AGX - Argan Stock: Recalibrating Expectations

2023-08-23 11:15:23 ET

Summary

- Argan, an energy infrastructure company, has been upgraded from a 'hold' to a soft 'buy' due to its strong balance sheet and long-term outlook for energy needs.

- This is in spite of volatile results, including weakening sales last year.

- Shares of Argan are attractively priced compared to similar firms, and the company's significant cash balance makes it an appealing investment.

Even the best investors in the world make a mistake from time to time. I definitely make more mistakes than I would care to admit. But when we do make mistakes, the important thing is to learn from them. Only by learning from our mistakes can we prevent them from occurring again in the future. One example of a company that I feel I misjudged was a firm called Argan ( AGX ). In its simplest sense, the company can be described as an energy infrastructure business. Most of its revenue is centered around engineering, procurement, and construction services dedicated to designing, building, and commissioning large-scale energy projects. That accounts for about 75% of the company's revenue. However, 22% comes from industrial field services and fabrication services, while the remaining 3% is attributable to telecommunications infrastructure services.

One of the reasons why, in the past, I was cautious about the company was because of mixed financial performance. Revenue, profits, and cash flows have been all over the map. Interestingly, that picture has not changed. However, when you look at the company's fortress balance sheet and focus on the long-term outlook for energy needs, the business does start to become far more appealing. And it's because of these reasons, combined with how cheap shares are, that I have decided to upgrade the business from a 'hold' to a soft 'buy'.

Reassessing the picture

My, how time flies! It seems like not long ago that I last wrote about Argan. However, looking back, my last article about the company was published at the end of November 2022. We are approaching the 10-month mark sunset time. Back then, I kept the company rated a 'hold' because of declining sales and profits on a year-over-year basis. Even back then, I recognized that the firm benefited from significant amounts of cash on hand and the absence of debt. But that was not enough, even after seeing how cheap shares were, to cause me to turn bullish on the firm. Since then, shares of the company have outperformed the market slightly, rising 12.2% compared to the 9.8% the S&P 500 experienced. That is certainly enough for me to say that my prior call on the company was overly pessimistic.

