BXSL - Ares Capital 10% Yield: Need To Check Credit Quality

2023-07-13 12:36:39 ET

Summary

- This article discusses portfolio credit quality for Ares Capital which is the largest BDC currently yielding 10%.

- Credit quality is the most important consideration when selecting which BDCs are "buy and hold" as well as setting target prices.

- The following is a quick discussion of specific portfolio companies including the amount of "watch list" investments, non-accrual investments, and the potential impact on NAV per share.

- If you're not getting this level of detail for each of your BDC investments, please consider taking a more detailed approach to due diligence each quarter.

- Next week, we will discuss dividend coverage for ARCC which is reporting Q2 2023 results in less than two weeks.

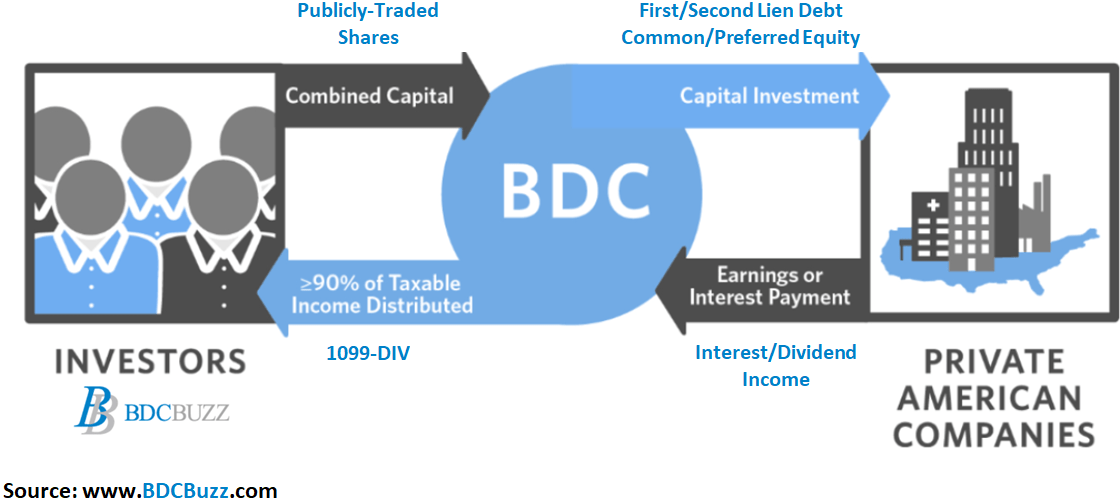

Quick Introduction To Business Development Companies

Business development companies ("BDCs") invest shareholder capital in privately-owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds. Anyone can invest in BDCs as they're public companies traded on major stock exchanges.

{kind=link}

BDC Buzz

The three biggest mistakes that new BDC investors make are:

- Not taking the time to dig into portfolio credit quality and assess which investments could potentially have a negative impact on earnings and NAV per share.

- Focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality.

- Not understanding why BDCs trade at different prices and thinking that price-to-NAV is the only measure to find a "good deal."

Please see the end of this article for a quick discussion of how BDCs are valued and the chart comparing the potential impact on net asset value ("NAV") per share assuming that 100% of watch list investments (including non-accruals) defaulted with 0% recovery.

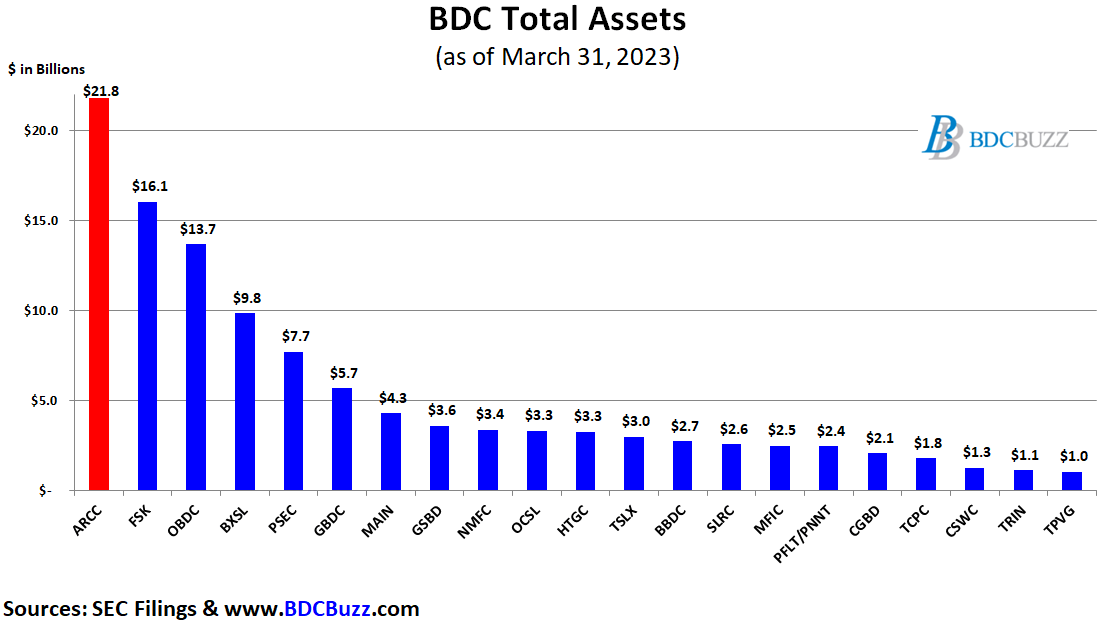

This article discusses portfolio credit quality (not dividend coverage) for Ares Capital ( ARCC ) which is the largest BDC (by any measure):

