ARNC - Arconic: Company Sale Is Likely

2023-04-14 11:04:17 ET

Summary

- Arconic has recently attracted acquisition interests from a number of private equity firms, including Apollo Global Management, Carlyle Group, and Lone Star Funds.

- Meanwhile, activist investor Sachem Head has accumulated a position and is pushing for the company’s sale.

- There is a chance of a bidding war breaking out here.

- I expect the company to fetch north of $32/share in a potential sale vs the current share price of c. $26 - for a 25% upside.

Arconic Corporation ( ARNC ) is a $2.6bn market cap producer of rolled aluminum products, such as coils, sheets, and plates. The company's production is used in a number of end markets, including airplane frames, automotive body panels, and beverage cans, among others. In late February, WSJ reported that the company has been in sales talks with private equity giant Apollo Global Management which has had debt financing in place. While ARNC's management did not confirm acquisition interest, the media also reported that the company's financial advisors have reached out to other potential bidders. Subsequently, in March, rumors appeared that private equity firms Carlyle Group and Lone Star Funds have also joined Apollo in the bidding process. The rumors mentioned that at least two other parties might be interested in scooping up Arconic, suggesting a bidding war might be brewing here. These recent developments were followed by the news in late March that activist investor Sachem Head has accumulated an undisclosed stake in the company and is pushing for a sale. ARNC's stock has reacted favorably to the recent developments, with the share price jumping 16% since February. A recent Bloomberg report suggests Apollo might make an offer at $27-$28/share or 5-9% above current share price levels. A potential acquisition bid at these levels would likely be low-balled and opportunistic given that ARNC seems to be on the brink of a substantial EBITDA inflection. Relative valuation suggests that, in a sale scenario, the company might instead be worth materially more. Valuing ARNC in line with a close peer and on my conservatively estimated forward adjusted EBITDA, the company would fetch over $32/share. Downside to pre-rumor levels is 14%.

