ARDC - ARDC: A Very Good Choice For Anyone Seeking A High-Yielding CEF

2023-08-14 14:30:11 ET

Summary

- The high level of inflation in the US is making it difficult for Americans to maintain their standard of living.

- Ares Dynamic Credit Allocation Fund, Inc. offers a high level of income for investors through its portfolio of debt securities.

- The fund's use of leverage and allocation to floating-rate securities helps to boost its effective yield and protect against rising interest rates.

- The fund's distribution is fully covered by NII so it will fluctuate somewhat with interest rates but it ensures the long-term sustainability of the fund.

- The fund is currently trading at a reasonable discount to net asset value.

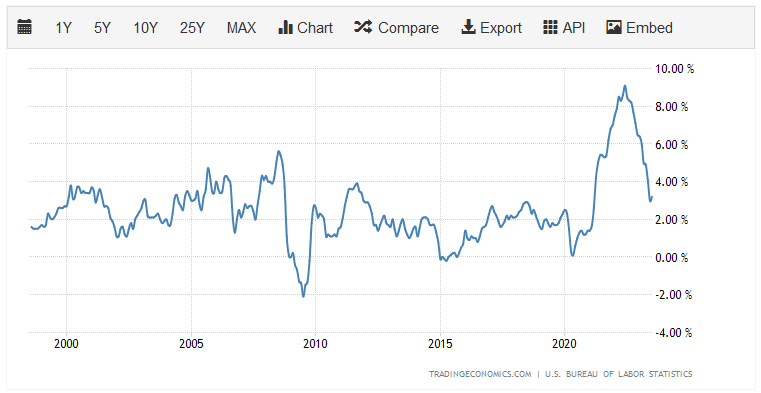

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high level of inflation that is pervading the economy. This inflation has driven up the costs of all our daily lives, making it ever more difficult to maintain the standard of living that most of us have become accustomed to. We can see the extent of this inflation by looking at the consumer price index, which claims to track the price of a basket of goods that is regularly purchased by the average person. This chart shows the year-over-year rate of change of the consumer price index during each month in the past 25 years:

{kind=link}

As we can clearly see here, the year-over-year rate of change in the index has been substantially higher than normal ever since the COVID-19 lockdowns. This is due to the fact that the Federal government and the Federal Reserve increased the money supply by 40% during that period without a commensurate increase in actual economic output. Thus, more units of currency were attempting to purchase each unit of economic production, pushing prices up. This is the reason why real wages have declined over the past two years, as prices have generally risen more rapidly than wages. As approximately 64% of Americans live paycheck-to-paycheck , this situation has caused incredible strain on most households in the nation. We have started to see people resort to desperate measures such as dumpster diving and pawning possessions simply to make ends meet. We have also begun to see a rise in the number of people taking on second jobs in order to obtain the extra money that they need to maintain their lifestyles. In short, people are desperate for any means through which they can increase their incomes in order to maintain their lifestyles in today’s environment.

As investors, we are certainly not immune to this need for higher income. After all, we require food for sustenance and energy to heat our homes. We also may desire an occasional luxury. These things all cost considerably more money than they did only two short years ago. Fortunately, we do not have to resort to some of the desperate measures that we just discussed in order to obtain the extra money that we need to maintain our lifestyles today. This is because we have the ability to put our money to work for us to earn an income.

One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in the generation of income. These funds are unfortunately not very well followed in the financial media and many investment advisors are unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have in order to make an informed investment decision. This is a shame because these funds offer a number of advantages over familiar open-ended and exchange-traded funds. In particular, a closed-end fund is able to employ a variety of strategies that have the effect of boosting their yields well beyond that of any of the underlying assets or indeed pretty much anything in the market.

In this article, we will discuss the Ares Dynamic Credit Allocation Fund, Inc. ( ARDC ), which is a fund that can be used by any investor that is seeking a high level of income from their portfolios. The fund yields 10.56% at the current price, so its income generation characteristics are undebatable. I have discussed this fund before, but a few months have passed since that time so naturally some things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Ares Dynamic Credit Allocation Fund has the objective of providing its investors with an attractive level of total return. This is a somewhat surprising objective, considering that the fund’s name implies that this is a fixed-income fund. Its portfolio confirms this as right now the fund is entirely invested in bonds, along with small allocations to cash and convertible securities:

