OWL - Ares Management: Amazing Returns Of The Past Are Likely To Persist In The Near Future

2023-05-14 05:35:21 ET

Summary

- Ares has achieved 20%+ annual returns historically and in recent years.

- At this point, Ares is trading on par with other alt managers but may grow faster.

- Ares' main business is lending to low-grade borrowers. It represents risks under unfavorable macro conditions.

I first heard of Ares Management ( ARES ) in 2013, shortly before its IPO the following year. At that time, Alleghany Corporation (now a part of Berkshire Hathaway ( BRK.A ) ( BRK.B )), the most circumspect and conservative insurer I have ever followed, invested $250M in Ares and contributed about $1B to Ares-managed funds. I immediately marked Ares as a promising company.

Between the Big Six of alternative asset management (the others are Blackstone ( BX ), Brookfield ( BN ) ( BAM ), Apollo ( APO ), KKR ( KKR ), Carlyle ( CG )), Ares is arguably the smallest and the least-known. But it is one of the best in terms of performance.

Nine years ago, it started trading at around $18 and is currently at ~$81. This represents 17% CAGR plus 3-4% yield for a total of 20+% annual return. If we check only recent performance limited to, say, the last 3 years it is even more impressive.

Is Ares poised to continue delivering similar returns? Let us start with the basics.

The company's structure

Ares traces its history to the nineties, became public in 2014 as a partnership, and got incorporated in Delaware in 2018. Similar to its peers, it has a complicated structure with three classes of shares and an operating partnership 60%-owned by the public corporation. The remaining 40% of the partnership is owned by founders and senior management. Partnership units are exchangeable into public voting (class A) shares on a one-for-one basis.

Two other classes of shares (B and C) are non-economic and are also owned by the same insiders. These classes exist only to provide insiders with voting control. Besides three classes of voting shares, there are also non-voting shares that have the same economic rights as class A shares and belong exclusively to Sumitomo Mitsui Banking Corporation.

Assuming the full exchange of partnership units and not voting shares for Class A common shares, founders and management would hold 44.48%, Sumitomo Mitsui would hold 5.72% and the public would hold 49.80% of Ares Management Corporation. Some of the public class A shares are also owned directly by Ares employees. Together all insiders (founders, management, and employees) hold close to half of economic interests and eat their cooking.

Ares and peers

The easiest way to describe Ares is by comparing it with other big alt managers. It is different from each of them.

First, Ares is persistently asset-light meaning that the company invests the minimum capital legally required in the funds it manages. In this regard, it is comparable with Blackstone or the new BAM.

However, differently from Blackstone, it is a management fee-centric company. As a reminder, alt managers, broadly speaking and slightly oversimplifying, extract three types of fees from the funds under management - recurring management fees (often grouped with much smaller transactional fees), performance fees (accrued periodically but based on achieving certain targets), and carried interest that is realized only after exiting from investments. For Blackstone, management fees, on average, are comparable in size to performance fees and carry. For Ares, management fees dominate and this difference has important implications for the dividend policies of both companies.

Since management fees are recurring and predictable, Ares' quarterly dividends do not change from quarter to quarter during a calendar year. Almost all of the management fee-related earnings ("FRE") are being paid out while performance fees and carry are being retained for business development. Blackstone, on the contrary, pays out about 85% of all distributable earnings, and the dividend changes from quarter to quarter.

Most of the big alt managers started as buyout outlets (aka private equity) and later diversified into other lines of business - private credit, real estate, infrastructure, etc. The public, at large, still considers alt managers as private equity even today underestimating their earning potential and overestimating the risks involved. But Ares does not fit this pattern: private credit has been and remains its dominant segment dwarfing other lines of business.

Today, Ares has 4 main segments - Credit, Private Equity ("PE"), Real Assets ("RA"), and Secondaries. One can measure their size by either assets under management ("AUM") or fee-generating assets under management ("FGAUM"). Both metrics are related since assets that do not generate fees become fee-generating typically within 18 months. For the rest of this article, we will use FGAUM as the main metric.

Out of ~$234B of FGAUM, Credit accounts for ~$154, PE - for ~$19B, RA - for ~$41B, and Secondaries - for ~$18B. The balance belongs to the "other" segment.

Of all alt managers, only asset-heavy Apollo is so much skewed toward credit. But this is but a token resemblance. While Apollo is focused on investment-grade credit and invests heavily in its own product, Ares operates mostly in low-grade debt and opts out of carrying its product on its balance sheet. This is an important point that we will revisit later.

The new BAM is the best comp as it is both management fee-centric and asset-light. But this comp is not ideal either: BAM is better diversified between different alts and has been in existence for less than two quarters. We would argue that BAM can be analyzed using Ares but not vice versa.

Growth

I started this post by showing ARES stock's impressive annual returns of 20+%. These returns closely match the growth of the underlying business as Ares targets and delivers ~20% growth in terms of FGAUM without a glitch. In its turn, this growth leads to a ~20% dividend bump every year recently. From a dividend seeker's standpoint, Ares appears the most impressive among all big alt managers.

