WEC - Are Pinnacle West Capital Investors Setting Themselves Up For A Fall?

2023-06-29 07:30:00 ET

Summary

- Pinnacle West Capital Corporation stock has outperformed its peers in the electric utility industry and major index ETFs, despite a challenging interest rate environment.

- My suggested trading strategy for Pinnacle West, which I consider low risk, is buying when the price approaches $70 and selling when it exceeds $80.

- The main risks to Pinnacle West stock include a severe recession, which could delay profits, and rate decisions in 2024.

- However, I maintain a "SELL" rating on Pinnacle West stock for any price above $80 and a "BUY" rating for prices nearing $70.

Introduction

Pinnacle West Capital Corporation ( PNW ) is the dominant electric utility in Arizona. In the electric utility industry, long characterized by slow, steady growth, Pinnacle’s performance has been stunning. It has far outpaced its industry, as in the comparison with five peers in the chart below: Consolidated Edison (ED), Southern Company (SO), WEC Energy Group (WEC), Alliant Energy (LNT), and NRG Energy (NRG).

YCharts

In an inflationary, rising interest rate environment, harmful to interest-sensitive industries like electric utilities, Pinnacle West has even outperformed major index ETFs like the SPDR® Dow Jones Industrial Average ETF Trust ( DIA ) and SPDR® S&P 500 ETF Trust (SPY). It even held its own against the high-flying Invesco QQQ Trust ETF ( QQQ ) until an upward burst in the QQQ in the last two months.

YCharts

The question naturally arises about why Pinnacle West has performed so strongly. Is this performance a sign of the future? In this analysis, we will answer that question, and look at what actions investors might want to take.

My Pinnacle West trading history

I have had a very profitable history with PNW since 2016. The strategy was to buy near a low (duh!), sell near a high, and then re-buy more shares with the proceeds when the price declined again. Reinvesting dividends increased the funds available. The investment history is below.

1/6/2016: Bought 300 sh. @ $62.16: Total $18,648

12/24/2018: Sold 300 sh. @ $85.82: Total $25,746

GAIN: $7,098

9/1/2020: Bought 350 sh. @ $71.57: Total $25,050

8/16/2022: Sold 387 sh. (includes 37 DRIP shares) @ $77.56 : Total $30,106

GAIN: $5,056

10/03/2022: Bought 360 sh. @ $66.51: Total $23,945

12/15/2022: Sold 364 sh. (includes 4 DRIP shares) @ $77.98: Total $28,748

GAIN: $4,803

My PNW trades have been quite rewarding, and I expect to be able to repeat the process again, but only at the right price. I planned on buying in 2023 around $70, which would have resulted in another quick gain this month, but the low was $72.12. Another opportunity could come along at any time, but patience is essential.