The Timing Is Opportunistic

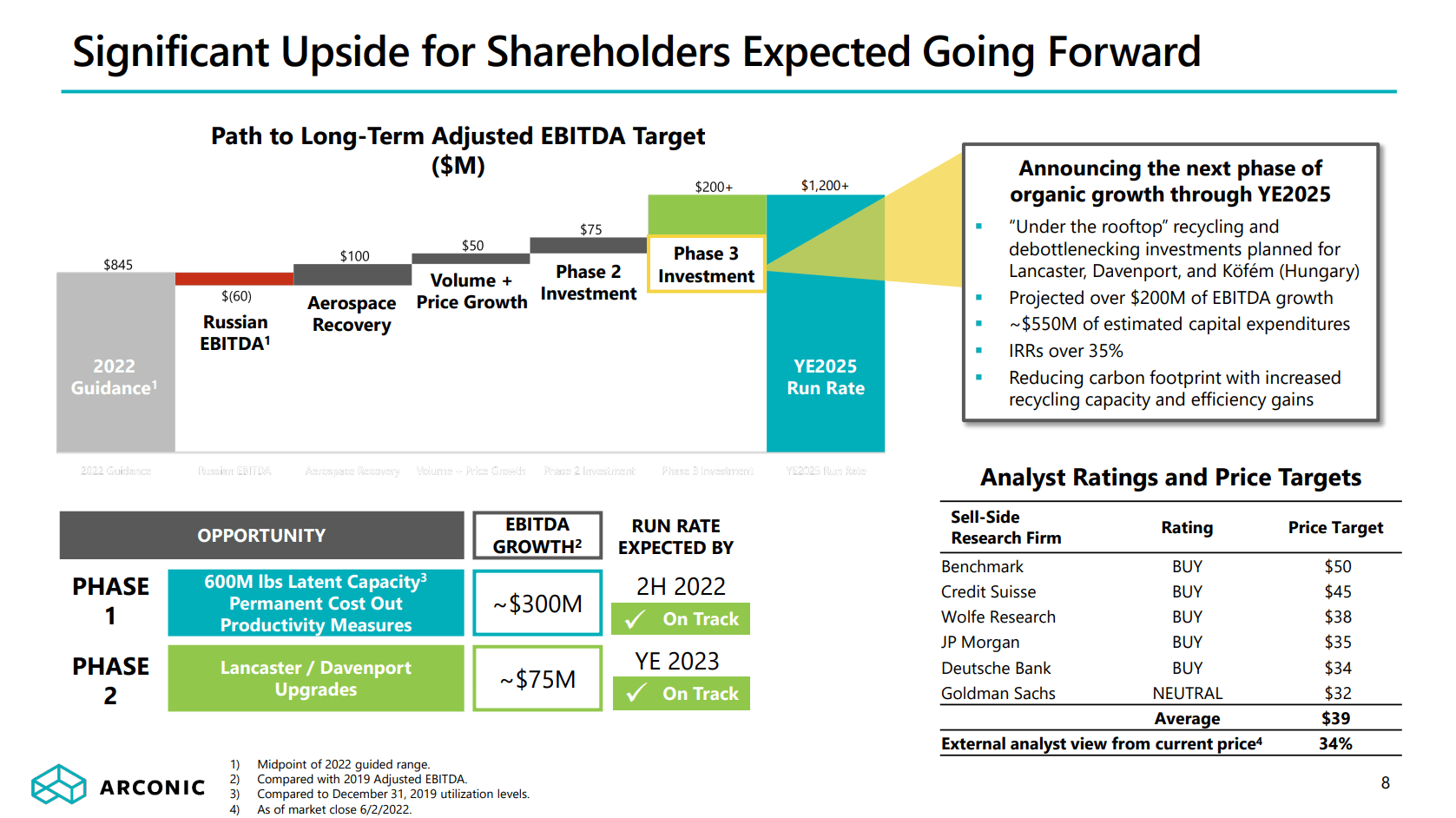

Current PE firm interest in Arconic comes at a quite opportunistic time as the company seems to be on the cusp of a substantial long-term adjusted EBITDA inflection given the ongoing strategic transformation. Since the separation of the company's jet engine component/aerospace fastening system business Howmet Aerospace back in 2020, ARNC's management has pursued a multi-stage operational improvement/cost-cutting plan aimed at boosting the company's bottom line. The first phase of the operational improvements (primarily through expanded production capacity and cost cuts) was completed in mid-2022 and is expected to deliver $300m in run-rate incremental EBITDA. Despite the completed Phase 1 (though not yet fully reflected), the company's adjusted EBITDA growth has so far been stagnant, with $635m in 2022 adjusted EBITDA vs $712m in 2021. This has been driven by a deteriorating macroeconomic environment impacting end-market demand, outages in the company's production facilities in H2'22 (~$100m adjusted EBITDA impact), and divestiture of Russian operations ($71m in 2022 adjusted EBITDA). Going forward, however, ARNC's long-term adjusted EBITDA seems likely to inflect materially above current levels:

