PSP - Ares Management: Outperforming AUM With Plenty Of Dry Powder

2023-11-01 23:19:06 ET

Summary

- Ares Management Corporation's stock price has increased by over 50% in 2023 its peer group of alternative investment managers.

- The company's latest quarterly results show continued growth in assets under management with solid fee income momentum.

- Ares has a large balance of available capital for deployment, representing a runway for further earnings momentum.

Ares Management Corporation ( ARES ) has emerged as an exception among major asset managers and publicly listed alternative investors with its stock price up more than 50% in 2023. While much of the industry is being challenged by interest rates at a two-decade-high, the company's latest quarterly results were highlighted by continued growth in assets under management and strong fee income.

The attraction here is the diversified global platform which has proven to be resilient in a shifting macro backdrop and well-positioned to capture discounted private credit opportunities in the next stage of the cycle.

The company's large balance of available capital for deployment represents a significant growth runway. We like ARES as a leader and see room for shares to climb higher going forward.

ARES Q3 Earnings Recap

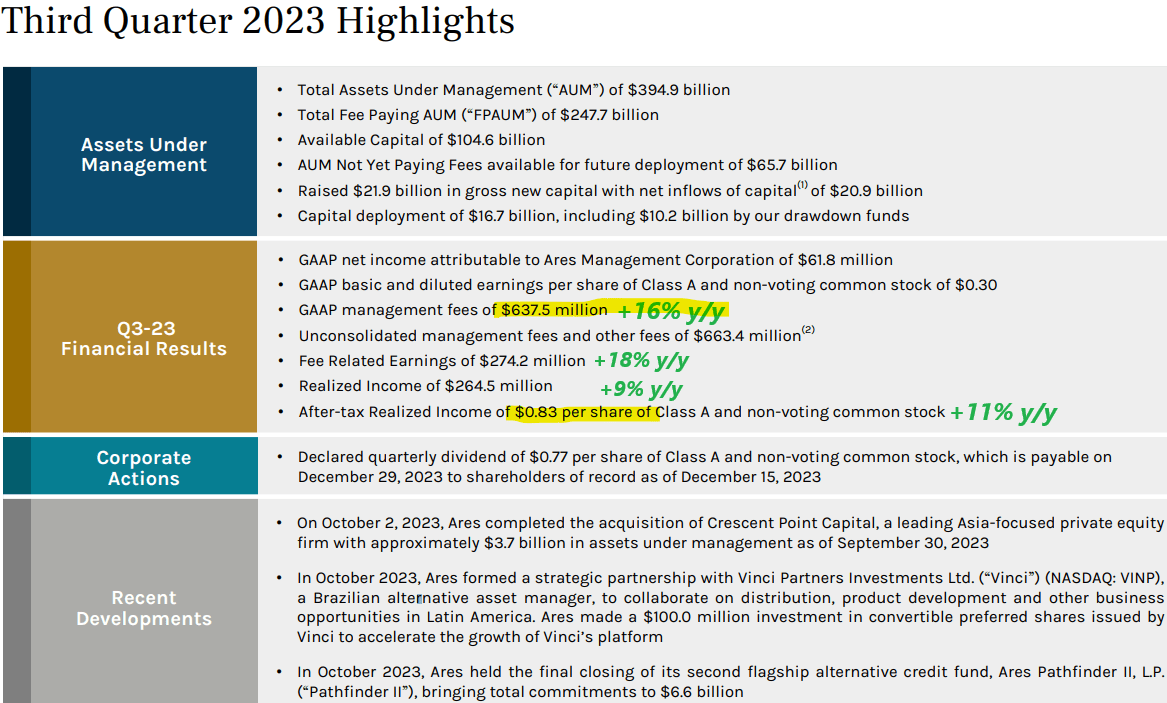

ARES reported Q3 EPS of $0.83 , up 11% year over year from $0.75 in Q3 2022. At the operational level, management fees of $637.5 million increased by 16% year over year. Fee-related earnings are up by 18% y/y with realized income was also higher.

Consistent with the market volatility against what was still some post-pandemic momentum last year, the carried interest allocation turned negative on the total revenue side, although this was balanced by sharply lower performance compensation-related expenses.

Net income of $62 million this quarter, reversed a loss of -$35 million continuing a trend of firming profitability in the first nine months of the year.