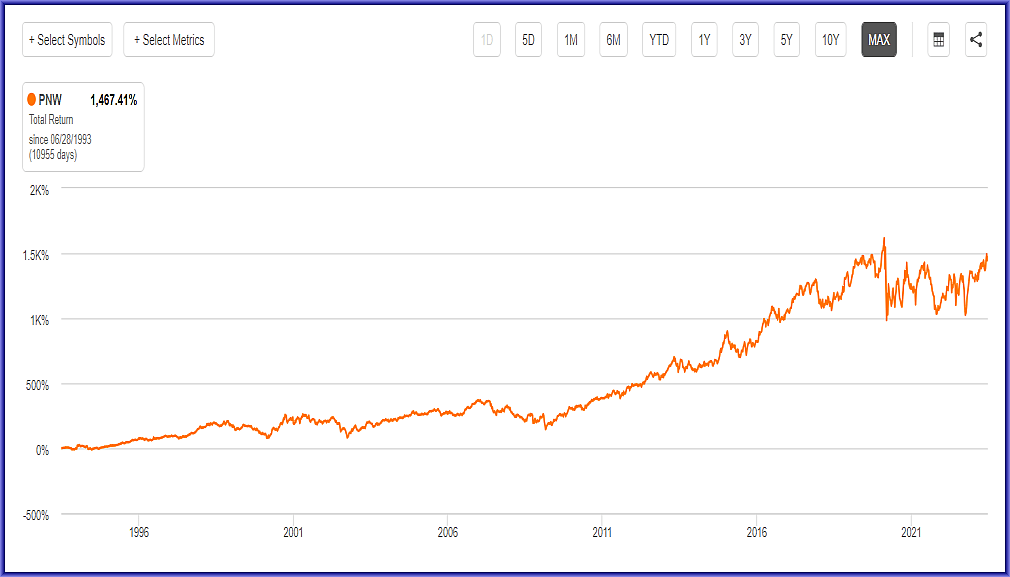

Recent Pinnacle West History

As the main utility in Arizona, Pinnacle West has had a reputation for rewarding shareholders at a slow but steady pace over time, as shown in the long-term chart below. Management is respected, and they operate in a growing service area.

{kind=link}

Then, as I detailed in my article , "Making Money With Pinnacle West When Everything Is Going Wrong," the regulators struck. In October 2021 the Arizona Corporation Commission reduced PNWs allowed return on equity from 10.0% to 8.7%, which analysts described as “draconian,” and the worst utility ROE in the country. Arizona is known as a difficult regulatory environment, but this was extreme. The stock price responded, going from $74.18 to $63.36 in short order. It had been as high as $87.88 in the summer.

Since then, PNW shares have gone from $63.36 to $84.59, up 33%. This is hard to explain based on company performance. Since the disastrous rate decision, Pinnacle West’s earnings have declined from $5.47 a share to $4.26 in 2022, a projected $4.06 in 2023. It will be 2024 before new rates might provide relief, and the amount of any relief is very uncertain.

YCharts

The price rise comes almost entirely from the increase in the P/E ratio above. The chart below shows the justifiable P/E ratio gap that opened up between PNW and peers as the impact of the Arizona rate case became evident in mid-2021. That gap has disappeared even though there has been no change in the outlook for PNW.

YCharts

In the chart below, we can see the magnitude of PNW forward P/E change compared to peers.

YCharts

What is behind the rise in PNW?

If financial projections don’t account for the premium, we must look elsewhere, and the primary explanation is investor sentiment. A lot has been going on in Arizona over the past several years, and the state has been receiving more than its share of attention. It was a hotbed of 2020 election controversy and a crucial state in the final results (and 2022 gubernatorial candidate Kari Lake continues to put it in electoral news even today). It is a center of domestic in-migration, the migration crisis from Central and South America, and the recent Western drought. It is proving to be central to the federal government’s high-tech industrial policy, with Intel (INTC), Taiwan Semiconductor (TSM), KORE Power , LG and others announcing massive investments in the state.

With this raised profile, investors start asking if there are investment opportunities to be had. Investors are encouraged by Arizona’s profile as a high growth state. A few of many examples of the state’s perceived growth potential:

- Phoenix Tops the Nation in Population Growth for the Fifth Year in a Row

- Arizona’s Economy Breaks New Ground Again

- Arizona's population growth leads the West in latest Census estimate .

Pinnacle West, as a major economic power in the state, is a natural focus of attention. Electric utilities expected to be an important beneficiary of economic and population growth. In their latest quarterly report , PNW includes customer growth as a positive for their business future:

Additionally, we continue to project steady population growth, along with solid APS customer growth. According to recent data from the U.S. Census Bureau, Maricopa County had the largest population increase in the U.S. in 2022 and led the nation in net domestic migration.

PNW is clearly in a position where growth in Arizona has led to positive sentiment and great improvement in the price/earnings ratio. But are the prices behind the higher PE justified?