CEF Connect

The reason that its total return objective is somewhat surprising is that bonds and other debt securities are by their very nature income vehicles. There is no potential for net capital gains with these securities because they have no inherent link to the growth and prosperity of the issuing entity. This is not too difficult to visualize. After all, an investor purchases a bond at its face value when it is issued, receives a steady stream of income in the form of coupon payments, and then receives face value back when the bond matures. Thus, the only investment return that is delivered over the life of the bond is the coupon payments made to the bondholders. For its part, the fund appears to recognize this as it does state that its total returns are expected to be primarily in the form of current income. From the webpage:

“Ares Dynamic Credit Allocation Fund, Inc. Is a closed-end management investment company. The fund’s investment objective is to provide an attractive level of total return, primarily through current income and, secondarily, through capital appreciation.”

Thus, investors should expect to receive most of the returns in the form of current income. This is totally acceptable for our purposes, as our basic thesis for investing in this fund in the first place is receiving current income.

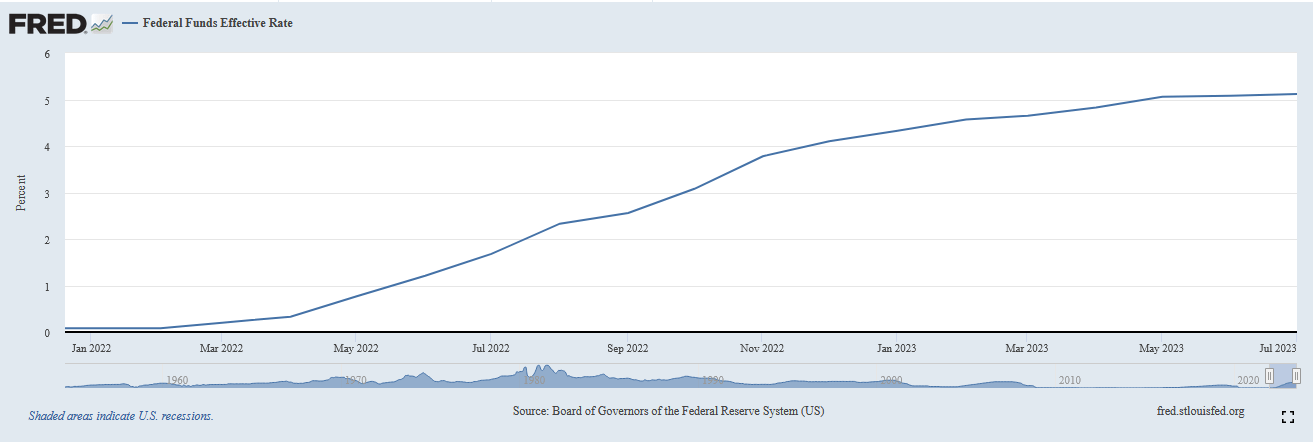

The fund states that it also aims to achieve some returns through capital appreciation. This is very difficult to achieve with bonds, although it is possible to generate some capital gains by trading bonds prior to maturity. This is because bond prices vary with interest rates. It is an inverse correlation, so when interest rates go up bond prices go down. The reverse is also true. In recent months though, the bond market has experienced the effects of interest rate hikes more than declines. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates as part of a campaign to get inflation under control. As we can see here, the effective federal funds rate has gone from 0.08% to 5.12% since the start of 2022:

{kind=link}

This is the biggest factor that has driven down the American bond market over the past eighteen months or so. Over the twelve-month period that ended on June 30, 2023, the Bloomberg U.S. Aggregate Bond Index ( AGG ) delivered a –0.94% total return. The index delivered a –13.01% total return for the full-year 2022 period. Thus, the decline in bond prices was sufficient to more than offset all of the coupon payments that were paid out by these securities. That is not really surprising though since fifteen years of very low interest rates have resulted in most bonds in the market trading with incredibly low coupon rates relative to their face values.