{kind=link}

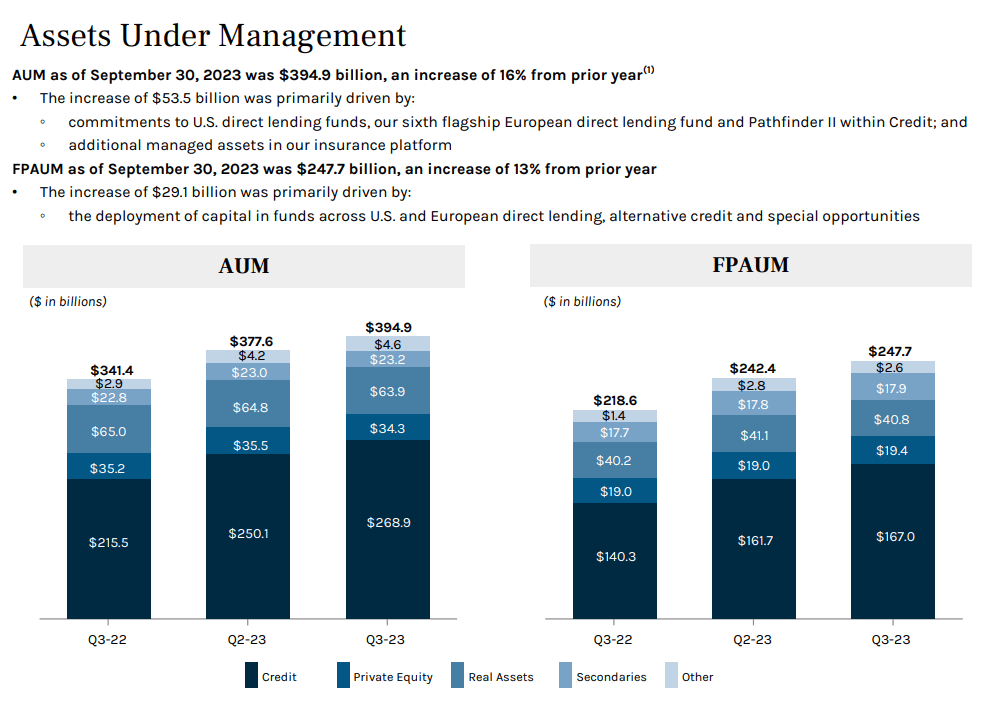

The big picture here considers the climbing assets under management, reaching $395 billion in Q3, up 16% y/y. Within that amount, the level of fee-paying AUM at $248 million was also higher through the deployment of $29 billion in capital into various funds.

A theme for the company has been an ongoing expansion internationally including in Europe, Asia-Pacific, and even Latin America highlighting the group's global ambition. Private credit is the group's strong point, but private equity deals, real estate, and secondaries are also part of the strategy.

Keep in mind that the figures here consolidate the results from the subsidiary Ares Capital ( ARCC ) structured as a business development company ((BDC)) that focuses on debt financing and middle-market transactions.

