ACHR - Archer Aviation: Cathie Wood Is Bullish We Are Skeptical

2023-09-13 08:28:03 ET

Summary

- Archer Aviation has risen over 87% since our last "Buy" rating, but caution is advised right now due to uncertainties and risks.

- ARK Invest, led by Cathie Wood, is optimistic about Archer and owns a significant stake in the company after a recent Equity raise.

- There are uncertainties surrounding FAA certification, production costs, and competition, leading to a cautious outlook on Archer's prospects.

- We estimate Archer stock is likely to be fairly valued, with the intrinsic value being close to the current share price.

Investment Thesis

Archer Aviation ( ACHR ) has been one of our best investment ideas over the past year, rising a whopping 87.36% after our last "Buy" rating in May 2022 compared to the S&P 500 which returned just 11.80% over the same time horizon. After the immense recent rally, however, we have become a bit more cautious about whether we can still find value in the stock at current prices.

By contrast, well-known fund manager Cathie Wood of Ark Invest, a leading fund in disruptive innovation, is enthusiastic about the company's eVTOL prospects. They have recently invested significantly in the stock and currently own 22.1 million shares, or 8.80% of all outstanding shares. In this article, we look at why we currently rate Archer as "Hold" and point out some of the reasons why we have become less optimistic.

ARK Invest Is Bullish

A lot has changed since we last wrote about Archer Aviation. For investors unfamiliar with Archer, they specialize in the production of electric vertical takeoff and landing (eVTOL) aircraft. Their main aircraft intended for production, called "Midnight," is expected to carry 4 passengers and 1 pilot and has a range of up to 100 miles. However, most trips are expected to be only 20–50 miles to optimize charging time and profitability.

{kind=link}

Archer IR

As for their timeline, they are currently working with the FAA to obtain "type certification" for their aircraft "Midnight" and aim to be on the market in 2025. Yet they expect to have their first test flight next year, in 2024. In other words, 2025 seems like a pretty optimistic timeline to us, if everything falls perfectly into place.

Certification aside, Archer recently secured $215 million in funding from an equity investment round, in which renowned fund manager Cathie Wood also invested $44 million with her fund Ark Invest, expressing her confidence in Archer's ability to bring their eVTOL to market. In addition to participating in this investment round, Ark Invest also purchased shares of the open market in their flagship ARK Innovation Fund ( ARKK ), as well as in their Autonomous Technology & Robotics ETF ( ARKQ ) and Space Exploration & Innovation Fund ( ARKX ).