{kind=link}

BDC Buzz & SEC Filings

Please note that the BDCs in the previous chart account for around 90% of the total assets and market capitalization for the sector. Over the last few weeks, we discussed the portfolio credit quality and/or dividend coverage for many of them including FS KKR Capital ( FSK ), Prospect Capital ( PSEC ), Goldman Sachs BDC ( GSBD ), Hercules Capital ( HTGC ), PennantPark Floating Rate Capital ( PFLT ), PennantPark Investment ( PNNT ), TriplePoint Venture Growth ( TPVG ), Monroe Capital ( MRCC ), and BlackRock TCP Capital ( TCPC ) in the following articles:

- Better High-Yield Buy: FSK or PSEC?

- PennantPark: Big Win From Dominion/Fox Settlement

- Venture Debt Opportunity Yielding 13% To 14%: HTGC or TPVG?

- BlackRock Or PennantPark For Solid 12% Yield?

- Safer 12% Yield: Goldman Sachs BDC or Monroe Capital

BDC Buzz & SEC Filings

Next week, we will discuss dividend coverage for ARCC which is reporting Q2 2023 results in less than two weeks so make sure to watch for our updates.

BDC Buzz & SEC Filings

Many BDCs have investment grade ("IG") bonds/notes for lower-risk investors building a balanced 60/40 portfolio (composed of 60% to 70% stocks/equities and 30% to 40% bonds or other fixed-income offerings). These notes were previously overpriced, but prices have declined and are now at attractive levels. The following article is from last year when ARCC's notes were offering ~6% yield-to-maturity:

ARCC has eight bonds/notes totaling almost $8 billion that are currently yielding around 7% to 8% as shown in the BDC Google Sheets which was discussed earlier this week in " Introduction To BDC Google Sheets ."

{kind=link}

ARCC

Comparing Portfolio Credit Quality

The following is a quick discussion of specific portfolio companies which is absolutely critical when investing in the BDC sector. Credit quality is the most important consideration when selecting which BDCs are "buy and hold" as well as setting target prices. If you're not getting this level of detail for each of your BDC investments, please consider taking a more detailed approach to due diligence each quarter. We have seen many BDCs with higher amounts of first-lien positions and lower non-accruals underperform due to increased credit issues. One of the best approaches to assessing risk in a BDC portfolio is using a “vintage analysis” that takes into account many aspects including the time frame that each loan was originated, asset class, pricing, maturity date, directly originated vs. syndicated, industry sector, PIK vs. cash yields, etc.

During Q1 2023, ARCC exited its equity position in National College of Business and Technology resulting in a realized loss of $50 million partially offset by realized gains including the exit of Cipriani :

{kind=link}

SEC Filings

There was an increase in the amount of higher-risk internal credit Grade 1 and Grade 2 credit-rated investments, from 6.7% to 7.7% of the portfolio fair value, and likely includes many of the watch list investments discussed below. The weighted average grade of the portfolio at fair value declined slightly from 3.2 to 3.1.

