RIO - Argentina Lithium: $90 Million Investment From Stellantis Implies A Substantial Upward Rerate

2023-10-11 19:52:40 ET

Summary

- Stellantis recently paid $90 million for a ~20% stake in Argentina Lithium & Energy Corp. It includes a 7-year offtake agreement.

- The valuation of the deal implies $2.30 CAD per share, however there are some obstacles to realizing the full value of it right away.

- LIT will have $0.68 per share in cash upon exercise of all warrants and options; this should be a reasonable floor for the stock going forward.

- The deal has significant positive implications for other junior explorers in the lithium triangle in Argentina.

Argentina Lithium & Energy Corp. ( PNXLF )( LIT:CA ) has been a trending stock in Canada since the afternoon of September 27th when it announced a $90 million USD-equivalent investment made by Stellantis N.V. ( STLA ). Stellantis will acquire a 19.9% stake into LIT's subsidiary Argentina Litio y Energia but has the option to exchange that for a 19.9% stake into LIT itself. The deal includes a 7-year, annual 15,000 tonne lithium offtake agreement starting in 2028. Considering that LIT had a $30 million CAD market cap on the day prior to the deal being announced, interest in the stock has understandably increased. The stock price more than doubled immediately after the announcement, but settled around $0.40 in the days that followed as the market felt that it was too good to be true. It has since regained life and ended at $0.55 on Tuesday upon the announcement of the deal being closed last week.

Despite the move up, I believe that LIT still has an upside potential of over 100% as a $0.55 stock price implies a $72 million CAD market cap, less than the money being received in the deal. Not only does LIT require a substantial upward re-rate, I believe that this deal is an absolute game-changer for all junior lithium plays in the region.

How did LIT pull off this deal?

Canadian junior market traders have witnessed a long history of claims from microcap resource explorers getting deals with larger companies that were either faked or greatly overstated. So there was understandably some nervousness or skepticism about this deal. Once it closed and documentation on SEDAR (the Canadian equivalent to SEC.gov) filed, there was no longer any issue about the deal being fake. What remains are two other criticisms:

1. Stellantis overpaid for LIT and could have just bought it out for that level of investment.

2. Stellantis overpaid for LIT relative to other lithium players in Argentina.

Had Stellantis just offered $90 million in a takeover offer, it likely would have succeeded in a buyout attempt based on the stock price prior to the deal being announced. However, Stellantis isn't interested in making an investment in a lithium company the same way private investors would, nor is it interested in operating a mine itself. Its interest in LIT is primarily in sourcing and securing a supply of lithium in Argentina so that it has enough of the resources to build its fleet of electric vehicles. It is willing to far overpay relative to market cap in order to ensure that LIT has enough cash and financial motivation to build out a mine and ship lithium to the company's front door starting in 2028. Stellantis has the right of first refusal on any future financing needed or sale of lithium to third parties on production beyond the 15,000 tonnes outlined in the offtake agreement. Further evidence that the company's primary motivation is securing supply and making sure LIT has the cash to get the mine operational, regardless of cost.

The second argument is a more interesting one, and could imply a substantial upward re-rate for other junior lithium players that have mostly been overlooked while the price of lithium has crashed recently. But after speaking with LIT's CEO Nikolaos Cacos, it's clear that Stellantis had direct company-related reasons to target LIT. The two companies were negotiating the deal for over a year, and closed it despite the drop in the price of lithium. One prime motivating factor was Joseph Grosso being the Chairman of LIT, and the company being a part of the Grosso Group . Grosso has a history of success bringing resource projects to operations in Argentina, a very important factor when dealing with the sensitive and volatile nature of the country's geopolitical and economic climate.