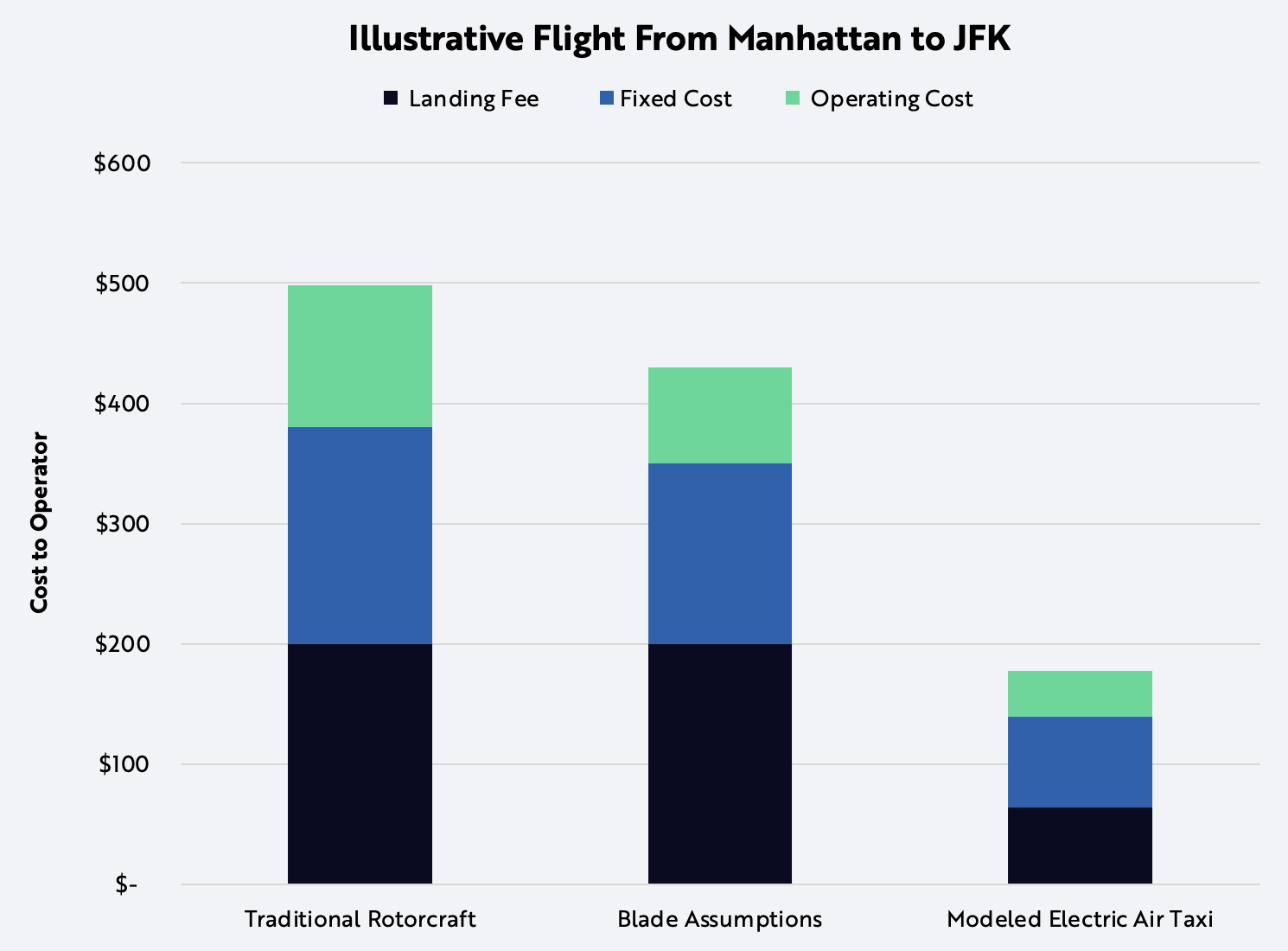

In total, Ark owns about 12.21 million shares in ARKK , along with 7.88 million shares in ARKQ and 2.05 million shares in ARKX , or nearly 22.15 million shares worth $144 million, making them one of the largest holders , along with American Airlines ( AAL ), Stellantis ( STLA ) and founder Adam Goldstein. Taking this large position in the eVTOL maker came after they published research last month detailing their assumptions about the future unit economics of the eVTOL market. According to their modeled eVTOL assumptions, a flight from Manhattan to JFK can be reduced from $500 with a traditional helicopter to less than $200 at scale, even surpassing estimates published by other eVTOL maker Blade ( BLDE ).

