ASC - Ardmore Shipping: Returning To Port With An 11% Yield Aboard

2023-03-15 03:06:16 ET

Summary

- After years of battling difficult operating conditions, Ardmore Shipping saw a dramatic change of fortunes during 2022.

- Due to the fallout from the Russia-Ukraine war, trade routes for refined products are shifting in response to Western sanctions on Russia.

- This increases demand for their vessels and, therefore, supports a bullish outlook for charter rates.

- They seized upon this event to deleverage and reinstate dividends, which could see growth in future years after repaying more net debt.

- In light of this structural change, I believe that a buy rating is appropriate.

Introduction

The shipping industry is no stranger to difficult times, something the shareholders of Ardmore Shipping ( ASC ) likely know all too well after seeing their dividends suspended for years as the company battled difficult operating conditions and struggled with leverage. Even though the Russian invasion of Ukraine is certainly nothing to celebrate, the resulting shift in trade routes creates a structural change in their industry. Due to this dramatic change of fortunes, management was able to reinstate their dividends that effectively sees them returning to port with a very high near-11% dividend yield aboard, metaphorically speaking.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

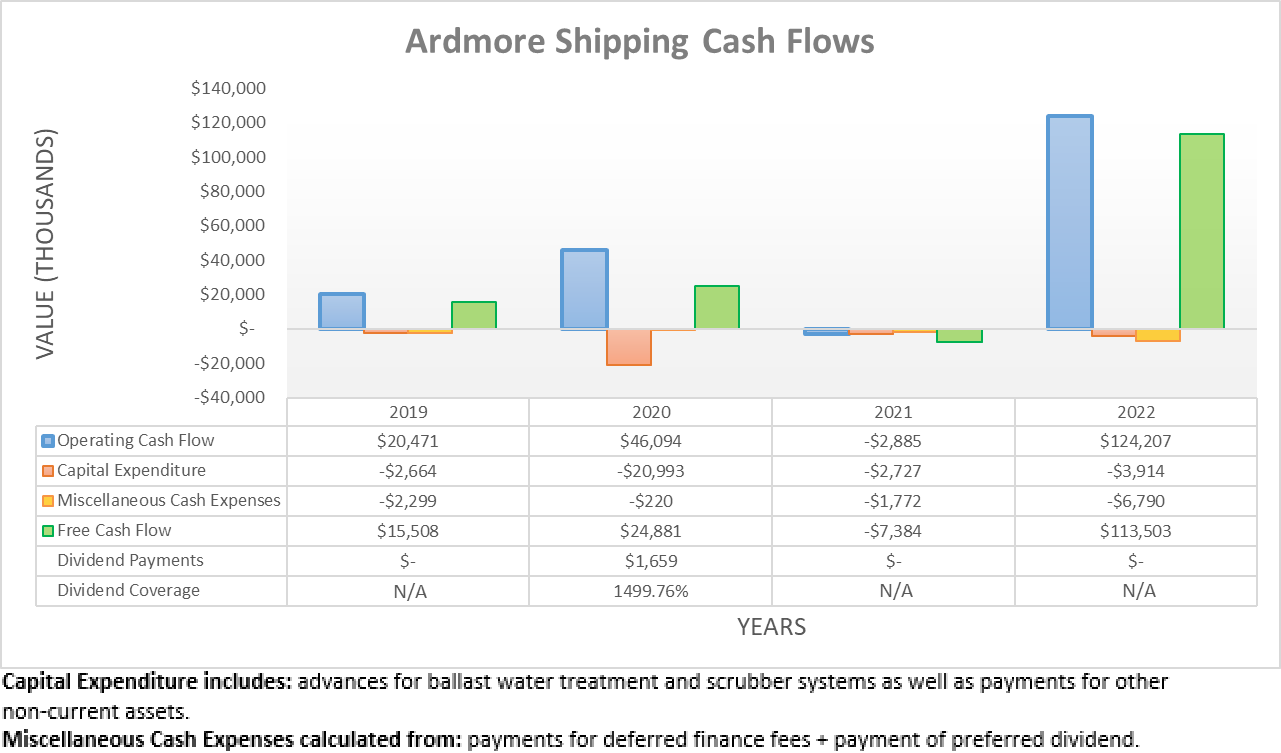

After struggling throughout 2021 with their operating cash flow at negative $2.9m, they saw a reprieve during 2022 as their result surged all the way to $124.2m. As many would suspect, this resulted from the fallout of the Russia-Ukraine war reshaping global energy markets alongside trade routes and thus sending charter rates surging for their refined product vessels, as evident on slide twenty-four of their fourth quarter of 2022 results presentation . Since they maintained their minimal capital expenditure during 2022 as was also evident during 2021, they were able to seize upon their very strong operating conditions to translate most of their operating cash flow into free cash flow, which ultimately landed at $113.5m during 2022.

