DMCOF - Ardmore Shipping: Lagging Peers Time To Catch Up

2023-10-26 03:11:58 ET

Summary

- Ardmore is the cheapest product tanker stock and is currently lagging behind its peers.

- Improved shareholder returns are expected in the near future, which could help close the valuation gap.

- Best tanker market in the last decade.

Editor's note: Seeking Alpha is proud to welcome Oriol Madaula as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

In spite of improved fundamentals and impressive tanker market, Ardmore (ASC) is lagging its peers and trading at just 0.7 NAV when it used to trade around (or above) NAV. Also, shareholders' return should improve shortly closing the valuation gap, about 40% upside.

Business Overview

Ardmore is engaged in the ownership and operation of product and chemical tankers with 100% spot exposure. ASC owns a fleet of 22 midsize eco product tankers, plus 4 vessels chartered-in and one managed.

All of ASC's vessels are constructed at high-quality yards in Korea and Japan, incorporating advanced eco-design or eco-modifications. This eco-conscious approach aligns with the growing industry emphasis on reducing environmental impact and achieving higher fuel efficiency. It also positions Ardmore well to meet tightening regulatory standards and to appeal to environmentally conscious customers.

In addition to its eco-friendly fleet, Ardmore places a strong emphasis on operational efficiency. The company continuously explores opportunities to optimize its operating performance. This includes investments in technologies and practices that not only enhance operational efficiency but also contribute to reducing the company's environmental footprint.

Ardmore introduced a capital allocation policy in March 2020 with four main objectives:

Maintain Fleet Over Time: One of the primary goals of this policy is to ensure the long-term sustainability and efficiency of the fleet. The company is actively investing in optimizing operating performance, which includes installing scrubbers to reduce emissions. These measures contribute to both operational efficiency and environmental compliance.

Sustain Leverage Below 40%: As of Q2 2023, ASC's net leverage stands at a remarkable 18%, a testament to its prudent financial management. This low leverage not only reduces financial risks but also positions the company for further growth and return of capital to shareholders. In fact, if they do not increase shareholders' return, they will be net cash in a few months.

Well-Timed Accretive Growth: While Ardmore is cautious about expansion opportunities at present, it maintains a strategic focus on well-timed, accretive growth. The company is poised to seize attractive opportunities when they arise in the market, ensuring that growth aligns with value creation. In the meantime, they could buy back shares, but management has stated no desire in doing so.

Return Capital to Shareholders: Ardmore initiated a quarterly cash dividend plan in Q3 2022, with dividends set to be one-third of adjusted earnings.

Management's history and performance are often scrutinized by investors, especially in a sector as competitive and cyclical as the shipping industry. Trust in management is crucial, and it's often built over time through consistent financial prudence, effective communication, and a commitment to shareholder value.

It's worth noting that, in the past, management did some decisions that may have raised questions among investors. One notable example is the issuance of shares below net asset value ('NAV'). However, it's important to highlight that, in the context of Ardmore's current financial position with low leverage, such past decisions might be seen as reflecting a period of different financial constraints and uncertainty. With the company's financial stability greatly improved, there may be opportunities to rebuild trust with investors through prudent capital allocation and more shareholders' returns. But until the latter improves, I wouldn't trust management for a long-term investment.

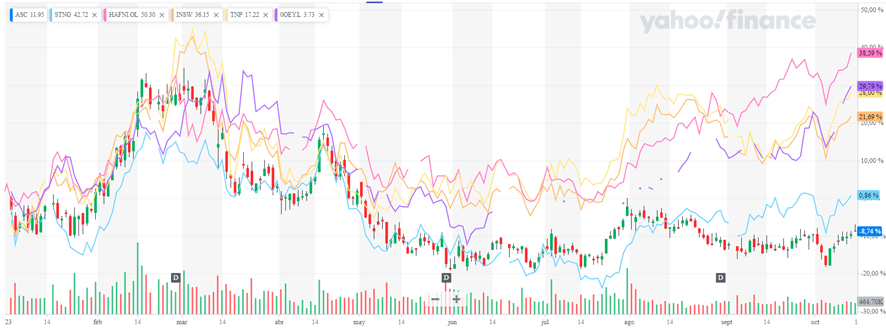

Regarding the stock price, in one of the best markets in recent history, ASC is down year to date.

