ARCH - Arch Resources Still Has Room To Grow

2023-07-27 12:19:49 ET

Summary

- Despite the boom-bust cycle of the coal industry and recent capital exodus, Arch Resources has seen superior profitability due to conservative capital expenditure and disciplined capital allocation.

- Arch Resources' share price has risen by nearly 55% in the last five years, with a total shareholder return of over 98%, largely driven by dividends and share buybacks.

- The company's capital return program has resulted in $1.6 billion deployed since 2017, with room for growth in dividend issuance and share repurchase due to the gap between free cash flow generated and capital returns.

Arch Resources, Inc. ( ARCH ), one of the world’s largest coal producers and an important producer of metallurgical coal, has managed to beat the market despite what the Street would view as the firm possessing two big red flags. Firstly, the industry tends to exist in a boom and bust cycle, secondly, there has been an exodus of capital over the last few years. However, the post-2011 period has seen firms more conservative about capital expenditures, and more disciplined about capital allocation, and this has, in the case of Arch Resources, led to superior profitability. The firm is trading at very attractive levels, with a price/earnings (P/E) of 1.99, a gross profitability of 0.54 and free cash flow ((FCF)) yield of 39%.

Dividends Drove Market Performance

In the last five years, Arch Resources share price has risen by nearly 55%, compared to nearly 68% for the SPDR S&P 500 ETF Trust ( SPY ), which tracks the S&P 500 ( SPX ), and over 61% for the iShares Russell 3000 ETF ( IWV ). Taking dividends into account, Arch Resources enjoyed a total shareholder return (TSR) of over 98%, while the SPDR S&P 500 ETF Trust had a TSR of nearly 83%, and the iShares Russell 3000 ETF had a TSR of nearly 75%.

Source: Morningstar

Capital Returns Have Room to Grow

Having established the importance of dividends to Arch Resource’s performance, we should spend some time asking if there is room for growth.

The company began Phase 1 of its capital return program in May 2017. In that three-year period, the firm returned $921 million of capital, buying back 40% of its outstanding shares, before suspending the program in April 2020. Phase 2 of its capital return program began at the beginning of 2022, returning $613.18 million in capital in that year alone. The capital return program has resulted in Arch Resources deploying $1.6 billion since 2017, or 71% of its market cap.

Since 2017, dividend issuance has grown from $24.37 million in 2018 to $456.39 million in 2022, compounding at nearly 63% a year. In the last twelve months (LTM), the firm has paid out $519.44 million in dividends. Since 2017, the firm has grown FCF from $337.27 million to $1.04 billion in 2022, compounding at 20.56% a year, totaling $2.31 billion, or 102% of its market cap. In the LTM, the firm has generated $861.74 million in FCF. Since 2017, the firm has bought $984.15 million of its own shares, buying $177.6 million in the LTM. In 1Q23, the firm generated $95.58 million in FCF, paid out $66.9 million in dividends, and bought $22.91 million of its own stock. The gap between FCF generated and capital returns I think indicates that there is ample room for the business to grow dividend issuance and repurchase its shares.

Data Source: Arch Resources, Inc. Filings

Capital Exiting the Industry Will Boost Returns

Typically, when analysts look at an industry, they conflate its unpopularity -as measured by capital exiting the industry-, as a sign that returns will decline and that the industry is not investable. This is a very false notion. Managerial overconfidence often results in managers overestimating the FCF that can be generated as a consequence of their capital expenditures. As a result, they raise too much capital to fund these projects, until they realize that their dreams were built on glass, and the glass cracks open under them, the share price plummets, and the firm gets into difficulties repaying its debt, and this continues until the situation is sanitized. This boom-bust cycle is well-known to investors in metals and mining. I think the moment to invest then, is not when managers are pouring in money, but when capital is exiting, when capital discipline is high, when competition is decreasing, when supply is narrowing.

For Arch Resources, the pattern is clear: between 2017 and 2018, long-term debt was around 16% of assets, peaking in 2020 at nearly 28%, and declining to around 5% in 2020 and the LTM. This is not simply a story of de-risking, but mirrors a global pattern of capital exiting the industry.