{kind=link}

Ark Invest

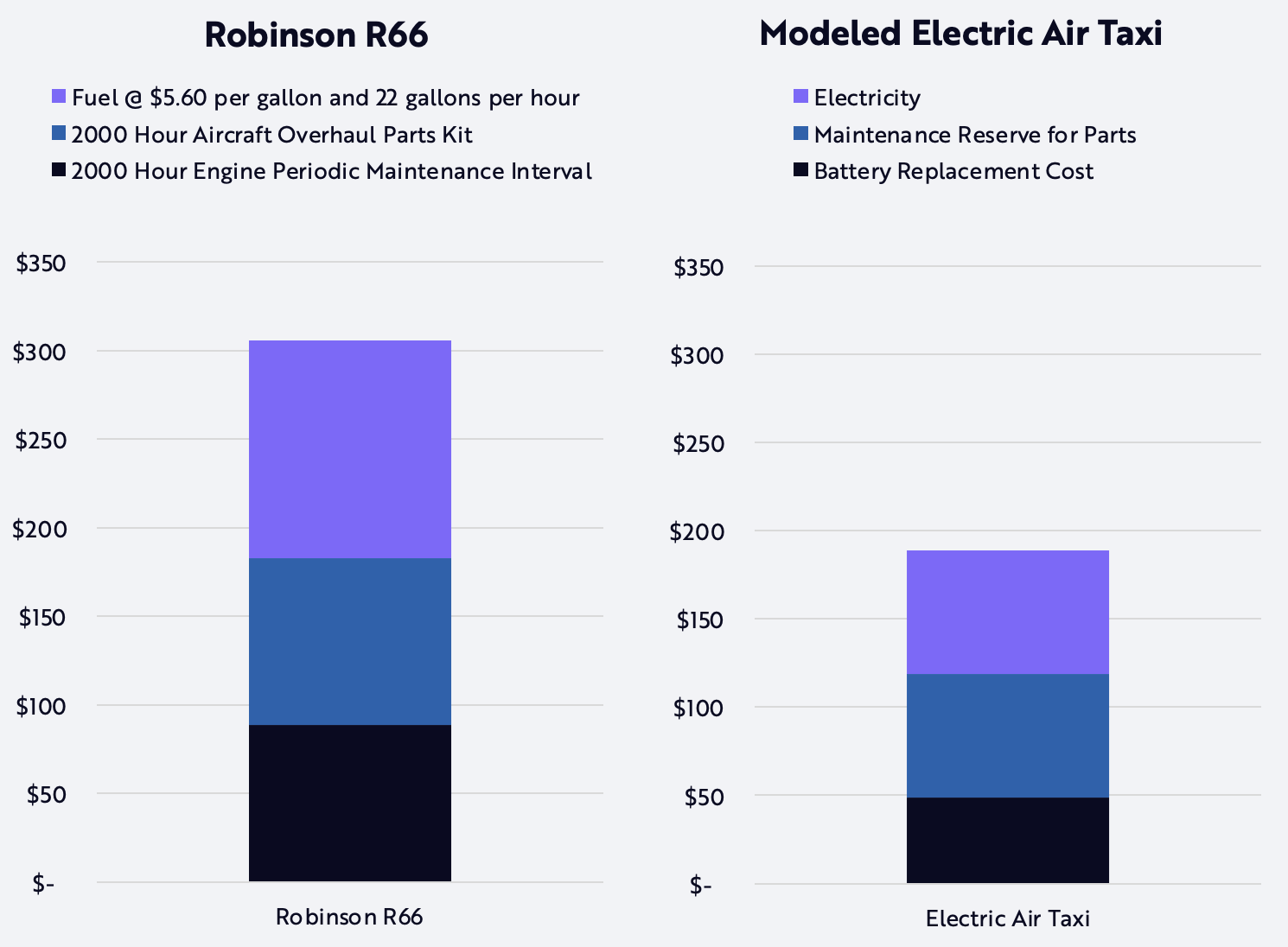

However, the key variables are the initial cost of the vehicle and the number of flight hours per year. Ark Invest assumes that the upper limit for eVTOL taxi's would be 2000 hours per year, while regular helicopters typically fly only about 1000 hours per year. An eVTOL flying 2000 hours per year would mean it would be in operation 24/7 with a utilization rate of ~23%. They also point to the cost benefits associated with both fuel savings and lower maintenance-level ownership costs, which should give eVTOL companies a competitive advantage in the marketplace.

