ARBKL - Argo Blockchain: The Next Miner Squeeze Casualty

Summary

- Argo Blockchain has been selling down its BTC treasury holdings all year. That selling started to become more aggressive in June.

- The company has also been selling machines to raise liquidity and has dealt with challenges from higher energy costs.

- Argo also has baby bond shares that are now priced at just 50 cents on the dollar, indicating the market is worried about Argo's ability to pay the dividend.

Yesterday both the cryptocurrency community and the traditional equity investment world learned the leading Bitcoin ( BTC-USD ) miner by monthly production is facing insolvency . While each company has its own struggles, it's difficult not to look at what just happened with Core Scientific ( CORZ ) and wonder who is next. The majority of the macro headwinds that Core Scientific has been dealing with are challenges that every other Bitcoin miner is sharing. Specifically, with increases in the hashrate and difficulty for block rewards, the miners have been experiencing a nasty margin squeeze for most of 2022:

Mining profitability (BitInfoCharts)

{kind=link}

Mining profitability hit an all-time low just a few days ago and in light of the CORZ news, it's reasonable to start wondering if there will be another casualty from the margin squeeze.

Argo's Underperformance

One of the publicly listed Bitcoin miners that I've been telling BlockChain Reaction subscribers to avoid for several weeks is Argo Blockchain ( ARBK ) ( ARBKL ).

1 Month Returns (Seeking Alpha)

{kind=link}

You can see in the chart above that Argo had already been the weakest performing publicly listed miner over the last month before yesterday when CORZ collapsed about 75%. This weakness was likely a response to Argo's announcement that it was selling 3,400 mining machines earlier this month. The asset liquidation being an attempt to raise $6.8 million in cash. From the company's PR :

As previously reported on 9 September 2022, the Company has seen headwinds from the price of both natural gas and electricity caused by the geopolitical situation in Europe and low levels of natural gas storage in the United States. These factors, coupled with the decline in the price of Bitcoin since March 2022 and the increased mining difficulty, have reduced the Company's profitability and free cash flow generation.

High energy prices have been plaguing many of the publicly traded miners but Argo stands out in a bad way because of its high debt load compared to other similarly sized mining operations.

Balance Sheet

Glancing at the balance sheet, it's easy to see why the company needs cash. There is a high debt burden compared to peers and not much left to pay the bills.

| CORZ |

| BITF |

| IREN |

| CLSK |

| BTBT |

| ARBK |

| Market Cap |

| 360.87M |

| 222.25M |

| 198.21M |

| 174.25M |

| 92.37M |

| 94.03M |

| Enterprise Value |

| 1.38B |

| 296.03M |

| 196.53M |

| 190.94M |

| 57.12M |

| 219.94M |

| Total Cash |

| 128.54M |

| 45.98M |

| 109.97M |

| 3.48M |

| 44.30M |

| 11.21M |

| Total Debt |

| 1.15B |

| 123.64M |

| 108.29M |

| 20.16M |

| 0 |

| 143.63M |

| Net Debt |

| 1.02B |

| 77.65M |

| -1.68M |

| 16.68M |

| -44.30M |

| 132.42M |

| Total Debt to Equity |

| 275.77% |

| 36.89% |

| 24.76% |

| 5.35% |

| 1.71% |

| 71.44% |

Source: Seeking Alpha

Like Core Scientific, Argo Blockchain has a debt to equity position substantially higher than most peers. At the end of Q2, Argo had $53.4 million in short term borrowings, $15.3 million in accounts payable, $14.9 million in combined cash and receivables, and just $14.4 million in revenue in the quarter.