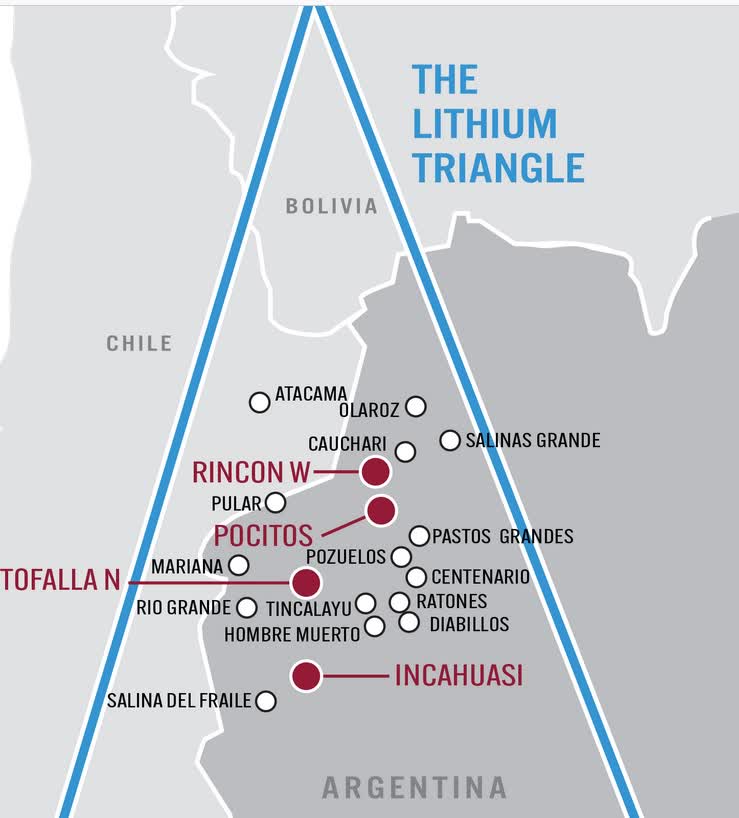

The other major motivating factor was location. LIT's flagship project is Rincon West, a 3,742.8 hectare-sized land package (460.5 hectares wholly owned, the rest under option) that is adjacent to Rio Tinto Group ( RIO ). Rio paid $825 million for the 83,000 hectares of mining rights from Rincon Mining less than two years ago. Stellantis was very interested in securing supply from this specific spot as the lithium arm's race in the Argentinian Lithium Triangle heats up.

argentinalithium.com/projects/overview-project-map/

{kind=link}

However, Stellantis isn't solely interested in Rincon West, although that will likely be the near-term focus. LIT has three projects just south of Rincon West with Antofalla North, Pocitos and Incahuasi being approximately 10,000, 26,000 and 25,000 hectare projects, respectively. So Rincon only makes up around 5% of the total land in the Lithium Triangle that is either wholly owned or under option to LIT. There is a lot of lithium potential for this company and it's all proximal to each other, which was likely the clinching factor for Stellantis calling first dibs. In this context, a $60 billion market cap company "overpaying" $90 million for a ~20% stake in a company that has secured about 65,000 hectares within the Triangle makes sense.