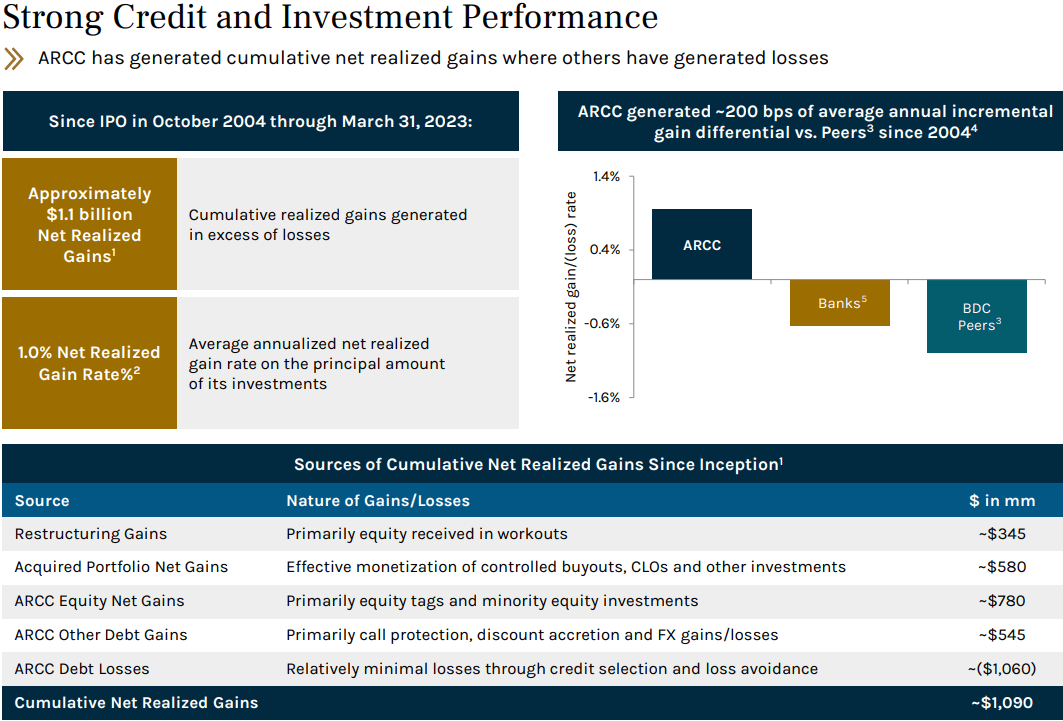

“The resulting health of the portfolio is demonstrated by our stable weighted average portfolio grade of 3.1 and our collection of 99% of contractual interest from our portfolio during the first quarter. Through our nearly two decades of operating ARCC, we have a time-tested playbook for successfully navigating periods of volatility and market cycles. In collaboration with our core investment teams, our portfolio management professionals focus on identifying problems early and developing strategies to maximize our outcomes. These capabilities are central to our ability to deliver our industry-leading track record for credit performance since inception. Which includes generating a 1% annualized net realized gain rate in excess of losses on our investment since inception. This means that along with generating gains on many of our investments, we have also successfully minimized losses in the portfolio in more difficult times.”

{kind=link}

SEC Filings

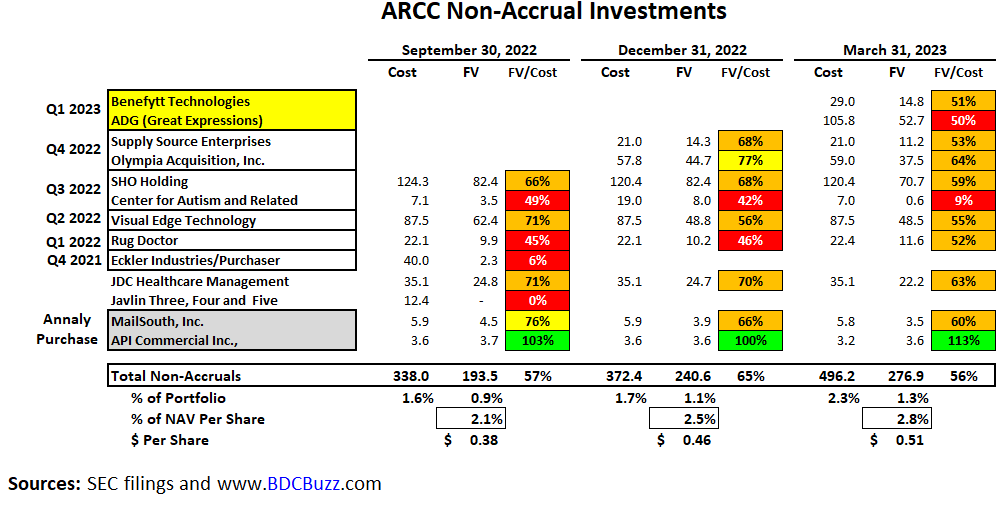

As expected, its watch list investment in Benefytt Technologies which is a health insurance platform, was added to non-accrual status during Q1 2023. BXSL also has a position in Benefytt which was previously amended to include a PIK portion (from 0.00% to 7.75%). In May 2023, Benefytt filed for bankruptcy after paying fraud settlements related to misleading consumers into buying “sham” health insurance plans. Benefytt’s liabilities are as much as $1 billion, while its assets are as much as $10 billion. Non-accrual investments increased slightly from 1.1% to 1.3% of the total portfolio fair value due to adding its watch list investments in Benefytt Technologies and ADG (Great Expressions, dental business mentioned later) partially offset by marking down SHO Holding (Shoes for Crews), Olympia Acquisition , and Supply Source Enterprises . Please note that ARCC has a very large portfolio with 466 portfolio companies valued at over $21 billion, so there will always be a certain amount of non-accruals.

With respect to non-accruals, despite increasing modestly this quarter, our nonaccrual rate is meaningfully below our 15-year historical average and is substantially below the historical KBW BDC average for the same time through year-end 2022. Our portfolio quality is also reinforced by the substantial amount of equity invested in our companies, most often by large and well-established private equity firms. At the end of the first quarter, the weighted average loan to value in the portfolio, including that through our junior loan investments was only 43%, which we believe gives us strong downside protection on our loans.”

