ARNGF - Argonaut Gold: Inflationary Pressures Dent Margins In Q2

Summary

- Argonaut Gold released its Q2 results earlier this month, reporting quarterly production of ~59,200 gold-equivalent ounces, a 7% decline from the year-ago period.

- The lower gold sales translated to a decline in revenue year-over-year despite a higher gold price, with a further dip likely in Q3 with the softness we've seen quarter-to-date.

- Worse, operating costs were up sharply to $1,474/oz, with Argonaut revising its cost guidance higher due to inflationary pressures.

- While Magino is a game-changer that should begin production in Q2-23 and the stock is cheap at less than 0.50x P/NAV, I continue to see far better bets elsewhere in the sector.

Just over three months ago, I wrote on Argonaut Gold ( OTCPK:ARNGF ), making a terrible call that the stock would become a Speculative Buy below US$0.89. While I was certainly correct to label this a speculative bet, given that it was going to need additional capital as a buffer to complete Magino construction. However, I expected this to be funded through the mix of debt and a stream, or a joint venture. Instead the company chose to sell over 430 million shares at arguably the worst possible time, leading to a doubling of the share count.

{kind=link}

Magino Construction (Company Presentation)

The result is that I took a loss on my position, and it's a good reminder of why stops are critical for small-cap stocks, especially in the mining sector, where downside surprises come often. It's also a good reminder that there's simply no reason to go dumpster diving or get involved in risky situations, a rule I broke on this swing trade gone wrong that cost me 0.25% of my year-to-date portfolio gains. Now that the dust has settled let's take a closer look at the recent results and whether the stock is worth buying.