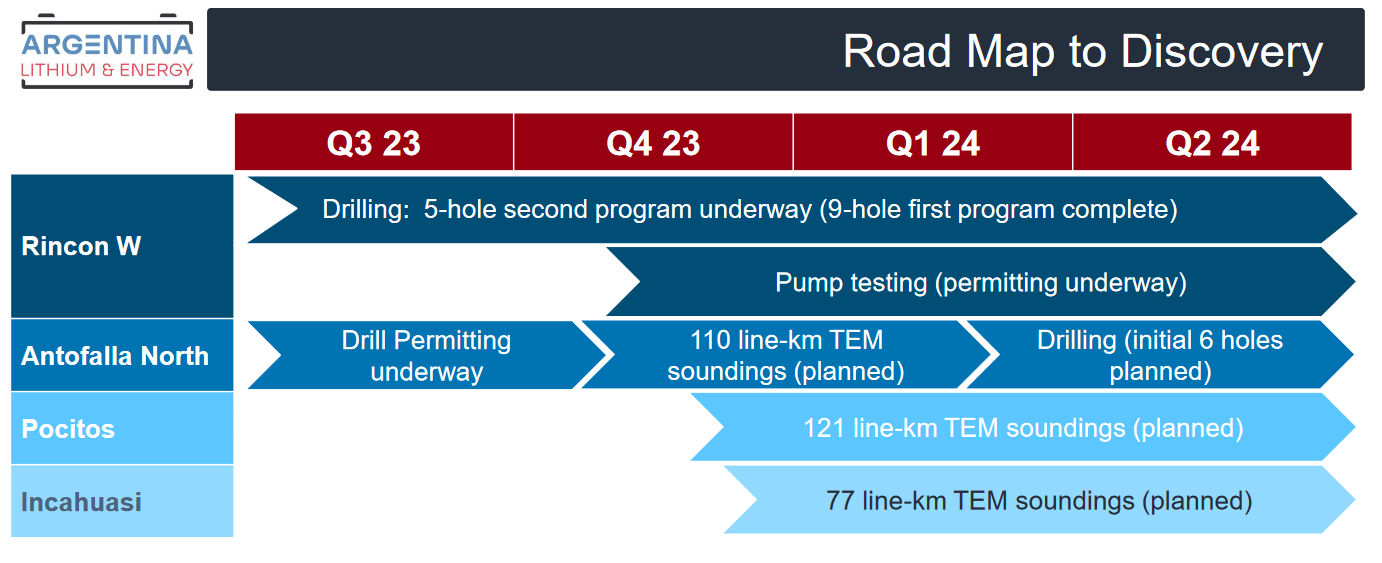

The company's roadmap shows that Rincon has an active drill program underway with drilling planned in Antofalla North in 2024. These projects are all in the early to very early stages and will take years before fully operational mines are present, but this is no issue for Stellantis as it's looking to secure resource for planned production five years from now. The single biggest obstacle to roadmaps being achieved in the junior capital world is a company's ability to fund all of its plans. With that obstacle removed for LIT and a large partner interested in seeing things move along as quickly as possible, I expect these timelines to be met or possibly even exceeded. Subject to timing of government permits and availability of equipment and labor in the region.

argentinalithium.com/site/assets/files/6485/lit-ppt-october-2023.pdf

{kind=link}

If we are thinking from the perspective of a large automaker trying to secure supply within a competitive Lithium Triangle, Stellantis didn't overpay, it paid the amount it needed to pay to accomplish a needed goal for future development plans. I liken this to an NFL football team that is desperate to secure a quarterback in the draft with the 5th overall pick. The teams drafting ahead of them already picked quarterbacks. Now this team has to draft what it feels is the next best one available with the 5th pick, even if that QB is rated the 10th or 15th or 20th or 25th best prospect overall by all the so-called experts. The team will have tryouts and interviews with the QBs leading up to the draft, and then analyze which one still available best fits their organization.

It doesn't matter what other people think of LIT's land package or accomplishments relative to other junior explorers in the region. They aren't the multi-billion dollar vehicle manufacturer ponying up $90 million betting on LIT's future ability to perform. It only matters what Stellantis thinks. The rest of the investment community must make its own buy and sell decisions knowing that Stellantis is highly motivated and capable to ensure LIT succeeds.

Coming up with a fair value today for LIT

As one member of that investment community, I have to assess what I believe to be a fair value for LIT based on the information I have, as well as the caveats and potential roadblocks that must be overcome to get to that valuation in a timely fashion.

As with every explorer, LIT is pre-revenue. It has about $2 million in expenses a quarter and this burn rate will substantially increase going forward as it attempts to accomplish the plans laid out in the roadmap for its four properties. Given the substantial investment by Stellantis, I believe that financing risk is completely taken off the table, as long as Stellantis remains a solvent entity. Any unexpected cost overruns or delays to expected production in 2028 might result in dilution but won't result in insolvency. I expect the cash runway from the investment to be a minimum of three years and if that cash is spent wisely, any further financing will happen at a superior valuation than today.

