WHITF - Arch Resources: Massive Dividends And Buying Back 5% Of Shares

Summary

- Arch Resources management suggested they will buy ~5% of outstanding shares.

- The company is aggressively returning cash to shareholders through special dividends as well.

- Coal prices continue to be high and prospects are good due to non-economic supply constraining forces.

Arch Resources ( ARCH ) trades at a market cap of around $2.7 billion and an enterprise value of $2.39 billion because of a net cash position. It is a U.S.-based primarily metallurgical coal producer currently generating a lot of cash. According to S&P Global Commodity Insights , metallurgical prices are hanging in there:

The seaborne metallurgical coal market is entering Q1 2023 on a strong note amid growing hopes for easing trade between China and Australia and possibility of wet weather conditions in Queensland.

The benchmark Platts premium low-volatile hard coking coal prices, basis FOB Australia, increased $24/mt, or 9%, quarter-on-quarter to $294.50/mt, while PLV CFR China was up $7/mt or 2%, to $315/mt at the end of Q4.

That's even though coal prices in Europe are coming down as the winter has been mild so far, and the region stocked up when China was still in lockdown mode.

At the same time, there's still some uncertainty around the global economic outlook. Whitehaven's (Australian thermal producer) CEO recently said :

“We continue to see strong demand for high CV coal and tight supply, particularly with the sanctions/bans on Russian coal to Europe, Japan and some segments in Taiwan.”

In metallurgical markets, while pricing is relatively strong compared with historical levels, Whitehaven said it expected further volatility owing to ongoing global economic pressures.

Thermal coal has been doing unusually well in the past six months and this is helping Arch achieve great numbers as well.

{kind=link}

Arch is currently a $150 stock. In its last quarter, it generated more than $400 million in operating cash flow. Management is not interested in deploying capital in the thermal coal business and milking it for all its worth. The capital return policy is solid, with 50% of free cash flow earmarked as dividends and there's a readiness to deploy free cash flow in share repurchases. Per its most recent earnings call :

In terms of our priorities for that part of the capital return program, the third quarter activity provides a good roadmap. Our primary focus will likely be share buybacks, but we will continue to look for attractive opportunities to repurchase the remaining convertible bonds. At the end of September, our remaining authorization for share repurchases was more than $442 million.

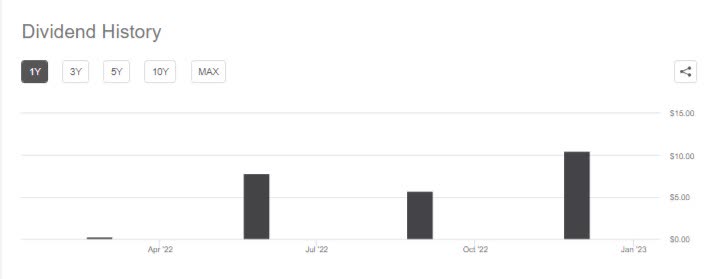

In 2022, that resulted in a bunch of dividends and special dividends of more than $24 per share:

{kind=link}

Analyst estimates for earnings for next year have been coming down but are still at $20 per share:

When I last wrote up the company , the estimates were still $33 per share.

Historically, the problem with cyclical is always that their earnings get smashed in recessions. Lately, it appears that recession is still not upon us, and there are some reasons to think coal producers' earnings may hold up better than expected. ESG forces are throttling capital going into coal development, and now Australia's judges are even outright blocking development (even if there's capital available).

Here's how the Arch CEO commented on the outlook (emphasis mine):

...coking coal prices remain at constructive and profitable levels. This is impressive given the recessionary pressures that continue to build around the world. And more impressive still, when you consider the knock-on effect these pressures have had on global steel production, which is down around 4%. We believe this resilience of the metallurgical markets is largely attributable to the profound underinvestment in coking coal supply in recent years.

Despite strong coking coal prices for the better part of the last six years, global coal, global coking coal supply in the major producing regions continues to languish. In Australia, which is the source of over 50% of the seaborne metallurgical supply, coking coal exports are down nearly 7% year-to-date, even when compared to last year's already weakened levels. In the United States and Canada, exports are up modestly versus 2021, but continue to dramatically lag pre pandemic levels. At the same time, the outlook for Russian supply continues to dip in face of import bans in many countries, logistical challenges, and an increasingly negative investment climate.

In terms of buybacks, the company is very flexible, but the management team has said they have liked stepped on the gas in Q4:

Lucas, this is Matt, and really probably the best way to look at it, we clearly came out of Q3 with a little more cash on our balance sheet than we wanted to quite a strong collection performance in the last couple of weeks of the quarter, which as you know, is a blackout period around earnings. So that really limited how much of that cash we could deploy in Q3, but puts us in a very good position, as I mentioned in my remarks, as we head into Q4. So as I indicated in those remarks, we think we can as much as double what we spent in Q3 on the second 50% of the program. And as we said, that's likely going to be buybacks. Just to put that in perspective, we did buyback over 400,000 shares nearly 450,000 shares in Q3. And so if we're able to hit that, that doubling level of that, depending on the share price, we can buy back as much as a million shares, or maybe even slightly more , slightly more as we go through Q4.

