ARCH - Arch Resources: Long-Term Cash Cow

2023-06-16 13:43:21 ET

Summary

- Arch Resources delivered a positive Q1 adjusted EBITDA of $276 million confirming a solid 2023 outlook.

- The company declared a quarterly DPS of $2.45, confirming to be a shareholders-friendly company.

- Arch Resources' buy rating is confirmed at $175 thanks to a supportive valuation on an EV/EBITDA lower than 2x.

Last year, we started to analyze Arch Resources (ARCH) swallowing our environmentalist pride and deciding to rate the stock with an overweight. We left our readers with a key question: " Is it our responsibility as investors to invest in the change we want to see in the world?". After our Glencore analysis (we are currently up by 18%) called " M&A Risk Offers A Possibility To Enter ", we decided to review our Arch investment thesis on the back of the latest potential M&A in the coal segment. Here at the Lab, even if our internal team recognized that this coal environment won't last, and Wall Street's current market dislikes corporations such as Arch Resources, we still believe that the company could sustain long-term shareholders' return. Why?

- Very briefly, the company delivered Q1 adj. EBITDA of $276 million excluding a minor positive one-off of $1.5 million compared to Wall Street estimates of $264 million. Metallurgical coal, the output used to make coke (a vital part of steel making manufacturing process) reported sales price per ton at $204, while Thermal coal, the output mainly used for heating, was sold at an average of $82.66. On the volume side, the company managed to beat consensus estimates and this is a key point of the coal resiliency despite a non-friendly market;

-

Looking ahead, 2023 metallurgical coal forecasts were confirmed, while thermal coal output targets were slightly reduced. This is due to the West Elk mine and is not coming as a surprise. In addition , this is also evident in the oil environment , global coal CAPEX investments continue to exhibit a lack of investment and both Canada and the USA continue to modestly increase export despite higher coal prices. However, this is very supportive of Arch Resources;

-

Related to point 2), we are applying these changes in our 2023 estimates: 1) we are lowering thermal coal volume from 66-74mt to 64-70mt, while 2) metallurgical coal volume remains unchanged. On a cost basis, given the management comment, we slightly increased thermal cost expenses from $14.50 to $15.0 per ton. While CAPEX is left unchanged at $150 million;

-

Looking at the Q1 update, the company declared a quarterly total DPS of $2.45. This is structured on a $0.25 regular dividend plus a $2.20 special dividend. This was above Wall Street estimates of $1.92 per share. The company also repurchased 131k shares which is equivalent to 0.6% of Arch's shares outstanding. More important to emphasize is that the company has a $322 million repurchase authorization. In addition, the company repurchased $58 million in convertible securities, reducing future dilution by approximately 423k stocks (circa 2.0% of shares outstanding);

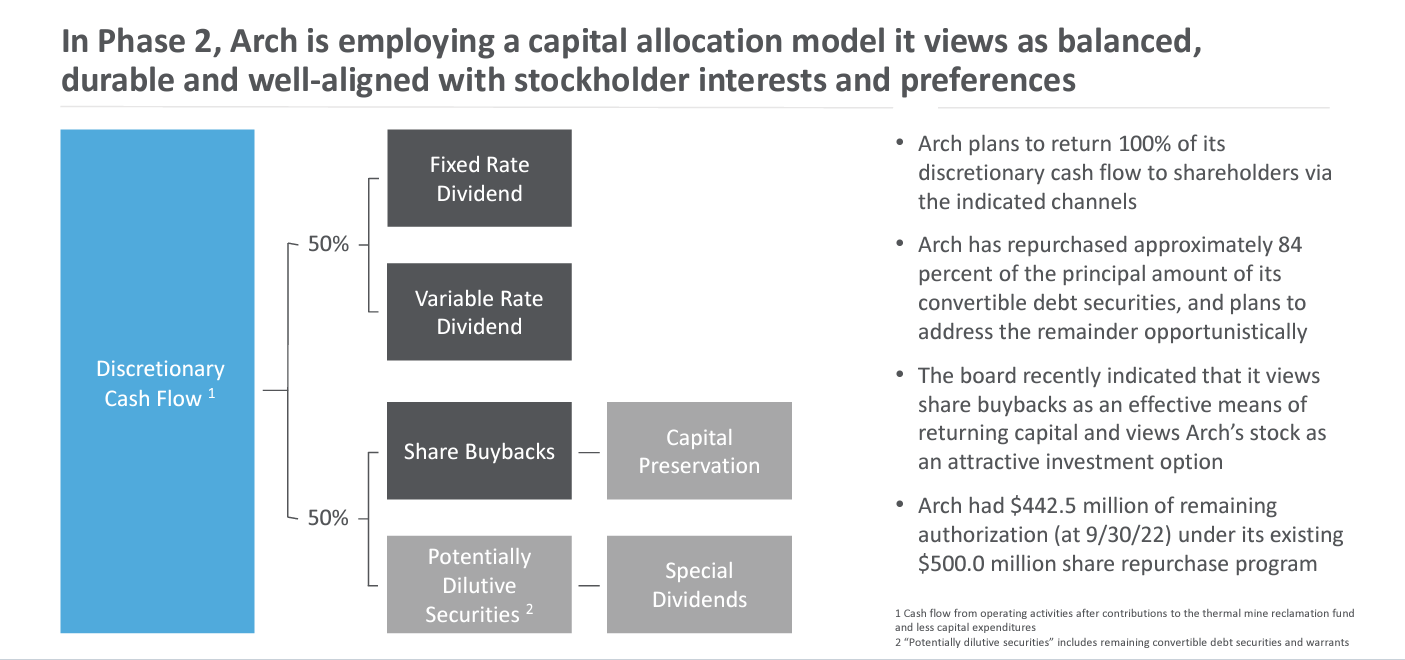

- At first sight (Fig 2), the company seems to suffer from a stock price depreciation; however, if we account for the last twelve-month dividend payment, we should report that Arch paid $27.72 per share (Fig 1). At today's price, the last twelve-month dividend yield represents almost 1/4 of the company's total market cap. Indeed, Arch aims to return 100% of its discretionary cash flow to shareholders (Fig 3);

-

In our estimates, the company will continue to remunerate its shareholders and the latest quarterly DPS of $2.45 was better than expected even if there were higher working capital requirements. However, we believe this will likely reverse in 2023. The West Elk issues might persist for the 2 quarters, but here at the Lab, met coal performance/outlook remains positive. Our buy rating is confirmed at $175 and is achieved with multiple valuations of 2.2x/3.5x on our estimated EBITDA in 2023 and 2024. The company is currently trading at an EV/EBITDA multiple of 1.85x which is also lower than its peers (the industry mean is at 2.44x). As a reminder, Arch is also cash positive and ended Q1 with a net cash position of more than $70 million.

Arch dividend payment (LTM)

Source: Arch Dividend History - Nasdaq - Fig 1

{kind=link}

Fig 2

Discretionary cash flow evolution

{kind=link}

Source: Citi’s Basic Materials Conference - Fig 3

Downside risks to our buy rating are 1) underlying commodities price, 2) weaker-than-anticipated volumes, 3) a concentrated asset base, and 4) regulatory risks.

For further details see:

Arch Resources: Long-Term Cash Cow