Similarities to Core Scientific

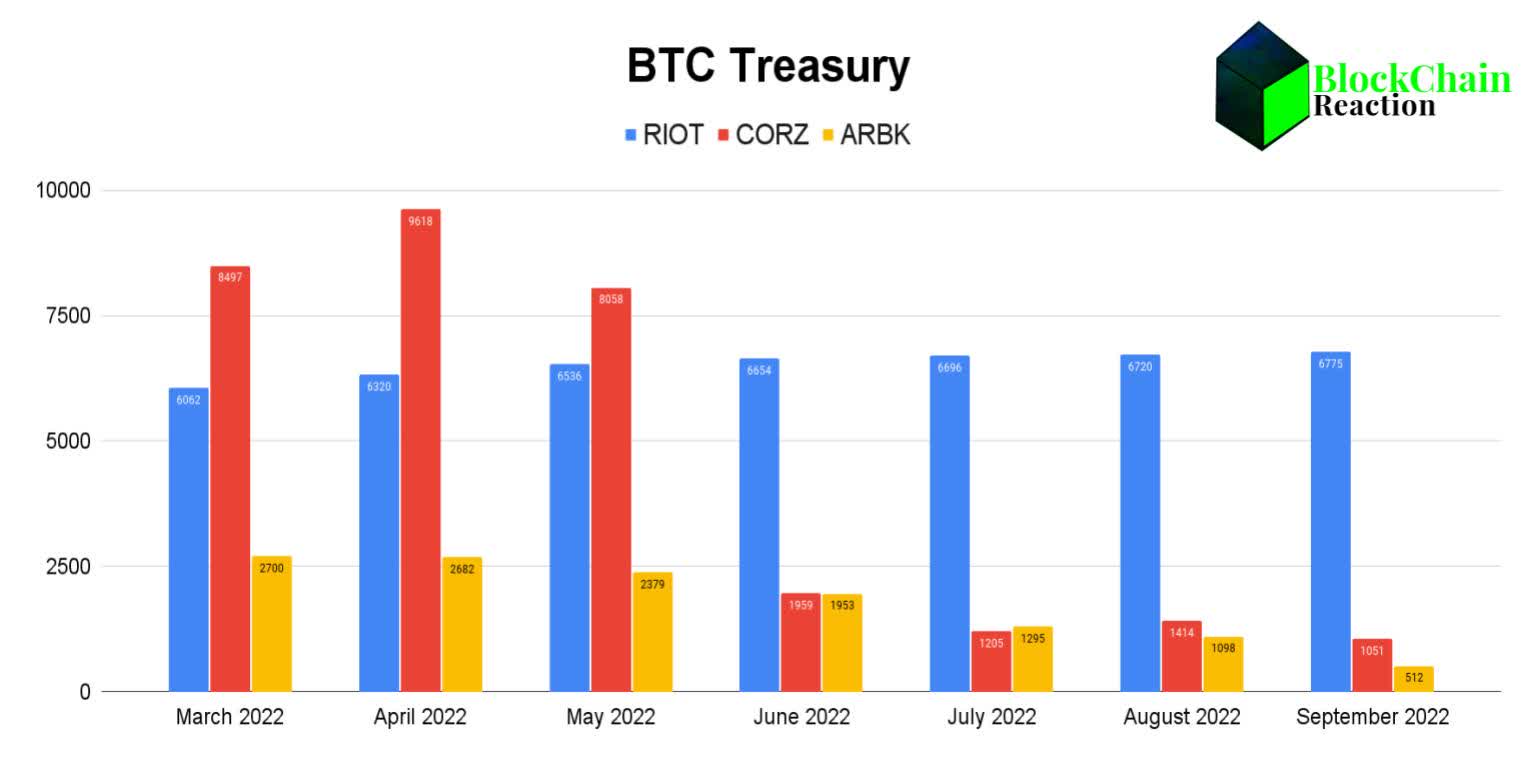

There were tea leaves to read leading up to Core's disclosure that it can't service its equipment obligations next month. A big indication that Core was in trouble was the aggressive treasury selloff from May to June. Core sold off roughly 75% of its BTC stack over that time period but the peak in the company's treasury actually happened in April. We can see some similarities in Argo. I've added fellow Bitcoin miner Riot Blockchain ( RIOT ) as a barometer to show that not all miners have been selling down their treasuries this year:

BTC holdings (Company releases)