{kind=link}

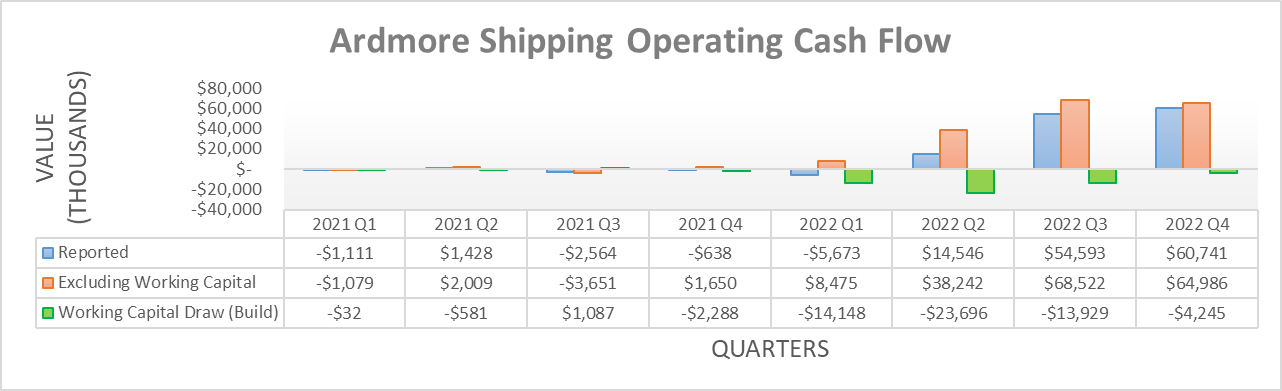

If viewed on a quarterly basis, it better shows their dramatic change of fortunes as their quarterly operating cash flow suddenly went from routinely negative single-digit millions during 2021 and early 2022 to a very strong $54.6m and $60.7m during the third and fourth quarters of 2022. This same story is shared regardless if viewing their reported results or their underlying results that exclude their working capital movements.

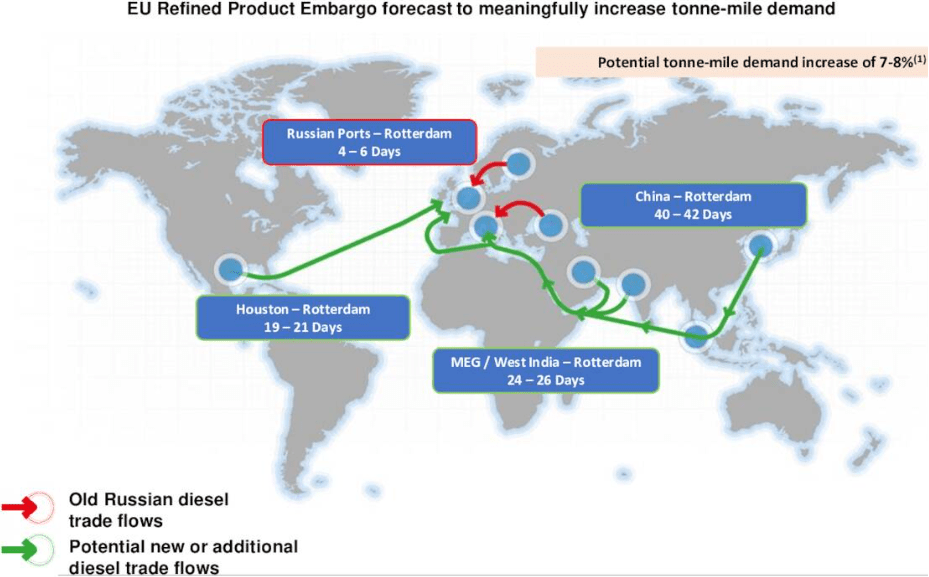

Due to the inherent volatility of the shipping industry, it is impossible to ascertain their future financial performance with high accuracy. That said, in this instance the backdrop is looking more bullish than a normal upcycle given the structural changes from the Western sanctions on Russia. What were once traditional and economically efficient trade routes for refined products are being upended, possibly never returning to the old ways as Western nations impose sanctions on Russia in punishment for their invasion of Ukraine.