{kind=link}

Ark Invest

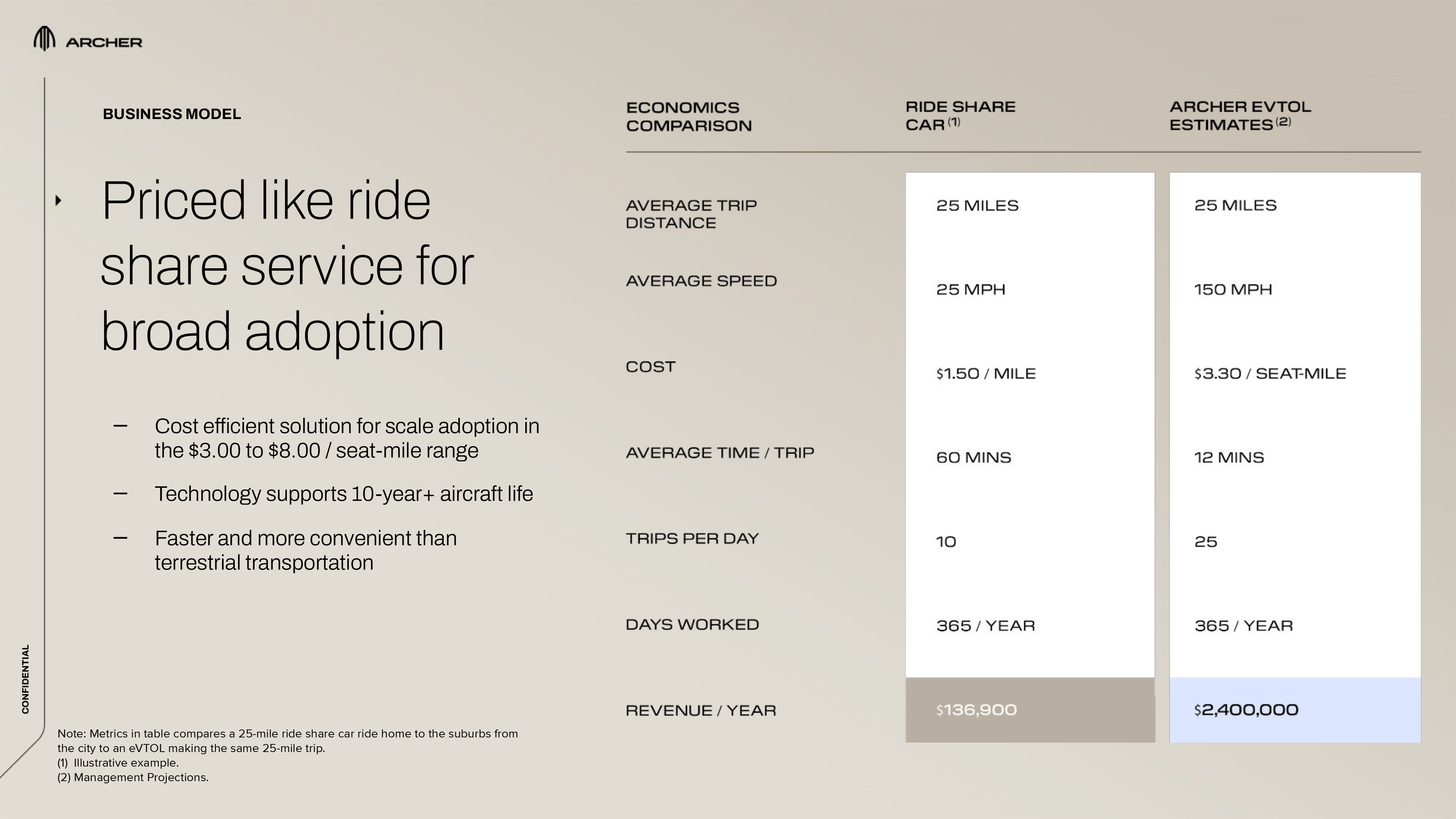

If we look at Archer's assumptions, they compare themselves to a Ride Share service, which reportedly makes $136.9K in revenue per year, compared to Archer's estimated eVTOL at $2.4M. However, in our opinion, these assumptions are rather misleading when looking at their investor deck. Since eVTOL is supposed to be faster than ride-share on the ground, they expect to do 25 rides per day compared to 10 for the normal ride-share service that takes 60 minutes over the same route that Archer does for only 12 minutes.