Q2 Production

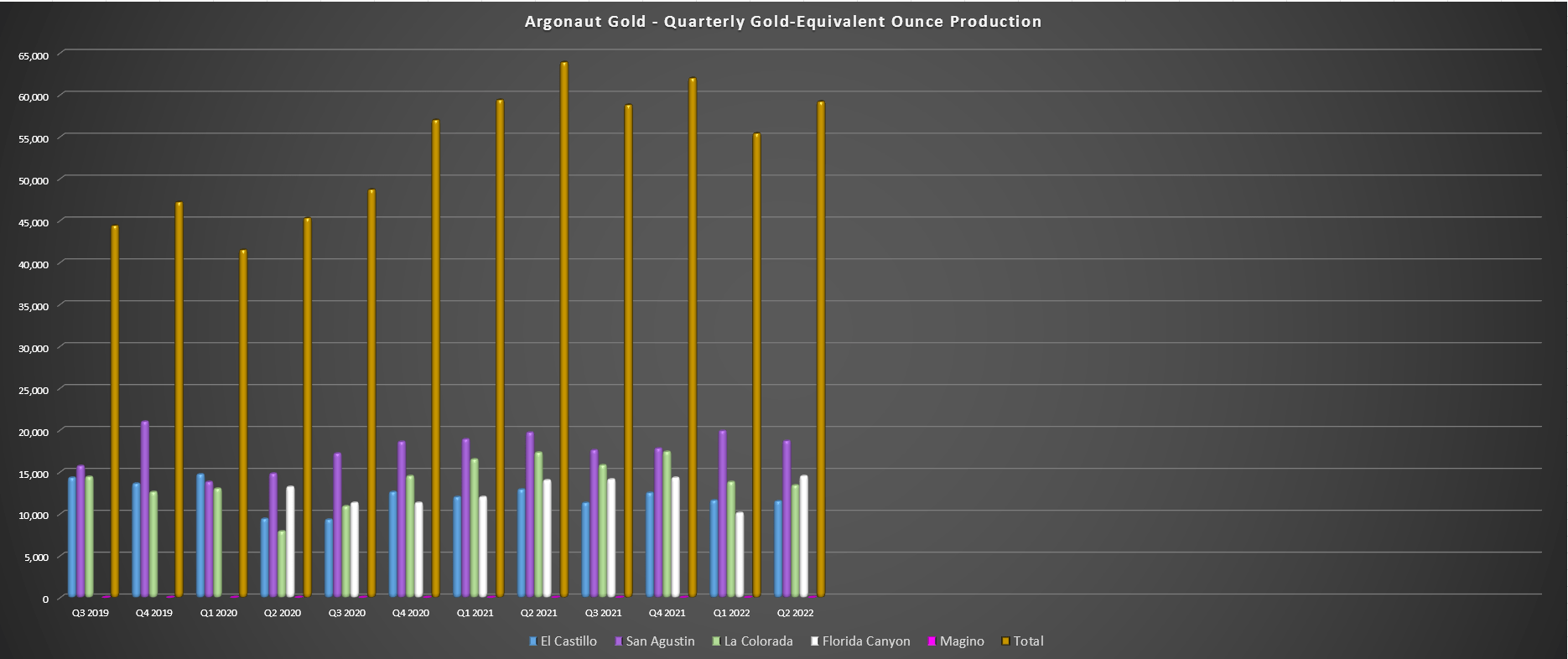

Argonaut Gold released its Q2 results earlier this month, reporting quarterly production of ~59,200 gold-equivalent ounces, a 7% decline from the year-ago period. The lower production was related to fewer tonnes mined, lower grades, and lower recovery rates at La Colorada, with lower production year-over-year at every mine except its highest cost Florida Canyon Mine. The largest decline was at La Colorada, where production slid from ~17,300 GEOs in Q2 2021 to ~13,400 GEOs, with the 500 extra GEOs produced at Florida Canyon unable to offset this sharp dip in production.

{kind=link}

Argonaut Gold - Quarterly Production by Mine (Company Filings, Author's Chart)

The good news is that despite the lower ounces produced, production was in line with budget and is sitting at ~114,700 GEOs year-to-date, with Argonaut in good shape to meet its FY2022 guidance (~200,000 - 230,000 GEOs). Unfortunately, while production is tracking in line with FY2022 guidance, Argonaut wasn't immune from inflationary pressures and joined the list of miners revising full-year cost guidance.

This shouldn't be surprising, given that Argonaut operates four low-grade, high-volume operations (La Colorada, Florida Canyon, El Castillo, and San Agustin). So, while production guidance was maintained, cost guidance was pushed considerably higher and now sits at industry-lagging levels by a wide margin. In fact, even at the bottom end of guidance ($1,500/oz - $1,600/oz), Argonaut's AISC margins are below 20% at spot prices. Let's take a closer look below.

Costs & Recent Developments

As discussed in more recent updates, Argonaut Gold was one name that was likely to be particularly sensitive to inflationary pressures. The reason is that it already had high-cost operations, it doesn't benefit from economies of scale, and due to the large volume of material it moves/treats, higher fuel and reagent costs would put a severe dent in margins. This is what we saw in Q2, with all-in sustaining coming just shy of a new high at $1,474/oz, which was just shy of the previous high of $1,514/oz recorded in Q4 2021. If we compare this to pre-COVID-19 levels, all-in-sustaining costs are up ~25%, wiping out most of the benefit from a higher gold price ($1,750/oz vs. $1,450/oz).

{kind=link}

Argonaut Gold - All-in Sustaining Costs Per Ounce (Company Filings, Author's Chart)

Argonaut noted that this was related to inflationary pressures from oil, natural gas, and lime, areas where it's quite sensitive due to the nature of its operations. The particularly disappointing part about the costs is that these all-in-sustaining cost figures in Q2 were despite a sharp decline in sustaining capital from the year-ago period and a decline in exploration spending. Hence, Argonaut had a ~$5.0 million tailwind in the period but still saw a high double-digit cost increase. If we look at the revised guidance, all-in sustaining costs are now projected to come in at $1,550/oz for the year at the mid-point, which hurts given the recent decline in the gold price, putting a severe dent in already slim margins.

{kind=link}

Argonaut Gold - Updated Guidance (Company Presentation)

So, what's the good news?