{kind=link}

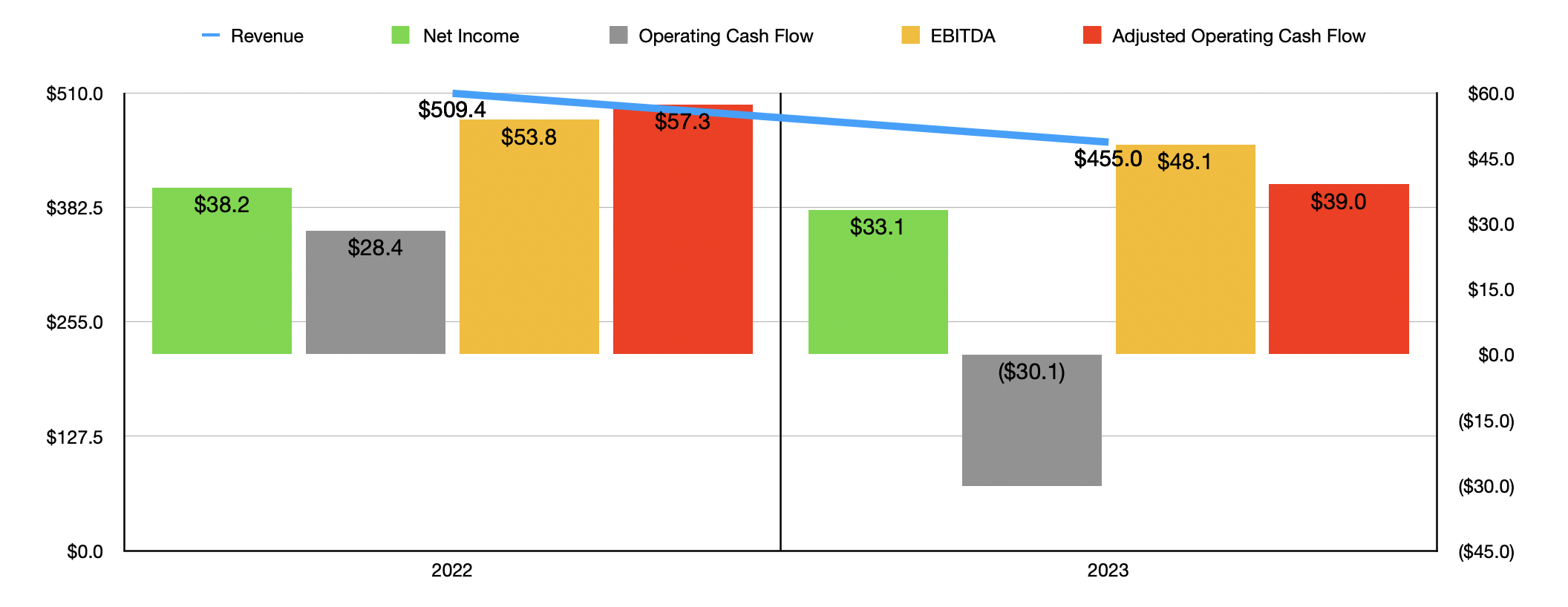

This is not to say that the financial picture of the business has gotten much better. It really hasn't. In the chart above, for instance, you can see the financial performance of the firm for its 2023 fiscal year compared to its 2022 fiscal year. Revenue for the company came in at $455 million. That's 10.7% lower than the $509.4 million management reported one year earlier. Most of the pain for the company came from its Power Industry Services segment, with revenue tanking $52.1 million year over year. This drop in revenue is driven by the falling off of activity at the company's Guernsey Power State and its Maple Hill Solar Facilities that it has been working on. In 2022, construction activity was at its peak for these operations. That was not the case in 2023. Having looked at other companies engaged in the construction space before, I can tell you that lumpy revenue caused by some projects being finished, delays in other projects, and new projects gearing up is just the way things are. So, this is not surprising to me one bit.