The most important part of their estimates, however, is the cost per mile, which they estimate at $1.50 for ride-share, while for eVTOLs they charge $3.30 per "seat-mile". While this may not seem like much of a difference at first glance, it becomes apparent when you take an example of a group of 4 people who need to make a 25-mile trip. In the ride-sharing example, the 4-person group would pay only $37.50, or simply $1.50 per mile. The same trip with an eVTOL and 4 people would cost as much as $330, taking $3.30 per "seat-mile" and multiplying that by 4 people and 25 miles.

{kind=link}

Archer IR

In other words, the question is whether it's almost worth paying $292.5 extra to save 48 minutes of time. And while eVTOLs also have the cost advantage when it comes to maintenance and fuel savings, it may also be important to point out that the ride-sharing industry, which they compete with, have the same advantages when it comes to the electrification and perhaps automation of the current auto industry.

Right now there are just too many unknown parameters, from whether they will be able to get FAA certification, to the actual construction cost of the aircraft, to whether there will be a large enough market willing to pay these premium rates. Not to mention possible problems with certain neighborhoods not wanting eVTOLs operating in their areas. There is also the question of competition, such as Joby, which has partnered with Uber ( UBER ) and already has the capability for integration into one of the largest ride-sharing apps.

The Fundamental Picture

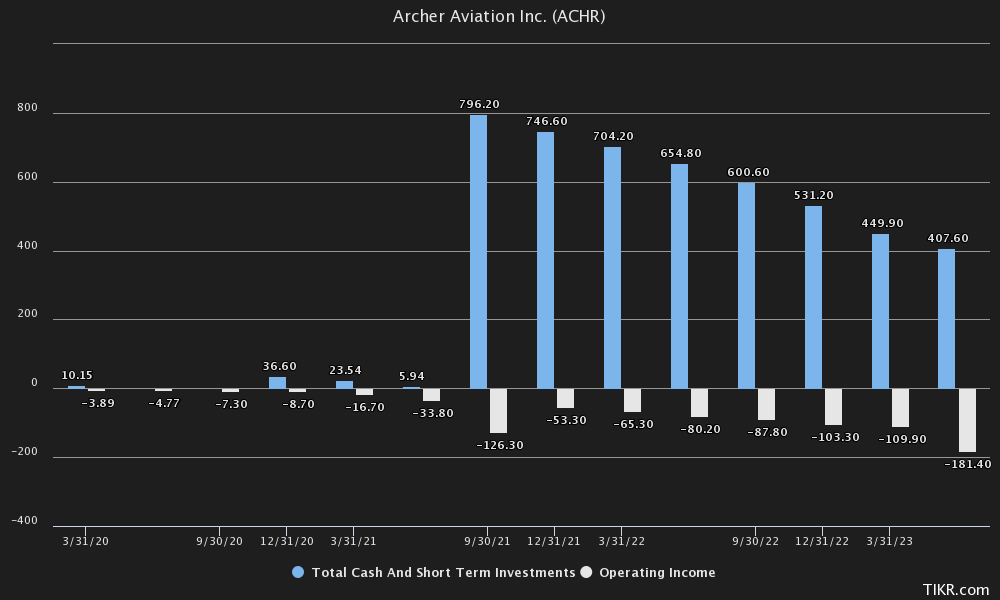

Fundamentally, much has changed since last year. Archer's operating income has gone south as they move closer to FAA certification, with a current burn on an operating income level of -$181.4M in the last quarter. However, total non-GAAP operating expenses are expected to be only $75M to $85M for the third quarter.

Anyway, the initial cash mountain of $796.2M that Archer had in 2021 is starting to shrink quite a bit, to $407.6M as of June, although their total liquidity now amounts to more than $675M including the recent round of equity investment, as mentioned in the latest earnings call .