Previously, Argonaut was at risk of not being able to complete Magino construction, and while it sold out its shareholder base to fund the project (equity dilution at multi-year lows), Magino will be Canada's newest mine in April 2023. This operation will likely have average costs below $950/oz even with the impact of inflationary pressures (2024-2027), pulling Argonaut's consolidated cost base below $1,200/oz in 2024. The result would be that Argonaut would move from being a high-cost producer to an average-cost producer, boosting margins for the remainder of the decade, even if gold prices remain below $1,800/oz.

The other good news is that it appears to be tracking well against its updated capital estimate of ~$730 million. However, this isn't anything to hang one's hat on with capex already revised 140% above initial estimates (~$300 million). Lastly, simultaneous with its financing to fund the remainder of Magino capex (construction is 57% complete at quarter-end), Argonaut hedged its gold price exposure with 25,000 ounces per quarter hedged for $1,860/oz. While this might not have seemed bright then, it will help improve Argonaut's average realized price in Q3 2022 and potentially Q4 2022 if the gold price remains under $1,800/oz.

While these are positive developments, and the bad news is mostly out of the way after multiple capex revisions, it's largely overshadowed by the company's decision to sell ~430 million shares (~120% share dilution) at a price of C$0.45 [US$0.36]. Although Argonaut had limited options to take care of the funding gap, I think selling a stream or partnering on the project to help fund the remainder of capex would have made much more sense than diluting at these prices when each share was providing little benefit due to waiting for an 80% decline to raise money.

So, while Argonaut's future might be brighter, it has kissed any production growth per share or cash flow per share growth goodbye with its massive capital raise at extremely unfavorable prices. Unless I'm mistaken and am focused on the wrong metrics, I thought this was the whole point of building a new mine: to grow cash flow per share/production per share).

Valuation

Based on ~775 million fully diluted shares and a share price of US$0.38, Argonaut trades at a market cap of ~$295 million. This compares favorably to an estimated net asset value of $650 million after adjusting for higher capex at Magino, higher costs at its existing assets (inflationary pressures), and $150 million in corporate G&A. So, assuming the gold price can maintain the $1,700/oz level, Argonaut trades at just 0.45x P/NAV or less than 3x FY2023 cash flow estimates.

This is a very reasonable valuation for a mid-tier producer, and we have seen an overhaul of the management team, with new President & CEO Larry Radford previously being Senior Vice President & COO of Hecla Mining ( HL ), where he managed multiple mines. That said, we've also seen a significant decline in multiples sector-wide, with several more diversified producers with much more robust operations are also trading at significant discounts to net asset value and their historical multiples.

The result is that it makes it difficult to justify going dumpster-diving for Argonaut when lower beta names that would likely hold up better against continued general market weakness are also trading at fire-sale prices. Besides, suppose inflationary pressures persist, or gold prices weaken further. In that case, the relatively high-grade and lower volume mines that some operators like Agnico ( AEM ) have in their portfolio will perform much better and have a large buffer from a margin standpoint. In Argonaut's case, this is really a Magino/La Colorada story, with its other mines being quite marginal and very sensitive to oil, natural gas, and lime prices.

Based on what I believe to be a fair P/NAV multiple of 0.70x for Argonaut once Magino is in production (slightly below average cost producer, but still meaningful exposure to Mexico), I see a fair value of US$455 million. If we divide this by an estimated 780 million fully-diluted shares (year-end 2023), this translates to a fair value of US$0.58, or 52% upside from current levels. However, with names like Karora ( OTCQX:KRRGF ) and Agnico having more than 80% upside to fair value with less risk (not relying on a future project for a re-rating), I continue to see far more attractive opportunities elsewhere.

