ASC - Ardmore Shipping: Quality Company At A Discount To Play The Shipping Cycle

2023-12-19 03:20:01 ET

Summary

- Ardmore is focused on products and chemical tankers. The fleet's average age is 9.3 years.

- The trinity of tight ship supply, growing vessel demand, and geopolitical catalysts mean we are in the middle of another shipping bull cycle.

- The Company has a solid balance sheet with $50 million cash and $102 million total debt. Net leverage dropped from 34% to 14% YoY.

- ASC managers are capable capital allocators given Total Debt/Total Capital vs. ROTC. The company has attractive returns and margins, given the average ship size in its fleet.

- Ardmore is undervalued compared to its historical multiples and its peer group. One thing is missing to give a strong buy, more ships with scrubbers. I give ASC a buy rating.

Introduction

Ardmore Shipping (ASC) owns and operates chemical and product tankers. The company's fleet consists of 26 vessels with an average age of 9.3 years. The company has a robust balance sheet with $50 million cash and $102 million debt. The company has been profitable over the last two years due to growing daily rates. Multiple catalysts, I believe, will push the rates further in the coming 12 months. ASC pays dividends with an attractive yield ((TTM)) of 8.07%. The company is undervalued compared to its past multiples and its peer group.

Day rates catalysts

The tanker industry, I believe, will be one of the best-performing industries due to supply and demand imbalances. On the supply side, we have an aging global fleet. In the coming five years, 37% of the product tanker fleet will be older than 20. After 20 years, the ships are considered for demolition. The product tanker's order book represents 10% of the current fleet. In other words, the incoming new build will not compensate for the outgoing ships to the scrap yards. Apart from that, the shipyard's capacity is limited. In my articles on Frontline (FRO) and Scorpio Tankers (STNG), I gave more details on those developments.

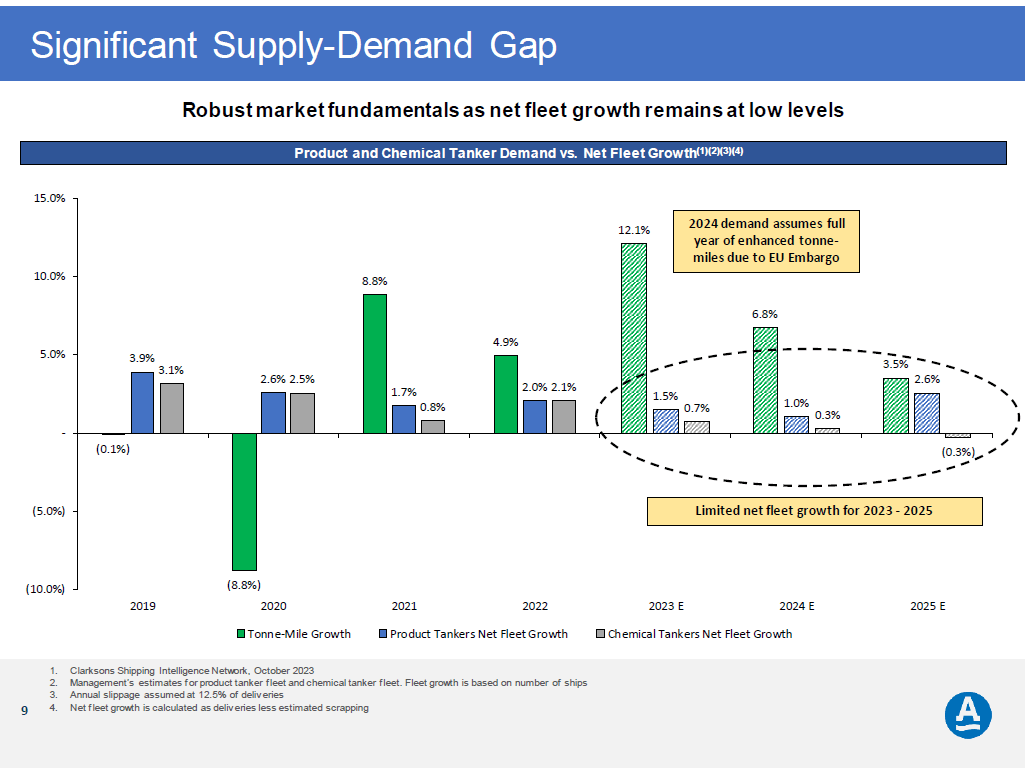

On the other side of the equation, the demand is expected to grow, too, as seen in the image below from the last company presentation .

{kind=link}

As seen above, the demand growth rate exceeds the fleet growth rate. The reasons are threefold: refineries' offline capacity will decrease, operational refineries' dislocation across the globe, and declining global inventories.