Ardmore Shipping Fourth Quarter Of 2022 Results Presentation

{kind=link}

Whilst geopolitical events can be unpredictable, given the death toll in Ukraine is sadly rising ever higher as the war rages past the one-year mark, there is zero sign of Western sanctions easing and if anything, I feel they are more likely to tighten further. Even though this does not necessarily increase demand for refined products, it means greater shipping distances as Russian exports no longer enter Europe and instead have to make their way to Asian nations, such as China that does not abide by Western sanctions. The longer a voyage takes, the longer until that vessel can transport another cargo and thus, it sees an increase in what the industry calls, tonne-mile demand. In light of this structural change, management decided to reinstate their dividends with a new variable policy, as per the commentary from management included below.

“As a result of the strong performance and consistent with the capital allocation policy, we are pleased to declare a quarterly cash dividend of $0.45 a share, representing one-third of adjusted earnings.”

- Ardmore Shipping Q4 2022 Conference Call.

If interested in further details regarding the calculation of their new variable dividends, please refer to slide eight of their previously linked fourth quarter of 2022 results presentation. Whilst it may vary quarter-to-quarter alongside their prevailing financial performance, if annualized, their recent quarterly dividend of $0.45 per share equates to a very high near-11% yield on ASC stock's current price of $16.49. Quite importantly, this would only cost a modest $18.3m given their latest outstanding share count of 40,626,583. Due to this only modest cost, they could easily be repeated again, especially as they hopefully finish repaying net debt and thus possibly begin returning even free cash flow more via dividends, relative to their prevailing future financial performance.

