ARES - Ares Management: Supercharged Growth In Private Markets

2023-06-20 03:57:39 ET

Summary

- Ares Management Corporation is a global alternative asset manager.

- AUM growth has been fantastic, propelling revenue growth at a CAGR of 23%.

- Our expectation is for this to continue, as further capital is allocated to private markets in the coming years. As this occurs, margins will also improve (Current EBITDA-M of 34%).

- Ares is trading at a rich valuation (30x LTM EBITDA) but we see this contracting rapidly as growth continues.

- Relative to peers, Ares is outperforming in growth and closing the gap in margins.

Investment thesis

Our current investment thesis is:

- Ares is a leading alternative asset manager which is a positive AUM growth trajectory, as strong returns encourage new client wins. We expect this to continue going forward despite market weaknesses.

- Margins have improved dramatically and we believe this will also continue, driven by scale economies.

- Ares has a rich valuation but we still believe there is value for investors. Growth with margins will contribute to a rapid contraction of its trading multiple.

Company description

Ares Management Corporation ( ARES ) is an alternative asset manager operating globally. The company has four main segments:

- Tradable Credit Group: This segment manages investment funds for institutional and retail investors in the tradable and non-investment grade corporate credit markets.

- Direct Lending Group: The company provides financing solutions to companies.

- Private Equity Group: This segment focuses on making majority or shared-control investments in under-capitalized companies.

- Real Estate Group: Ares invests in new developments and asset repositioning, primarily through control or majority-control investments. It also provides financing opportunities for middle-market owners and operators of commercial real estate.

Share price

Ares has performed extremely well in the last decade, significantly outperforming the market as a whole. This has been driven by a rapid expansion of the company's operations while improving profitability.

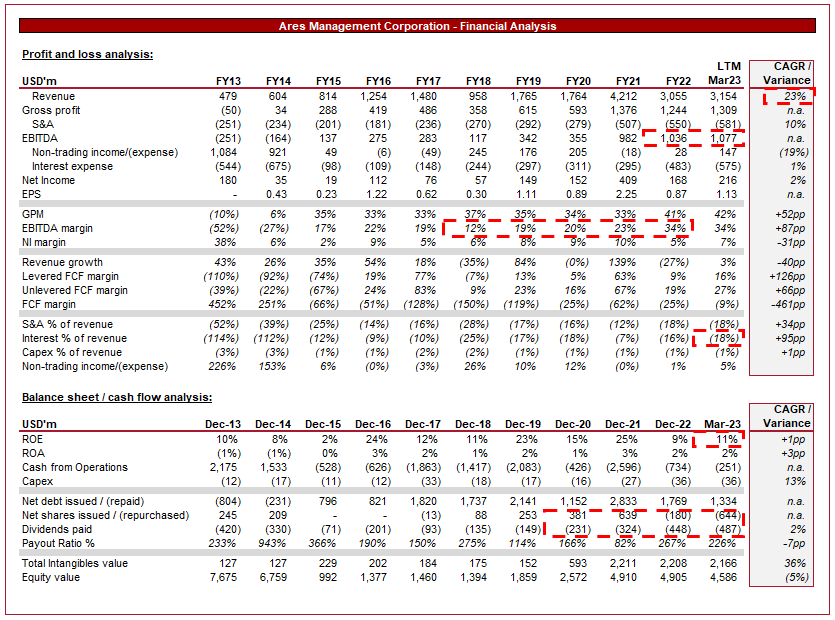

Financial analysis

Ares financial analysis (Tikr Terminal)

{kind=link}

Presented above is Ares's financial performance for the last decade.

Revenue & Commercial Factors

Ares has grown its revenue at an impressive rate of 23% across the last 10 years. During this period, the company has been on a consistent upward trajectory, with a revenue decline in only 2 periods.

This expansion is attributable to a rapid expansion of Ares' operations, with the firm raising new funds consistently and winning new clients.