Argentina has historically been reasonably friendly to mining, and I don't expect that to change given the economic opportunity that lithium will provide the country. Being a member of the Grosso Group and getting the deal with Stellantis are two pieces of assurance that the company will be able to navigate at least one project through to production by 2028.

Stellantis is paying $90 million for an option to hold a 19.9% stake in the public listing, fully diluted. If Stellantis exercises this option, it would receive 53 million shares (out of a then total 266 million), essentially paying approximately $1.70 USD or $2.30 CAD for the shares. The simplistic analysis would be that if Stellantis is willing to pay that much, investors should be able to feel comfortable holding until at least that price range. But it may not be that simple.

The first issue to overcome is that this deal is in Argentinian Pesos. Due to the country's high inflation rate, the currency has been on a consistent downward trajectory. Therefore, LIT is looking to transfer most of that cash into USD and CAD, with some expected slippage in the 10% range. I expect the net result to be $80 million USD or $110 million in CAD.

There are currently 130.2 million shares outstanding along with 71.7 million warrants with a weighted average strike of $0.44 and 11.3 million stock options with a weighted average strike of $0.31. In the week between announcing the deal and closing the deal, SEDAR documentation shows that 150,000 warrants were exercised for shares. This share overhang may have accounted for the pullback in the stock price and may continue to apply some selling pressure going forward. Upon exercise of all of those derivatives, the share count would increase to 213 million but would also lead to an additional $35 million in cash.

Between the $110 million CAD-equivalent received from the Stellantis deal and $35 million from the exercise of derivatives, total cash in the bank would be $145 million, $0.68 per share. This is a reasonable floor valuation for LIT. The cash from Stellantis is earmarked for exploration and mine development costs or the purchase of additional properties in Argentina with some corporate expenses allowed. It can't be used for purposes like buying back stock or paying dividends. However, I don't see how cash received from the exercising of warrants would have that same restriction. It might seem silly to use cash received from the exercise of warrants to buy back shares, but in this circumstance, it makes sense to do so should the stock remain below the $0.68 level for an extended period of time. That may be one way to offset any overhang from the warrants being exercised.

The component of the deal that will provide LIT investors with the highest long-term value is the offtake agreement. It calls for "up to" 15,000 tonnes per annum of lithium produced over a seven-year period. However, with the way the offtake agreement is worded, I interpret it as Stellantis being at LIT's all-you-can-eat lithium restaurant and other customers only being allowed in once Stellantis has had its fill. For the purpose of my analysis, I will assume 15,000 tonnes shipped starting in 2028. The price paid by Stellantis will be market pricing based on the prior calendar quarter's price of the relevant sub-type of lithium as quoted by Fastmarkets with a small freight discount.

Violent swings in the price of lithium will likely continue, making price predictions for 2028 difficult. Though the bearish movement seen in 2023 is very unlikely to be the same market sentiment five years from now, unless a new battery technology comes along that puts a significant damper on the demand for Li-ion batteries. Pricing is much more likely to be above $50,000 per tonne than $20,000 per tonne, but I will take a reasonably conservative middle-ground price of $30,000 per tonne.

From there it's a matter of simple math. 15,000 tonnes at $30,000 per tonne is $450 million in revenue. Assuming a 35% margin, that's $158 million in gross margin. Take off another $30 million or so for SG&A and 25% for taxes and LIT is left with approximately $100 million per year in net income. Apply a 10x multiple and we are looking at a billion dollar company. Now it's time to look at the obstacles to be overcome in order to get to that level.