{kind=link}

Adding the geopolitical wild card, the day rates will stay higher for longer. The last news from the Red Sea and Houthis rebels' attacks on merchant ships will significantly extend the length of voyages. Panama Canal's improved situation will not help much to absorb the disruptions caused by the turmoil in the Middle East.

The Pentagon announced its "Operation Prosperity Guardian" to reopen the Red Sea passage. However, I am skeptical about its efficiency. The reason is simple: the Houthis successfully fought the Yemeni government and Saudi Arabian military attacks. Last week, they proved their capability to launch ballistic missiles on a running target. The rebels are well-equipped and trained, meaning they will fiercely resist and might increase the scale of their attacks. In conclusion, I expect the Red Sea to be temporarily out of the equation for most major shipping companies, resulting in higher rates for longer.

ASC is well positioned to cash on the rising rates due to limited ship supply, rising demand, and geopolitical turbulence. The voyages will be longer and at higher daily rates.

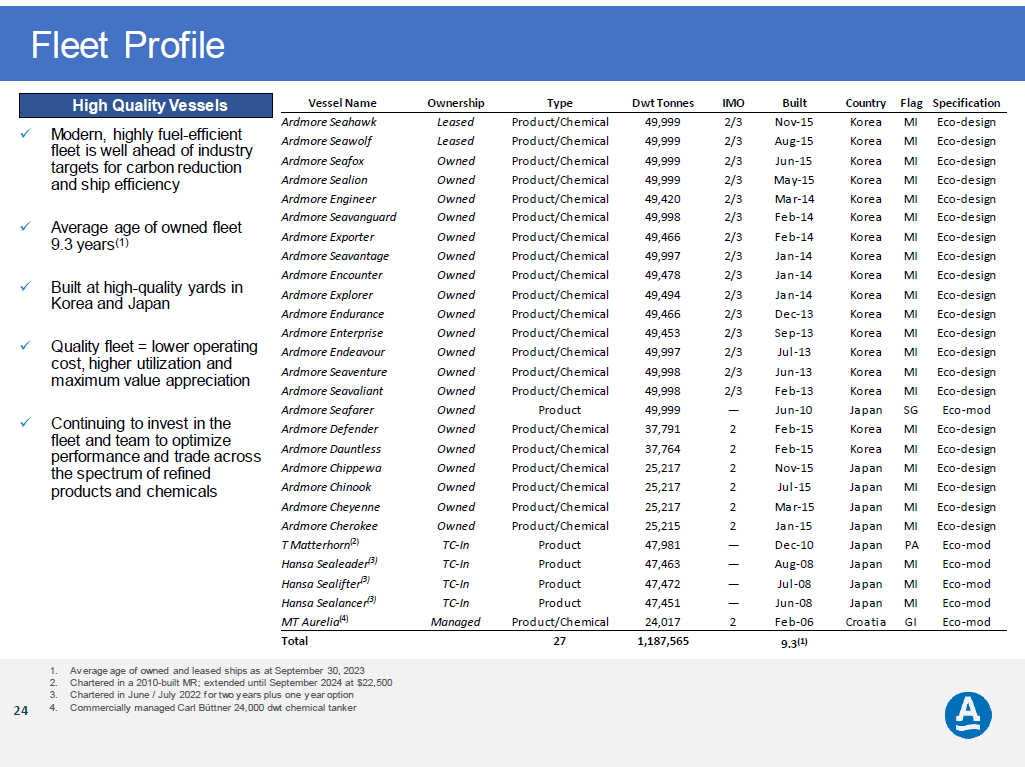

Ardmore fleet overview

All ASC ships fall under the Handy category. 16 of them are 49,000 dwt, 4 are 25,000 dwt, and 2 are 37,000 dwt. The table below from the last company presentation shows ASC's fleet profile.

{kind=link}

Most of the ships (20) are owned by the company, while two are leased, and ASC charters 4. The fleet's average age is 9.3 years, and 70% of the ships are built in Korea, while 30% are in Japan.

I consider a low percentage (23%) of scrubber-equipped vessels in the ASC fleet to be a disadvantage. The scrubber's day rates are higher than eco ship rates, and a long-term capital investment to install scrubbers pays off.

Ardmore balance sheet

ASC has a solid balance sheet with $50 million cash and $102 million total debt, resulting in a 0.49 cash-to-total debt ratio. Compared with product tanker companies, STNG has 0.20 cash to total debt, Hafnia (HAFNF) has 0.09 debt, and TORM ( TRMD ) is 0.22.

Over the last five years, ASC significantly reduced its leverage.

{kind=link}

Net leverage dropped from 34% to 14% YoY, while the cash to break even dropped from $16,500 in 2019 to $14,000 in 3Q23. The company has more than adequate interest coverage at 13.1 EBITDA/Interest expenses.

