ARCO - Arcos Dorados Holdings: Attractive At Current Level

Summary

- ARCO is a leader in the QSR industry, which is growing faster than other foodservice segments.

- Arcos Dorados has been investing in its online capabilities and is planning to continue with 25% of capex for the next few years, mostly going to digital strategy.

- Arcos is trading at steep discounts of almost 21% vs. its 3-year average and 10% vs. its 5-year average, which is unjustified in my view.

- My $12 NTM price target is derived through an assumed EV/EBITDA of 7x at the end of FY23.

Thesis

I believe freestanding units offer a good value proposition, given their drive-thru and delivery capabilities, and customer traffic that isn't dependent on shopping malls -which could be impacted by social distancing measures and an adverse consumer environment- a reason why the company is planning to invest heavily in this format. As the performance of these units throughout the last quarters has improved considerably vs. pre-pandemic sales, I expect Arcos Dorados Holdings Inc. ( ARCO ) to focus on these formats, with 90% of the 2022-24 expected 200 openings planned to be freestanding, a higher proportion vs. the 40-80% range in previous investment plans. I believe that the QSR industry is well-positioned to grow faster than other foodservice segments, and ARCO's investments in digital strategy position the company well to close the valuation gap vs. Peers. I keep a price target of $12 on the stock derived from an assumed EV/EBITDA of 7x at the end of FY23.

{kind=link}

Company Background

Arcos Dorados is the largest McDonald's franchisee in the world operating nearly 2300 McDonald's. In terms of revenue and number of outlets, accounting for 3.1% of McDonald's sales in 2021. A majority of restaurants are operated by ARCO while the rest are sub-franchised. Depending on the location, Arcos Dorados offers four types of restaurants: 1) freestanding, 2) in-store, 3) foodcourt, and 4) in-mall shops.

Industry Overview

QSRs: positioned for growth

Excluding the pandemic, the growth in the overall foodservice industry, improving consumer lifestyles, and the adoption of on-the-go purchases, have driven consumption in quick service restaurants (QSRs). Additionally, the accessibility of healthier fast-food alternatives, together with advanced recipes of organic and plant-based ingredients are another growth factor for the industry. Technology has certainly helped, fostering convenience -a highly relevant factor in today's consumer habits and needs, and where QSRs play a leading role in the eating experience, via mobile applications and 3rd party vendor apps, along with touchscreen kiosks and kitchen-display screens, improving customer service and experience.

Globally, the full-service restaurant industry had a market size of $1.2 trillion in 2020 , and is predicted by Statista to be valued at $1.7 trillion by 2027. Meanwhile, the QSR industry generated over c.$736bn in 2020 , and is expected to reach c.$931 billion by the end of 2027 (a 3.4% CAGR in 2020- 27), according to Allied Market Research. The penetration rate has surged due to the gain in digitalization from QSR vs casual restaurants, and should bring further market share gains for the industry.

The QSR leader worldwide by number of branches is McDonald's, leading with c.38.7k stores in over 100 countries, and with c.20k units more than its direct competitor Burger King as of June, 2022. Subway is at a close 2nd position with c.36k units, but I think it is a less direct competitor vs McDonald's. KFC leads in the chicken segment (c.24.1k units), while Pizza Hut dominates the Pizza segment with c.18.7k outlets.

Top 10 largest fast food chains worldwide (Alltopeverything)

QSRs in LatAm: an even healthier picture

QSRs have had their ups and downs in Latin America, and while countries like Brazil have numerous McDonald's restaurants, other countries such as Bolivia have zero, amid consumers not receptive to fast food chains.

Overall, the QSR industry topped ~$270 billion sales in LatAm during 2021, and the absolute country leader in the region was Brazil, followed by Argentina and Mexico. The industry grew 2.3% y/y in 2021,a CAGR of 2.6% since 2016 vs a global fall in the CAGR rate of 0.2%. Additionally, LatAm's fast food and QSR market is projected by Global Research Consulting to grow at a significant CAGR of 6.9% between 2020-26, which is attributed to the changing food consumption behavior of consumers such as increased eating and snacking away from home, and growing urbanization. While the pandemic has clearly decelerated the former, I consider that a higher reliance on familiar brands and on the formal restaurant segment to eat in healthier conditions support QSR growth. Macro factors such as a growing population, improving disposable income, and the surge in digitalization in the region are further growth drivers. Even amid the current inflationary environment, I view McDonald's as well positioned given its broad portfolio with low entry prices, and freestanding restaurants that don't rely on shopping mall traffic.

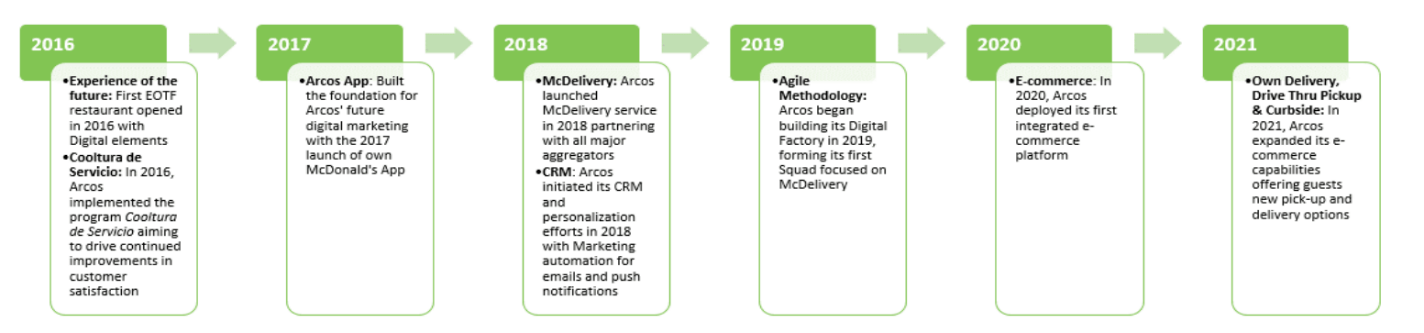

ARCO: Digital strategy

Arcos Dorados has been investing in its online capabilities, and is planning to continue with 25% of capex for the next few years, mostly going to digital strategy. Its Three Ds of strategy are Digital, Delivery and Drive-thru, and its mobile app already has over 62mn downloads. Omnichannel capabilities such as order & pickup, among others, are being developed.