As I mentioned before, this deal takes financing risk off of the table. Any additional funds needed for construction will be found. However, that will come at the cost of dilution. While Stellantis wouldn't have signed this deal without having a strong inkling that LIT will have the resource ready for shipment starting in 2028, until we have feasibility studies available on the properties, this remains a big "if" for the investment community. As seen in the roadmap above, LIT is still at the starting stages of drilling.

Based on the vague nature of the economics and timing of lithium operations - the same level of vagueness any early-stage explorer would have - I require a discount rate of 75%. That would take the billion dollar valuation down to $250 million. My analysis assumes LIT's full ownership of the operating subsidiary, and that Stellantis exercised its option to convert into shares, leading to a total of 266 million outstanding. All cash would be used in mine development so nothing would be available to buy back shares or could be added to the enterprise value to pad the valuation. This leads to a $0.94 US per share target, or approximately $1.30 for LIT's Canadian listing.

The steep 75% discount is a by-product of a 4-5 year wait before LIT generates revenue, a lithium price which has been volatile and will continue to be volatile towards 2028 (though I expect more upside than downside), and the fact that we have no economic reports out to assess construction costs, cost to mine, grade or total resource estimate yet. If any of these variables were to be substantially below mine and Stellantis' expectations, it would hurt the $1.30 price target. Conversely, if these issues met or exceeded expectations, the stock should head towards this target. But because of the strong cash balance today, I believe the floor on LIT is high enough that there is an asymmetrical reward-to-risk outcome even in a less than favorable performance scenario.

I have three ways to evaluate a fair price target on LIT. First, the CAD cash per share estimate assuming all derivatives are exercised leads to $0.68. That could be seen as a minimum target for short-term holders who aren't really that interested in the lithium story, but want to take advantage of the opportunity provided by Stellantis' aggressive cash-heavy investment. The second method would be to use Stellantis' valuation based on paying $90 million US for a 19.9% stake, leading to a valuation of over $600 million CAD or $2.30 per share. The third would be to take my back-of-the-napkin math on the offtake agreement to come to $1.30 per share, then re-assess the position should the stock price hit that level but company accomplishments might require an improved discount rate. No matter what method I use, at $0.55, LIT is ambiguously a buy and hold.

What does this mean for other lithium players in the region?

Going back to my NFL Draft analogy, let's say Team Stellantis decided to draft the QB that was deemed the 15th best pick by the pundits. Now only the 10th, 20th and 25th best-rated players are available at the QB position. The options for QB for the rest of the teams just dropped from four to three, and it also doesn't preclude Team Stellantis from drafting another quarterback because they plan to do A LOT of passing in the next few years. Okay, so the analogy isn't perfect, but it gets the point across. Stellantis just made an aggressive move to take one junior explorer from the Lithium Triangle essentially for itself, but that doesn't mean that it's done. Buyout offers for Arena Minerals and Alpha Lithium have also taken place in 2023, further limiting cheap junior options to securing lithium supply.

This M&A activity makes the remaining explorers inherently more valuable and the companies looking for lithium supply more desperate. We should be seeing a substantial upward re-rate across the board in Argentina, but the price action since LIT's deal first came to light hasn't indicated as such so far.