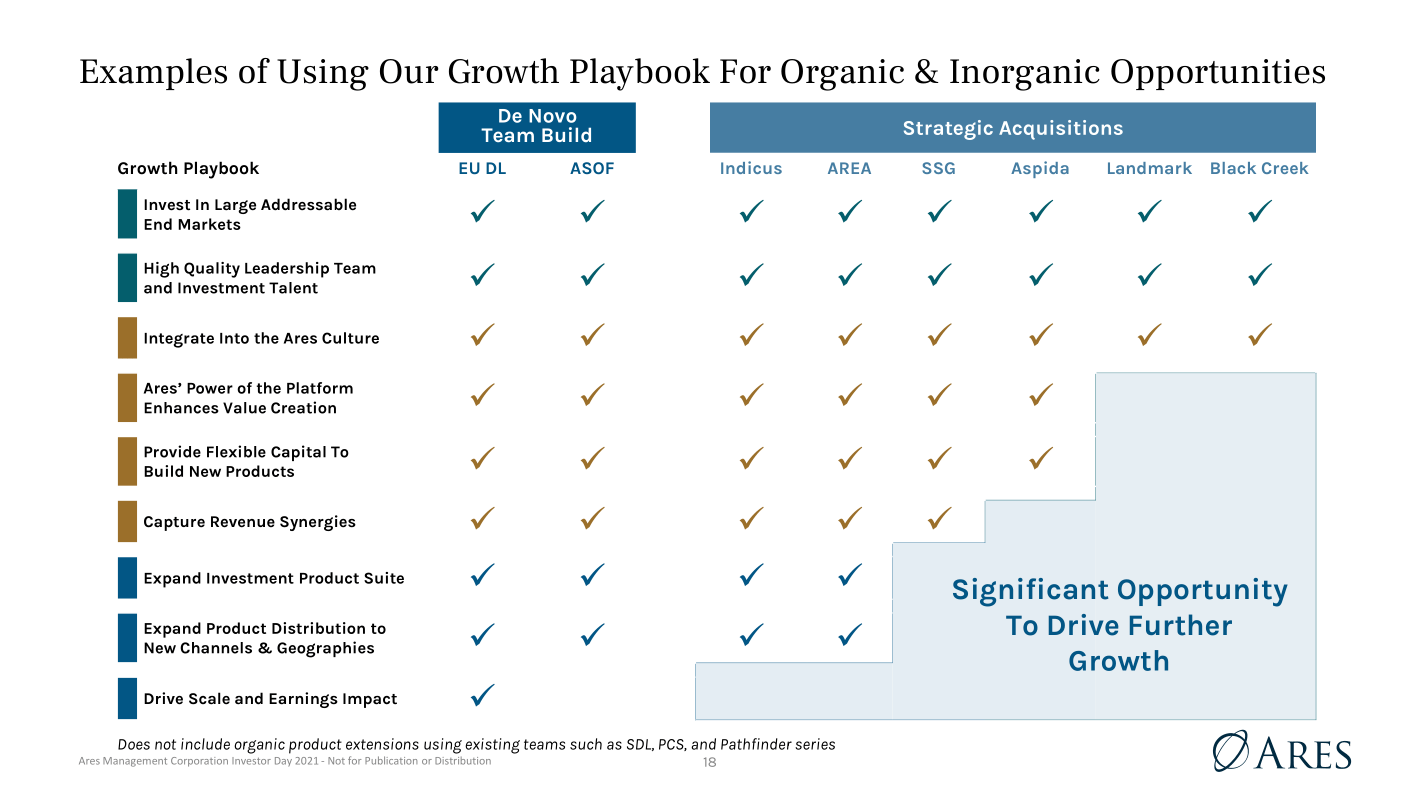

Besides scaling up existing strategies, Ares consistently adds adjacent products by either building them from scratch or via acquisitions as the following slide shows:

{kind=link}

Company

This is not different from what other alt managers are doing but Ares seems more active on the acquisition front. As follows from the slide, quite a few past acquisitions still have growth potential.

Overall, Ares is smaller than other dominant alt managers (e.g. four times smaller than BX and two times smaller than BAM or APO) and can grow faster, especially against the favorable macro backdrop as explained in the next section.

Valuations

Since asset-light alt managers pay out almost all distributable earnings, the simplest way to value them is by dividend yield. Below is a table with the current yields:

{kind=link}

Author, companies' filings

The results of the table are quite consistent. Only Blue Owl ( OWL ) is trading at a higher yield which is not surprising - it is much smaller and newer than others.

The next table presents historical yields for Ares:

Author, companies' filings

Based on it, Ares is currently trading closer to a higher end of its normal range. Perhaps, this can be easily explained as well. Since the Great Financial Crisis and subsequent legislation (Dodd-Frank, etc.), banks have become less aggressive in offering credit because of additional regulations. Recently this trend exacerbated due to the banking crisis. As a result, banks' market share in commercial lending has shrunk which is beneficial for alt managers specializing in credit. Alternative credit, as it is called, is in vogue and it may allow Ares and similar companies to grow even faster.