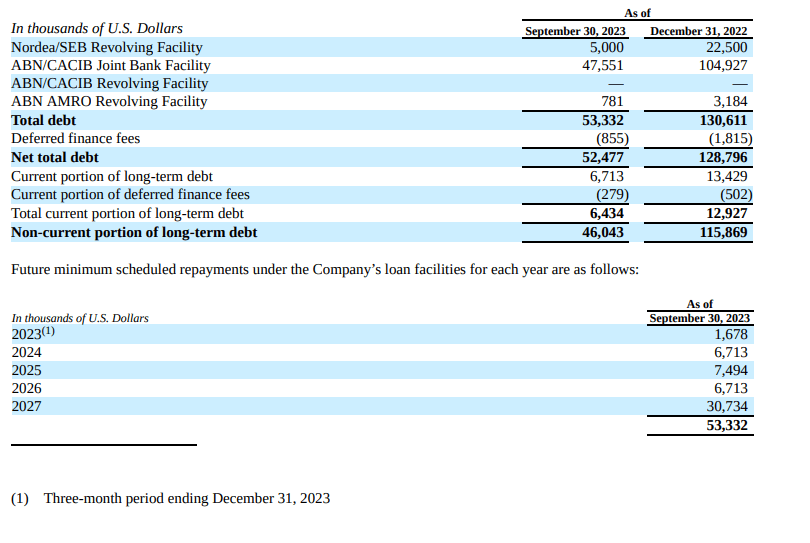

The table below from the 3Q23 report shows the ASC's debt structure.

{kind=link}

ASC has a $185 million revolving credit facility with Nordea under the following terms: interest rate SOFR +2.5% premium and maturity in June 2026.

ASC has a $108 million long-term loan with ABN AMRO under the following terms: interest rate SOFR + 2.5% premium and maturity in August 2027. The principal has to be repaid every quarter, and a balloon payment is due with the final installment. ABN/AMRO $15 million revolving credit facility with interest based on SOFR + 3.9% premium and maturity in August 2025.

The minimum debt repayment scheduled in the coming years is below ASC's current cash levels. The most extensive installment is $30.7 million, due in 2027. Given the company's liquidity, I do not expect any difficulties covering its debt repayments.