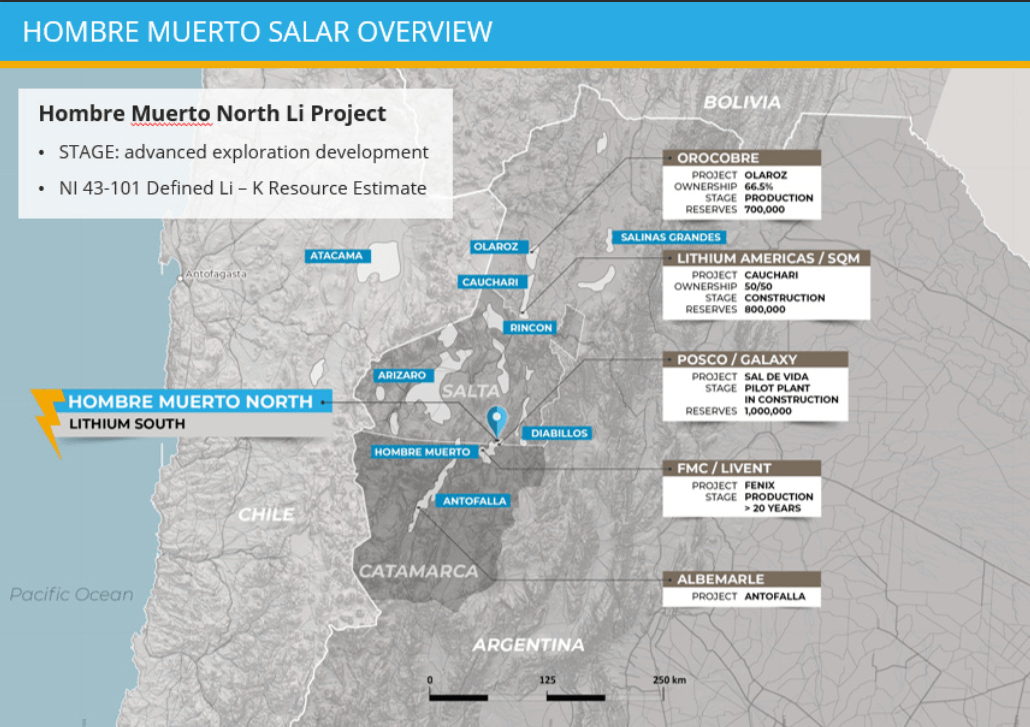

One such floundering company is Lithium South Development Corporation ( LISMF )( LIS:CA ), which sits just about at its 52-week low. It sits around a $40 million CAD market cap, a little more than half where LIT is now without a $90 million deal. There may be a good reason for that as LIS is further along with its drilling and resource estimate.

Lithium South's flagship project is Hombre Muerto North , which sits right in between LIT's Rincon West and Antofella projects. There are a number of larger players in the region, namely POSCO Holdings Inc. ( PKX ) which is directly adjacent to LIS' 5,687 hectare project.

www.lithiumsouth.com/projects/

{kind=link}

LIS filed a preliminary economic assessment in the past and has recently increased its lithium resource estimate by 175% after further drilling in 2022 and 2023. It now has 1,583,100 tonnes of Lithium Carbonate Equivalent with 1,462,900 of that being measured. If there was another company looking for 15,000 tonnes of LCE per year, it appears that LIS would be able to provide that for the next 100 years.

LIS is a company I own and therefore have more familiarity, but there are numerous publicly traded companies with early-stage projects in the Lithium Triangle, such as Argosy Minerals Limited ( ARYMF ), Lithium Energi Exploration Inc. ( LXENF )( LEXI:CA ) and NOA Lithium Brines Inc. ( NLIBF )( NOAL:CA ). Companies with holdings primarily in Chile but within or close to the Triangle also can't be overlooked, such as Lithium Chile Inc. ( LTMCF )( LITH:CA ) or First Lithium Minerals Corp. ( PGPXF )(FLM:CA). I encourage investors who are interested in the region to do some research into those names.

Junior lithium companies have been pounded into the ground due to the general bearish market in the small-cap space and with the diving price of lithium in particular. What LIT's deal with Stellantis shows, along with other M&A activity in the region, is that high interest rates, inflation and general geopolitical instability is not going to stop the supply and demand imbalance of the lithium industry. The electric vehicle manufacturers will determine the viability of this industry, not the general macro climate nor Wall Street pundits. If a deal like this between LIT and Stellantis can be made in the fall of 2023, imagine what the value of lithium companies in Argentina will be when bullish supercycles become the buzzwords of day again.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Argentina Lithium: $90 Million Investment From Stellantis Implies A Substantial Upward Rerate