{kind=link}

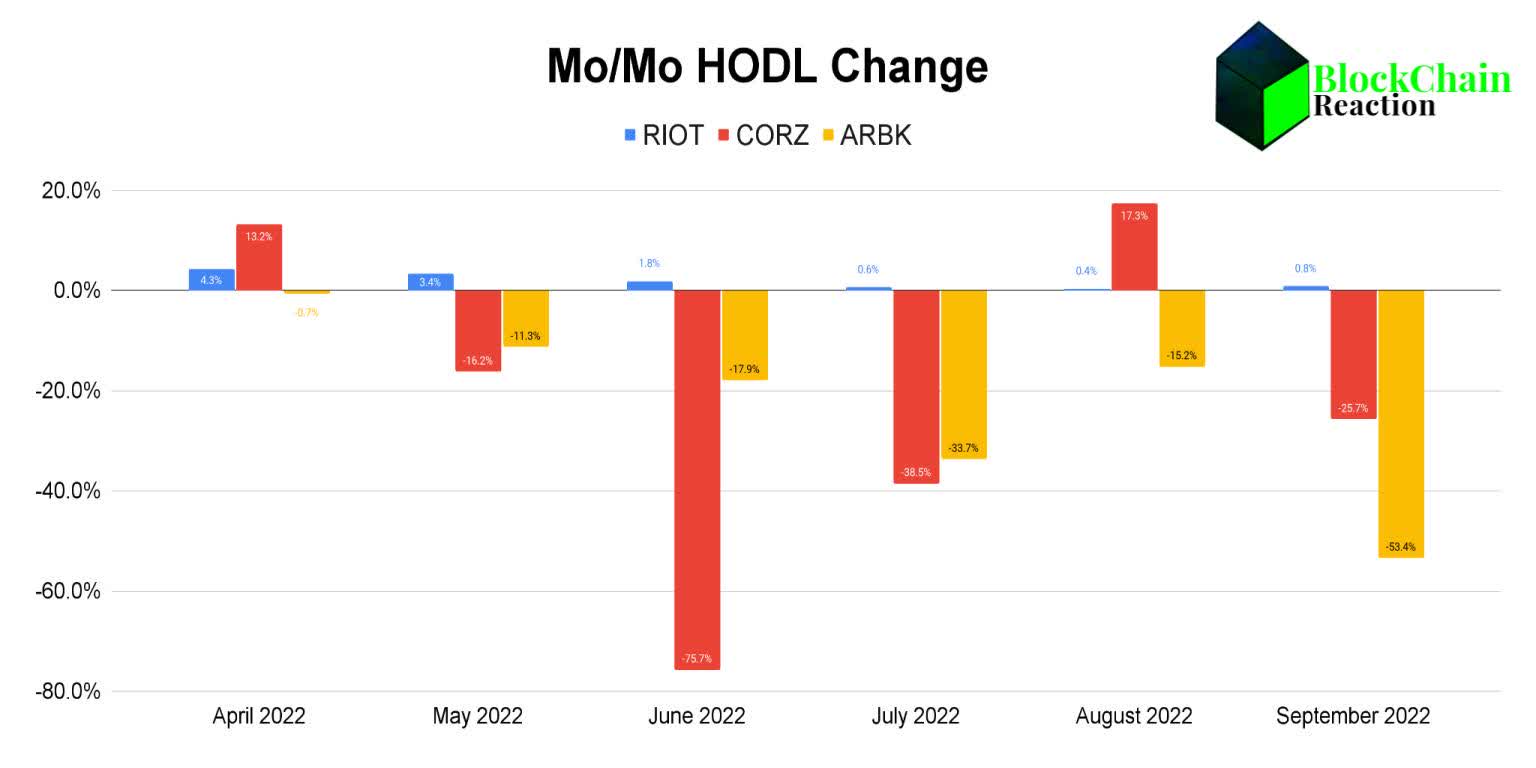

Argo had 2,700 BTC in March and just 512 BTC at the end of September. While Argo's BTC sales started a little bit earlier than Core's, we do see Argo's BTC selling getting more aggressive in the last few months:

Monthly HODL change (Company releases)

{kind=link}

Argo sold down by 34% in July and by 53% in September. While Argo's drawdown has been slower than Core Scientific's over the last 6 months, the company is running out of BTC to sell to raise cash.