Profitability and dividends

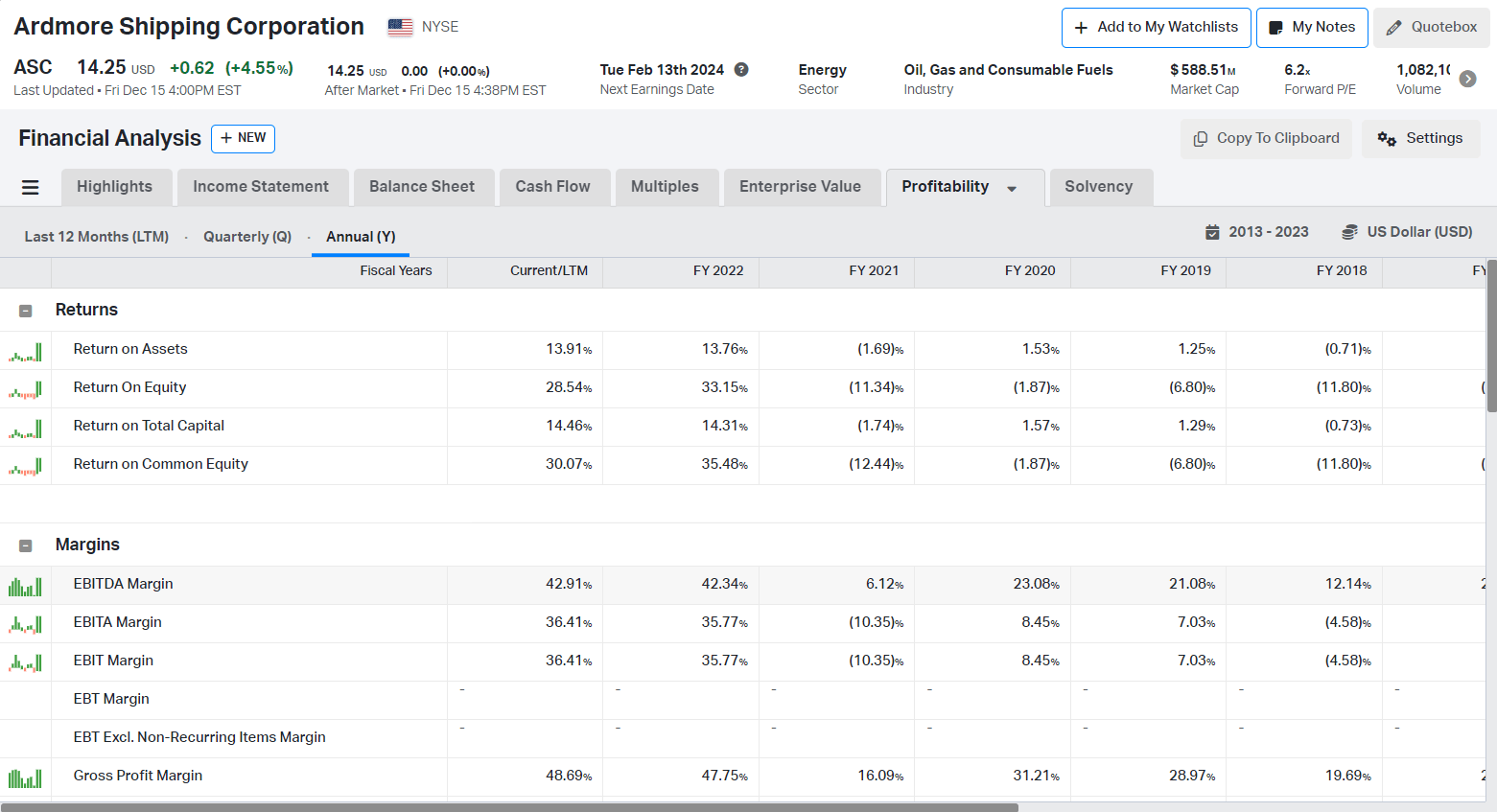

The last two years have been successful for the shipping industry. ASC results are proof of that. The table below shows ASC margins and returns in the previous five years.

{kind=link}

ASC margins and returns are not the best among its peer group.

- ASC has 48.7% Gross Margin, 42.9% EBITDA Margin, 28.5% ROE, and 14.5% ROTC

- STNG has a 75% Gross Margin, 55% EBITDA Margin, 30.2% ROE, and 11.9% ROTC

- HFNF has 55% Gross Margin, 48% EBITDA Margin, 43% ROE, and 15.3% ROTC

- TORM has 59% Gross Margin, 54% EBITDA Margin, 46% ROE, and 17.9% ROTC

The above comparison is imperfect because ASC has only Handy-size tankers, while the others have bigger ships in their fleets. The larger the vessels, the lower the cost per cargo ton, resulting in larger profit margins.