{kind=link}

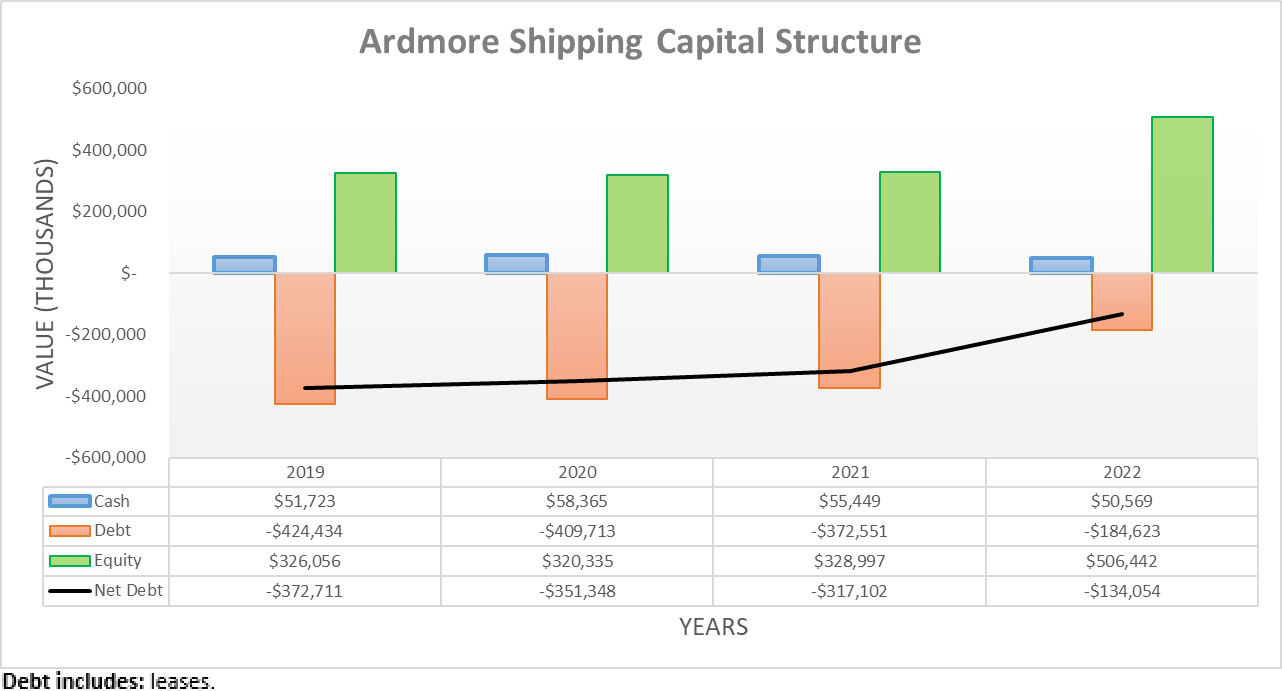

After spending the earlier years chipping away at their net debt, they were finally able to make solid inroads thanks to the strong operating conditions of 2022, thereby transforming their capital structure. By the end of the year, their net debt was down to $134.1m and thus saw them repaying more than half its previous level of $317.1m at the end of 2021. Whilst their free cash flow certainly led the way, it should be noted that its effect was further enhanced by $39.9m of divestitures alongside another $38.9m from equity issuances.

Going forward into 2023, it stands to reason their net debt should continue dropping even lower given their variable dividend policy. In fact, their net debt might even be eliminated during the year ahead if their very strong cash flow performance during the second half of 2022 persists going forwards. To this point, the fourth quarter saw operating cash flow of $60.7m that almost equals half of their remaining net debt. Assuming they maintain their minimal capital expenditure as evident throughout 2021 and 2022, the $18.3m cost to fund their recent quarterly dividend payment does not consume even half of their cash inflow, thereby leaving plenty for repaying net debt.