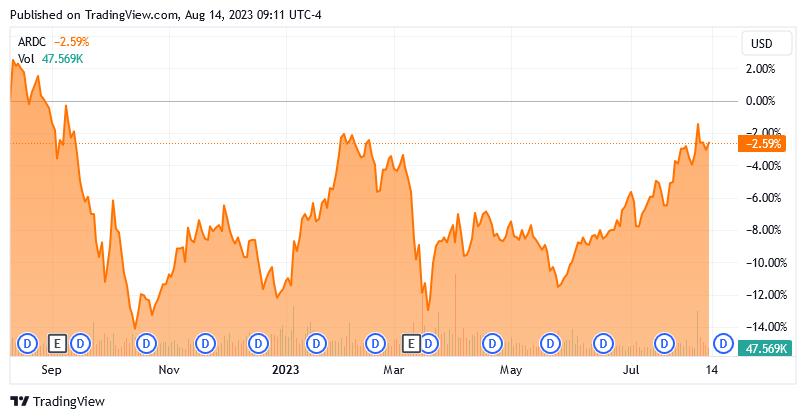

The Ares Dynamic Credit Allocation Fund has certainly been affected by the carnage in the bond market as well. Over the past twelve months, the fund’s share price has declined by 2.59%:

{kind=link}

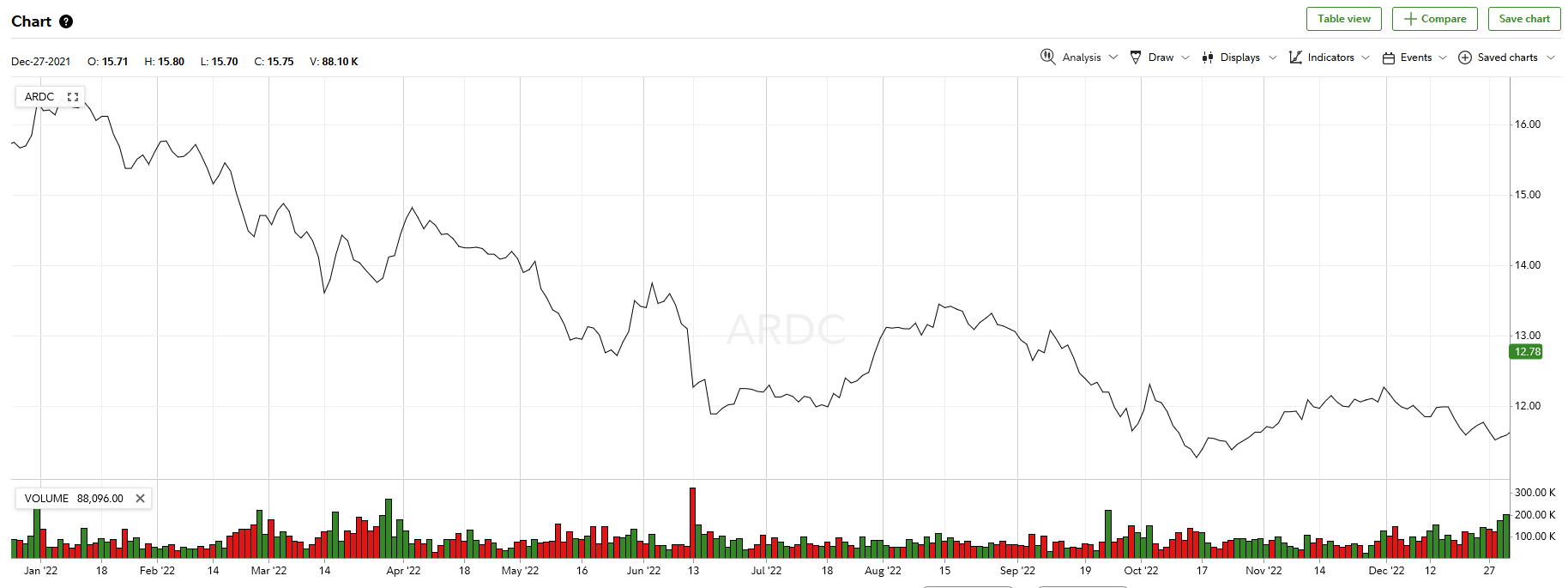

The fund also went from $16.33 per share on January 3, 2022, to $11.59 at the end of the year. That is a 29.02% decline over the course of the year.

