AGX - Argan: Encouraging Near-Term Trends Point To Further Share Price Gains

2023-11-08 08:36:59 ET

Summary

- Argan's revenues grow by close to 20% in the second quarter.

- Gross margin tops 16% which was a sizable improvement over Q1.

- Income statement trends look encouraging with shareholders continuing to be rewarded through sustained buybacks and an increasing dividend.

Intro

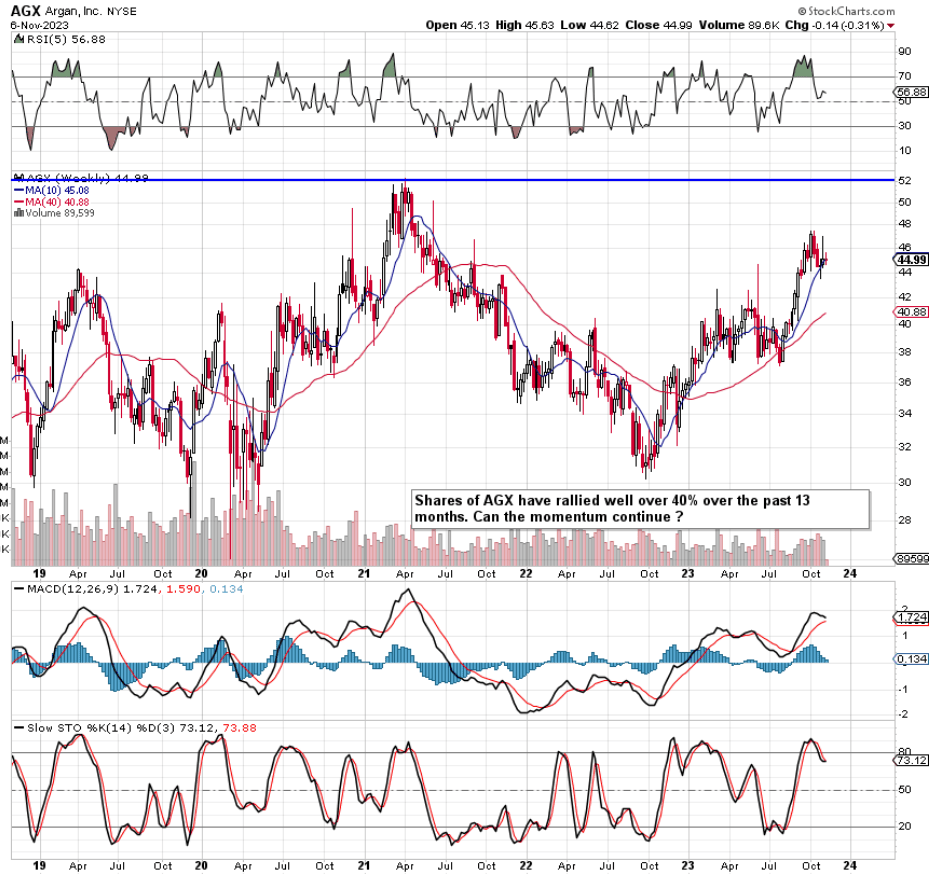

We wrote about Argan ( AGX ) in September of last year when we looked at the potential of the engineering & construction company from the long side just before the company announced its second-quarter numbers for fiscal 2023. It was noted at the time that the market continued not to reward the share price despite Argan's impressive backlog. In fact, due to how well management continued to deploy its cash, we predicted that shares (if the bearish trend continued) would bottom at long-term support around the $30 mark.

As we see below, this is precisely what happened with shares only going from strength to strength since that multi-year bottom in September of last year. In fact, given the strength of Argan's upward trend, there is every possibility that shares at least test their 2021 highs of close to $55 a share in this latest bullish run. Therefore, let's delve into Argan's most recent quarterly report ( Q2 in fiscal 2024) and specifically the company's income statement to see if the firepower is there to keep on pricing shares higher. Remember, share-price appreciation is principally driven by earnings growth so strong momentum will be a prerequisite here to keep shares rallying higher.

