ARNC - Arconic: Unrolling Growth Prospects

Summary

- The Arconic Corporation divestment of Arconic SMZ in Russia weighed on the Q4 performance while improving the company’s operating leverage position.

- On the upside, Arconic prospects in North America remain resilient; on the downside, EU macro weakness could restrain the recovery of the end markets.

- I have updated the valuation with a higher target price, as I am more bullish on Europe’s automotive demand, and expect Arconic Corporation management to revise upward its revenue outlook.

Arconic Corporation (ARNC) took a dip after reporting the fourth quarter prints , since the divestment of its Russian facility impacted the company's performance. However, I expect the company to free up operating leverage out of this move, due to the increased exposure to the higher margin segments. In the meantime, the company is content with the strong demand steaming from North America, while management is concerned about the weakness of the EU economy, which could affect the main segment's performance.

Regarding the outlook for the construction and industrial market, I would most likely agree with the management's expectations. However, I am more bullish on the prospects of the Ground Transportation segment, as the EU automotive industry is gaining moment, while concerning heavy vehicles market, I expect it to recover in a while. Additionally, ARNC is taking prudent measures to improve its cost profile and address the operating challenges going forward. I am more bullish on Arconic Corporation now, and with this piece, I will update my previous coverage on Arconic going through financials, growth prospect and valuation.

Arconic Financials and outlook

Arconic experienced an 8.9% YoY decrease in Q4 2022 total revenue, which amounted to $1.9 billion, and was significantly impacted by the divestiture of the Arconic SMZ (Samara plant in Russia). Segment-wise, the Extrusions business, along with Building & Construction Systems (B&CS) delivered strong performance of 25.3% and 16.5% YoY, respectively. On the downside, the Rolled Products segment registered a 14.2% YoY drop, as the operating challenges at the Lancaster plant impacted the sales volume and net productivity, and weighted on the overall quarterly performance.

Q4 financial results (company reports)

A breakdown by end-markets revealed that sales to the Aerospace industry outperformed significantly, boasting a 40% YoY growth. Another growing end-market was Building and Construction, which registered a 2% YoY increase. The sales to all other markets followed the downside trend during the fourth quarter. In particular, Ground transportation registered an 11.3% YoY drop; Industrial products followed with a 15.1% YoY decrease due to operational challenges in North America and a weak European market; Packaging marked a 28.7% YoY fallout on the back of a discontinued Russian business.

Performance by end-markets (company presentation)

The bright point amid the above negative figures is that Arconic calculated organic growth rates (which excludes the effects of some one-offs) to be positive, with the exception for Industrial products.

Moving on, adjusted EBITDA for the quarter came 12% lower YoY to $154 million, where favorable pricing was not able to cover both the inflated cost pressure and net productivity loss. However, the respective margin decreased only marginally to 7.9%, due to the decrease of exposure to the Packaging segment following the divestiture. Bottomline, the company ended Q4 with a net loss of $2.62 per share, which included a $304 million loss related to the sale of Arconic SMZ, compared to $0.37 loss per share a year ago.

Going forward, ARNC is well positioned among the secular growth trend for aluminum demand across the company's each business line. I will not focus on the long-term drivers, as we already discussed them in my previous pieces about aluminum stocks. Rather, let's discuss the aluminum price prospects.

Aluminum price (USD/mt) (tradingeconomics.com)

Although the prices declined to around $2 400/mt from the record levels in March last year, the long-term nature is still there and may appear. Specifically, I believe the green trends will lead to a reduction in production capacity, which uses coal-fired electricity to power aluminum electrolysis. Thus, in my view, could force aluminum into short supply, and lead to a further uplift in the metal's prices.

Concerning the aluminum trade, the U.S. plans to dampen RUSAL's aluminum by preparing a step to impose a 200% tariff on Russian-made metal. I will share some thoughts about this matter from my piece on Alcoa ( AA ):

Back in 2018, after the US imposed sanctions on Rusal and the LME blocked its metal, aluminum prices jumped 35% in a matter of days. Thus, a complete ban on the supply of Russian aluminum by the US could lead to the metal prices skyrocketing back to $ 3 000/mt levels.

The sharp increase in the tariff will make the export of Russian aluminum to the US almost impossible. No doubt why some upstream players are urging actions against Russian metal, as this will benefit the American aluminum producer. However, I think that this shouldn't be implicitly taken as good news for downstream players in the industry. Let me explain. Since the downstream companies pass the aluminum volatility on to their customers, the metal prices do not affect the companies as much as the dynamics of the end-markets they serve do. However, the downstream producers pass on the increased aluminum costs only if the end-markets can afford it. Moving to the point, despite the key end-markets (auto, building, aerospace, packaging) are showing a sight of recovery, the demand is still weak in my view, especially amid the high macro uncertainty. As a result, the eventual hike in aluminum prices could put Arconic in a position of not being able to fully pass on the increased metal costs, thus deteriorating its operating profitability.

With the above in mind, I don't think such radical actions against Russian aluminum will take place. If they will, this could have a great impact on the further development of the aluminum industry.

