ACHR - Archer Aviation: Powering Up The Engines But Not Ready For Takeoff

2023-11-29 20:34:09 ET

Summary

- Archer Aviation is in a stable financial situation with $461.4 million in cash and cash equivalents and $175.1 million in liabilities.

- Archer has achieved key operational developments, including completing testing of the Maker aircraft and making progress in the development of the Midnight aircraft.

- In a competitive industry, ACHR is starting to emerge as a dominant player but, they must prove their operational excellence in the coming quarters.

Archer Aviation Inc. ( ACHR ), is engaged in the development and sale of electric vertical takeoff and landing (eVTOL) aircraft. While they are in heavy R&D mode they are in a reasonably stable financial situation. The company's balance sheet reports $461.4 million in cash and cash equivalents, which is a significant part of its total current assets at $475.7 million. This liquidity is contrasted with a total liability of $175.1 million, indicating that the company has a solid footing to manage short-term liabilities, absorb market fluctuations and survive quarters of R&D to get to market. The recent issuance of $145 million in shares is a boost for their balance sheet but we see further equity dilution in the near short to mid-term. Due to the lack of immediate profitability we are placing a "Hold" Rating on ACHR until we can see significant revenue. Below we explain the key short term developments ACHR has completed and we discuss the unique challenges and opportunity that we foresee in ACHR's future.

R&D Costs

The income statement portrays a certain narrative - one that is not uncommon for companies pioneering new technologies and all too common to SPACs. With their 11th quarter in a row of zero revenue, it is evident that Archer is still in the pre-revenue stage. This pattern of investment spending without immediate revenue generation was consistent throughout 2023, and is reflective of the high-cost nature of the aerospace industry, particularly in the emerging eVTOL market.

Expenses are, to no one's surprise, concentrated on research and development, totaling a considerable $67.8 million for the quarter, which underlines the company's commitment to innovation and product development and their reliance on it. This substantial investment in design and technology fueled an operating loss of $46.2 million, culminating in a net loss of $51.5 million for the quarter. This is due to a massive increase in Operating Income driven by SG&A department making $21.6 Million vs last quarter's loss of $181.4 Million. Removing this anomaly we can estimate that the quarter's net loss would have been ~$100 million. With a net cash balance of $286 million this puts them in quite a precarious position and we believe they're likely to need continued outside financing through either debt issuance or share issuance before a positive gross profit. We believe the most likely source of funding will come from share issuance and equity dilution. We have a working assumption of continued double digit share inflation over the next few years, with share issuance declining near 2025.

Operations Development

With orders coming in , the true test for ACHR and other eVTOL manufacturers is right around the corner. The company's strategic and technical progress align with its goal to begin commercial operations in 2025, suggesting a determined pursuit of bringing eVTOL technology to market efficiently and capital-effectively.

Recently they've had 3 Main Operational Developments

-

Completion of Maker Aircraft Testing : Archer successfully completed testing of the Maker aircraft, which served as a crucial testbed to inform the development of their future aircraft. This milestone is pivotal in validating the performance of Archer's eVTOL designs and ensures the technology is on par with safety and functionality standards.

-

Midnight Aircraft Developments : Significant progress has been made in the Midnight aircraft's development. Leveraging data and insights from the Maker aircraft has allowed Archer to create efficient feedback loops that are vital for advancing Midnight's flight test program. The company has indicated that comprehensive flight testing of the Midnight aircraft will begin with unmanned flights before moving to piloted testing, slated for mid-next year [2024].

-

Achievements in Manufacturing : Increase in manufacturing capacity by initiating the construction of a high-volume factory in Covington, Georgia. Furthermore, suppliers are supposedly accelerating the manufacture of parts for the Midnight aircraft in preparation for pilot onboarding and subsequent testing phases.

*The key milestone of flight testing in mid 2024 is a corner piece of our trading strategy highlighted below.

With the FAA administration becoming more and more focused on eVTOL support we assume there is a low likelihood of legislative delays at the national level. We believe this puts the odds of 2025 commercial markets opening very high.

These developments are critical components for Archer Aviation's path to commercialize its eVTOL aircraft and could serve as potential catalysts for the company's future growth and success in the burgeoning urban air mobility market. While significant delays may allow competitors to take hold in potential customers.

Valuation

With no revenue and no earnings, ACHR must be valued relative to their R&D goals and their ability to capture the market prior to the need for external funding either through debt or equity financing. With such a competitive and absolutely new industry it makes it extremely challenging to estimate the potential earnings for the company.

As we explained in our JOBY article , we believe that the market for eVTOL's is massive and a chance for dominant players to make their mark on the industry but with little fundamentals to value the company against we must instead focus on relative valuations to allow us to simultaneously capitalize and hedge in this challenging industry

While ACHR has many competitors we believe the easiest to draw similarities with is JOBY . Joby is at a similar position developmentally and operationally. They too have an ongoing testing program and are both building factories for serial production of their aircraft.

Joby Aviation appears to have secured a 6 to 12-month lead over Archer Aviation, underscored by Joby's successful flights in New York City , and Archer closes that technical gap quarter after quarter. It is our assessment that this disparity is unlikely to significantly impact the progression and rollout of their respective eVTOL fleets.