{kind=link}

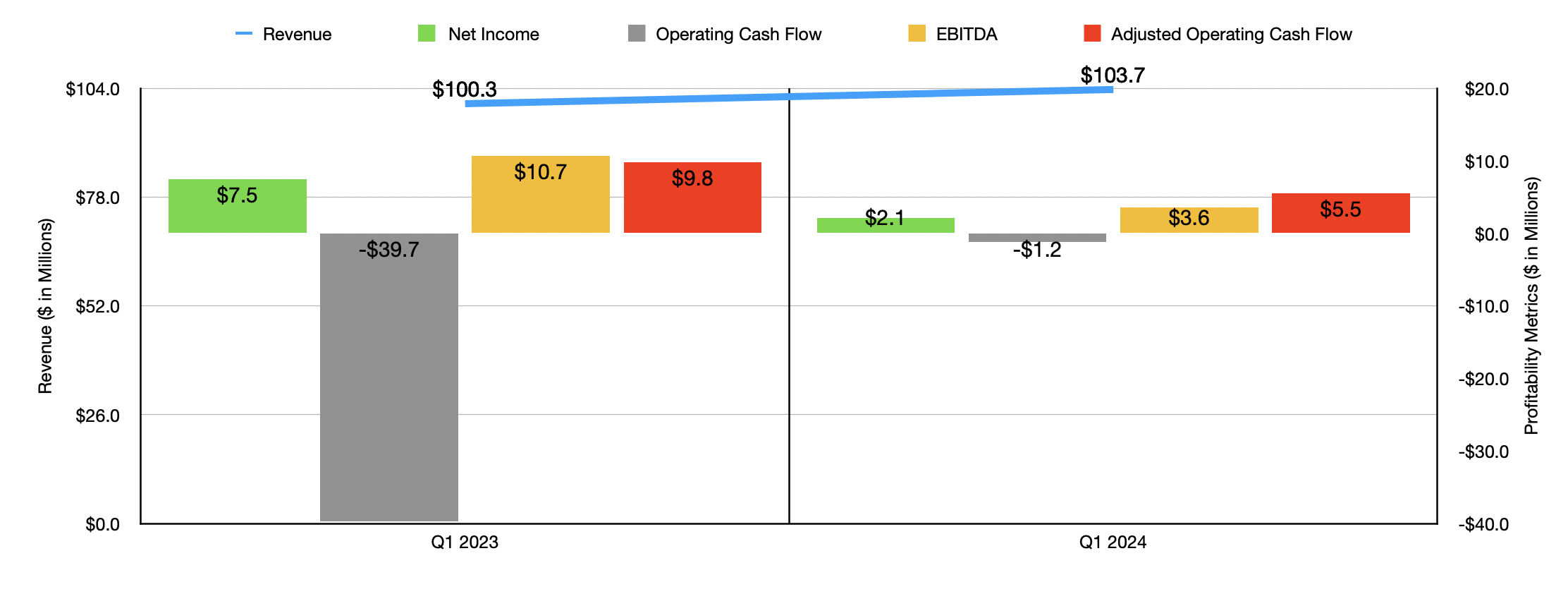

On the bottom line, the picture has also been rather volatile. The company went from generating a net profit of $38.2 million in 2022 to $33.1 million in 2023. Other profitability metrics for the business also worsened. For instance, operating cash flow went from $28.4 million to negative $30.1 million. Even if we adjust for changes in working capital, cash flow went from $57.3 million to $39 million. And lastly, EBITDA for the enterprise fell from $53.8 million to $48.1 million. As you can see in the chart above, volatile financial results continued into the first quarter of 2024 compared to the same time of 2023. Revenue increased, but all of the company's profitability metrics, except for operating cash flow, worsened year over year.