{kind=link}

Around March, valuation was a bit overextend but since then NAV has been increasing, market fundamentals have kept strong, and the company has continued to deleverage. If Q4 is strong as usual, the stock could trade to new highs.

Product Tanker Overview

The tanker market has a strong seasonality, usually the summer months are the softer ones and during winter there is a huge improvement due to higher demand.

As can be seen in the following graph , each red circle is around July/August, and usually it is a local low for rates. This year, local lows are higher than previous high season rates since the 2008 bull market. This could be an indication that product tanker utilization is really high, and any additional demand or disruption could send rates to new highs.

Rates in context (STNG Q2 presentation, slide 18 (red circles added))

{kind=link}

Besides seasonal demand increase, this year inventories are low, which could lead to some panic if any disruption appears or if there is a very cold winter.

Global Inventories (STNG Q2 presentation, slide 14)

{kind=link}

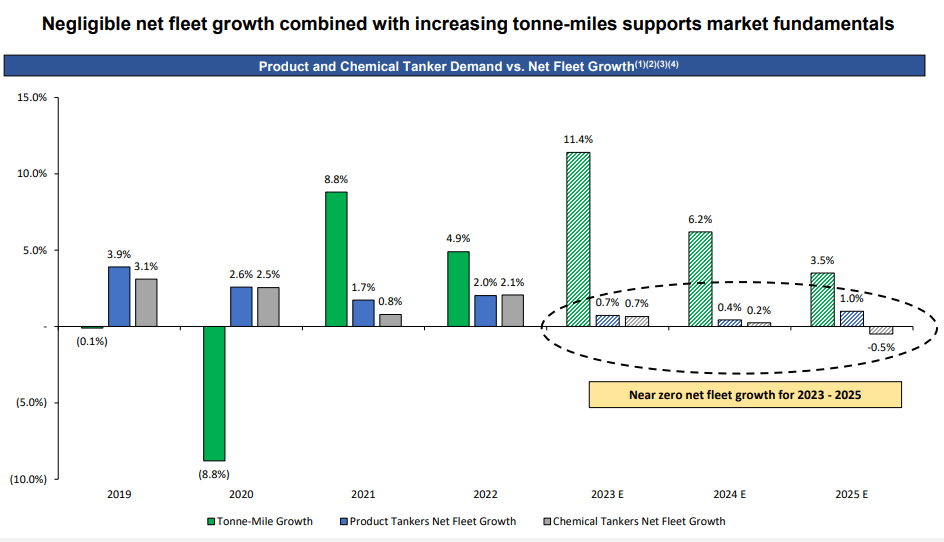

Regarding supply, the orderbook has been steadily increasing, and it is about 10% of the product fleet, but heavy squeezed towards LR2 while MR (ASC vessels) only have an orderbook around 5%. What is more interesting is that most of those ships would not arrive until 2026 and fleet growth in 2024 and 2025 will be very small and inferior to ton mile growth.

Fleet growth (ASC Q2 presentation, slide 9)

{kind=link}

This graph has some aggressive assumptions, and probably the ton mile growth will be smaller and fleet growth a bit higher because the only ships that are being scrapped are 25+ years old. But the main point stands, fleet growth will be minimal until 2026 and any additional ton mile growth will tight the product market even more.

Fleet Supply dynamics (ASC Q2 presentation, slide 10)

{kind=link}

There is still room to increase the orderbook without crashing the market due to the aging fleet, >40% of MR fleet is above 20 years old, but if this ordering path continues much longer, the outlook will start to look less promising.

Stock Valuation

In Q2, Ardmore reported adjusted earnings of $23.7 million or $0.57 per share with $26.5k/day fleet average TCE.

Q3 usually is the worst quarter, and they guided for 45% of MR days fixed at $26.1k/day and 63% of their chemical tankers at $23k/day. Q3 fleet average should be around $25.5k/day for an adjusted EPS between $0.45-$0.5 a bit above analyst expectations of $0.36.