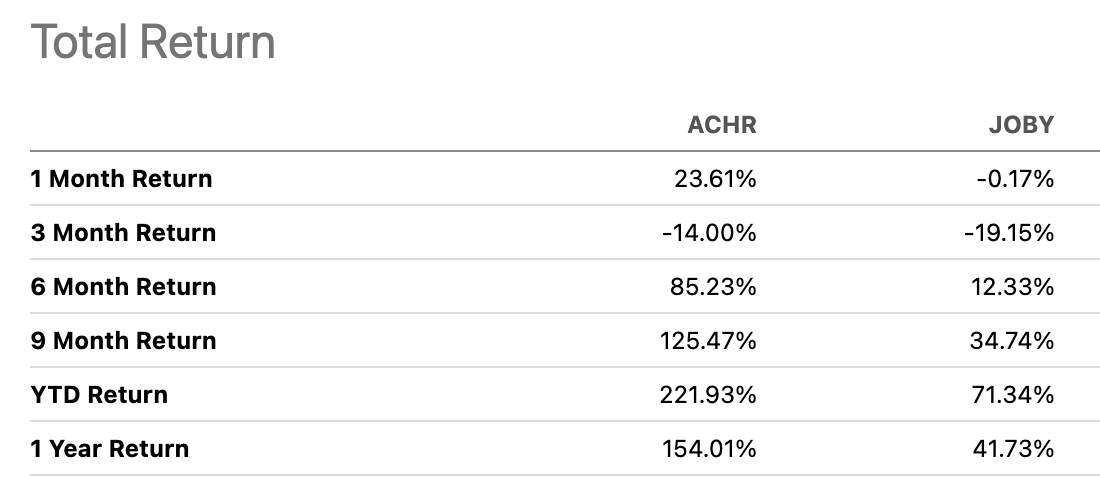

When evaluating both companies from a valuation standpoint, it's apparent that JOBY's recent market performance has not kept pace with ACHR's. This divergence may be attributed to JOBY's market capitalization already reflecting more than twice the valuation of ACHR. Given their distinct business strategies within the same industry, it is reasonable for their market valuations to differ. ACHR's primary focus is on manufacturing and selling eVTOL aircraft, while JOBY's business model is centered around both the creation and operational management of their aircraft fleet.

Comparative Returns (Seeking Alpha)

{kind=link}

Both companies strive for efficient and cost-effective aircraft production, yet manufacturing and margin challenges may more significantly affect ACHR than JOBY as JOBY also has valuation prospects related to their services down the line. ACHR's comparatively limited industrial partnerships, especially when contrasted with JOBY's key supplier relationship with Toyota, suggest that JOBY may experience fewer supply chain difficulties due to the strength of this alliance. We believe ACHR is going to be valued purely as an industrial manufacturer, where their entire valuation is going to based on their ability to produce aircraft at profitable levels. On the other hand JOBY will be valued as a "full-stack" eVTOL business which may offer it some unique advantages when it comes to the valuation associated with not only building the aircraft but also operating them. This difference we believe will in the long term cause JOBY to be more likely to harness upside as compared to ACHR.

Conclusion

One could argue that the same transformative economics observed in the automobile sector are likely to apply to electric vertical take-off and landing (eVTOL) vehicles. The substantial decrease in the cost of batteries, combined with advancements in electric motor efficiency, have been central to the automobile industry's electric revolution. As battery technology continues evolving, with improvements in energy density and reduction in weight, these synergies are expected to extend to eVTOL aircraft, making them considerably more viable and cost-effective to make and maintain.

We believe that in the short 1-4 year timeframe that we are likely to see ACHR have more significant volatility vs JOBY and potentially higher returns. We believe the news cycle that ACHR is in will allow them more upside but the lack of profitability leads us to be hesitant to purchase the stock outright, especially with likely more equity dilution in the next 1-2 years. Due to this we are giving the stock a 'Hold' rating. As aircraft role in to production we will keep our eye on ACHR but the lack of revenue or any signs of immediate profitability makes it challenging to value ACHR outside of a relative comparison to JOBY.

Our Trade

We anticipate that JOBY's vertical integration strategy may ultimately prove advantageous in the long-term. However, we believe Archer Aviation ( ACHR ) is also expected to play a pivotal role in the industry. Given the current developmental stages of these companies, a pairs trading strategy using options seems prudent. ACHR, with its relatively lower market valuation, presents more potential for upside compared to JOBY. Moreover, ACHR's business model, which could generate significant market movement through announcements of major orders, is a unique advantage over JOBY, potentially leading to both positive and volatile market reactions.

We plan to take advantage of the high Implied Volatility in ACHR and plan to open Iron Condors in both JOBY & ACHR and using the proceeds to purchase ITM long dated call options. We plan to use this strategy through 2023 and in to 2024 & Early 2025. We see a higher chance of ACHR diluting shares than JOBY so we will be placing a more negative skew to our Iron Condors on ACHR.

For further details see:

Archer Aviation: Powering Up The Engines But Not Ready For Takeoff