Baby Bonds Collapsing

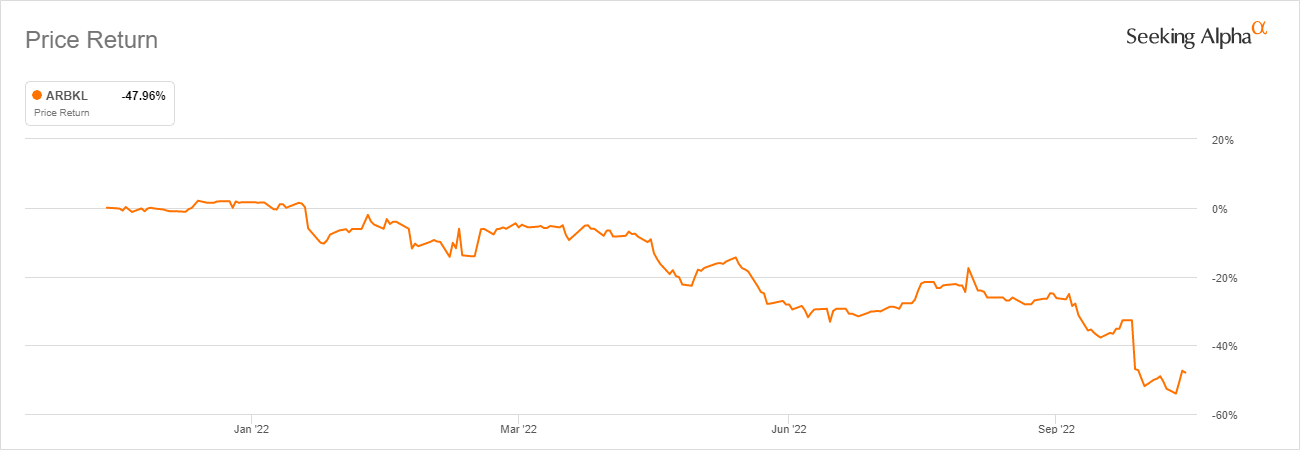

But it isn't just the drawdown in the company's Bitcoin treasury or the selling of machines that I think are the most concerning indicators for Argo. If the market expected Argo to survive crypto winter, I don't think the ARBKL baby bond shares would be trading at 51 cents on the dollar:

1yr ARBKL share return (Seeking Alpha)

{kind=link}

The 90% drawdown in the price of the common shares is bad. But the collapse of the ARBKL shares is worse from an optics perspective in my view. These shares have a value of $25 and pay an 8.75% yield at par. At a current share price of $12.75, ARBKL is trading at a 49% discount to par and offering a 17.15% yield. This is either a huge opportunity or a clear sign that the market doesn't think Argo can pay its bills. I'm leaning it's the latter.

Risks in Going Short

While I think Argo Blockchain is in a race against time, I would only short after a 90% selloff if you are a highly experienced trader. Argo's success is still tied to Bitcoin at the end of the day. Also, according to iBorrowDesk, shares available have been trending down the last few days and cost to borrow is trending higher:

{kind=link}

While the fundamentals look absolutely terrible for Argo, sentiment can change if Bitcoin starts to rise and profitability in the sector gets a rebound. I'm of the opinion that there are several miners that will do better if BTC does indeed turn it around, but a short position in ARBK could get wiped out very quickly if BTC has a sustained bear market rally and there are reasons to suggest a move like that is possible. If you do go short ARBK it might be wise to go long one of the better positioned miners as a hedge.

Summary

The biggest problem for every Bitcoin miner at the moment is the margin squeeze from low BTC prices. If you are of the opinion that Bitcoin is going lower, then I think Argo Blockchain is highly likely to be the next listed miner to take a dive. The company has a high debt burden, high costs, is selling assets for cash, has very little BTC left to sell, and has baby bonds priced at 50% of face. Even if Bitcoin rallies, there is a chance ARBK shares still go down through dilution if the company decides to raise capital through an offering. If you're long, I'd sell and move on. If you want to short it, I'd wait for a pop in price and hit the rip.

For further details see:

Argo Blockchain: The Next Miner Squeeze Casualty