{kind=link}

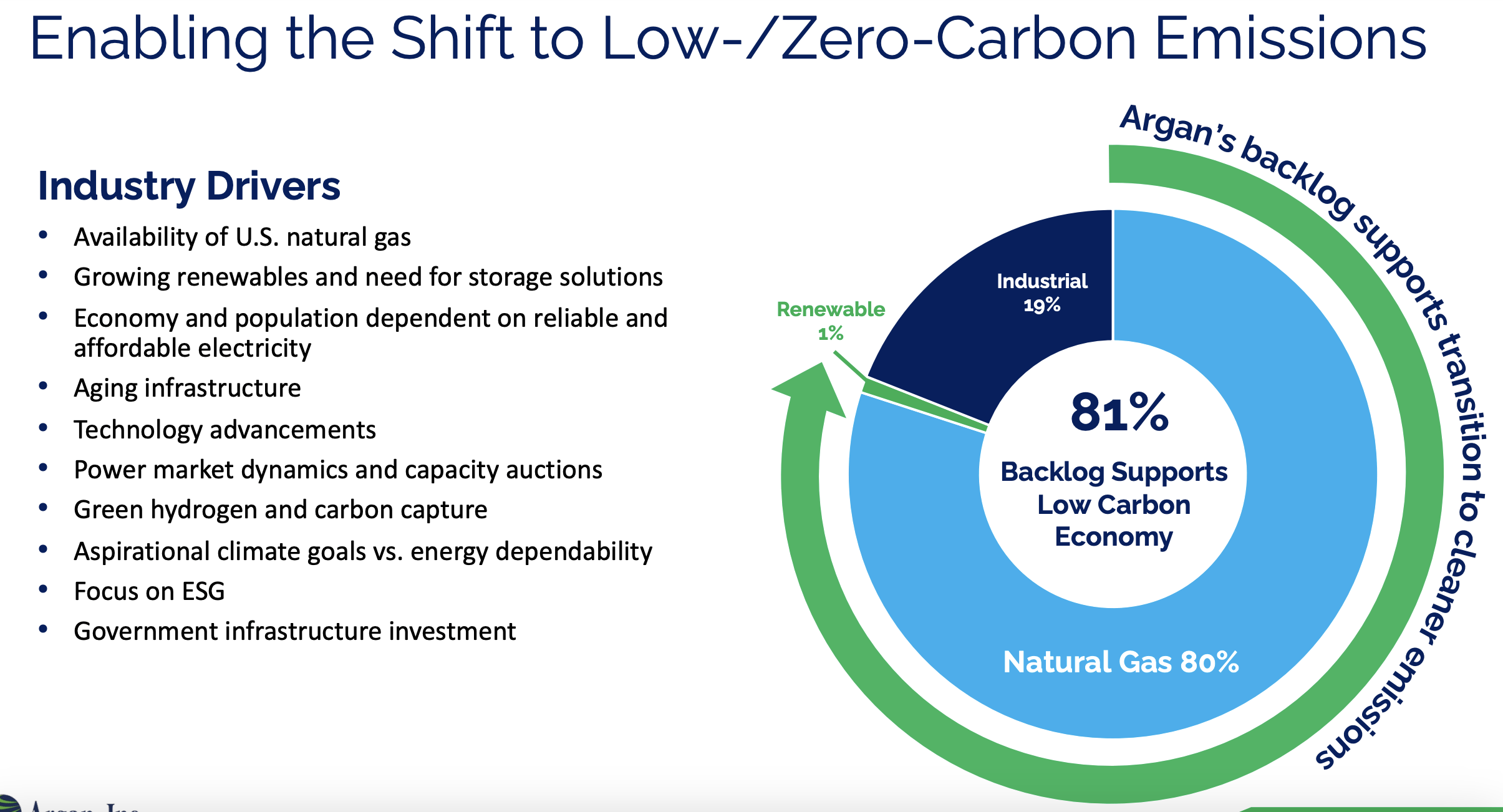

Even though I would like to see more consistency than what we are seeing, there are things about the company that make it more appealing to me. For starters, backlog for the business remains robust. At the end of the most recent quarter, it totaled $806 million. That is lower than the $822 million reported one quarter earlier. However, it still represents almost two years' worth of revenue. To make things even better, 80% of the company's backlog is associated with natural gas projects, with renewable energy projects adding another 1% to the picture. While I would ideally like to see a lot more on the renewable side of things, particularly when you consider that most new energy capacity is now being done in the form of renewable projects, natural gas is not an awful way to go.

