ARDC - ARDC: This Fixed Income Fund Trades At A Wide Discount And Yields 10.5%

Summary

- Since I last wrote about ARDC in August, the discount has widened to more than -13% while the NAV has stabilized.

- Based on the current monthly distribution that was raised to $.1025 in August, the annual yield is now more than 10.5%.

- The outlook for high-yield fixed income is optimistic for 2023 after one of the worst years since 2008 has taken place in 2022.

It's almost Christmas here in Colorado and we are experiencing record cold temperatures, snow, and the weather outside is frightful. But I am writing today to give you a Christmas gift, one that keeps on giving month after month, year after year. The gift that I am speaking of is an update on a CEF that pays a monthly dividend, trades at a healthy discount to NAV, and recently raised the distribution. That CEF is Ares Dynamic Credit Allocation fund (ARDC).

The ARDC fund just celebrated its 10th anniversary with an inception date of November 27, 2012. The investment strategy of the fund is explained on the fact sheet, which can be found on the fund website .

The Fund invests primarily in a broad, dynamically managed portfolio of (i) senior secured loans ("Senior Loans") made primarily to companies whose debt is rated below investment grade; (ii) corporate bonds ("Corporate Bonds") that are primarily high yield issues rated below investment grade; (iii) other fixed-income instruments of a similar nature that may be represented by derivatives; and (iv) securities of collateralized loan obligations ("CLOs") and other asset-backed issuers.

In my earlier article published in August of this year, I explained how a credit fund like ARDC is a better investment than an equity fund in a bear market like the one we have been experiencing in 2022 due to the fact that the fund does not have to sell off assets to continue paying its sizable distribution. Conversely, equity funds experience NAV destruction when they must return shareholders' capital when capital gains do not cover the distribution. In theory at least, this is the reality of investing in credit funds like ARDC that are continuing to receive loan payments and debt installments that generate enough NII to cover the monthly distribution without having to reduce NAV by selling off core assets.

Seeking Alpha

Back in August I liked the fund and rated it a Strong Buy because it was trading at a -8% discount to NAV and offered a 9% yield and had just increased the distribution. Today, the discount has widened and is now over -13% while the yield has increased to 10.5%. The yield has increased, and the discount has widened because the market price of the fund has dropped even further than the NAV in the past four months. The total return of the fund since I last wrote in August declined by about -7.5% versus [[SPY]] down about -5%.