{kind=link}

TIKR

However, a large part of these costs are non-cash costs such as share-based compensation, which are nonetheless dilutive to shareholders. Looking at free cash flow , for example, we see that it has been between -$50M and -$75M for the last few quarters, or $263.1M for the last 12 months. Which begs the question for us how much additional capital will be needed to bring these eVTOLs to market, knowing that at a burn rate of $263.1M, they only have a little over 2.5 years until they run out of cash, aside from the dilution from stock-based compensation and warrants.

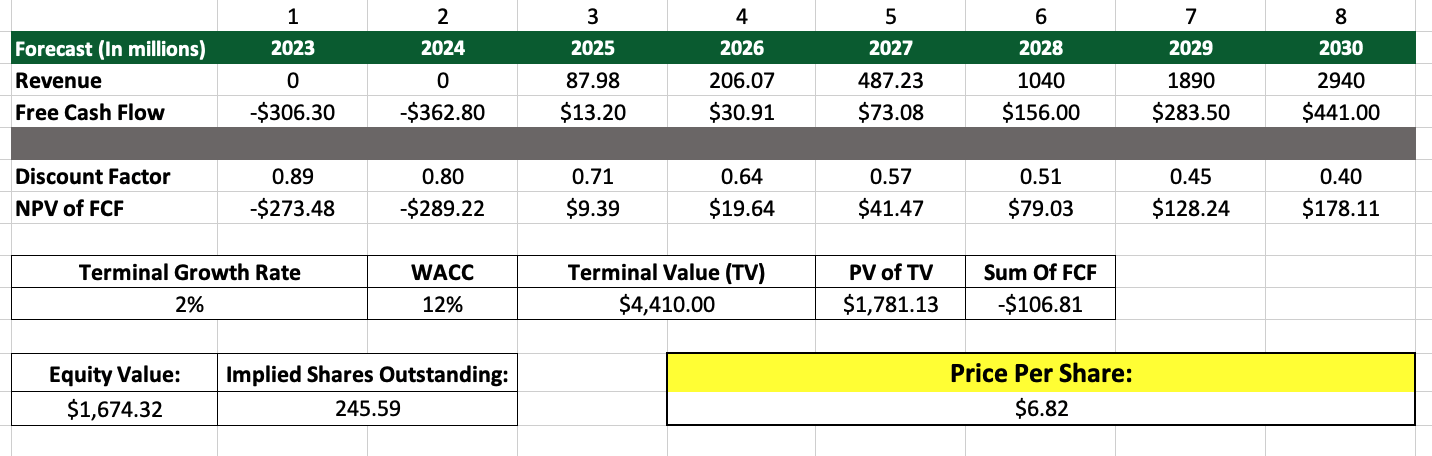

The last time we looked at Archer, it struck us as a no-brainer, as they were trading at a P/E ratio of 1.29, with most of their market capitalization at that time supported by cash and short-term investments. Currently, Archer is trading at more than 2.63x P/E, if we take into account their $675 million in liquidity. From an intrinsic valuation standpoint, we believe Archer is probably reasonably valued if we use optimistic forecasts. In our valuation, we took analysts' projections for revenue through 2030, where revenue would come in at $2.94BN. To put this figure in context: United Airlines ( UAL ) placed an order for 300 planes for $1.5BN, which would put the price for each plane at $5M. This would mean they would have 588 aircraft in service, which seems an optimistic goal, but perhaps achievable.

{kind=link}

Author's Calculations/ Valuation

If we look at Free Cash Flow, the first few years are expected to be quite negative as they move towards certification of their aircraft. Going forward, we assume a Free Cash Flow margin of 15%, which again we think is quite optimistic when we look at peers in both the aircraft manufacturing and ride-sharing sectors, with FCF margins typically between 2-8%. Discounting this figure at a WACC of 12%, we arrive at a sum of free cash flows worth -$106.81M over the period.