{kind=link}

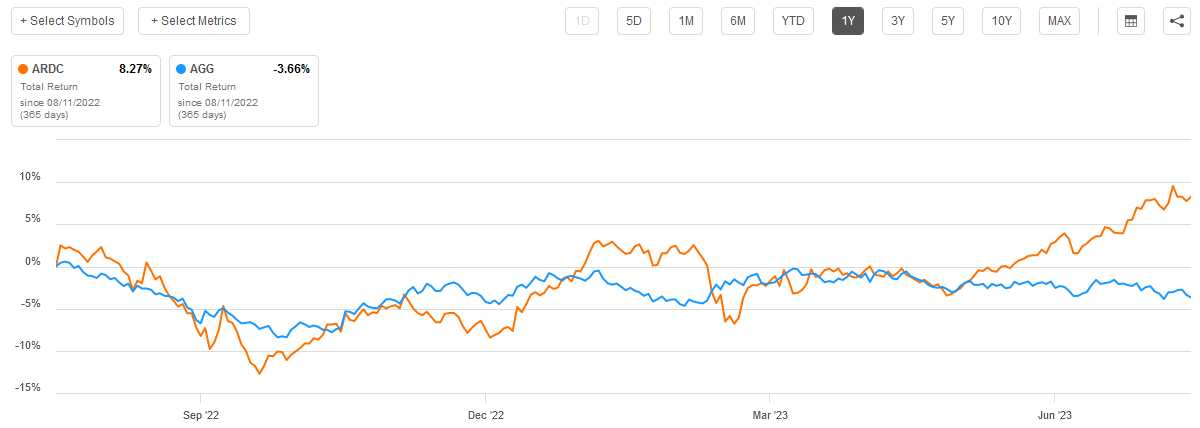

In the case of this fund though, the yield is high enough to offset a good portion of the decline in 2022. It is also more than enough to offset the decline over the past twelve months. In fact, this fund has managed to deliver a positive total return over the past year, which was more than sufficient to beat the index:

{kind=link}

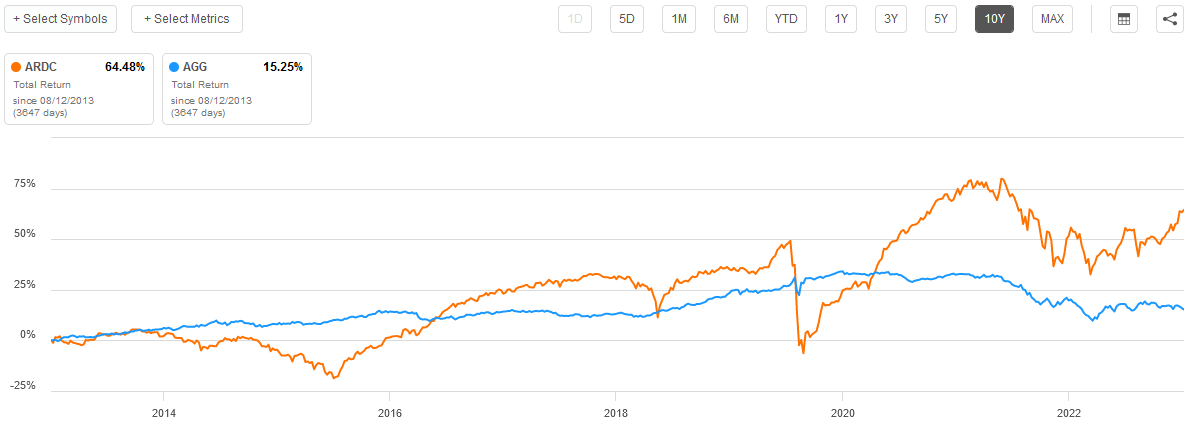

Clearly, we can see that the Ares Dynamic Credit Allocation Fund managed to beat the index over the past year in terms of total return, although it has not managed to do it consistently. The fund actually does much better over longer periods. For example, over the past ten years, the Ares fund managed to completely slaughter the aggregate bond index:

{kind=link}

Admittedly though, the Ares Dynamic Credit Allocation Fund includes some assets that the index does not. In particular, this fund includes floating-rate loans and other debt securities:

Ares Public Funds

We can see that 42.1% of the fund’s assets are invested in traditional fixed-rate bonds. These are the same type of securities that are in the index, although this fund is not purchasing bonds mechanically. As such, its bond holdings are not as diverse as they are structured in a way that the fund’s management thinks will deliver better performance than the market. Ares is pretty well-known as being a very high-quality management company in the debt space so the fund’s management certainly could enjoy some success here.

The key to this fund right now though is that 30.9% of the fund is invested in senior loans and another 30.3% is invested in collateralized loan obligations. These are usually floating-rate securities, which are quite advantageous right now. This is because floating-rate securities do not have the same problem that fixed-rate bonds have in a rising interest-rate environment. The reason why bond prices decline when interest rates rise is because brand-new bonds will offer better coupon yields in such an environment. Nobody will pay full price for existing securities when they can buy a brand-new bond with a better yield, so the price of the existing securities has to decline until they deliver a yield-to-maturity that is competitive with a brand-new bond with identical characteristics. A floating-rate security, such as the ones that comprise much of this portfolio, has a coupon that adjusts with the market so it will always deliver a competitive interest rate.