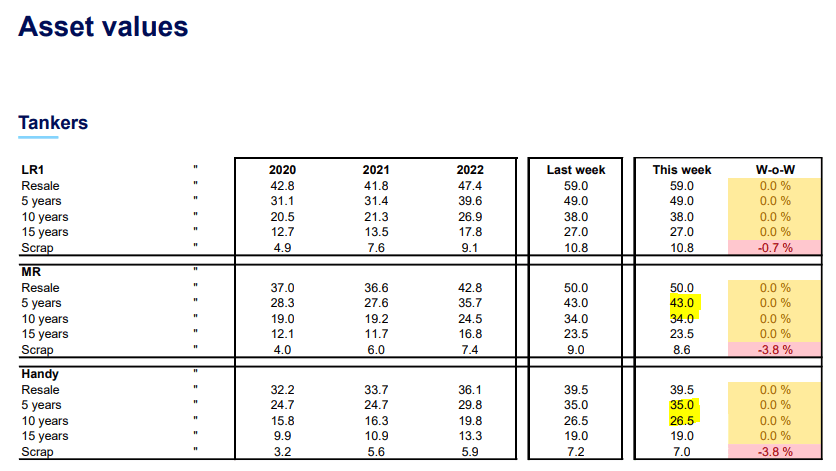

Taking into account Q2 balance sheet, projected Q3 and looking at last MR transactions prices and Arctic asset values (without scrubbers) we can estimate the Net Asset Value to be around $17.5/share:

ASC Balance Sheet (ASC Q2 presentation, slide 13) Asset Values (Arctic Securities Research, Arctic Shipping)

{kind=link}

Doing a gross estimate with a lineal approximation, we get this value with Q2 numbers and actual Arctic values:

ASC NAV (Personal calculation)

If we add Q3 results, we get a NAV about $17.5/share.

Q4 will be a very heavy drydock quarter with 4 of them (15% of the fleet) making it more difficult to predict earnings. Being conservative and considering Q4 usually is the best quarter, if they achieve a fleet average TCE of $35k/day, EPS will be about $1 per share and NAV will be approaching $20/share.

Right now the stock is trading around $13, more than 40% upside to close the valuation gap and trade at valuations more similar to peers.

How Can This Gap Be Closed?

The first catalyst could be analyst revisions or Q3 earnings surprise. It seems that Q3 expectations are a bit low and can surprise to the upside.

Another possible catalyst would be improved sentiment in product tankers, Ardmore is the cheapest product tanker, and it is lagging their peers, if sentiment improves in Q4 it should attract more interest and help to close the gap.

{kind=link}

An important positive point is that we could expect better shareholder returns. When the dividend started net leverage was 34.3% now is below 20% and with current rates will be net cash in a few quarters. In the last conference call Bart Kelleher, Ardmore CFO, said: " And as we've mentioned in the past, we're happy to return additional capital to shareholders beyond the 1/3 dividend we've stated, and our Board supports this. And that would be if we built further cash position likely in the form of a special dividend, and we've consistently reiterated that messaging in the past. "

I don't expect a special dividend this quarter, but it is very likely with Q4-23 results if rates continue to be strong.

Finally, another potential scenario, particularly if Ardmore's stock remains undervalued in comparison to its NAV, is a buyout. Recent developments in the shipping industry, such as the Euronav and Frontline deal in the dirty tanker segment, and International Seaways' ( INSW ) poison pill defense against Fredriksen, demonstrate increased activity in mergers and acquisitions. Just last week, Torm PLC acquired four 2015-16 MR vessels for $150 million. This strategic move indicates a commitment to fleet renewal and expansion. If Torm (trading slightly above NAV) or other companies continue down this path, Ardmore Shipping Corporation could emerge as an attractive acquisition target.

Risks

Recession or demand destruction. Product tankers move the marginal barrels, so a small reduction in consumer demand can have a big impact on tanker demand. If high oil price and dollar continue climbing, it could affect demand.

Orderbook: the actual orderbook is manageable, but if it continues to climb much more, it will be a risk for long term outlook.

Management and desire to grow. Ardmore does not have the best management in the sector and just a few quarters ago were issuing shares with the ATM below NAV. With current leverage, I don't expect to use it again below NAV, but I have no doubt that if ASC trades above NAV, management will try to do acquisitions or start a new build program. While issuing shares above NAV to buy vessels is not negative, this is not a management I will trust for the long run until they prove that can reward shareholders.

Conclusion

Product tanker companies are enjoying the best market in the last decade. Ardmore is the cheapest one ahead of the best quarter of the year and with the outlook of improved shareholder returns. It could return >40% just to close the NAV gap in few weeks or months.

For further details see:

Ardmore Shipping: Lagging Peers, Time To Catch Up