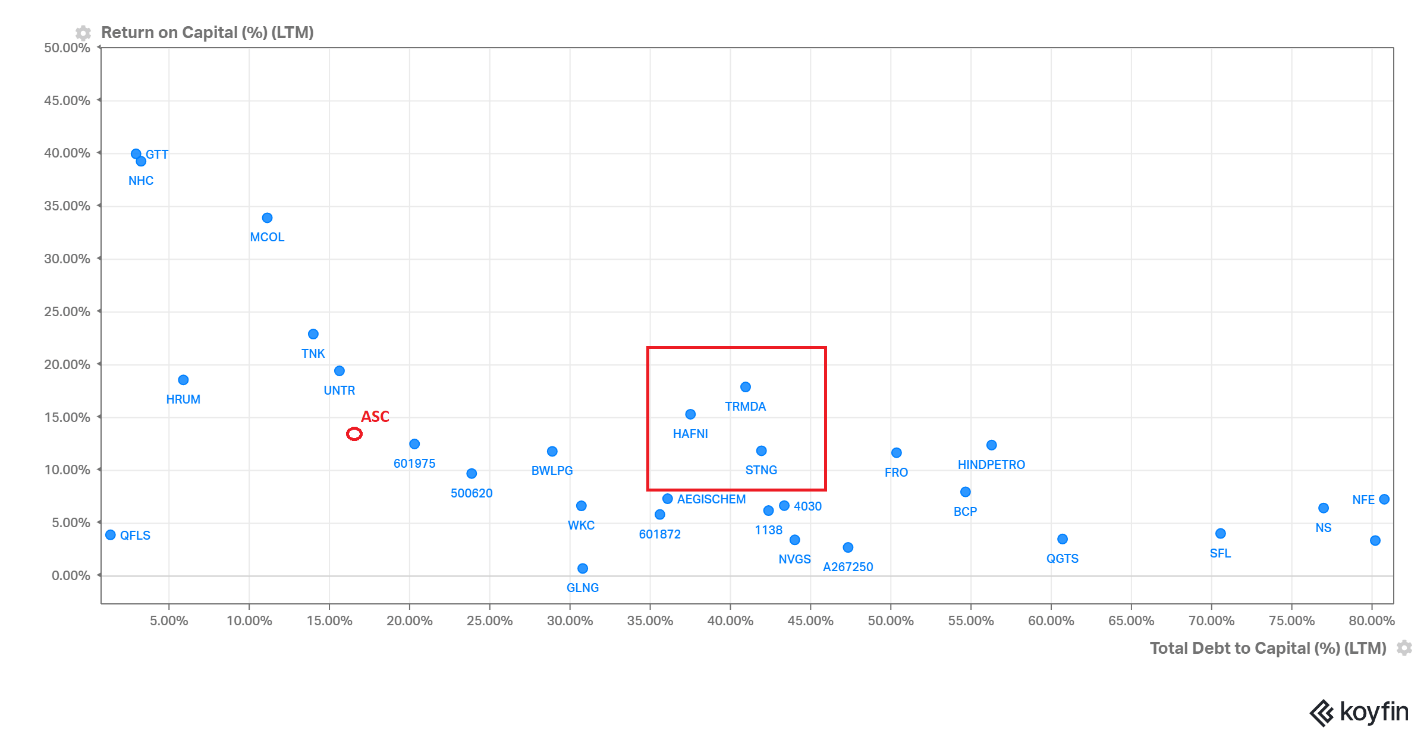

ASC managers are capable capital allocators given Total Debt/Total Capital vs ROTC.

{kind=link}

HAFNI, STNG, and TRMD have slightly better ROTC but much higher leverage.

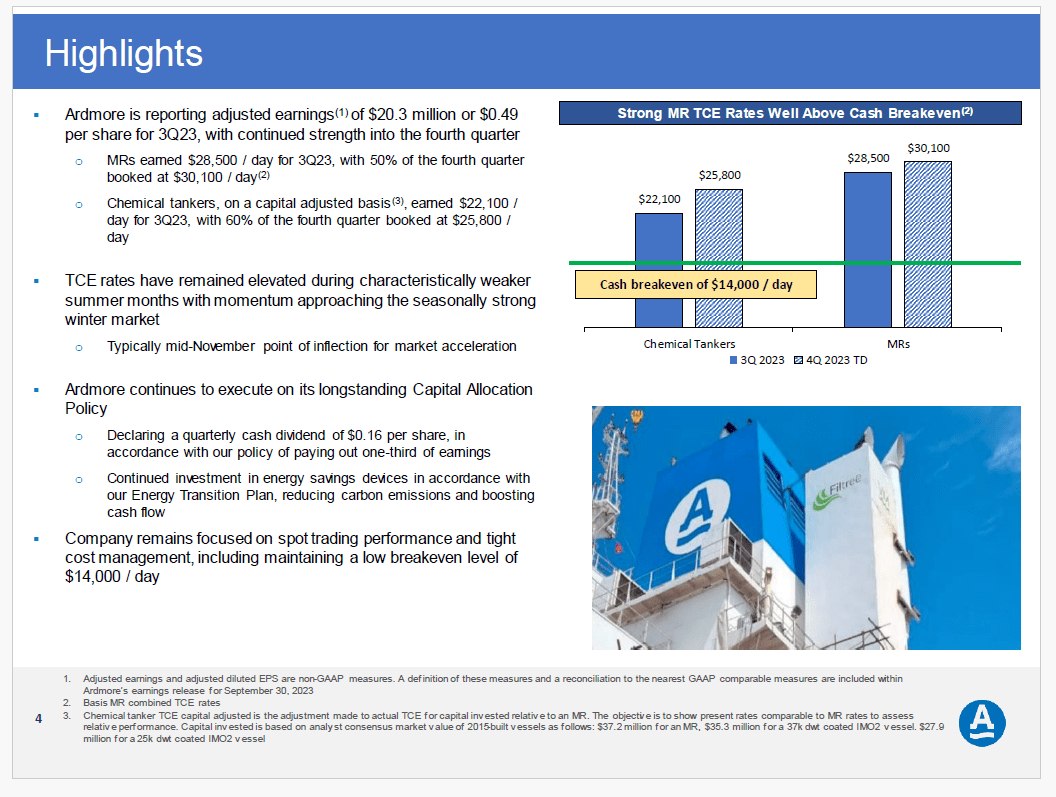

The day rates remained high in the summer months. In 3Q23 , chemical tankers' TC rates were $22,100, MR rates were $28,500, and cash breakeven was $14,00/day.

{kind=link}

ASC had MRs booked at $33,100/day and chemical tanker booked at $25,800 for 4Q23. Given the supply and demand dynamics in the shipping industry and geopolitical stress, the rates will grow further in the coming months.