{kind=link}

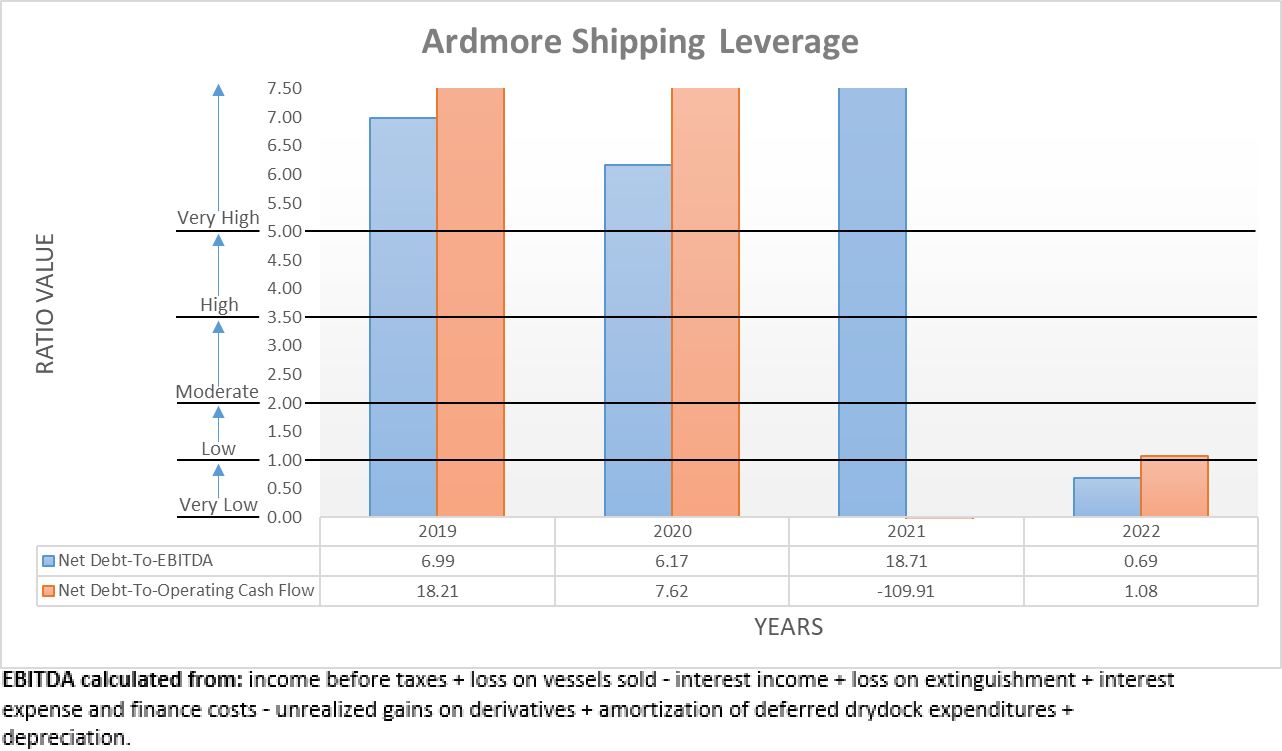

Thanks to transforming their capital structure via repaying more than half of their net debt, it also provided immense help with deleveraging. In the past, they struggled with leverage, such as during 2019 and 2020 when their net debt-to-EBITDA and net debt-to-operating cash flow were both above the threshold of 5.01 for the very high territory. As for 2021, their almost non-existent EBITDA and negative operating cash flow temporarily resulted in logically invalid respective results of 18.71 and negative 109.91, which obviously also meant their leverage was very high. Whereas right now, they see respective results of only 0.69 and 1.08, the former of which is even beneath the threshold of 1.00 for the very low territory, whilst the latter is only slightly above this threshold and thus within the low territory of between 1.01 and 2.00.

Admittedly, their results at the end of 2022 have also benefited from their recent strong financial performance, not just their significantly lower net debt. That said, their prospects to continue repaying more of their net debt throughout 2023 should cement these improvements and thus avoid a return to the days of struggling with leverage, even if future operating conditions weaken in 2024 and beyond.