Business model

Ares generates its revenue primarily through the levying of management fees. These are usually charged on assets under management or invested capital, representing the least volatile of Ares' revenue streams. Given this is based on the valuation of assets, this income stream is cyclical based on market performance, although is usually supplemented by net inflows.

In addition to this, Ares can earn fees based on outperformance (Incentive fees / carried interest allocation). These are usually the target for Management as they can be highly lucrative once the hurdle is reached.

Finally, Ares generates investment income from principal investments, as well as other transaction and administrative fees.

As of FY22, revenue is divided as follows (It is worth reiterating that this can easily fluctuate YoY).

Revenue split (Ares)

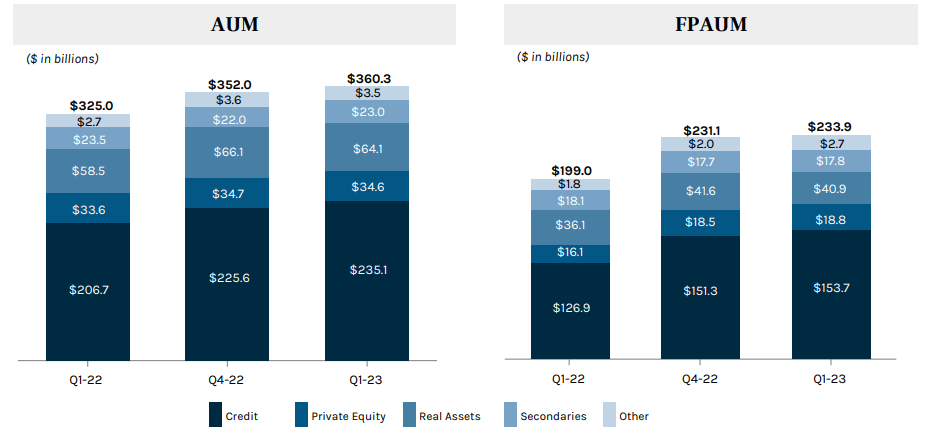

AUM

As of Q1'23, Ares has $360.3m in assets under management, of which £233.9m is fee-paying (65%). The majority of this capital is committed to Credit investments, which are Ares' specific area of expertise. This said, Ares is focused on expanding its other functions, creating greater diversification.

This is a critical development as the attractiveness of asset classes fluctuates over time based on economic conditions and key macro indicators. Following such an impressive growth trajectory, it is important to now develop the fundamental position of the business.

{kind=link}

Included within AUM is $51bn of AUM available for future deployment. This has the potential to generate c.$483bn in incremental annual management fees. This alone represents c.15% growth on the current revenue level. This illustrates why raising new finances, alongside growing the value of its committed assets, is critical.

The ability to continually raise capital is predicated on displaying an impressive track record relative to the other options in the market. Without conducting a repetitive exercise of discussing each fund, Ares' performance has been consistently strong across the various funds. These results can be found in the appendix of the quarterly reports .

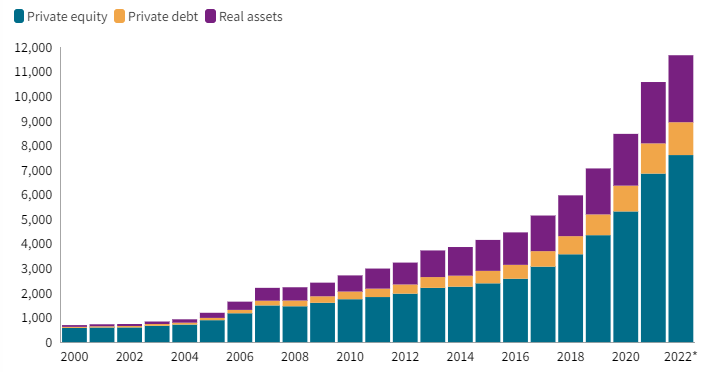

Alternative asset industry

The asset management industry is witnessing a rising demand for alternative investments such as private equity, real estate, infrastructure, and credit strategies. This has been driven in large part by a decade of expansionary monetary policy, with investors seeking improved returns and diversification beyond the traditional asset classes.