{kind=link}

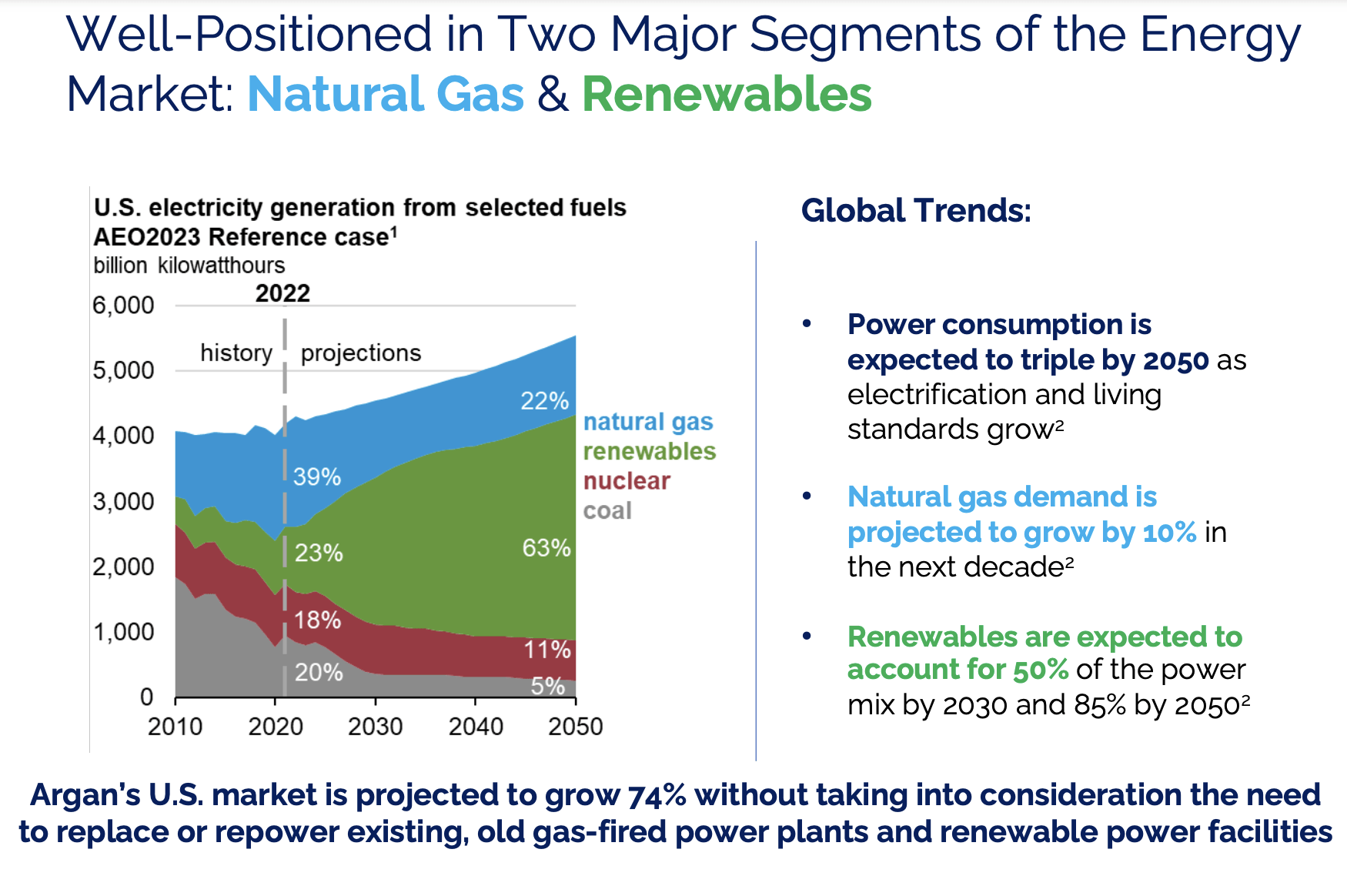

Management paints the gas heavy backlog as serving an important role as a transition on our way to a cleaner economy. Even without factoring in the fact that renewable projects are going to become more important over the next several years, it's also believed that, over the next decade, aggregate natural gas consumption will grow by about 10%. Between 2022 and 2050, overall power consumption in the US is expected to approximately triple. Renewables are forecasted to account for about 50% of the power mixed by 2030, before eventually growing to 85% by 2050. So, it is important to point out that any long-term investor who does invest in the company should do so with the goal in mind that the renewable project backlog needs to start growing and at a rather significant pace.