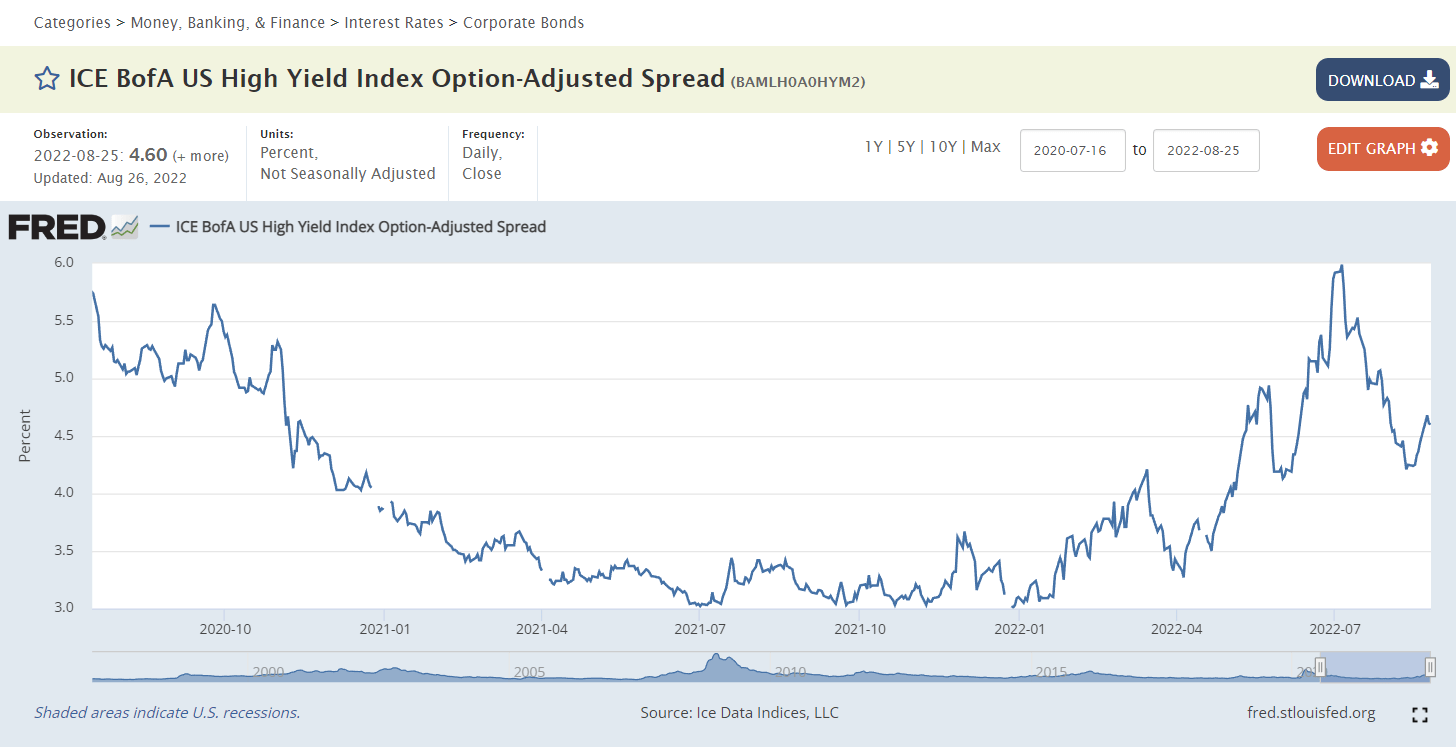

So, what has changed since then? In my previous article I wrote about how widening credit spreads in the first half of the year were impacting the ability of fund managers to navigate the loan markets effectively. I included this chart from the St. Louis Fed showing the chart of the high yield credit spread from August 2020 to August 2022.