Data Source: Arch Resources, Inc. Filings

Before we look at the global picture, the firm’s capital expenditure is another interesting data point, with capex as a share of total assets beginning the era at nearly 3%, seeing a peak in 2020 of nearly 17%, and declining to around 7% in the LTM. Arch’s return on invested capital ((ROIC)) has risen from 13.2% in 2018 to 57.2%

Data Source: Arch Resources, Inc. Filings

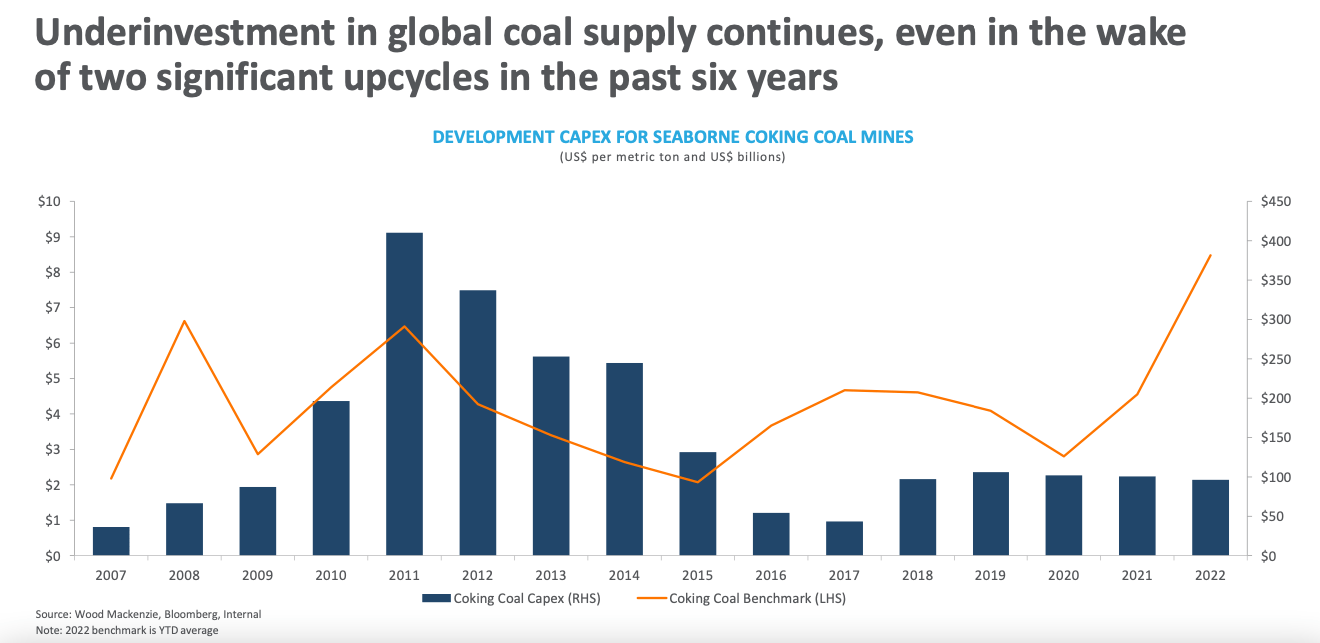

Declining investment isn’t just about Arch Resources. Per their 2022 Basic Materials Conference investor presentation , there has been a marked underinvestment in global coal supply, despite two significant upcycles in the last six years. This is a theme that is pervasive across metals and mining, with firms scarred by the collapse of the last bubble in 2011, which forced players to clean up their balance sheets, and place capital discipline and profitability ahead of growth, which has had the effect of creating a situation of underinvestment.

{kind=link}

Economics 101 will tell you that, demand held constant, if supply is flat or declines, then prices will rise. That seems to be the case here as well, with the long run average price of coking coal rising since 2003, with the coking coal benchmark averaging $183 per metric tonne since then, rising to $199 per metric tonne since 2010. As underinvestment continues, and demand continues to rise -despite volatility-, we can expect the long run average to continue to rise, boosting prices, and industry-wide profitability.

Valuation

Arch Resources has a P/E multiple of 1.99 compared to a P/E multiple of 26.44 for the S&P 500. In addition, the firm has a gross profitability of 0.54 compared to a benchmark for attractiveness of 0.33 , suggesting that the firm’s profitability is very attractive. The firm’s LTM FCF are trading at a yield of around 39%, compared to the market’s FCF yield of 2.3% , according to New Constructs’ calculations. The firm, therefore, appears attractive compared to the market, with its profitability and FCF standing out.

Conclusion

Arch Resources belongs to an industry that investors associate with boom and bust cycles, and, at present, with an exodus of capital, we're in a bust. Whereas the Street view is that this is a negative, the actual impact has been that capital discipline has risen along with profitability, despite the firm and the industry as a whole, reducing capex. This suggests that this period of profitability is sustainable, and investors should look to this era as a glorious opportunity to buy very profitable businesses at a sharp discount to the market.

For further details see:

Arch Resources Still Has Room To Grow