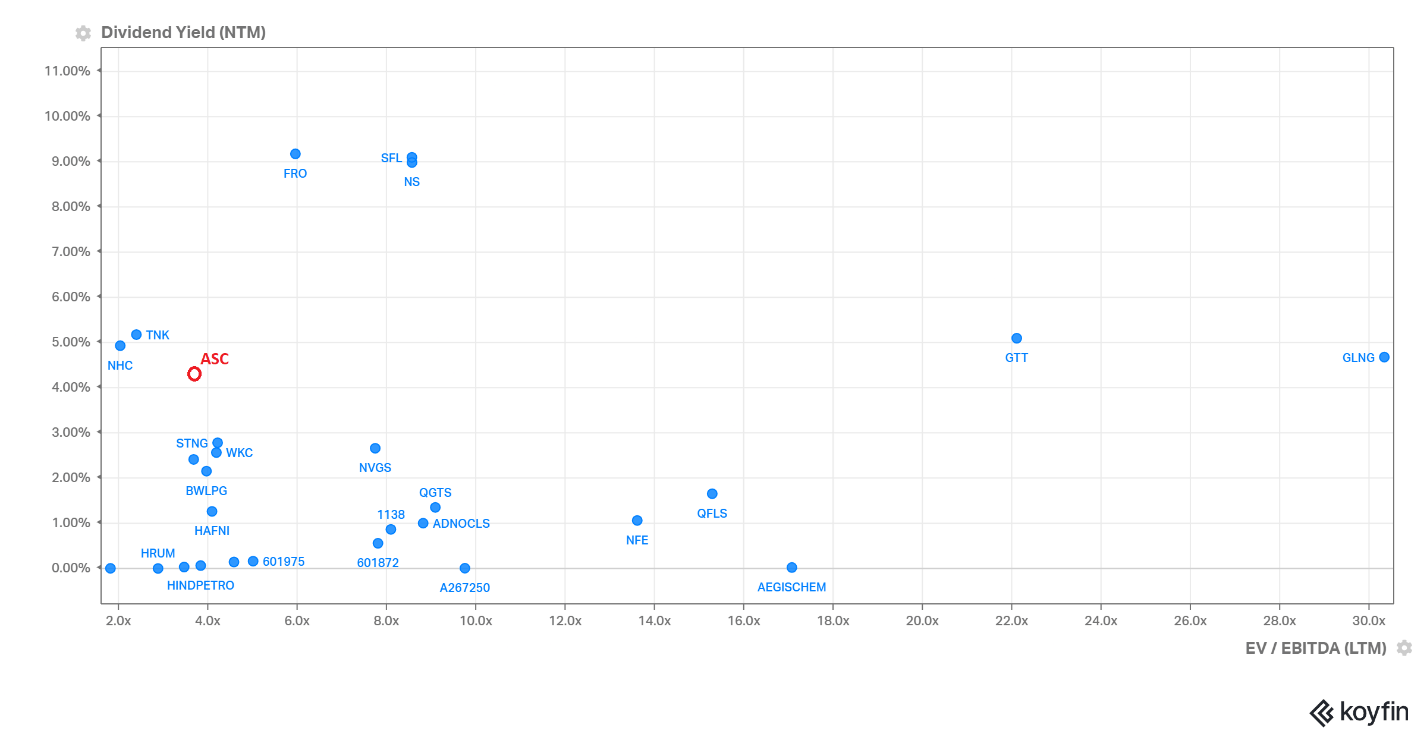

ASC pays $1.15 dividends ((TTM)) with an 8.07% yield. The yield is comparable to that of other product tanker companies. The chart below represents the dividend Yield ((NTM)) on the Y axis and EV/EBITDA ((LTM)) on the X axis for major tanker companies.

{kind=link}

To obtain dividends with a yield of 4.49%, I must pay an EV/EBITDA of 3.67. ASC trades at a discount compared to its peers with lower dividend yield ((NTM)) and higher EV/EBITDA.