Argan Technical Chart (Stockcharts.com)

{kind=link}

Q2 Sales Growth

Sales of $141.3 million in Q2 was a significant rise (19.6%) over the same period of 12 months prior. Both of the company's segments reported strong underlying growth (Power Industry Services and Industrial Construction Services) driven by the likes of construction overseas in Power & field services in Industrial. Revenue growth is the heartbeat of any company in that sustained earnings growth rarely takes place without it. Suffice it to say, given that AGX's revenue growth has come in more or less flat ( no growth) over the past five years, it is heartening to see the 30%+ ($592.3 million) expected top-line growth rate for fiscal 2024.

Gross Margin

Gross profit of $23.7 million off a top-line number of $141.3 million resulted in a gross margin of 16.8% in the quarter. Although Argan saw a rolling year decline in its gross margin number, the 16.8% number in Q2 still came in higher than

- Q1 (13.7%)

- The company's trailing 12-month average (16.15%)

- The company's 5-year average (13.3%).

Therefore, all things being equal, we still have bullish trends here when one takes a 'global' view of where the stock's gross margin is trending. Investors should NOT look at specific quarters (when analyzing gross margin) in Argan as its trends can be very lumpy due to revenue mix, commercial terms, etc., and where the respective project is in its current life cycle.

Operating Costs

A solid gross profit trend along with rising sales many times can mask other costs further down the income statement. SG&A costs for example (which entail the likes of AGX's staff & headquarters expenses) came in at $10.5 million at the end of Q2 in the present fiscal year. This was an excellent number in our view as it was lower than the corresponding $11 million figure in Q2-2023 despite the much higher revenue number. We do not like seeing rising SG&A costs (when related to sales) and this is not what we have in AGX.

SG&A costs made up 7.4% of the top-line number in Q2 whereas the comparable trailing 12-month average breakdown comes in at 8.7%. This trend demonstrates prudence by management (regarding controlling costs) meaning rising sales should continue to positively impact the company's earnings (and share price) over time.

Valuation

Operating income came in at $13.2 million in the second quarter which means EBIT for the past four quarters totals $36 million. Although AGX's net profit ($36.3 million) exceeded EBIT over this timeframe, we prefer to concentrate on operating profit (when valuing a stock) as it takes any interest expense, depreciation, or taxes out of the equation. One of the reasons why we saw elevated net profit in Q2 was due to lower tax expenses in the quarter. Suffice it to say, zoning in on operating profit trends is how a buyer for example would size up Argan's worth at present as it eliminates the ramifications of debt & taxes from the profit equation.

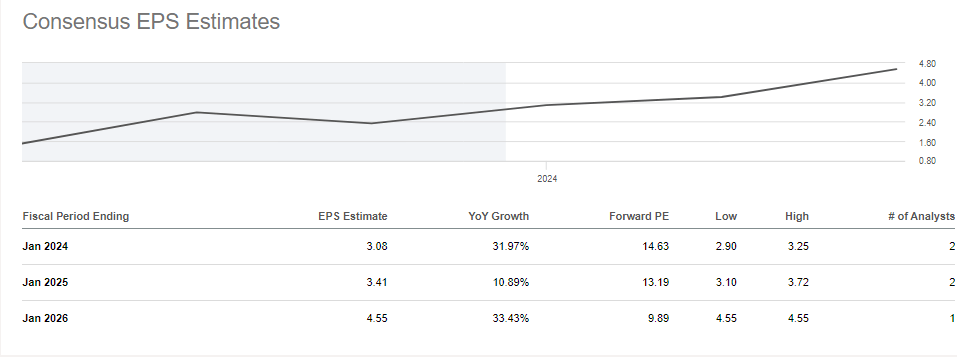

When we divide Argan's 'Enterprise Value' by its trailing 'Ebit', we get an EV/EBIT multiple of 7.71. This multiple looks very attractive when compared to the sector median (15.49) as well as Argan's 5-year multiple (17.72). Furthermore, when we see what consensus is projecting for Argan in terms of forward-looking EPS growth, it becomes evident that Argan's earnings are cheap and are also on a strong growth curve. The above trends ring true due to how sizable projects such as the Irish 'Shannonbridge power plant' & 'Vistra Solar project in the US have come onto the company's books. Moreover, a strong component of the EPS growth rates we see below is how management has been buying back shares aggressively in recent times. Over 2.6 million (16%) of shares have been bought back by the company over the past two years which again demonstrates how the company's interests remain aligned with its shareholders.