{kind=link}

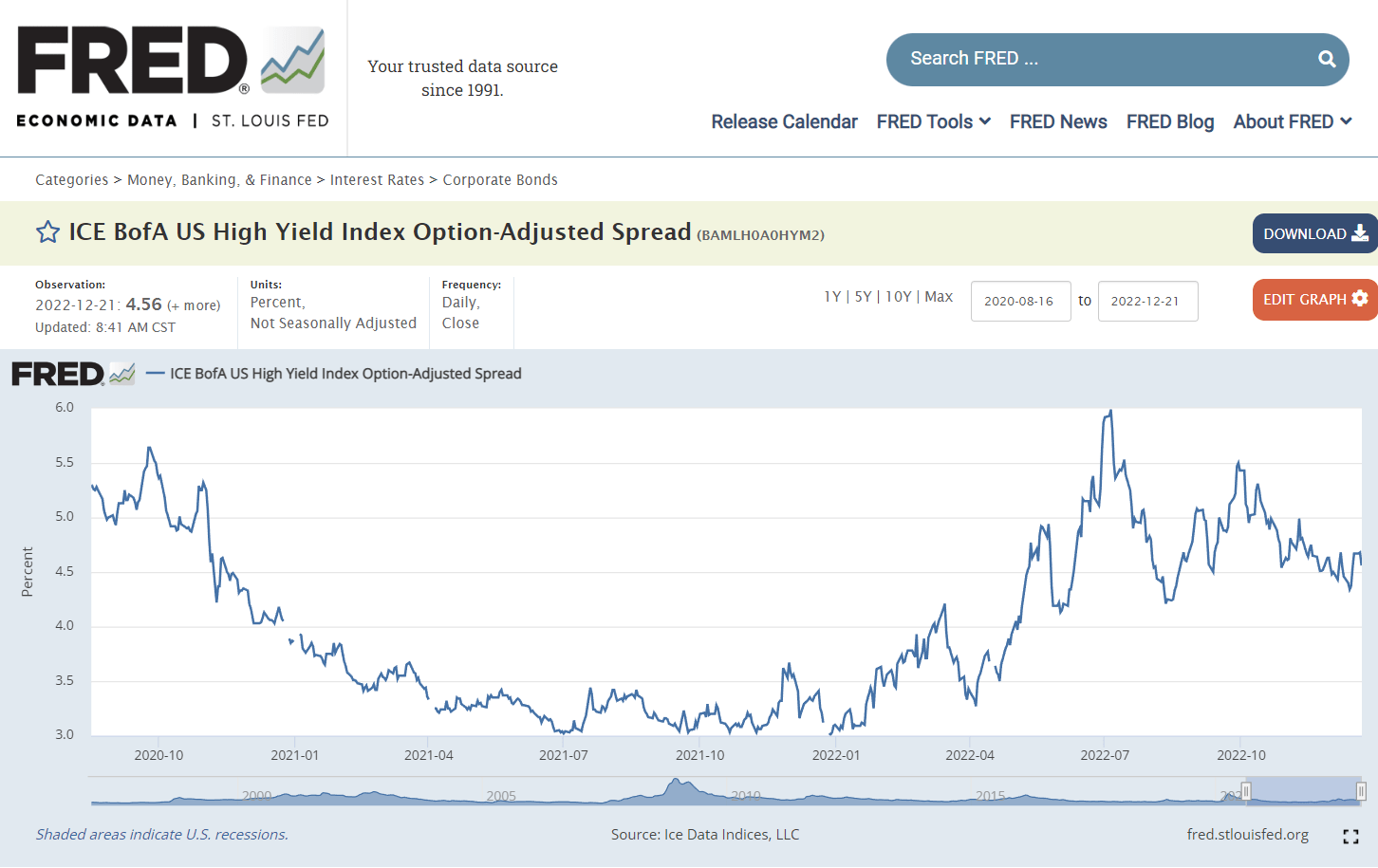

Since that time, the credit spreads began rising again into October before starting to fall again as can be seen in the latest chart from FRED.

{kind=link}

According to Moody's , the global leveraged loan market outlook for 2023 is optimistic, with higher expected issuance of high yield bonds and leveraged loans, relative to the record low levels of 2022. The current year is looking like it will be the weakest year since the 2008 financial crisis. In fact, according to this story on Yahoo Finance:

It was a tumultuous period for markets in 2022 as a variety of factors weighed on investors. In leveraged loans, risk aversion led to a secondary market sell-off and strangled the new-issue market, stifling refinancing opportunities and stranding committed LBO financing that arranging banks struggled to get off their books.

Total new-issue volume in the broadly syndicated loan market tumbled 63% to a 12-year low of $225.1 billion, as deal flow dried up on all fronts amid market volatility. Demand softened over the course of the year, as CLO origination was slower in the second half and cash outflows from retail funds accelerated.

Analysts agree that may translate into higher refinancing volume in 2023 compared to the past year as issuers address looming maturities, with Libor cessation in June 2023 potentially also playing a role.

Fund Holdings

The other change that I can determine from evaluating the information available to investors is that the fund holdings changed slightly in the past 4 months. In my previous article, I published this graphic from the August fund fact sheet that showed the industry allocation of the fund holdings as of July 31.

August fund fact sheet

From the latest fund fact sheet that shows the holdings as of November 30, I see a slight reduction in CLOs, an increase in Energy from 9.4% to 11.1%, Gaming & Leisure reduced from 8.9% to 8.0%, IT increased from 7.0% to 7.6%, Service increased from 4.5% to 4.9%, Housing reduced to 3.9%, Healthcare at 2.9% where it was not indicated previously, and Forest Prod/Containers not shown. The Other category is slightly higher now at 18.7%.

December fund fact sheet

In my August writeup I had also included this footnote from the fund fact sheet that discussed the liquidity position.

The Fund has $74 million aggregate principal outstanding on a $212 million revolving funding facility with an institutional lender, pursuant to which the Fund expects to borrow funds to make additional investments, subject to available borrowing base and leverage limitations.