Rain forecasted for the Pinnacle West Parade

The dominant factor in Pinnacle West’s earnings are Arizona regulators. Yes, growth in the state is a tailwind, but even in a high-growth state, the increase is only about 1.5%-3% a year. That number pales compared to the 22% hit to earnings in the immediate aftermath of the last rate decision. The ACC has determined the company will have depressed earnings at least through 2023. Earnings after 2023 will be determined by the next Arizona Corporation Commission rate decision.

Unfortunately, most of the stakeholders in Arizona will line up behind continued low profits for PNW. Arizona citizens, of course, like low electric rates, as do companies doing business in the state. Politicians on the lookout for votes will be on the side of voters and corporate ratepayers. Environmentalists will attack PNW, and as we have learned, no amount of effort to turn away from fossil fuels will be big enough or fast enough for them. These factors are present in many states, of course, but when they are added to a regulatory regime which is generally hostile it means improvement is unlikely.

The Seeking Alpha analyst consensus shows projected earnings of $4.84 for 2023, which would take PNW back to the level of 2020. This is mostly based on a favorable outcome in the next rate case and a minor favorable court decision in March . A number of Wall Street analysts, such as Wells Fargo , KeyBanc, Barclays and Evercore , are on record with negative outlooks. The only positive take is from Credit Suisse , whose opinion was a response to the March court case. Even there, though, as with the other publicly available analysts, the price target does not exceed $80.

What does this mean for PNW investors?

The stock price is unlikely to be driven upward by near or medium term fundamentals, and there are time limits on positive investor sentiment. However, the company does have a large, profitable, relatively stable business with generally well-regarded management. In this scenario, PNW is most likely to trade in a range, with its place in that range determined by the vagaries of general market factors. Since the 2020 recession, PNW has been in a range mostly between $65 and $85.

SELL Rating

At the current share price of $82.00, I give Pinnacle West Capital Corporation stock a rating of SELL. The SELL rating applies to any price above $80, in the upper part of its trading range. My previous rating, at a price of $72.61, was a BUY. I will give a BUY rating whenever the price starts to approach $70. These ratings will provide effective opportunities for trading, similar to what I outlined in the section on my past PNW trading above. If a $70 to $80 trading round trip can be done over a 12 month period, the returns will be:

$10 capital gain + $3.46 dividend = Total gain of $13.46, or 19.22 per cent.

Risks to the strategy

The main risk to this trading strategy is a recession, which would delay any profits from buying shares around $70. The strong relative growth in Arizona should still, over time, drive PNW earnings and share price higher, even with a difficult regulatory regime, and at $70 investors are getting a safe 5% dividend. Returns will eventually be positive, but on a longer time frame than investors prefer.

On the other side, a positive rate decision for 2024 would mean an immediate upward rating for the stock. General economic conditions can also play a role. If they improve through lower interest rates or other economic vectors, the stock could break to the upside. The “risk” here is that an investor would miss capturing the gain above $80, although a gain of $10 a share ($70 to $80) plus the 5% dividend would lessen the sting.

Summary and Conclusions on Pinnacle West Capital

Over the last 12 months, Pinnacle West’s stock total return is over 18%. This is far better than peers and even surpasses major indexes. This is a stunning result for a company in an industry characterized by slow growth and relatively predictable performance.

The gain, however, is not supported by fundamentals. Arizona regulators have put severe limits on the company’s return on equity for the next couple of years, and prospects of improvement beyond then are not good. The most plausible explanation for the gain is investor sentiment arising from projections of economic and demographic growth in the state.

Except for a few months, PNW has traded in a range of $65-$85 a share since the brief bear market that started in March 2020. There is a solid opportunity to trade the stock within the range of $70 and $80, or a wider range if you feel lucky. A trading round trip in this range over 12 months would mean a gain of over 19%. Considering the stability of Pinnacle West’s business and predictability of its performance, this is a particularly strong trade for conservative investors and income investors who like some capital gains thrown into the mix.

For further details see:

Are Pinnacle West Capital Investors Setting Themselves Up For A Fall?