Argan Consensus EPS Estimates (Seeking Alpha)

{kind=link}

Strong Forward-Looking Earnings Potential

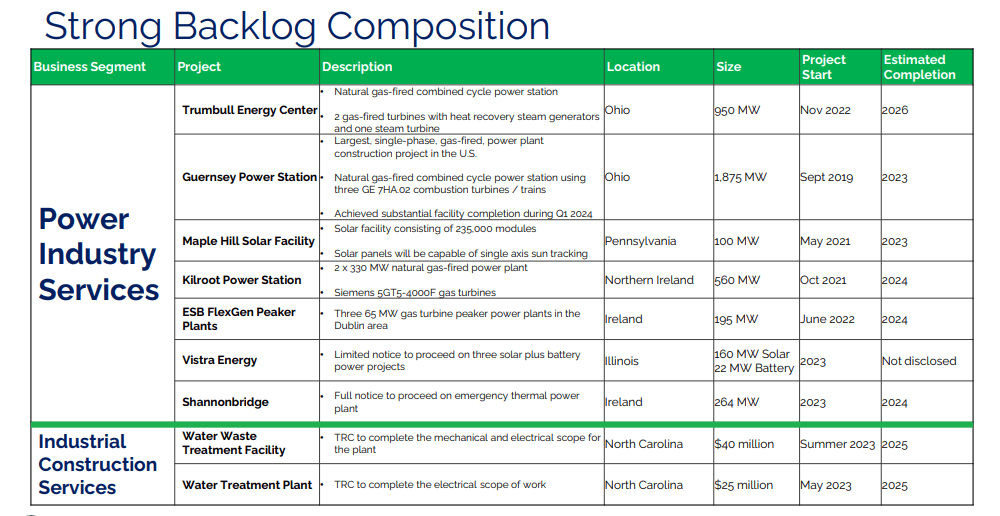

As we see below in Argan's backlog breakdown, both the Guernsey Power Station & Maple Hill Solar projects are due to end this year. However, both of the water treatment plant projects as well as the Shannonbridge power plant in Ireland & the Vistra solar project in Illinois have already started, driving Argan's earnings forward over the forthcoming years. Concerning the near term, the 'Trumbull Energy Centre' in Illinois continues its ramp and is not expected to hit peak quarterly revenue for another 12 months at least. Therefore, given the fact that demand for natural gas power plants, as well as renewable energy, will only grow over the upcoming decades, we believe Argan's backlog will continue to go from strength to strength.

Considering the above which ties into what consensus is predicting concerning forward-looking EPS growth, we do not see any risk to the 2.7% dividend yield which is currently being paid out to shareholders. Management recently raised the quarterly payout to $0.30 per share which was a 20% hike over the previous amount. The increase looks well affordable due to Argan's low cash dividend payout ratio of just over 23%.

{kind=link}

Risk

The principal risk going forward concerning the share price is whether the backlog can be completed in a timely fashion. Although margin trend as alluded to earlier looks promising at present, sizable projects can always run into expected delays at the worst times. The Kilroot project for example in Northern Ireland reported some significant cost overruns due to a myriad of factors. Suffice it to say, given that Argan's trailing gross margins come in at 16%+, stage-phased work must be completed in a timely order to ensure EBIT margins remain elevated . Any deviation from the above will result in the technicals letting investors know swiftly about the company's forward-looking fundamentals growth path.

Conclusion

To sum up, Argan's income statement and associated trends for its second quarter this year point to further growth for the engineering & construction company. 20% sales growth due to growth in both of its segments led to strong earnings growth and a total of 77k shares being bought back in the quarter. Gross margin improved sequentially and SG&A costs came in lower as a percentage of top-line revenues. Suffice it to say, as alluded to earlier, we believe AGX shares can run to approximately the $55 level (2021 highs) in this latest move based on current trends. We look forward to continued coverage.

For further details see:

Argan: Encouraging Near-Term Trends Point To Further Share Price Gains