{kind=link}

BDC Buzz & SEC Filings

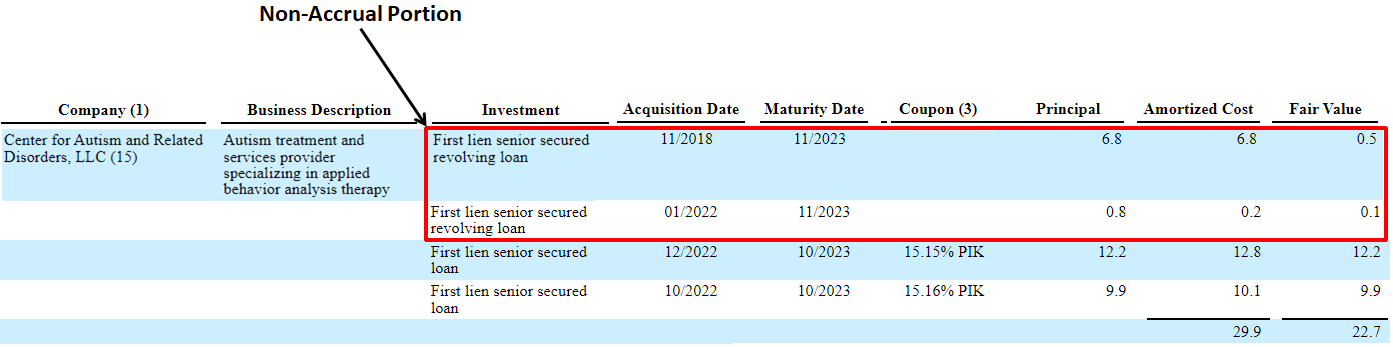

Center for Autism and Related Disorders (“CARD”) is an autism treatment and services provider specializing in applied behavior analysis therapy which was added to non-accrual during Q3 2022. In June 2023, the company filed for Chapter 11 bankruptcy due to a $82 million net loss in the 12 months ending April 2023, largely as a result of the long-term impacts of the COVID-19 pandemic. The center entered bankruptcy with just $2 million in cash on hand, and it intends to fund its bankruptcy with an $18 million loan from its primary lender, ARCC.

The debtors have struggled since ‘20. First, the pandemic brought on severe labor shortages in the healthcare space and “it became exceptionally more difficult to recruit and retain qualified behavioral therapist[s] to administer CARD’s [applied behavior analysis] treatments to its patients.” Second, the labor CARD did have become increasingly expensive due to the overall explosion of the cost of labor in the US. Third, the debtors’ lease obligations and corporate overhead costs were an albatross at a time when in-person services came to a halt. Fourth, CARD is party to a number of existing payor contracts dating back to ‘12-’16 that are no longer profitable due to growing medical inflation: The reimbursement rates are far too low these days for certain treatments. Fifth, the debtors are subject to a variety of lawsuits including a class action in California. And, finally, there’s the debt:

CARD Bankruptcy Filing

It's important to point out that only the revolving loans for CARD were on non-accruals status as of March 31, 2023:

{kind=link}

SEC Filings

Visual Edge Technology was added to non-accrual during Q2 2022 and is a provider of outsourced office solutions with a focus on printer and copier equipment and other parts and supplies. MailSouth, Inc. and API Commercial are smaller non-accrual investments from the direct lending portfolio of Annaly Capital, acquired during Q2 2022. RugDoctor (manufacturer/marketer of carpet cleaning machines) was added during Q1 2022 and is a legacy investment from the ACAS acquisitions.