As the following graph illustrates, the industry has been on an upward trajectory since 2000, but this only really accelerated post-GFC. Our expectation is for this to continue in the coming years, as the quality of private assets continues to represent value relative to public assets. It should be noted that this is a positive reinforcing cycle, as if funding options are improved in the private market, higher-quality businesses will not be forced into entering the private market.

Private market growth (S&P Global)

{kind=link}

Within this segment, there appears to be a growing interest in private credit assets. This is driven by the relative lack of options for many mid-market businesses, with Banks de-risking post-GFC. With an extended period of low-interest rates, investors are looking for exposure to interest income at an attractive risk-adjusted return. Private credit looks to be satisfying this interest. Ares' current growth trajectory is a reflection of this, as the firm has exploited the growth.

Current economic conditions are spooking investors, with elevated rates and heightened inflation implying to some that a recession will occur. Overarchingly, this has caused a bear market and uncertainty around consumer demand. We do not believe this will materially impact Ares in the medium term, primarily due to the level of "dry powder" in the private market. S&P estimates the private equity industry alone has $2tn . This will support a market resurgence as this capital is invested. This said, we could see soft conditions continue in the coming quarters until there is sufficient signaling that rates will decline.

Global expansion represents a primary opportunity for Ares from several perspectives. Firstly, with economic development in many developing nations, we are seeing a rise in the middle class and thus investors seeking exposure to global assets. This increases the potential client base for Ares. Secondly, with development in these regions, Ares has a greater market within which to acquire assets.

A key risk we see to the firm is issues in the real estate market. The Covid-19 pandemic has fundamentally changed both the residential and commercial markets, with consumers increasingly happy to work-from-home. This allows consumers to live further away from the office, reducing the demand for lucrative inner-city residentials. Further, with reduced office attendance, we are seeing lower demand for office space, as well as some smaller businesses becoming fully virtual.

According to CBRE and Morgan Stanley , commercial real estate could see valuations fall as much as 40%, contributing to a heighted risk of default as c.£1.5tn in debt comes due by the end of 2025.

Margins

Ares' margins have improved well over the last decade. The firm currently has an EBITDA-M of 34% and a NIM of 7%.

Margins have been volatile in the last decade, primarily due to the impact of achieving incentive fees (timing) and the rapid growth in the business. The marginal cost of delivering services to new clients is fairly low and so as AUM increases, so will margins.

The low NIM relative to EBITDA-M is due to income attributable to minority interest and preferred dividends.

It is difficult to assess where the "normalized" level for the firm is, following a period of rapid growth and subsequent slowdown. Our view is that margins could improve in the coming years by an additional 5-10%, as AUM growth continues and further funds are committed.

Balance sheet

Ares currently has c.$272m in cash and $2.4bn in debt obligations, of which $795m has been drawn against a facility of $1.3bn. This is a fairly aggressive approach by Ares but thus far has maximized its returns. We are not overly concerned by this given the consistent coverage of debt through the reliability of management fees, although we would like to see Ares reduce its leverage over time.

