressive estimate.

Conclusion

With Arch having performed well over the last six months, it might be prudent to wait for at least a smaller correction before buying or adding to Arch, but the stock is very attractively priced in relation to current coking coal prices.

{kind=link}

The company has announced a slight tweak to the capital return policy, where 100% of free cash flow or excess cash flow will continue to be distributed to shareholders. However, going forward, 75% will be in the form of buybacks and only 25% will be in dividends. The strong performance of Alpha Metallurgical Resources ( AMR ) has likely influenced this decision.

So, with more aggressive buybacks going forward, I would expect future corrections to be shallower than in the past. We can also expect more shares to be repurchased going forward, because part of the buybacks have in the past gone to retire convertibles and warrants, instead of common shares.

For further details see:

Arch Resources: Good Valuation And 100% Of Free Cash Flow Being Returned To Shareholders