Delivery should contribute to top-line growth, although at a slower pace vs the 2020-21 tough comp base. Online growth will add to recovering on-premise performance, and delivery still represents more than 10% of the company's sales, which I expect to continue, given the company's focus in this area. Given the operating leverage from the omnichannel and digital channels -deliveries, drive-thru, kiosks, together with higher average spend and better margins, investing in these channels are expected to provide accretive growth.

{kind=link}

Besides the online channel, the company has been investing in its omnichannel experience at the store. Arcos Dorados has more than 800 Experience of the Future (EOTF) restaurants, which include self-order kiosks that helps drive sales via customized orders -these generate 15-20% higher average checks vs the counters and reduce queues, improving both customer experience and employee efficiency. Self-order kiosks account for more than 50% of on-premise volume in EOTF restaurants in 2021 vs under 30% in 2019.

Current valuation level represents an attractive entry point

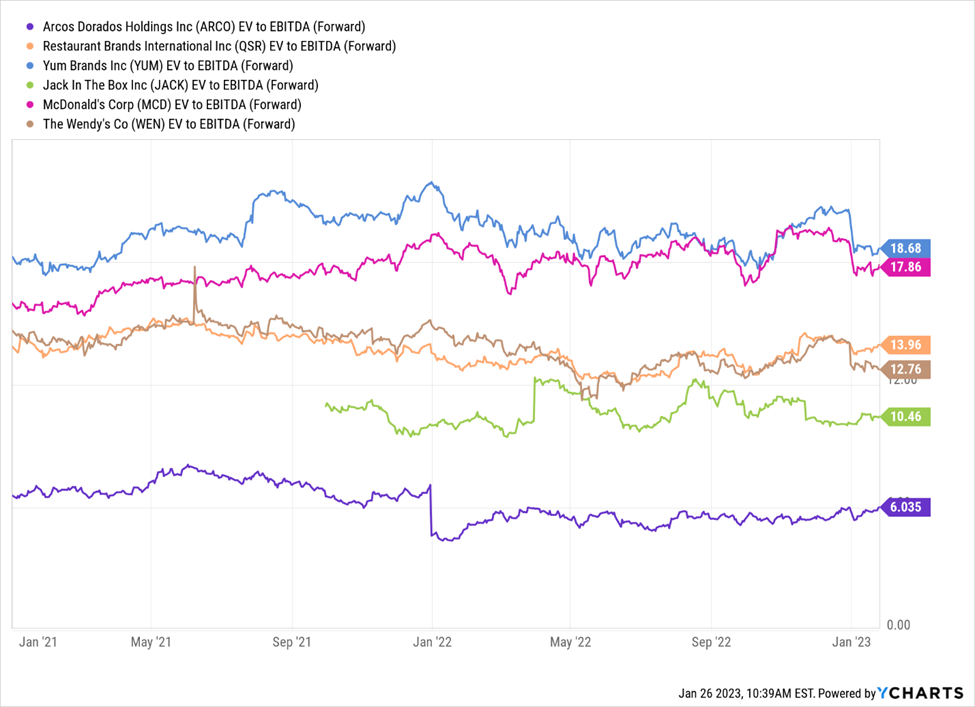

At 6.03x forward EV/EBITDA, Arcos is trading at steep discounts of almost 21% vs its 3-year average, and 10% vs its 5-year average, which is unjustified in my view, as the company has faced harder conditions both internally and externally but is now better positioned given the aforementioned strategies, such as more focused, omnichannel growth.

If Arcos already trades at a discount vs its historical levels, the difference vs peers is even larger. On average, peers are currently trading at almost 2x Arcos' current level, while historically, the discount was closer to 30%. In the meantime, the profitability gap has closed, and Arcos Dorados has reached record profitability levels; while some margin contraction is expected next year, I forecast margin levels that continue well above its historical levels. I continue to expect peers to trade on average at double-digit levels and Arcos at single-digit levels - given lower margins and the more volatile LatAm exposure-, but the high and increased discount is in my view, unjustified. My $12 NTM price target is derived through an assumed EV/EBITDA of 7x at the end of FY23.

{kind=link}

Risk

Competition

The foodservice industry is highly competitive, partially due to relatively low barriers to entry, which means the company competes with a variety of participants ranging from well-established restaurant chains (both national and international), to smaller local restaurants, street vendors, and informal competitors. As discussed earlier, informal food market represents around 60-80% of the whole foodservice sector in some countries of LatAm. This leads to a highly competitive environment, although in my view, the McDonald's brand and Arcos Dorados scale of operations provide a solid positioning in the LatAm region.

Final Thoughts

I see Arcos Dorados as solidly positioned to weather external headwinds. Its investment in digital strategies should drive better performance and contribute to accretive growth, while the QSR industry, which it is a leader in, is growing faster than other foodservice segments. Despite concerns about foodservice given its discretionary nature, I see QSRs as the most defensive segment within this sector. Given Arcos' steep valuation discount, I keep a buy rating on the stock with a price target of $12 on the stock.

For further details see:

Arcos Dorados Holdings: Attractive At Current Level