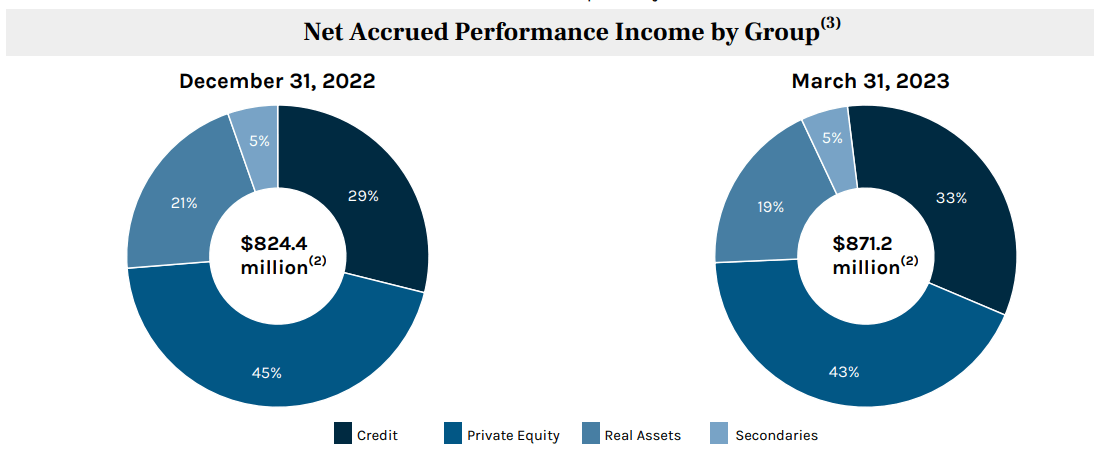

Further, there is c.$864m in corporate investments on the balance sheet, alongside accrued performance income of $871m.

Accrued investment income (Ares Management Corporation)

{kind=link}

During this period, distributions have come in the form of buybacks and dividends. There has been dilution but as the share price reflects, this has not been an issue for equity holders.

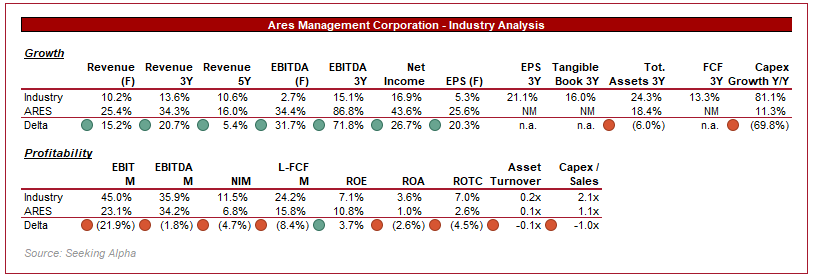

Industry analysis

Asset Management Industry (Seeking Alpha)

{kind=link}

Presented above is a comparison of Ares's growth and profitability to the average of its industry, as defined by Seeking Alpha ( 94 companies).

Ares' strong growth achieved is contextualized relative to its peer group, with the company far above the industry average.

Profitability is less standout, with Ares underperforming on the majority of metrics. This said, we acknowledge that the business is currently on an upward trajectory and so the expectation would be for an improvement (which we are forecasting). With an EBITDA-M and NIM deficit of c.2%/5%, we suspect Ares will rapidly close this gap in the coming years.

Valuation

Ares valuation (Tikr Terminal)

Ares is currently trading at 30.3x LTM EV/EBITDA and 19.7x NTM EV/EBITDA. Both multiples are slightly below the firm's historical average, likely reflecting a combination of bullish resilience and bearish market sentiment.

Our view is that this valuation is currently justified. From a commercial perspective, we remain bullish on the alternatives industry, expecting continued inward flows. With the rate at which Ares is raising AUM (and investing its uninvested capital), the business is already well progressed toward the 20x multiple. In conjunction with further margin improvement and revenue growth, we believe Ares' multiple will rapidly contract.

Key risks with our thesis

The risks to our current thesis are:

- Ares' ability to find quality assets within which to allocate capital as the firm scales in size.

- Increased competition in private markets for quality assets could contribute to a reduction in returns as the free market eats away at exceptional returns.

- Inability of Ares to materially improve margins without exceptional performance. Our thesis is predicated on a gradual margin uplift as AUM increases, rather than an expectation of incentive fee-led improvement.

Final thoughts

Ares has been a fantastic allocator of capital in the last decade. AUM growth has consistently been strong and allowed the business to expand its revenue. As funds have matured, returns have been accelerated by the impact of incentive fees, which we expect to continue.

Growth in the coming years will be driven by "business as usual", as private market growth continues, as well as expansion into new territories.

We believe margin improvement and continued growth will contribute to a contraction in the firm's trading multiple.

For further details see:

Ares Management: Supercharged Growth In Private Markets