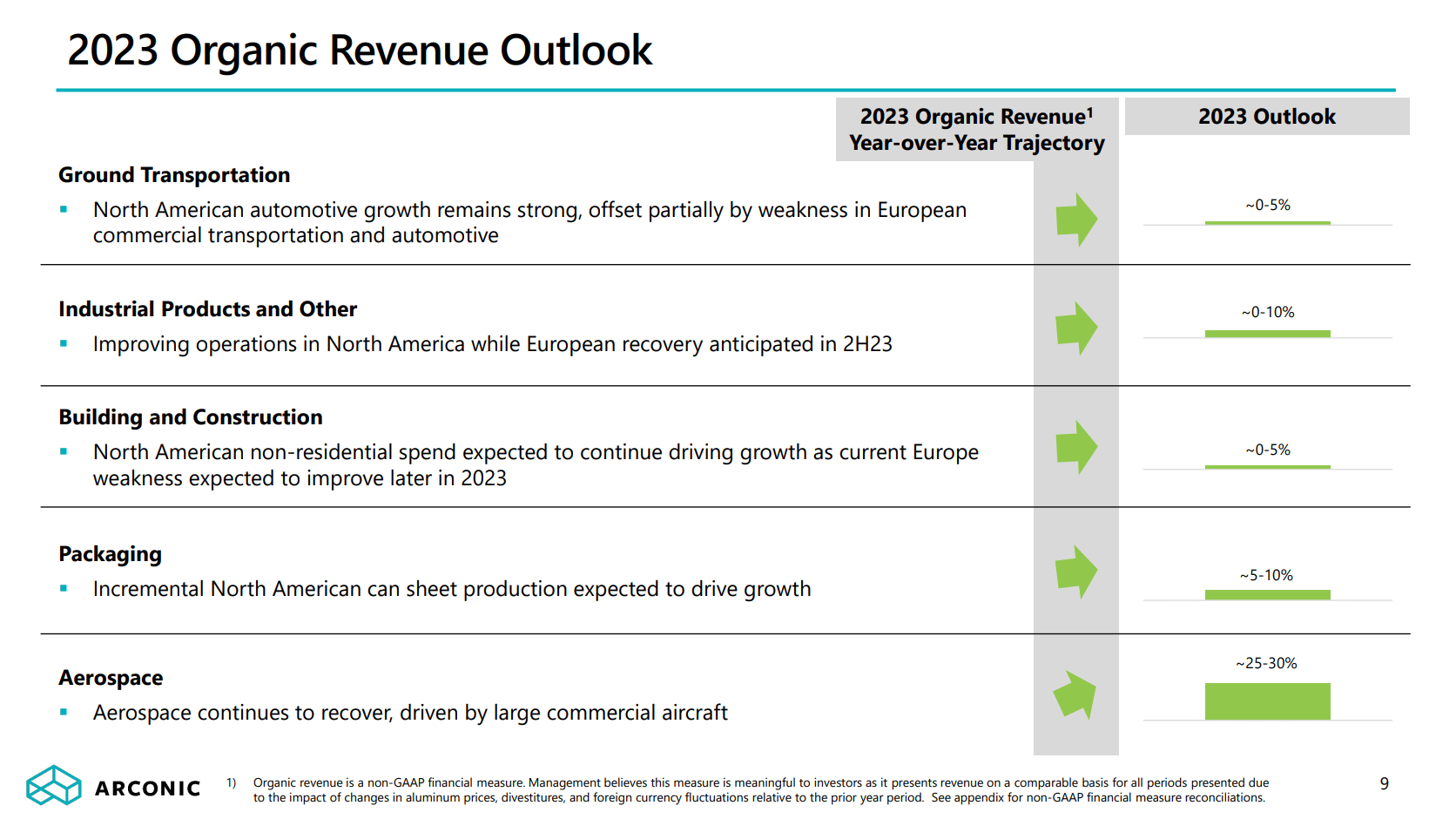

- Firstly, ARNC's management has recently guided for organic revenue growth in all of the company's end markets in 2023 (see below).

- Secondly, and perhaps most importantly, ARNC anticipates completion of Phases 2 and 3 of the strategic transformation plan focused on upgrades in several of the company's plants in 2024-2025. The upgrades involve increased casting capacities and debottlenecking initiatives aimed at boosting production volumes in two ARNC's facilities in the US and one in Hungary. The company has estimated total incremental EBITDA from these upgrades at $275m.

- Thirdly, the impact of outages experienced in H2'22 has already dissipated, with the management noting that the production capacity in facilities is already at or above pre-outage levels. Moreover, the management has hinted that the company will increase its maintenance capital expenditures (to $175m) to help mitigate operational issues, such as outages, in the future, including aging control and electrical systems.

These points suggest ARNC might very well generate >$1bn in adjusted EBITDA beyond 2025. The management's track record since 2020, including cost-cutting, share repurchases, reduction in defined benefit pension plan liabilities, and a number of new contracts signed (all detailed below), gives some confidence that these profitability targets can be reached successfully.

Worth highlighting that Apollo was in acquisition talks with ARNC back in 2018, however, both sides failed to reach an agreement. Apollo's size/credibility and long-standing interest in ARNC suggest it is highly familiar with the company's operational prospects.

ARNC's outlook for 2023 organic revenue growth by end-markets (Arconic Q4'22 Earnings Presentation) ARNC's anticipated EBITDA targets until 2025 (Arconic Investor Presentation, June 6, 2022)

{kind=link}

{kind=link}

Valuation

Relative valuation suggests there could be headroom for an offer above current share price levels. ARNC currently trades at 6.1x depressed 2022 adjusted EBITDA (7% margins). Similar size and margin peer CSTM (€2.1bn, 8%) is currently valued at 5.9x 2022 EBITDA. CSTM trades at 6.1x on management's 2023 adjusted EBITDA guidance. While ARNC's management does not specify 2023 adjusted EBITDA guidance, simply adding back the 2022 impact from facility outages would lower the multiple to 5.3x. Worth noting that comp CSTM is much more exposed to the European market, which has been significantly impacted by the recent macroeconomic turmoil, with 58% of revenues coming from the region vs less than 15% for ARNC (US is the primary market accounting for over 70% of sales). At 6.1x my conservatively estimated 2023 adjusted EBITDA (i.e., in line with CSTM), ARNC would be worth over $32/share. Note that this valuation gives little credit to ARNC's already achieved as well as planned EBITDA increases through capacity expansion and cost-cutting measures.