Ardmore valuation

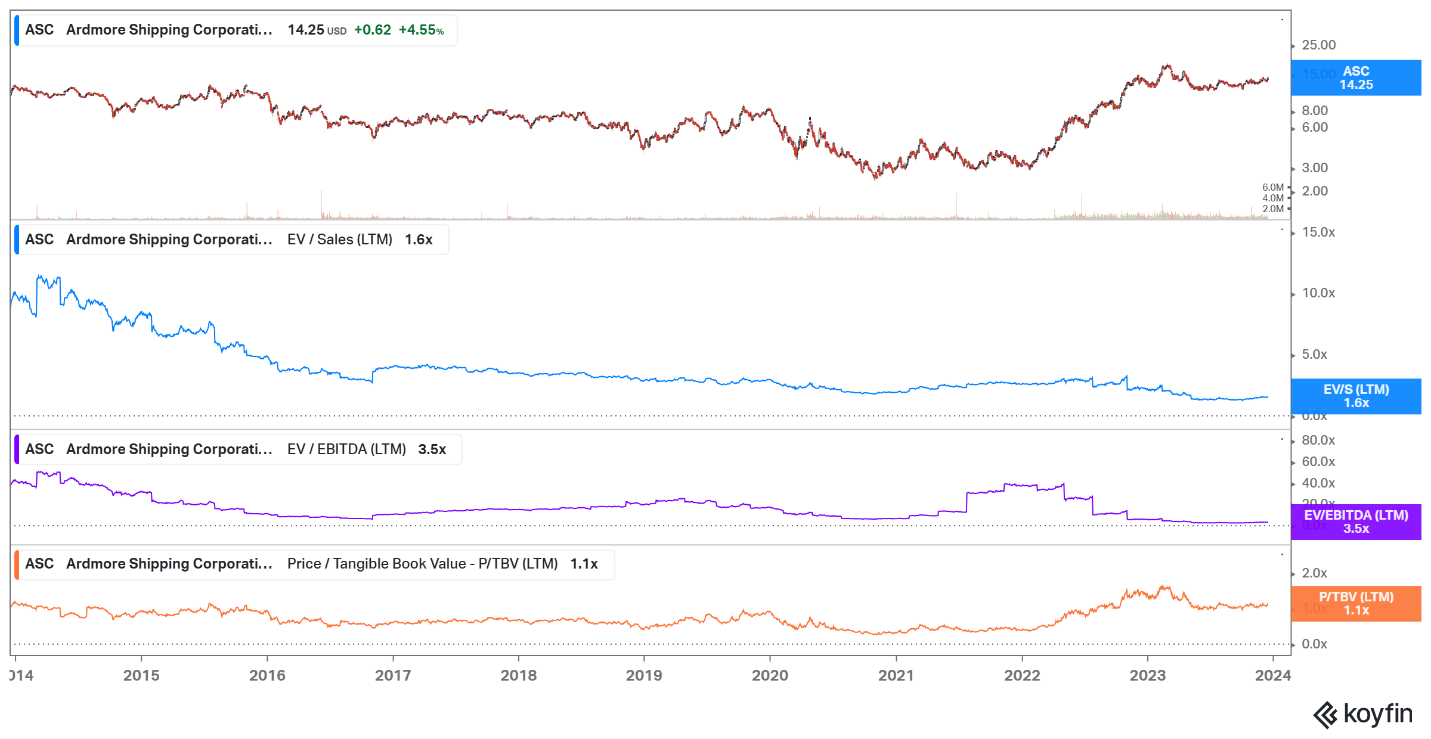

The chart below shows ASC EV/Sales, EV/EBITDA, and P/TBV.

{kind=link}

ASC trades at 1.58 EV/Sales, 3.67 EV/EBITDA, and 1.14 P/TBV. These figures were lower than its peak values (11.0 EV/Sales, 49.2 EV/EBITDA, and 1.3 P/TBV) in 2014 and its 5Y averages (2.34 EV/Sales, 18.28 EV/EBITDA and 1.25 P/TBV).

ASC is the cheapest in its peer group, too:

- STNG trades at 2.85 EV/Sales, 4.36 EV/EBITDA, and 1.18 Price/Book

- HAFNF trades at 2.11 EV/Sales, 4.37 EV/EBITDA, and 1.44 Price/Book

- TRMD trades at 2.03 EV/Sales, 3.7 EV/EBITDA, and 1.48 Price/Book

I believe the market discounted the lower profit margins and returns. However, I think it is justified due to the ship's size in the ASC fleet. ASC trades at lower multiples than its peers and past multiples, offering great value for the price.