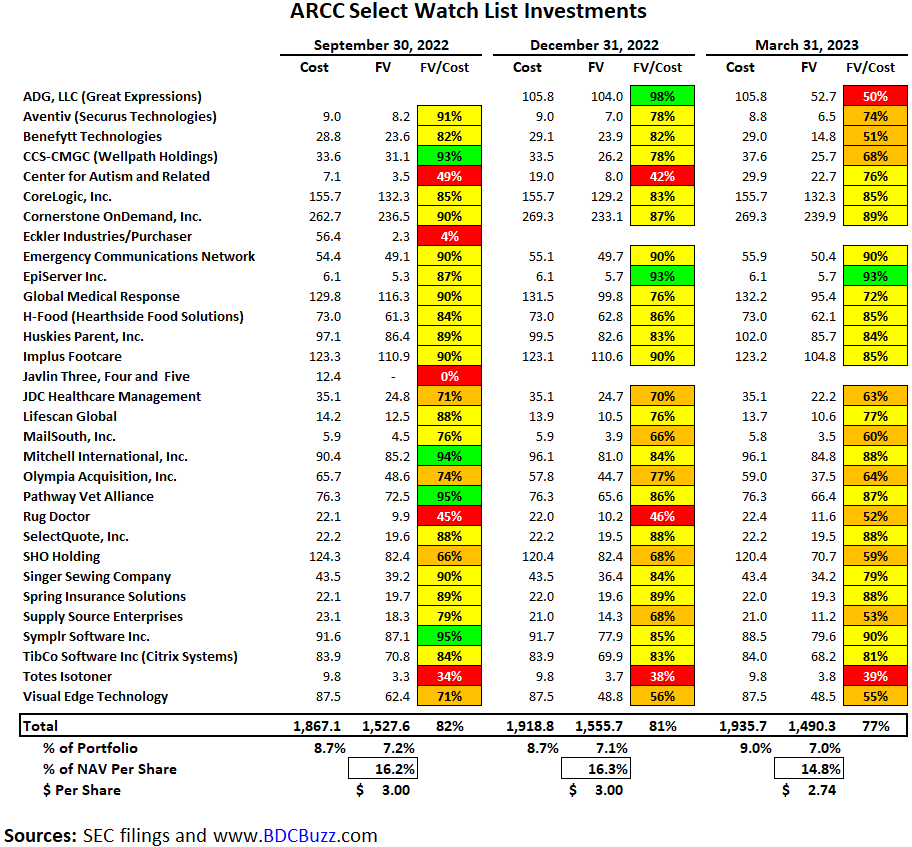

The following table shows many of ARCC’s "watch list" investments, which remain around 7% of the portfolio fair value (9% of the cost) that are likely many of the higher-risk Grade 1 and Grade 2 credit-rated investments mentioned later. Many of these companies are included in the previous table (showing non-accrual investments), but keep in mind that not all investments for these companies were considered non-accrual (similar to CARD as mentioned earlier). This table includes all investments for those companies. Many of the larger watch list investments, which are not on non-accrual, remain marked near or over 80% of cost. See later for discussions of some of the larger watchlist investments.

My primary concerns include ADG (Great Expressions), Benefytt, Supply Source, Olympia Acquisition, CCS-CMGC (Wellpath Holdings), SHO Holding , and JDC Healthcare which have been continuously marked lower (under 70% of cost) and currently account for 2% of the portfolio and 4% of NAV per share.

{kind=link}

BDC Buzz & SEC Filings

On May 17, 2023, ADG/Great Expressions Dental Centers (“GEDC”) filed a notice of data breach after determining that an unauthorized party was able to access and remove certain confidential patient information from the company’s computer network. After confirming that patient data was leaked, GEDC began sending out data breach notification letters to all individuals who were impacted by the recent data security incident.

SHO Holding (Shoes for Crews) is a manufacturer and distributor of slip-resistant footwear that's also held by GBDC, which currently has this investment on accrual status. However, ARCC’s position is second-lien at $129 million (maturity date of October 2024) compared to GBDC’s position, which is a smaller senior loan at $4 million (maturity date of April 2024).

CCS-CMGC (Wellpath Holdings) is a correctional facility healthcare operator that was downgraded by Moody’s in March 2023 from B3 to Caa1 citing labor and pharmacy costs, among other challenges, as reasons for the downgrade.

Singer Sewing Company is a manufacturer of consumer sewing machines also held by OCSL , which recently marked its first-lien position down to 86% of cost, compared to ARCC currently marked at 79% of cost. It's important to note that Platinum Equity Partners purchased a majority stake in Singer from ARCC in 2021and recently provided $50 million of additional financing with a 20% PIK coupon likely due to continued liquidity issues:

At the end of fiscal 2022 SVP-Singer completed a capital injection transaction provided by its financial sponsors, Platinum Equity Partners, via new $50 million senior secured first lien notes due 2028 (unrated). The notes are pari passu with the existing first lien term loan facility due 2028, and bear an interest of 20.0% payable in-kind ((PIK)). Proceeds from the PIK notes were used to repay borrowings outstanding on the company's $70 million asset based lending ("ABL") revolver due 2026 (unrated), and to increase cash on balance sheet. SVP-Singer had $47.5 million revolver borrowings outstanding as of 30 September 2022. Revolver borrowings were used in part to cover ongoing cash flow deficits in 2022 driven by meaningfully lower earnings, higher interest expense and elevated inventory levels. The capital injection transaction demonstrates financial support by the company's financial sponsors, and provides SVP-Singer with needed near term liquidity given its ongoing cash flow deficits. Moody's believes SVPSinger's 2022 earnings are below normalized levels due to cost increases and a significant overestimation of demand. Moody's expects the company's earnings will improve in 2023, but that leverage will remain high. The company will need to meaningfully improve its profitability and cash flow to be able to service its debt without the need for external financing. Persistently high inflation and weakening macro-economic conditions is pressuring consumer discretionary spending, which will make it challenging for the company to meaningfully improve revenue, earnings and cash flows."

Supply Source Enterprises is a manufacturer and distributor of personal protection equipment, commercial cleaning, maintenance, and safety products that recently announced layoffs:

Supply Source Enterprises, has submitted a WARN with the Ohio Office of Workforce Development. The letter explains that the company will carry out a reduction in force at its Toledo distribution center at 2840 Centennial Road in Toledo. The first separations are expected to occur within the 14-day period beginning on December 26, 2022.”

H-Food Holdings ( Hearthside Food Solutions) is an investment also held by ORCC and was previously downgraded by Moody’s partially due to supply chain and inflationary issues but affirmed its credit ratings:

The outlook revision to negative from stable reflects Moody's expectation that Hearthside's operating performance will remain weak and free cash flow will remain negative in the next 12 months as the company faces inflationary headwinds, labor issues, and supply chain challenges. An inability to execute an operational turnaround and reduce leverage will make it challenging to refinance approaching maturities (revolver in November 2024 and first lien term loan in May 2025) and would increase default risk. Moody's nonetheless affirmed the ratings because the company should be able to reduce Moody's adjusted debt-EBITDA leverage to below 8x within the next 12 to 18 months through EBITDA growth in 2023, as recently implemented price increase help to offset inflationary headwinds . In addition, employee wage increases have helped to improve the fill rates at its plants and should eventually reduce employee turnover. Hearthside's supply chain issues could persist in the next 6 to 12 months. However, Moody's believes the company should be able to restore EBITDA growth in 2023 due to implemented price increases that will help offset inflationary headwinds despite continued supply chain challenges .”

