ARQT - Arcutis Biotherapeutics: Market Discounting Zoryve Momentum

Summary

- The market has discounted momentum around Arcutis' Zoryve label.

- This looks overdone and investors appear to have overlooked the additional data points surrounding the segment.

- We are looking for positive numbers in the company's upcoming FY22 earnings.

- Alas, we are entering with a long position leading into this date.

Investment Summary

Arcutis Biotherapeutics (NASDAQ: ARQT ) continues building momentum around its Zoryve segment with a string of recent advancements at the back end of FY22' and into the new year. Surprisingly, the immediate price response following the updates was largely negative. However, shares have lifted off 52-week lows last month, and we believe the market may have overshot its selloff.

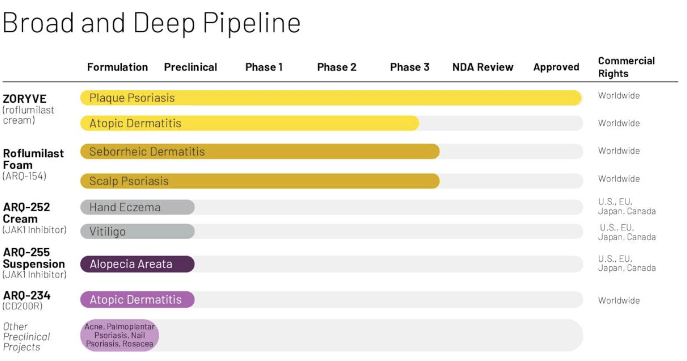

We are now constructive on ARQT with several factors supporting a buy thesis including 1) execution on its Zoryve pipeline, 2) robust efficacy data with the label meeting primary and secondary endpoints, 3) additional phase 3 assets due for pipeline conversion, 3) re-rating to the downside with attractive discount to broad sector, 4) Zoryve competing on-top of the current standard of care [corticosteroids] not directly against it, 5) Zoryve added to the Express Scripts national formularies. The company left Q3 last year with ~$480mm in cash and looks well capitalized to continue driving shareholder value with the aforementioned points. It's full pipeline is observed in Exhibit 2. Net-net, we rate ARQT a buy for those speculating on late-stage clinical assets.

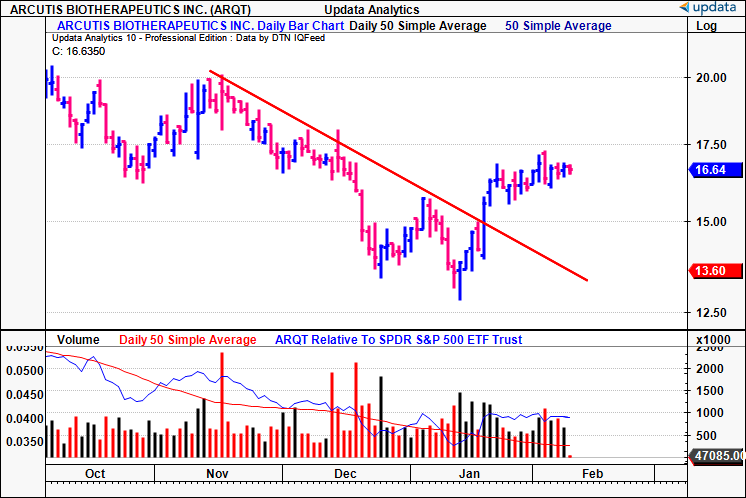

Exhibit 1. AQRT breakout above downtrend

{kind=link}

Exhibit 2.

Data: AQRT Investor presentation

{kind=link}

Zoryve entrance to atopic dermatitis treatment market

Atopic dermatitis ("AD") is the most prevalent form of eczema, impacting ~10mm children and 16.5mm adults across the U.S. The AD treatment market is expected to see significant growth in the coming years, with projections estimating its value to reach $22.6Bn by FY31', growing at a CAGR of 15.1%. Additional research points to 9% CAGR into FY30'. This growth is attributed to an increase in product approvals and the advent of biologic treatments for management. In recent years, notable advancements in the field have been made, with FDA approvals to labels such as Dupixent by Sanofi [ages 6 months to 5 years], and AbbVie's RINVOQ, approved for the treatment of severe AD in both children aged 12+ and adults. This latter medication has been specifically recommended for those who have not responded to previous treatments involving injections or pills. Moreover, Opzelura, Dermavant and Vtama are Zoryve's competitors in the topical cream segment.

It's therefore pleasing therefore to observe that ARQT made several recent advancements in its Zoryve segment:

- First it announced the cream has been added to the Express Scripts national formularies, providing access to over 26 million commercial lives in the US as of November 18. This is an essential progression, seeing as the label is prescription only. This comes after approval in July FY22'.