{kind=link}

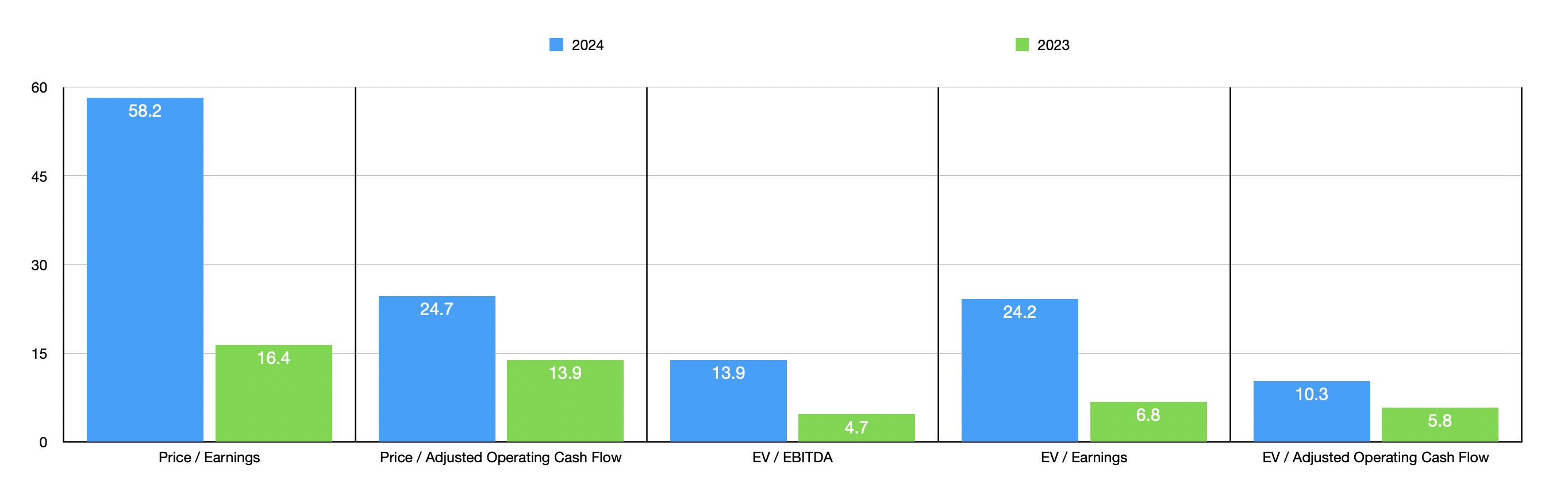

When it comes to pricing the company, the picture is rather difficult. This is true in part because of the aforementioned volatility. But it's also true because of the company's unique balance sheet. The firm has no debt on its books, and it enjoys $316.9 million in cash and cash equivalents. Compared to its small market capitalization of $541.7 million, this is a tremendous amount of cash. You can see this reflected in the chart above with how shares are priced. Annualizing results experienced for the first quarter of 2024 compared to the same time last year, I got net income of $9.3 million, adjusted operating cash flow of $21.9 million, and EBITDA totaling $16.2 million. As you can see, on a price to earnings or price to cash flow basis, shares of the company do look very expensive. But it might not be such a great idea to value the company based on results from a single quarter and with no significant guidance from management. Instead, relying on the 2023 data, shares look much more reasonably priced.

Where the picture changes from being reasonably priced to being very attractive is when you look at the EV to EBITDA multiple of 4.7. This is due to the fact that the significant cash balance on the company's books brings the enterprise value of the firm down to $224.7 million. If we were to compare the net profits and the adjusted operating cash flow of the company to the enterprise value instead of its market capitalization, for instance, we would get multiples of 6.8 and 5.8, respectively, for 2023. That looks much more appealing on an absolute basis. But even if we don't do this, relative to similar firms, shares of the company look to be a bit on the cheap side. In the table below, I compared the firm with five similar enterprises. On a price to earnings basis, only one of the five businesses was cheaper than it. This number increases to two firms on a price to operating cash flow basis. Meanwhile, when it comes to the EV to EBITDA approach, our candidate was the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Argan |

| 16.4 |

| 13.9 |

| 4.7 |

| Great Lakes Dredge & Dock ( GLDD ) |

| 18.0 |

| 16.4 |

| 228.5 |

| Concrete Pumping Holdings ( BBCP ) |

| 13.7 |

| 4.9 |

| 6.8 |

| Tutor Perini ( TPC ) |

| N/A |

| 4.1 |

| 30.3 |

| Bowman Consulting Group ( BWMN ) |

| 113.1 |

| 54.8 |

| 27.5 |

| Construction Partners ( ROAD ) |

| 57.2 |

| 14.6 |

| 16.4 |

Takeaway

From all the data that's in front of me, I do believe that it's appropriate for me to say my prior assessment of the company was overly bearish. Shares look attractively priced when you look at them through the right lens. The balance sheet of the business is robust, and it has a significant amount of backlog to benefit from. I am a bit worried that so little of the backlog is for renewable projects. If this picture persists over the next couple of years, I will become increasingly worried. But for now, that's not enough to offset the positives that I'm looking at. Given all of these factors together, I have decided to upgrade the company slightly from a 'hold' to a soft 'buy'.

For further details see:

Argan Stock: Recalibrating Expectations