{kind=link}

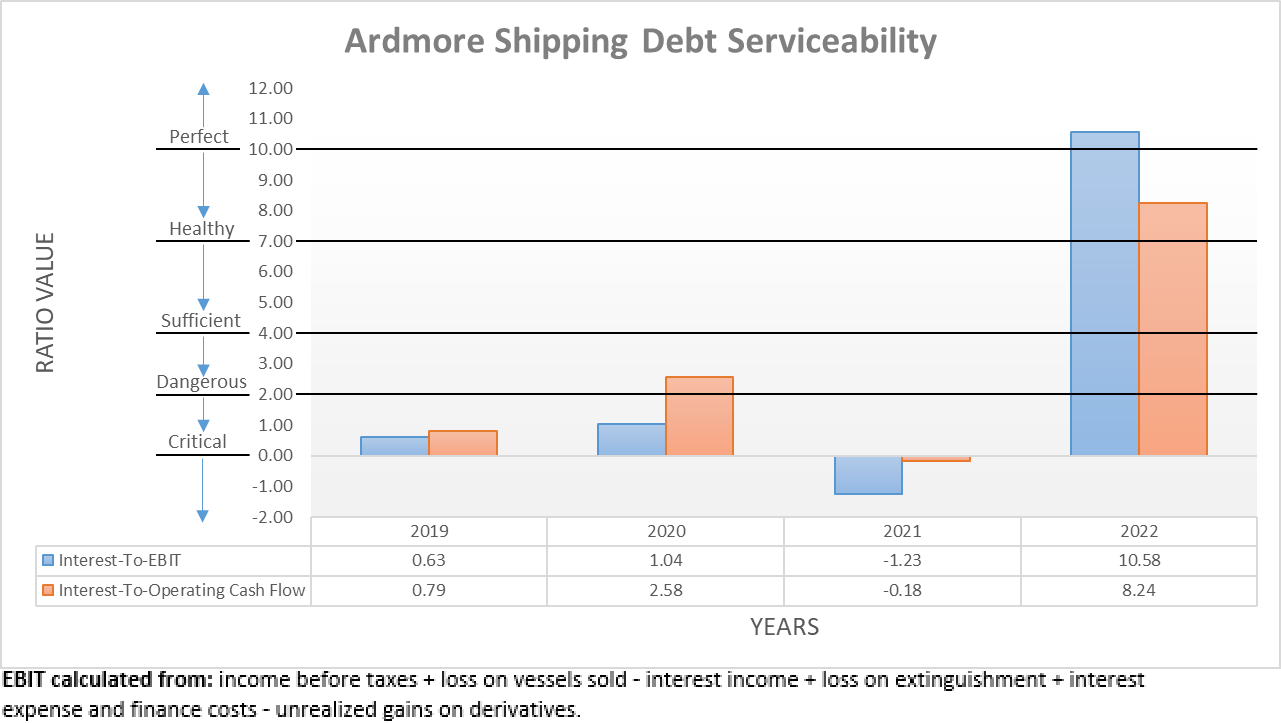

Similar to their leverage, the benefits of transforming their capital structure during 2022 continued to flow into their debt serviceability. Unsurprisingly, when they were previously plagued with very high leverage during 2019, 2020 and 2021, their interest coverage was often dangerous or critical with interest coverage seldom surpassing even the threshold of 2.01 for what I consider sufficient. Once again, this is a world of difference versus their interest coverage right now of 10.58 and 8.24 when compared against their respective EBIT and operating cash flow, which are both materially above the 7.01 threshold for what I consider perfect.

As they likely continue repaying net debt throughout 2023, their debt serviceability should only improve, similar to their aforementioned leverage. Furthermore, it should also lower their interest expense and thus, it could actually boost their free cash flow even higher in the future, relative to the prevailing operating conditions at the time. Whilst it remains to be seen how much more net debt they repay, if they were to eliminate the entire amount as previously flagged as a possibility, the savings would be material. To provide an example, 2022 saw a net interest expense of $15.6m that if removed, would have boosted their aforementioned free cash flow of $113.5m another near-14% higher, simply without doing anything else.

{kind=link}

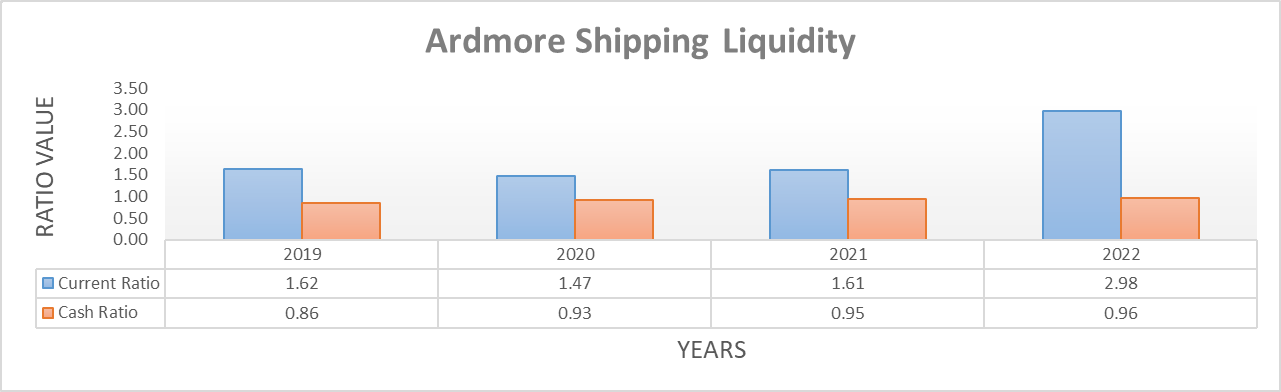

Whilst they previously struggled with debt problems, this seldom followed through into their liquidity with their current ratio always posting a result north of 1.00 during 2019-2021 and thus remaining adequate. To little surprise, this subsequently improved throughout 2022 to see results of 2.98 and 0.96 for their current and cash ratios, respectively. Thanks to their now strong liquidity and prospects to continue repaying net debt, they have little need for credit facilities nor concerns over future debt maturities, regardless of where monetary policy heads.

Conclusion

Normally, I am quite wary of shipping companies in general and especially during up cycles given the inherent volatility of their industry. Although in this instance, they see structural changes to their industry as trade routes shift following Western sanctions on Russian refined product exports that should fundamentally increase demand for their vessels. Equally as important, they made smart moves transforming their capital structure via repaying more than half of their net debt, which should continue during 2023. Apart from removing the risk of seeing a return to the days of struggling with leverage, it also increases prospects for even higher dividends, relative to their prevailing future financial performance throughout the up and down cycles and thus in this instance, I actually believe that a buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Ardmore Shipping’s SEC filings , all calculated figures were performed by the author.

For further details see:

Ardmore Shipping: Returning To Port With An 11% Yield Aboard