With the Q4 report, the executives revealed their 2023 outlook of adjusted EBITDA to come in a $650-700 million range due to widespread economic challenges in Europe . The company is also expecting $250 million free cash flow, which will be supported by a working capital release. In addition, Arconic delayed its Lancaster Phase 2 investments, and switched its CAPEX focus more on maintenance. I see this prudent move will allow the company to prevent operating issues in the future, or at least limit their potential negative effects on its financial performance.

Arconic sees the North American demand in strong shape in all business segments. However, the management has set a conservative $8-8.5 billion revenue target due to European macro weakness, which is expected to impact the transportation, industrial and building end-market performance of the company.

The management's revenue outlook (company presentation)

Regarding the latter two, I tend to agree and incorporate 5% growth for both Packaging and Building and Construction end-markets, as the EU doesn't have an infrastructure bill in place like the one in the US. Moreover, Europe appears to be concerned more with investment in digitalization and green ambitions. Regarding the company's Ground Transportation business line, I expect 10% growth in 2023. The reason I am more bullish on this segment could be evidenced by the following graph.

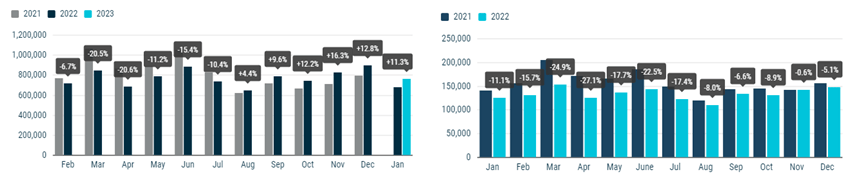

New passenger car (left) and commercial vehicle (right) registrations in the EU (ACEA)

{kind=link}

The automotive market in Europe is exhibiting a good path of recovery, marking the sixth consecutive month of growth. Not so with commercial vehicles, which are still lagging behind. However, the trend is starting to normalize and I expect the commercial vehicles market to recover in 2023, as the chip shortage problem is gradually appearing in the rearview mirror.

Moving on, for the Packaging end-market, I will apply 10% growth as the Tennessee facility has reached the planned production levels, while for the Aerospace, 30% growth, due to the continuing recovery of aircraft build rates. Overall, taking into account the company's outlook and my expectations, the first-quarter and full 2023 Sales and EBITDA are as follows

Forecasts for Q1 and 2023 full year (company reports; author's estimates)

I assume 10.8% sales growth in 2023 for the Rolled Products segment, underpinned by the resolution of the operational challenges at Tennessee and Davenport facilities. I also assume the B&CS and Extrusions segments will register a 5% and 18.3% increase. With the above expectations, total sales should be $9.9 billion and mark 10.3% growth in 2023. I expect the gradual strengthening of the end-markets and moderate aluminum price volatility, which will allow the company to pass on the increased cost on to the customers. Thus, I expect COGS to follow top-line performance in 2023, although some operating challenges should not be ruled out. I estimated full-year EBITDA at $856 million on a margin of 8.7% (+80bps), as the divestiture of Russian operations should allow the company to achieve a more favorable sales mix, due to the less exposure to lower-margin Packaging end-market. Still, I expect profitability in Q1'23 to deteriorate on the back of Lancaster challenges.

ARNC Stock Valuation

In terms of valuation, to the aforesaid Sales and EBITDA forecasts, I decided to apply sector EV/Sales and EV/EBITDA forward multiples (40:60 weight), derived from Arconic's main comps represented by Constellium ( CSTM ), Kaiser Aluminum ( KALU ) and Norsk Hydro ( NHYDY ).

Peer valuation (Seeking Alpha; company reports, author's estimates)

I added the EV/Sales to the model with a 40% weight, as Arconic has superior growth prospects compared to the sector, evidenced by Seeking Alpha growth grade.

Applying my financial estimates, ARNC is currently trading at EV/Sales and EV/EBITDA forward multiples of 0.5x and 5.4x, respectively, which represent a prominent discount to the peer's median multiples of 0.7x and 5.6x. With the latter multiples, the implied enterprise value should be $5.5 billion. Adjusting for cash position, IB Debt and pension-related liabilities, the implied equity value per share should be close to $32.1 with a potential of 39% to the upside. The valuation yields a higher target price, compared to that in my previous article, as I am more bullish on the company's recent development and growth prospects. In addition, Arconic concluded its previous share repurchase program, and has another two-years $200 million authorization, which will give a spot to the company's stock performance.

Risk factors

The main risk relevant to Arconic remains production outages, which impacted on the company's operating performance in 2022, while stagnation in the key end-markets due to recession fears could restrain the company's profitability going forward. In addition, aggravation of the military conflict in Eastern Europe and potential sanctions on the Russian export of the metal would be a source of price volatility and distortion of global aluminum trade flows.

Conclusion

I am more bullish on Arconic Corporation's prospects due to the gradual improvement of the demand in the strategic verticals amid secular growth trends. In light of economic challenges in Europe, Arconic is focusing on its casting and recycling projects which will improve the company's cost profile before bringing the Lancaster Phase 2 investment. In addition, ARNC is setting on a more favorable sales mix, which should add some operating leverage. I consider Arconic Corporation an attractive investment opportunity owing to its strong balance sheet , free cash flow generating capacity, attractive valuation, which combined with the growth prospects, puts the company in the right position to unroll future expansion.

For further details see:

Arconic: Unrolling Growth Prospects