Global Medical Response (“GMR”) is an emergency air medical services provider that could be impacted by the " No Surprises Act . " The previous table shows the total value of its first and second lien, as well as warrants currently marked at 72% of cost (down from 90% the two quarters ago).

No Surprises Act: “Starting on Jan. 1, 2022, you generally won’t be responsible for balance bills or out-of-network cost-sharing when getting emergency care, non-emergency care from out-of-network providers at certain in-network facilities, or air ambulance services from out-of-network providers. When this happens, instead of you paying for unexpected out-of-network costs, you’ll generally only need to pay your normal in-network costs.”

SelectQuote , Inc. ( SLQT ) is a publicly traded online insurance platform (that is also held by BXSL ) that remains valued at 88% of cost. Its credit agreement was previously amended to tighten covenants (a good thing for creditors) but also there was a slight increase in the amount of payment-in-kind (“PIK”) income (from 0.00% to 2.00%).

... amend the Company’s existing financial covenant to better align with its business plan and add an additional minimum liquidity covenant, terminate certain delayed draw term loan commitments and reduce the revolving line under the Credit Agreement form $135 million to $100 million, introduce a minimum asset coverage ratio for any borrowing of revolving loans that would result in a total revolving exposure of more than $50 million and provide certain lenders with the right to appoint a representative to observe meetings of the Company’s board of directors.”

Emergency Communications Network is also held by CGBD and is a provider of advanced critical communications and emergency notification systems that was previously combined with Send Word Now and rebranded as OnSolve. Previously, Ares Capital Management served as the joint lead arranger and bookrunner and ARCC served as the administrative and collateral agent for a senior credit facility in support of the strategic acquisition of Send Word Now by OnSolve, a Veritas Capital portfolio company.

CoreLogic, Inc. provides analytics, software, and other outsourced services primarily to the mortgage, real estate, and insurance sectors and is one of ARCC’s larger investments that need to be watched especially given the previous markdowns of its second lien and equity positions.

Tibco Software (Citrix Systems) is a relatively new investment in a provider of server, application, and desktop virtualization, networking, and cloud computing technologies which was added to the list in Q3 2022 (only its second-lien position).

In a deal closed in August, Citrix Systems was acquired in a deal led by Vista Equity Partners. To finance the deal, the newly emerging combination of TIBCO software and Citrix launched offerings in the high-yield and leverage loan markets for a combined $8.5 billion. Ultimately, the offerings were heavily discounted to yield 10%. On the transaction Wall Street reportedly lost $700 million. In the same quarter as the Citrix note losses, quarterly institutional issuance in the leverage loan market fell to its lowest level since late 2009.”

{kind=link}

ARCC

{kind=link}

ARCC

The following table shows the potential impact on ARCC’s NAV per share using a range of default rates only for its watch list and non-accrual investments , but also considering a range of potential recovery rates.

For example:

- If 100% of these investments defaulted with a 0% recovery, the negative impact on NAV per share would be around $2.74 or 14.8%. This is the worst-case scenario for this group of investments .

- If 50% of these investments defaulted with a 50% recovery, the negative impact on NAV per share would be around $0.48 or 2.6%.

- If 20% of these investments defaulted with an 80% recovery, the slightly positive impact on NAV per share would be around $0.02 or 0.1%.

It's important to understand that ARCC’s watch list (includes its non-accruals) is currently marked at an average of 77% of cost and any changes to other investments will also have an impact (positive or negative).

{kind=link}

BDC Buzz & SEC Filings

BDC Valuations

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with updated target prices and suggested limit orders (for making purchases) for ARCC .

There are very specific reasons for the prices that BDCs trade driving higher and lower NAV multiples mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). BDCs with higher-quality credit platforms and management typically have higher-quality portfolios and investors pay higher prices. This drives higher multiples to NAV and lower yields.

{kind=link}

BDC Buzz

The charts below compare the various credit metrics for ARCC including the amount of watch list investments and the potential impact to NAV, non-accrual investments, and changes in NAV per share for one, three, and five years.