According to the current fact sheet, that amount of principal outstanding is now $60 million. This would imply that $14 million in revolving funds were invested in new fund holdings in that 4-month period. The fund holdings include $470M in managed assets as of 11/30/22. The current portfolio mix includes 42% floating rate loans.

December fund fact sheet

Fund Performance and Pricing

In my earlier article I mentioned that the fund was trading at a discount of about -8% to NAV. Now, as illustrated by this chart from CEFconnect you can see that the discount has widened even further to more than -13%, while the NAV has levelled off and in fact, appears to be starting to rise again while the price continues to decline.

{kind=link}

The total return calculation that I referred to at the beginning of this article is based on the market price increase/decrease plus dividends paid (and reinvested). Therefore, the drop in market price since August is primarily responsible for the negative total return. For income investors who are not as concerned with total return, the monthly income has remained the same and if those dividends are reinvested, the amount of income generated from the fund over the past 4 months has actually increased.

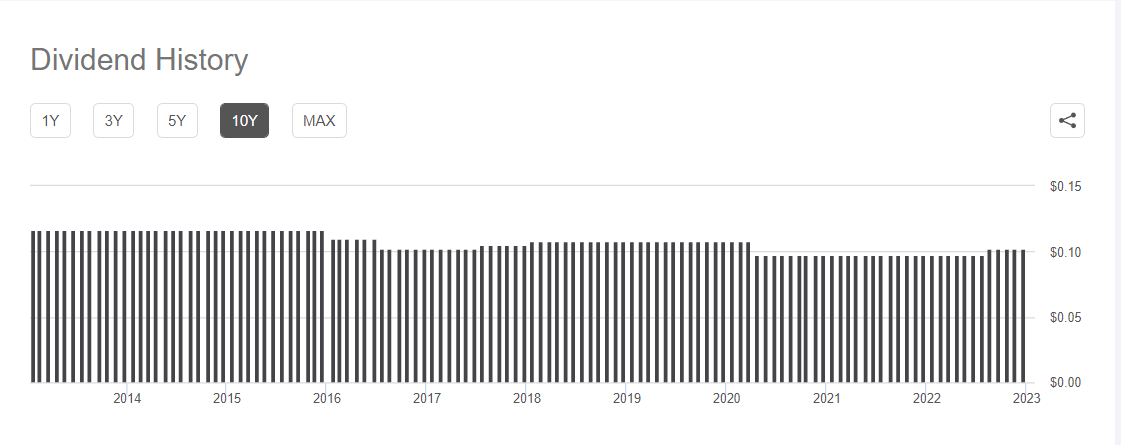

By examining the fund's dividend history since inception 10 years ago, it is clearly obvious that this fund offers a steady monthly distribution that income investors can rely on, and while the discount is wider than average, it is possible to purchase additional shares at even lower cost and thereby further increase the monthly income from the fund.

{kind=link}

Summary and Recommendation

The title of my earlier article on ARDC published in August referred to "retiring in comfort" with this fund. I rated it a Strong Buy and outlined the reasons why. Since that time, the fund performance has dropped along with the broader market, however, the market price has declined considerably more than the NAV of the fund leading to an even wider discount.

If you are a long-term investor who is either retired, nearing retirement, or building an income portfolio in preparation for future passive income during retirement or for whatever reason, you may want to consider buying shares of ARDC at these low prices. The market price is $11.73 as of market close on 12/22/22. The fund price has not changed much over the past 6 months, yet still trades near its 52-week low.

{kind=link}

With a regular monthly dividend that currently yields more than 10.5% annually, ARDC is worthy of consideration for your income portfolio, especially given the belief by many fund managers and financial institutions that the leveraged loan and high yield bond markets are likely to recover in 2023.

I continue to rate this fund a Strong Buy and I personally hold a medium size position in my No Guts No Glory portfolio and may add to it at these low prices.

For further details see:

ARDC: This Fixed Income Fund Trades At A Wide Discount And Yields 10.5%