- Additionally, Zoryve demonstrated efficacy in the 2nd pivotal INTEGUMENT-2 phase 3 trial for the treatment of AD. INTEGUMENT-2 showed the cream achieved the primary endpoint with 29% of patients receiving treatment achieving investigator global assessment ("IGA") success, compared to just 12% in the control group. The trial also met key secondary endpoints, such as a 75% improvement in eczema area and severity index ("EASI-75") at week 4, achieved by 42% of patients in the Zoryve arm compared to 20% in the control group [p<0.0001]. Safety-wise, the drug was well-tolerated with a low incidence of treatment-emergent adverse events ("TRAEs") that were mostly mild to moderate.

- The company intends to seek FDA approval for the cream for the treatment of mild to moderate AD in patients aged 6+, filing of a supplemental new drug application ("SNDA") expected in H2 FY23'. We like the move of targeting the 6+ range, as it lifts the revenue capacity of the label by distributing the addressable market across a broader age range.

- The company is also enrolling a third pivotal Phase 3 trial [INTEGUMENT-PED] to evaluate Zoryve cream 0.05% in children 2 to 5 years of age with mild to moderate AD, with top-line data expected at some point during mid FY23'.

- It also announced positive long-term data from its Phase 2 study evaluating the long-term safety of once-daily Zoryve in adults with chronic plaque psoriasis. Results indicated that over 50% patients [n=185] achieved an IGA score of either clear, or almost clear [IGA 0/1], and median duration of clear or almost clear was >10 months. We'd note rates are consistent with prior trials and remained unchanged over the course of the 52-weeks of the study. Safety data again held up well and was well-tolerated.

The run of clinical trial momentum is attractive and appears to be overly discounted by the market. Initially driving the selloff last year, was ARQT's decision to acquire Ducentis BioTherapeutics Ltd, with a cash-scrip consideration of $16mm in cash and $14mm in ARQT stock. Yet, the transaction has potential to broaden ARQT's AD profile via access to the DS-234 compound from Ducentis, albeit in the biologics division. We won't see evidence for this until it pulls through to earnings, however.

Liquidity

The company left the quarter with ~$480mm in cash and marketable securities at the exit of Q3. For the 9-months to September 30th, it had run through ~$185.6mmm in CFFO, and, subsequently secured a $300mm cash inflow made up of $161.5mm in stock issuance and $125mm from issuance of interest bearing debt. Net-net, it burnt ~$7mm in cash after the entire period. Based on these figures, and the rate of cash-burn at the operational level, we estimate the company has a runway of ~2.5 years on its current position [Exhibit 3].

Exhibit 3. ARQT estimated cash runway, based on current position Q3 FY22'

Note: Figures are calculated using ARQT's cash flows to the 9 months ending September 30, 2022. "Estimated cash runway" is measured in years. (Data: Author, using data from ARQT's SEC Filings)

This runway is quintessential to sustain the firm's planned growth activities in FY23', and this adds another bullish tilt to the risk/reward calculus.

Risks and conclusion

There are several risks to the investment thesis. Namely, the market's muted reaction to ARQT's recent updates. There is a large risk this could continue, and that competitors listed could instead attract the risk capital. The volatility of small-cap, pre-revenue biotech companies is also a potential concern, given the potential for wide price swings. We encourage investors to realize these risks.

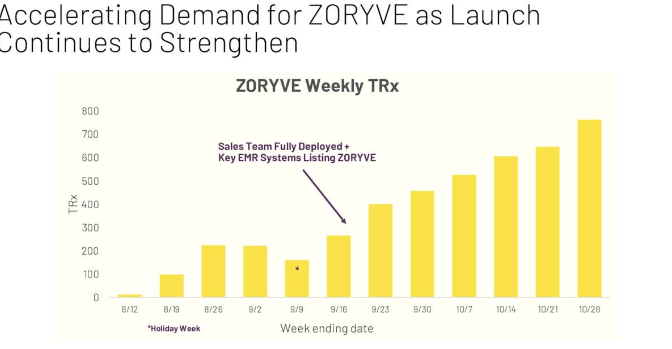

With respect to our investment thesis, we believe the stock has been oversold and we are expecting positive updates in its FY22 earnings at the end of February [Exhibit 4]. Net-net, we rate ARQT a buy, looking to play the momentum around its Zoryve label.

Exhibit 4.

Data: AQRT Investor presentation

{kind=link}

For further details see:

Arcutis Biotherapeutics: Market Discounting Zoryve Momentum