As such, these securities tend to keep a relatively stable value no matter what interest rates do. The presence of these securities thus prevents the fund’s portfolio from declining when interest rates rise as much as it would if it was entirely invested in traditional bonds. In addition, floating-rate securities cause the fund’s income to increase when interest rates go up. That is quite good for income-focused investors.

Leverage

As mentioned in the introduction, closed-end funds like the Ares Dynamic Credit Allocation Fund are capable of employing certain strategies that have the effect of boosting the effective yield of their portfolios well beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund is borrowing money and using that borrowed money to purchase various debt securities. This is the reason why the asset allocation chart above shows the fund’s bond holdings to exceed 100% of its assets. The strategy works pretty well to boost the effective portfolio yield though, as long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so this will usually be the case.

However, it is important to note that this strategy is not nearly as effective today with rates at 6% as it was eighteen months ago when rates were at 0%. This is because the difference between the fund’s borrowing rate and what it can get from the purchased securities is much smaller than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. That is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason. As of the time of writing, the fund’s levered assets comprise 34.13% of its assets so it is unfortunately slightly above this level. In this case, this is probably acceptable because it is not very much above that one-third level.

In addition, this is a debt fund and debt funds can usually carry a higher leverage than an equity fund because their assets are less volatile. That is especially true if the fund is investing in floating-rate securities. Thus, we probably do not have to worry too much about the fund’s leverage right now, but we also do not want its leverage to go up much more from its present level.

Distribution Analysis

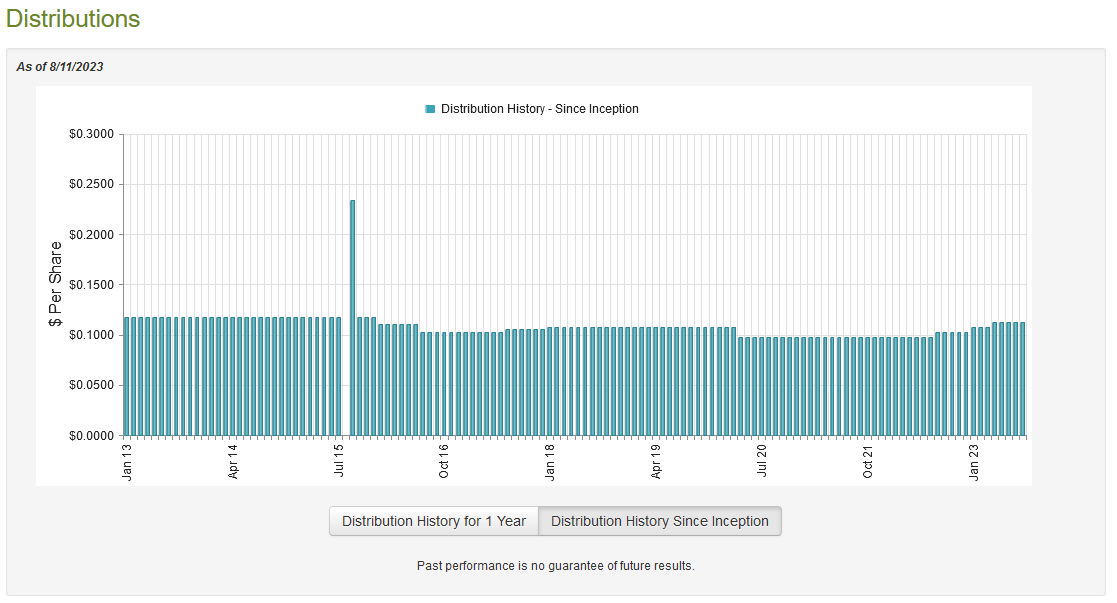

As mentioned earlier in this article, the Ares Dynamic Credit Allocation Fund has the stated objective of providing its investors with a high level of total return, primarily through the provision of current income. In order to accomplish this objective, the fund invests in debt securities of both the floating-rate and fixed-rate varieties. These securities typically deliver the majority of their returns in the form of direct payments to investors and have yields that are suitably high to attract investment dollars. This fund then boosts the effective yield of its portfolio through the use of leverage. As such, we can assume that it has a very high yield itself. That is certainly the case as this fund pays a monthly distribution of $0.1156 per share ($1.3872 per share annually), which gives the fund a 10.56% yield at the current price. Unfortunately, this fund has not been particularly consistent with its distribution over the years. In fact, it has varied quite a bit:

{kind=link}

This variable distribution is something that is likely to be a turn-off for those investors that are seeking a safe and secure source of income to use to pay their bills and finance their lifestyles. However, it is quite typical for a debt fund’s distribution to vary over time. This is due to the fact that interest rates have a substantial impact on the investment performance of their portfolios, and interest rates are completely out of the control of any individual fund. The fund will typically pay out as much as it can based on its investment returns without depleting the portfolio. This is why we have seen this fund increase its distribution twice in the past year, as the floating-rate component of the portfolio has resulted in its income climbing with time.

As is always the case though, it is important that we ensure that the fund can actually afford the distribution that it pays out. After all, we do not want it to be paying out more than it can afford because that would unnecessarily deplete the fund’s assets and make it more difficult to sustain itself over the long term. After all, a 10% return from $1 million principal is a lot less money than 10% from $100 million principal. Let us investigate the fund’s finances.

Unfortunately, we do not have a particularly recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, it will not include any information about the fund’s performance year-to-date. This is a shame because the bond market has proven stronger year-to-date than it was over most of last year and this may have provided the fund with the opportunity to earn some capital gains by trading bonds. With that said though, the report will give us some insight into how well the fund performed in the very challenging market of 2022, which could be a valuable insight into the quality of its management. After all, anyone can make money in a bull market, but it is a bear market that separates good fund managers from the rest.

During the full-year period, the Ares Dynamic Credit Allocation Fund received $43.908 million in interest from the assets in its portfolio. It had no other investment income, so that figure comprises all of its total investment income. The fund paid its expenses out of that amount, which left it with $29.947 million available to the shareholders. This was, fortunately, enough to cover the $27.383 million that the fund paid out in distributions. This should provide some comfort to the fund’s shareholders as it appears that all this fund is doing is simply paying out nearly all of its net investment income annually:

| FY 2022 |

| FY 2021 |

| Net Investment Income |

| $29,947 |

| $28,858 |

| Distributions Paid |

| $27,383 |

| $26,810 |

(all figures in thousands of U.S. dollars.)

It is logical to assume that the fund’s recent distribution hikes will end up being much of the same. Basically, the fund’s net investment income probably increased this year as the payments from the floating-rate securities adjusted upward because of the higher interest rates. The fund bumped up its distributions to pay out this higher income to its shareholders.

Unfortunately, the fund did experience an asset decline last year. It reported net realized losses of $20.617 million and had another $55.435 million in net unrealized losses. Overall, the portfolio declined by $73.488 million after accounting for all inflows and outflows. That is disappointing, but not really a big deal. The fund will almost certainly make this money back when interest rates decline at some point in the future. Until then, it will be able to collect a higher income due to higher interest rates. There is also the fact that the fund can simply opt to hold its securities to maturity and avoid losing money.

In short, the fund’s finances appear to be just fine. It will probably cut the distribution when rates go down, but with the recent uptick in inflation I find it unlikely that we will see rates drop in the near future.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Ares Dynamic Credit Allocation Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring a fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of August 11, 2023 (the most recent date for which data is available as of the time of writing), the Ares Dynamic Credit Allocation Fund had a net asset value of $14.12 per share but the shares currently trade for $12.88 each. This gives the fund’s shares an 8.78% discount on net asset value at the current price. That is not as good as the 9.40% discount that the shares have averaged over the past month, but it is not a particularly terrible discount. It might be possible to wait a bit and get a better price, but I would probably still buy this fund at the current price.

Conclusion

In conclusion, the Ares Dynamic Credit Allocation Fund offers an interesting alternative for investors that are looking to earn a high level of income today. The fund can adjust its portfolio between fixed-rate and floating-rate debt assets depending on the market environment, which is an advantage over funds that focus on just one or the other. It also allows it to be something of a “buy and forget” fund that can prosper in any interest-rate environment. The fund’s distribution is entirely covered by its net investment income, which is also nice as it is not dependent on management’s ability to earn capital gains. Finally, the fact that this fund is currently trading at a discount makes it a very good choice for any income-focused investor.

For further details see:

ARDC: A Very Good Choice For Anyone Seeking A High-Yielding CEF