{kind=link}

BDC Buzz

{kind=link}

BDC Buzz & SEC Filings

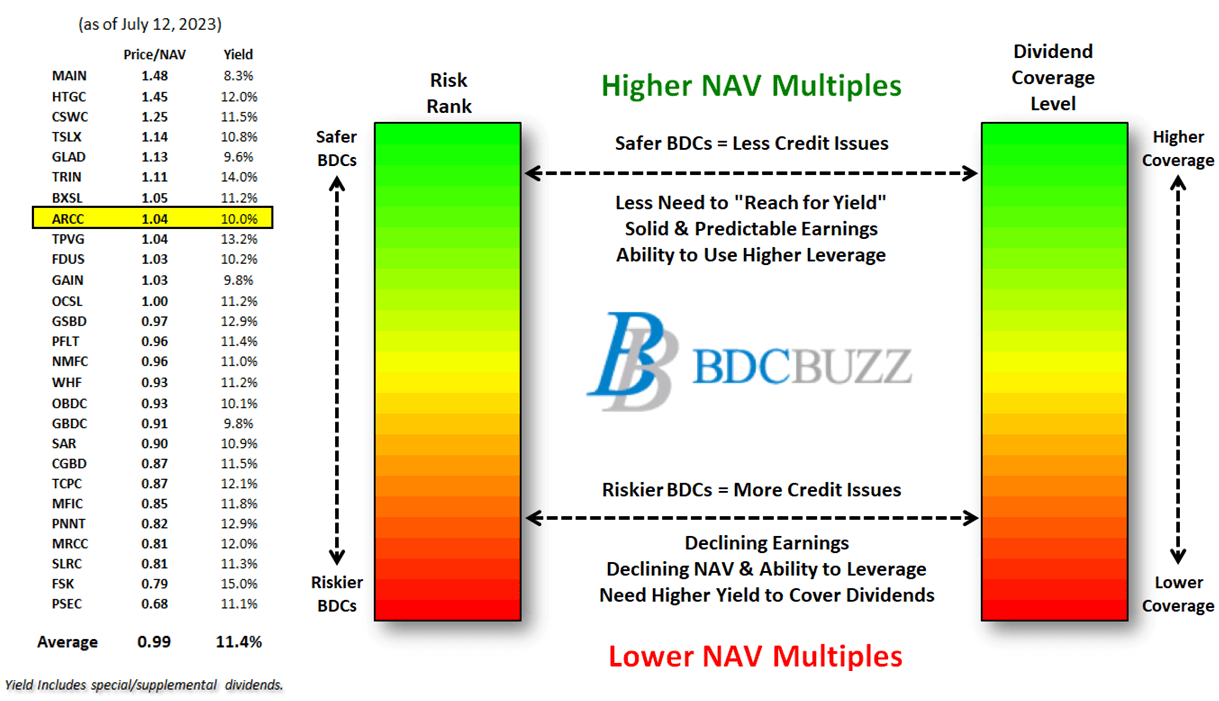

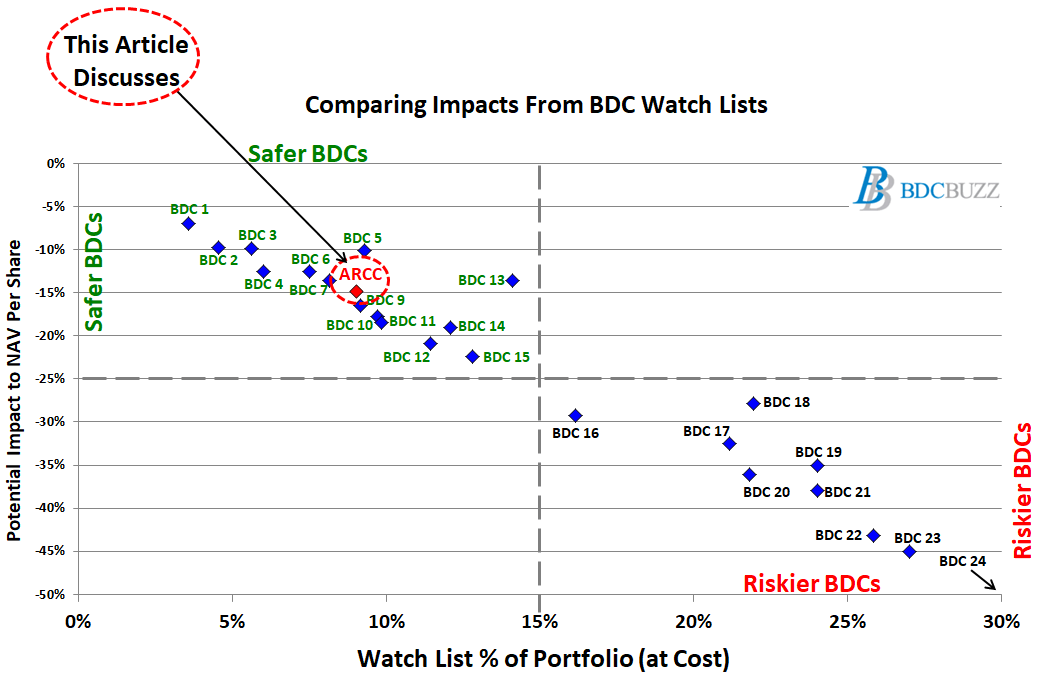

The following chart shows the potential impact on NAV per share for each BDC, assuming that 100% of watch list investments (including non-accruals) defaulted with 0% recovery. This is the worst-case scenario for this group of investments. The largest NAV declines over the last four quarters were mostly BDCs with larger amounts of watch list investments. Subscribers who believe the economy is headed for a "hard landing" with a deep, broad, and/or extended recession should focus on the BDCs closer to the top left corner.

{kind=link}

BDC Buzz

ARCC Important Considerations

As mentioned earlier, we will be discussing dividend coverage for ARCC next week before its reports Q2 2023 results in less than two weeks so please keep a lookout from us for updates.