Taking into account a 2% growth rate, we get a present value of $1.78BN of terminal value, or $1.67BN of equity value if we take into account the sum of free cash flows. Dividing this figure by the 245.59 million shares outstanding, we arrive at our estimate of intrinsic value, which is a price per share of $6.82, assuming optimistic estimates and assuming Archer is able to go to market and obtain "type certification" from the FAA in 2025.

{kind=link}

TIKR

This outlook is also optimistic in the sense that we believe it could be long after 2025 before Archer is certified. A recent audit by the Department of Transportation's Office of Inspector General also revealed these challenges and stated that:

Regulatory, management, and communication issues hindered FAA’s progress in certifying AAM aircraft, and challenges remain. Given their unique features, AAM aircraft do not fully fit into FAA’s existing airworthiness standards. For over 4 years, FAA made limited progress in determining which certification path to use.

The Bottom Line

Cathie Wood at Ark Invest may be bullish about Archer, but we believe there are too many risks associated with the stock at the moment. These risks can range from FAA certification to unknown production costs and operating margins, to the actual viability of the business model, along with possible production delays that would delay future cash flows.

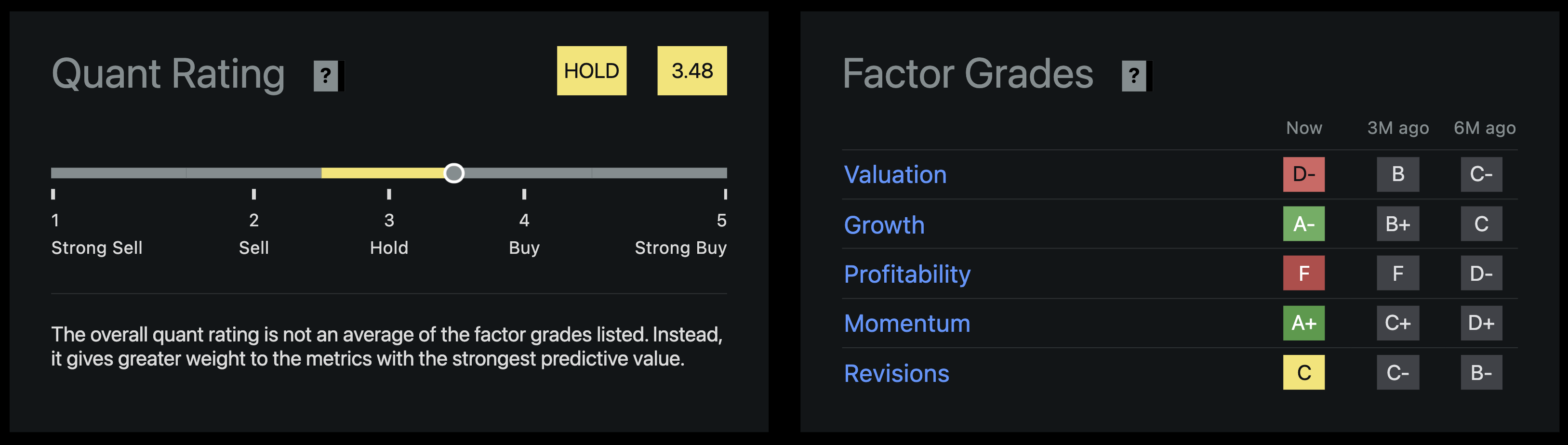

In our previous review, Archer was a no-brainer while trading close to its book value, while it now trades well over twice its book value with seemingly most of the price action in the stock driven by recent news about partnerships/ contracts and completing new steps toward certification of their aircraft. We believe intrinsic value is closer to $6.82 and currently believe Archer should be given a "hold" rating similar to Seeking Alpha's Quant Rating.

{kind=link}

Seeking Alpha

For further details see:

Archer Aviation: Cathie Wood Is Bullish, We Are Skeptical