There are indications that Ares is already benefiting from this trend and keeps firing on all cylinders. In Q1 2023 , it raised $16B in new capital while mighty BAM (that has credit specialist Oaktree as a subsidiary and is twice bigger) raised only $13B.

Please note that towards the end of a calendar year, Ares tends to trade at a lower yield as investors anticipate the next dividend bump. In the case of "business as usual," we can expect valuations to reach ~3% yield in late 23 or early 24 which corresponds to the ~$100 stock price.

Currently, Ares has ~$234B of FGAUM and a market cap of ~$25B. It means that the market values each dollar of FGAUM at approximately 11 cents. This is rather cheap. The same metric for Blackstone is 16 cents on average (currently, BX is trading at 14 cents). For Owl, the same metric is ~15 cents. This comparison also indicates Ares' likely appreciation.

$61B of Ares' AUM are not paying fees yet with $47B of them in credit strategies. They should become a part of FGAUM within the next 12-18 months in an environment extremely favorable for alternative credit. No doubt there will be other inflows as well. It almost guarantees that the same 20% growth rate will remain intact for at least one extra year and investors can count on a dividend of ~$3.70 or even higher in 2024.

Risks

Ares is focused primarily on low-grade debt in different shapes or forms and arguably shaky borrowers are its biggest risk.

Granted, Ares managers take all necessary precautions. They practice primarily first-lien lending on a secured basis. They know their verticals well. They demand high interest. They control documentation and impose rigorous covenants. And finally, they do not expose Ares's balance sheet (beyond what is legally required) but lend other people's money. All of the above mitigates risks significantly and it is quite instructional to trace the investment record based on public filings.

Ares is not the only ticker associated with the company. SA readers are much better familiar with Ares Capital Corporation ( ARCC ). Articles devoted to this ticker appear on SA almost every week (for comparison, the last article on Ares Management was published in March). ARCC is managed externally by Ares in return for paying management and performance fees.

ARCC is the biggest and, perhaps, the most successful BDC of all. Many retail investors hold it due to its high and growing yield. Here is a slide from its recent presentation :

ARCC

The top row of the slide lists the achievements. First, the yield is very high at 10.4%. Secondly, its average annual return is 12% and is beating the index. Thirdly, it has been increasing quarterly dividends for 13 years in a row.

Still, Ares Management is not in a hurry to invest its capital materially in ARCC aligning itself with investors (other alt managers specializing in low-grade debt such as Oaktree or Blue Owl are doing the same). All of them prefer stable management fees to the charms of lending to shaky companies.

On the contrary: the only alt manager specializing in high-grade credit - Apollo - invests in its products on a grand scale.

I think it proves two things. The management expects Ares to generate higher returns than ARCC and is fully aware that in a low-grade debt business, one bad year can wipe out ten good years.

{kind=link}

SA

This picture represents the long-term ARCC performance. During the Financial Crisis, the stock tanked from ~$20 to ~$3.50. It reached $20 again only in 2021.

{kind=link}

SA

This slide shows the ARCC's dividend history. Before the Financial Crisis, the dividend was $0.42. It dropped and did not recover to the same level until 2022.

As we know, everything worked fine in the end. But it shows how an unfavorable macro environment can punish low-grade lenders.

Ares was not public during the Financial Crisis. And it should have performed better than ARCC at least in terms of recovering. Still, the story provides some warnings.

This is the reason why I have invested in neither Ares nor ARCC. My logic works this way:

- Ares is a better investment than ARCC, so I should not even consider ARCC (I am primarily a total return rather than an income investor).

- Both Apollo and Ares thrive on fees on credit investments but Apollo is dealing primarily with safe high-grade debt and is less risky. So, I'd rather invest in Apollo.

This two-step reasoning is an oversimplification but you should get the idea.

Conclusion

So far, I have been wrong in ignoring Ares. The main allure is high growth coupled with a decent and growing dividend. The valuation is high in absolute terms but similar to other alt managers. The macro environment is very favorable due to high demand and a limited supply of credit.

The dividend bump of around 20% in 2024 is very probable as the company will be converting the already existing AUM into FGAUM increasing the management fees. Normally, the stock follows the dividend.

The company is likely to continue its growth beyond 2024 following the same recipe. Similar to other alt managers, Ares is planning to double its distributable earnings in 5 years but in Ares's case, this forecast seems rather modest.

Ares's main risks are related to long and severe recessions similar to the Financial Crisis when many companies fail and are not able to repay debt. Even under this grim scenario, a lot will be saved as most of FGAUM represent secured first-lien lending. Since Ares is practically not invested in the low-grade debt it promotes, its balance sheet will not suffer. However, its revenue will, at least on a temporary basis.

Everybody who is considering investing in Ares should balance these long-term risks with alluring growth and good income in the "business as usual" conditions. Even if the latter holds, Ares investors should be also prepared for a bumpy ride similar to or even exceeding the situation with other alt managers.

For further details see:

Ares Management: Amazing Returns Of The Past Are Likely To Persist In The Near Future