The following are positive considerations , some of which are discussed in this article:

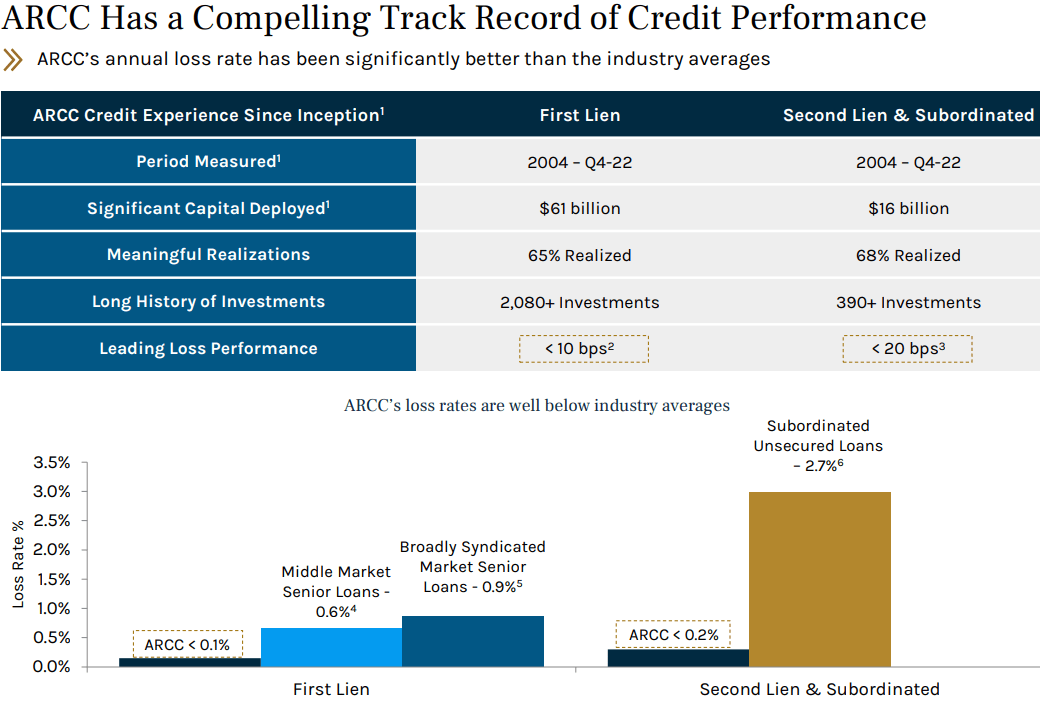

- 18-year history of very low defaults/credit losses

- NAV per share has increased by almost 10% over the last five years (much better than most BDCs)

- Net realized gains of almost $1 billion or around $1.75 per share over the last 10 years

- Increased its regular quarterly dividend from $0.36 to $0.48 per share (last 11 years)

- Investment grade ratings by S&P (BBB), Moody’s (Baa3), and Fitch (BBB)

- Strong coverage ratios for its fixed-income investors

- Lower-than-average leverage due to recently issued shares (including its ATM program)

- Current dividend is adequately covered, especially given that the company has earned an average of over $0.54 per share over the last two years

- Continued increase in returns from Ivy Hill Asset Management (“IHAM”)

- Management is “cautious about raising the dividend” and chose not to raise “because we'd like a stronger view on where we see rates normalizing in the future”

- Paid supplemental dividends of $0.12 per share in 2022

- Undistributed taxable income (“UTI”) of around $1.19 per share

- 69% of borrowings are unsecured (more flexible)

- 1.3% of portfolio investments at fair value on non-accruals status

- The amount of ‘watch list’ investments remains around 9% of the portfolio at cost

- Highly diversified with mostly larger middle market companies that would likely outperform in a higher interest rate and/or an extended recessionary environment

- The top 10 investments accounting for 12% of the portfolio

- Conservatively marked portfolio (higher quality reported NAV)

- Ares Management platform is higher quality

The following are negative considerations , some of which are discussed in this article:

- Many of its healthcare positions have been negatively impacted by labor shortages and/or wage inflation combined with higher rates

- Center for Autism and Related Disorders filed for Chapter 11 in June 2023

- ADG, LLC (Great Expectations), Benefytt, Supply Source, Olympia Acquisition, CCS-CMGC Holdings, SHO Holding , and JDC Healthcare have been continuously marked lower (under 70% of cost) and account for 2% of the portfolio and 4% of NAV per share

- SelectQuote was previously amended to include PIK and remains on watch list

- CCS-CMGC (Wellpath Holdings) was downgraded by Moody’s in March 2023

- Potential dilution to common shareholders from 2024 convertible notes which are convertible at $19.62 per share beginning in December 2023

- Potentially no supplemental dividends as management is retaining as a cushion to support “our goal of maintaining a steady dividend throughout market cycles”

- $1.3 billion of upcoming maturities for its March/June 2024 unsecured notes

- Slightly higher-than-average amounts of non-cash/PIK income

- Only 41% of the portfolio is first-lien

- Lack of ‘total return’ hurdle or ‘look back’ provision when calculating income incentive fees to protect shareholders from capital losses

- Potentially lower NAV and higher amount of watch list investments

For further details see:

Ares Capital 10% Yield: Need To Check Credit Quality