ARNC also seems cheap given the likely value of its Kawneer segment in a potential sale. Kawneer is a supplier of aluminum doors, windows, and entrances. ARNC's management has been seeking to sell the business since Jun'22. ARNC's management has underlined that similar companies have recently been acquired in the 9x-13x EV/EBITDA range - materially above current ARNC's EV/EBITDA. Kawneer is among the dominant players in the aluminum curtail wall market (see here ), suggesting a 13x multiple might be realistic. At this valuation, Kawneer would be worth c. $2.2bn. This would leave the remaining business at a 5x TTM adjusted EBITDA valuation. The RemainCo would primarily comprise ARNC's core rolled products division. Rolled products have admittedly displayed lower margins in recent years than the building and construction systems business (a part of which is Kawneer), with adjusted EBITDA margins of 8-9% in 2021-2022 vs 13-16% for building construction systems. Nonetheless, given that the ongoing operational improvements are primarily focused on rolled products, the current hypothetical RemainCo multiple on depressed TTM adjusted EBITDA seems too punitive in my view.

ARNC's management seems to agree that the company is cheap. The leadership bought back $185m and $161m worth of ARNC's stock in 2022 and 2021 at the average prices of $27-$33/share.

Arconic

Arconic focuses on producing rolled aluminium products, such as coils, sheets, and plates (80% of revenues). The other two segments are Building and Construction Systems (15%, includes aluminum door frames and window walls) and Extrusions (5%). Aluminum is the main production input, accounting for c. 70% of total costs. The primary end markets of the company's products are Ground Transportation (~42% of revenues), Building and Construction (~19%), Aerospace (~14%), Industrial Products and Other (~14%), and Packaging (~11%).

The management's track record since 2020 has been quite solid. Aside from share repurchases ($346m), the management has been active in a couple of areas:

- The company significantly reduced its defined benefit pension plan liability by transferring them to insurance companies in exchange for annuity contracts. This was a significant overhang previously, with $256m in annual US pension contributions paid in 2020. The figure has been reduced to $22m as of Jun'22. Net US pension liability stood at $1.3bn in 2020 vs $500m as of Jun'22.

- The company signed a number of new contracts. For reference, ARNC is expected to generate $3.5bn in revenue from long-term contracts recently signed in the aerospace and packaging segments.

Arconic Investor Presentation, June 6, 2022

{kind=link}

Arconic has a significant institutional ownership, with 49% of the stock held by five institutional investors, including BlackRock, Vanguard, FMR, State Street, and Orbis Investment Management.

Sachem Head

Sachem is a hedge fund with over $6bn in AUM founded by former Pershing Square veteran Scott Ferguson. The hedge fund has so far displayed a solid investing track record, with 22-46% returns generated in 2019-2021 ( here and here ). Sachem Head has already run a number of successful activist campaigns, including at US Foods (settlement in May'22 leading to CEO stepping down and three new independent directors appointed), Autodesk (settlement in 2016 achieved in tandem with another activist Eminence Capital, three new directors added) and Olin (agreement reached in Mar'20 to appoint two directors to the board). Given the date when Sachem Head's stake in ARNC was reported, it is likely that the activist amassed its position above current share price levels.

Risks

- A notable risk here is ARNC's so-called Grenfell liability. In 2017, the Grenfell Tower in London caught fire, resulting in fatalities, injuries, and damage. Arconic's subsidiary supplied a cladding system fabricator to the property which reportedly caused the fire. A number of lawsuits have been filed against the company since and the trial has been ongoing for five years. It is not clear what size of damages ARNC will need to pay, however, these might range in hundreds of millions/billions. A positive here is that during the most recent conference call, ARNC's management hinted that the US litigation claims under Behren lawsuit have been fully and finally dismissed.

- ARNC's management owns little of the company's stock (<2%) and is compensated quite generously. For reference, the CEO received $8m in total compensation in 2022.

Conclusion

At current prices, ARNC presents an interesting event-driven investment setup. The reported interest from a number of private equity firms, coupled with the opportunistic timing, suggests a company sale might be brewing here. Relative valuation suggests a potential acquirer might be willing to pay up significantly above current share price levels.

For further details see:

Arconic: Company Sale Is Likely