Price Action

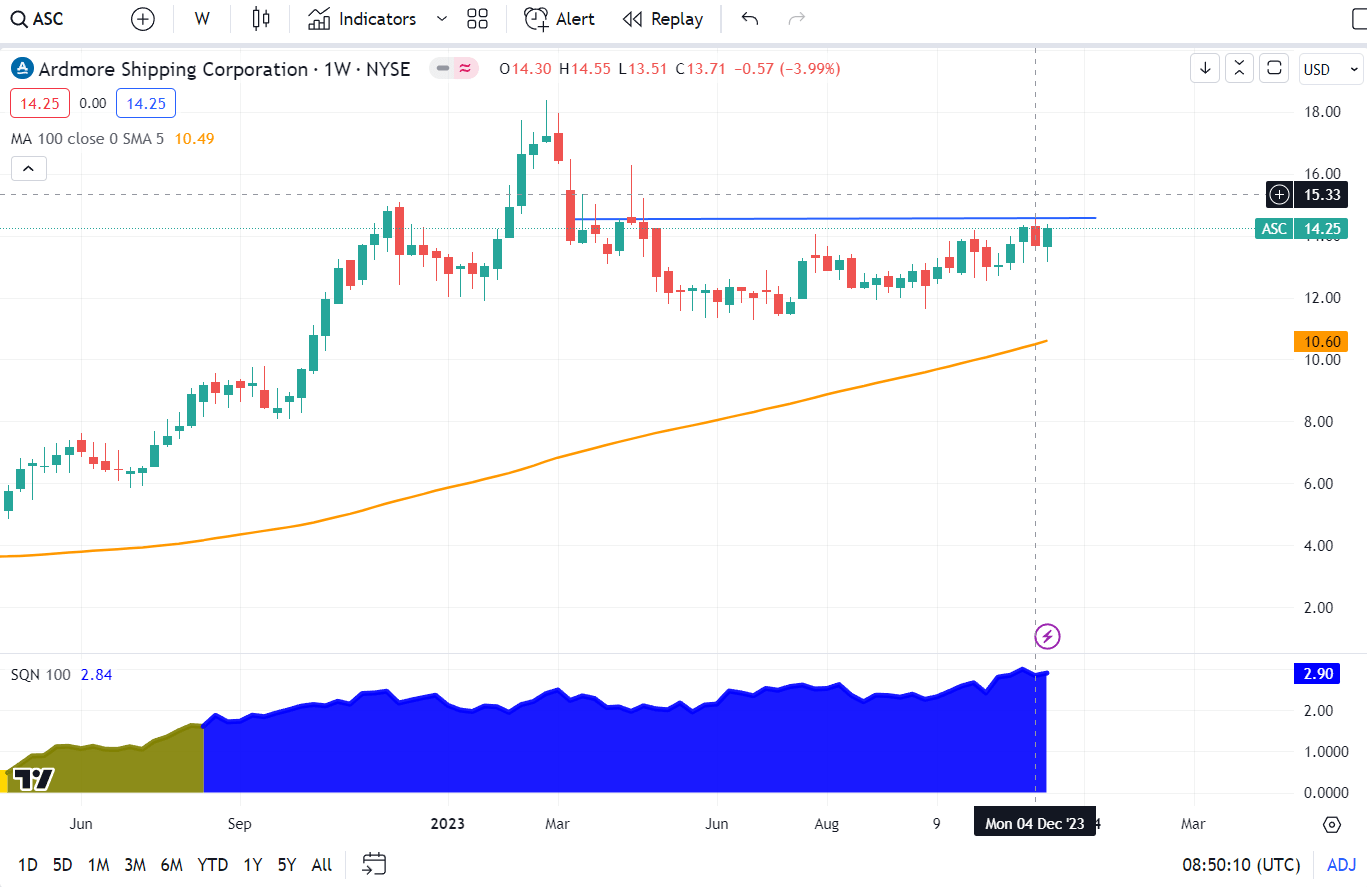

ASC price moves in a narrow range on a weekly chart.

{kind=link}

The price is in a bull volatile regime and above the 100 weekly moving average ((WMA)). Typically, volatile regimes are not the most productive for taking a position. However, SQN readings are not considered in isolation. The price is above 100 weeks moving average and is on the verge of breaking out of the range. The setup is imperfect but good enough to take an initial position. If the breakout succeeds, I will add more size to the dips.

Risks

The shipping business is cyclical. The cycle depends on ships' demand and supply dynamics. At the bottom, we have a low order book, many demolition sales, and freight close to operating costs. At the top, we have day rates over 3xOPEX, heavy ordering, record-low demolition sales, and positive sentiment. I assume we are in the first leg of another bull cycle. My arguments are as follows:

- We have a record low order book, more typical for cyclical bottoms.

- The demolition sales peaked in 2021 but did not decline to levels typical for cyclical peaks.

- The day rates are higher than daily OPEX but not exuberantly high.

- We have a catalyst in the face of geopolitical tensions.

Simply put, owning a ship in such times seems to be an investment with upside potential far exceeding the downside.

Financially, ASC is sound, having enough liquidity to cover its debt obligations. The market risk is always present. However, shipping companies and tankers, in particular, have a low correlation with broad equity indexes. However, the Fed pivot will boost investors' sentiment in the coming weeks, increasing equity prices.

Conclusion

ASC is an excellent way to play the next leg in the bull shipping cycle. The company is focused on products and chemical tankers. The fleet's average age is 9.3 years, meaning the company is not pressed to renew its fleet. ASC has sound financials with a cash-to-debt ratio of 0.49, superior to its peers. The company's debt maturities are well structured, with the next large repayment in 2027. ASC is profitable, considering its margins and returns. The company pays dividends with adequate yield. ASC is undervalued compared to its historical multiples and its peer group. One thing is missing to give a strong buy: only 23% of the company ships are equipped with scrubbers. I give ASC a buy rating.

For further details see:

Ardmore Shipping: Quality Company At A Discount To Play The Shipping Cycle