To put that into perspective, they would be taking out 5% of shares in a quarter in buybacks alone while also paying a $10 per share dividend in December. It is not a certainty that management has actually pulled the trigger but I'd definitely applaud it as the company looks undervalued.

I've pulled up valuations of several similarly sized (in terms of market cap) coal producers from Seeking Alpha data. These are primarily pure plays, but production can be weighted towards metallurgical or thermal coal. Metallurgical is generally considered to have a longer future, but it is also more prone to demand slumps due to the cyclical steel industry. Thermal coal demand is steadier because electricity demand is more stable.

| ARCH | ||||||

|---|---|---|---|---|---|---|

| P/E Non-GAAP (FY1) | ||||||

| 2.83 | ||||||

| 4.88 | ||||||

| 5.67 | ||||||

| 4.61 | ||||||

| - | ||||||

| - | ||||||

| P/E Non-GAAP (FY2) | ||||||

| 3.84 | ||||||

| 3.25 | ||||||

| 2.66 | ||||||

| 4.05 | ||||||

| - | ||||||

| - | ||||||

| P/E Non-GAAP (FY3) | ||||||

| 7.32 | ||||||

| 2.83 | ||||||

| 2.89 | ||||||

| 16.57 | ||||||

| - | ||||||

| - | ||||||

| P/E Non-GAAP ((TTM)) | ||||||

| 2.74 | ||||||

| 6.66 | ||||||

| 6.12 | ||||||

| 2.87 | ||||||

| 16.16 | ||||||

| - | ||||||

| P/E GAAP ((FWD)) | ||||||

| 2.72 | ||||||

| 4.92 | ||||||

| 5.66 | ||||||

| 4.43 | ||||||

| - | ||||||

| - | ||||||

| P/E GAAP ((TTM)) | ||||||

| 2.82 | ||||||

| 6.68 | ||||||

| 5.83 | ||||||

| 3.57 | ||||||

| 3.10 | ||||||

| 4.91 | ||||||

| PEG Non-GAAP ((FWD)) | ||||||

| - | ||||||

| - | ||||||

| - | ||||||

| - | ||||||

| - | ||||||

| - | ||||||

| PEG GAAP ((TTM)) | ||||||

| 0.00 | ||||||

| 0.04 | ||||||

| NM | ||||||

| NM | ||||||

| 0.00 | ||||||

| NM | ||||||

| Price/Sales ((TTM)) | ||||||

| 0.68 | ||||||

| 1.23 | ||||||

| 1.08 | ||||||

| 0.84 | ||||||

| 1.98 | ||||||

| 1.92 | ||||||

| EV/Sales ((FWD)) | ||||||

| 0.65 | ||||||

| 1.19 | ||||||

| 1.20 | ||||||

| 0.77 | ||||||

| - | ||||||

| 1.03 | ||||||

| EV/Sales ((TTM)) | ||||||

| 0.66 | ||||||

| 1.31 | ||||||

| 1.18 | ||||||

| 0.78 | ||||||

| 3.07 | ||||||

| 1.53 | ||||||

| EV/EBITDA ((FWD)) | ||||||

| 1.85 | ||||||

| 3.09 | ||||||

| 2.92 | ||||||

| 1.98 | ||||||

| - | ||||||

| 1.49 | ||||||

| EV/EBITDA ((TTM)) | ||||||

| 1.82 | ||||||

| 3.70 | ||||||

| 3.34 | ||||||

| 2.47 | ||||||

| 3.69 | ||||||

| 2.54 | ||||||

| Price to Book ((TTM)) | ||||||

| 2.28 | ||||||

| 1.84 | ||||||

| 2.38 | ||||||

| 1.55 | ||||||

| 1.56 | ||||||

| 2.17 | ||||||

| Price/Cash Flow ((TTM)) | ||||||

| 2.33 | ||||||

| 4.04 | ||||||

| 3.96 | ||||||

| 4.29 | ||||||

| 2.52 | ||||||

| 3.36 |

Arch stands out as cheap on most metrics. I think P/Es, EV/EBITDA, and price/cash flow are critical multiples and Arch trades at the bottom end of the range for all these. In my opinion, coal companies' future cash flows are overly discounted because the sector is deemed uninvestable by institutional investors. If a quarter or two passes while prices hold up around current levels, an investment in Arch or a competitor is already significantly derisked because of the high levels of free cash flow and low debt. Because the company actively returns capital to shareholders (through dividends, special dividends, and buybacks), investors are less dependent on the market assigning healthy multiples or correctly pricing future cash flows. The cash is actually coming out. As long as they keep allocating capital wisely, it is hard for me to ignore these deep-value names.

For further details see:

Arch Resources: Massive Dividends And Buying Back 5% Of Shares