{kind=link}

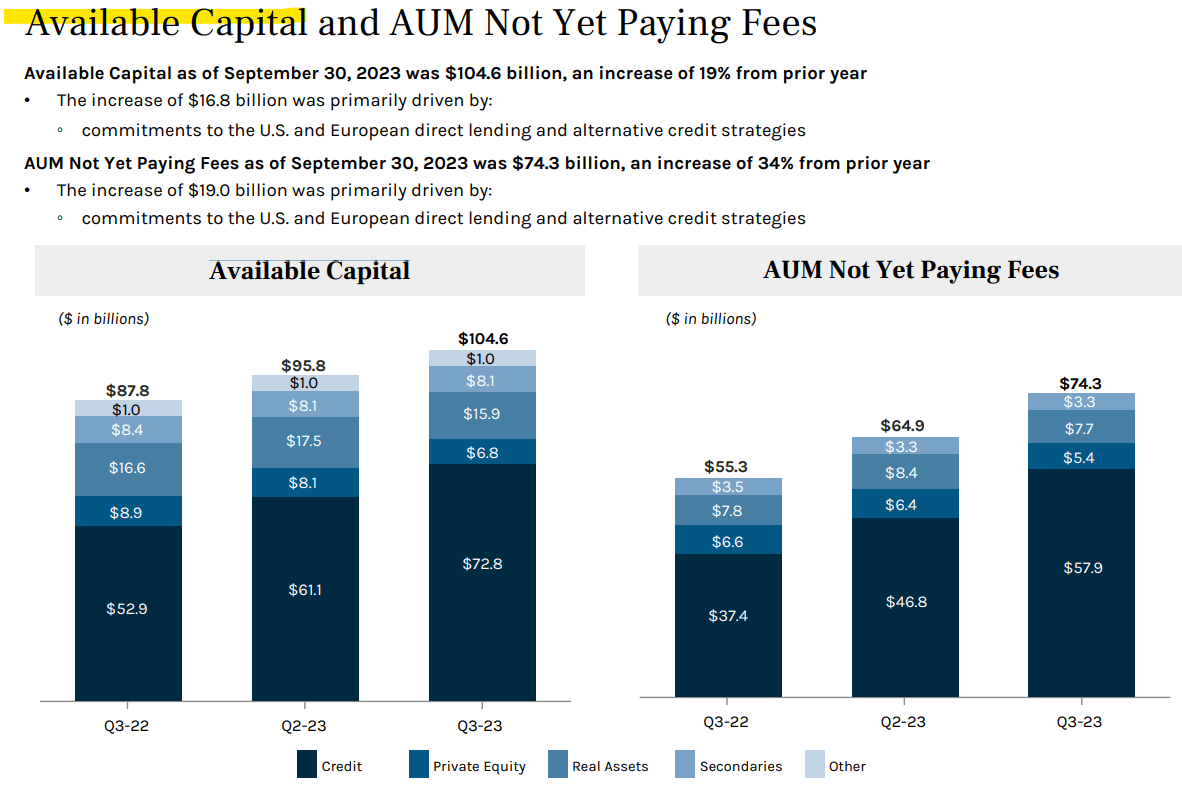

The metric that stands out to us is the level of available capital, also known as "dry powder". This amount of $105 billion, up 19% y/y, represents uncalled committed capital and undrawn amounts that are available to be invested consistent with market opportunities as per the fund managers. Within that figure, $74.3 billion of the AUM is not yet paying fees.

This is important as it provides some visibility for upwards of $648 million in potential incremental annual management fees and income down the line across the various funds and investment vehicles. While that figure is not "guaranteed", our interpretation of the trend is that investors are trusting Ares more as a sign of confidence in the platform.

The comments from CEO Michael Arougheti projected confidence in the outlook through 2024. From the earnings conference call:

Our quarterly results continue to demonstrate our strong growth and resiliency in these slower and more challenging market environments. We raised $21.9 billion in new commitments in the quarter, our second highest fundraising quarter in the history of our firm, and we've now raised $53.4 billion through the end of the third quarter.

We continue to benefit from our existing institutional investors who re-up or cross over into new Ares Fund products, along with new investors who recognize our consistent fund performance and leadership in managing private assets.

{kind=link}

What's Next For ARES?

To explain the relative strength of ARES this year, the understanding is that this side of private credit has benefited from the otherwise resilient economy. This is in contrast to fears at the end of 2022 of a looming recession that simply didn't materialize.

A scenario of widespread corporate defaults or a blowout in credit spreads would be more concerning, but simply not on the horizon at this point. Funding is being made at higher rates, and corporate borrowers continue servicing that debt which is a positive in underlying strategy. This is a view confirmed by Areas during the earnings conference call:

In credit, all of our primary investment strategies have generated double-digit gross returns in the last 12 months as we continue to benefit from higher base rates, attractive spreads, low defaults and strong fundamental performance. Our credit metrics remain strong across our portfolios.

Compared to alternative investment managers, Ares' exposure to the weaker and more volatile segments like private equity and even real estate has been limited as a smaller component of its overall strategy.

The advantage right now for Ares within credit is to take these higher yield opportunities with room for credit spreads to potentially tighten in a scenario where the macro outlook improves.

Beyond the market performance and macro uncertainty, the name of the game for ARES is the continued trend of climbing assets under management and the underlying demand for private credit. Data suggests alternative investments are outperforming the broader industry with investors generally under allocated to the types of strategies ARES specializes in.

From $7.7 trillion under management across the entire industry in 2021, the expectation is for the segment to nearly double with growth averaging 10% per year through 2027 . Within that amount, private wealth management funneling individual capital into alternative investments is set to accelerate over the next decade.

{kind=link}

For ARES, the results in 2023 already demonstrate that advantage compared to asset managers focusing on more segments like traditional fixed income and equities. Going forward, growth drivers include the expansion into new financial products, new channels including insurance and wealth management, as well as entering new international markets.

Another dynamic on the table for ARES is the growing investor base, from pensions as an important historical segment to other groups like banks, endowments, and even sovereign wealth funds. The experience has been that these types of clients typically start with one fund and ultimately expand the ARES relationship with multiple products.

{kind=link}

Overall, the outlook here is for continued growth supported by the expanding AUM and dry powder tailwind. This is reflected in the consensus forecasts for revenues and EPS to accelerate into 2024, where private equity and real estate could provide a more positive contribution to the overall results.

{kind=link}

In terms of valuations, we note that ARES trading at a price-to-book value of 11x and a 1-year forward P/E of 20x is at a premium to industry peers, although we believe this spread is justified given the company's underlying strengths. The bullish case here is that growth and earnings ultimately outperform expectations as the macro picture improves.

Final Thoughts

We are bullish on ARES as an industry benchmark. The current dividend yield of 3% is not the highest in the segment but adds to the allure of the stock's total return potential.

In terms of risks, it's clear that a deterioration of credit conditions and the global economy would undermine the earnings outlook. Sharply higher interest rates could introduce some financial market contagion and force a selloff in shares of ARES to a lower premium to its net asset value. Monitoring points here include credit spreads and the trends in AUM over the next few quarters.

For further details see:

Ares Management: Outperforming AUM With Plenty Of Dry Powder