Technical Picture

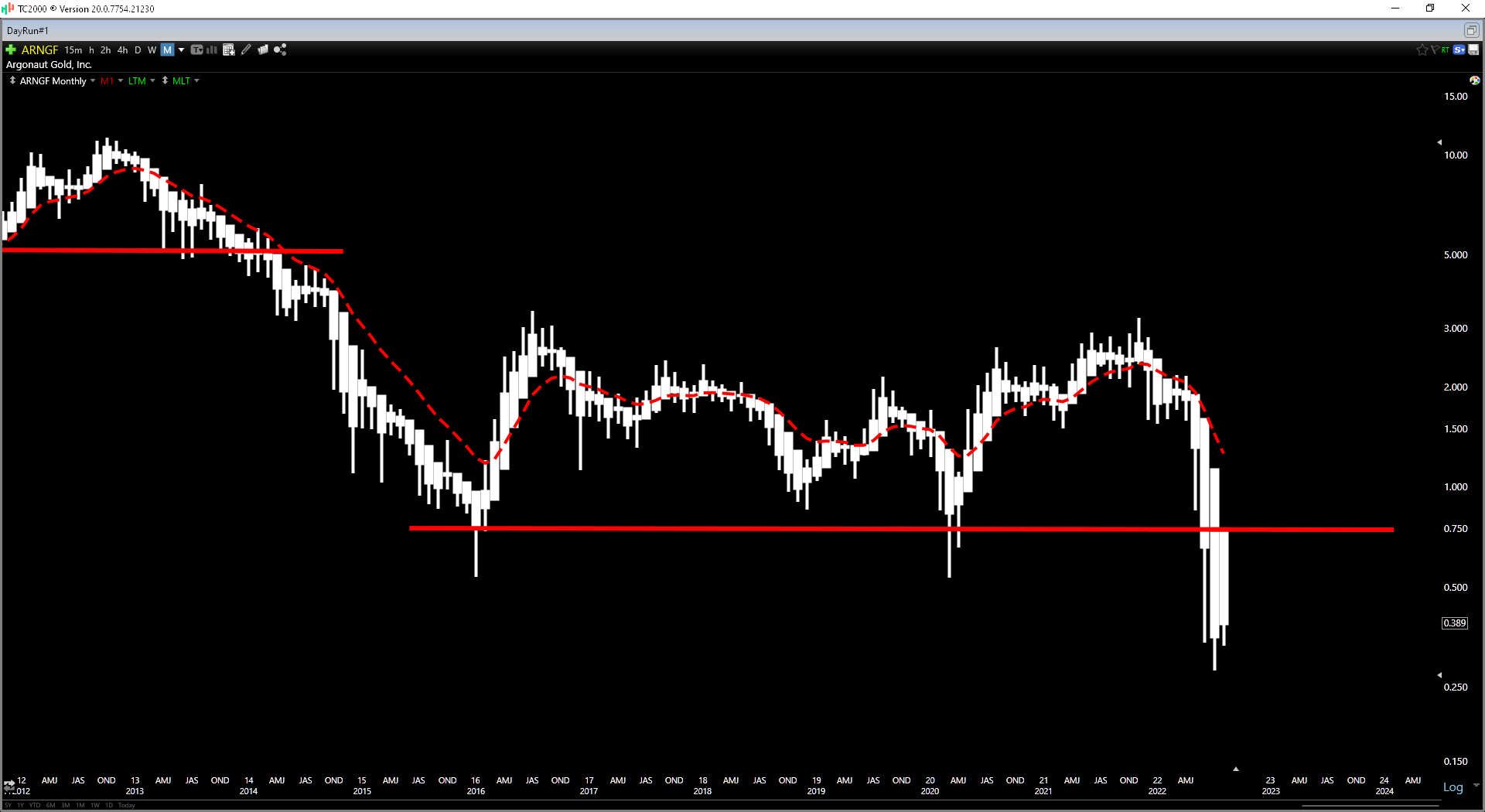

Moving to the technical picture, Argonaut has broken down below a multi-year base, similar to what it did in mid-2013. Following this breakdown, there was little value in going long the stock until it reclaimed its monthly moving average (red line), which took nearly three years and another 85% decline. While history may not repeat itself, and this is a different cycle currently, we are only at a 55% decline from the area of the breakdown currently, suggesting that Argonaut could easily break its lows at US$0.28 or make new lows before this correction is over.

{kind=link}

ARNGF Weekly Chart (TC2000.com)

So, if I were interested in bottom-fishing, I would be waiting for a similar setup to 2016 or 2020. This setup would be ARNGF reclaiming its monthly moving average, which significantly increased the probability that the low was in and led to triple-digit returns (draw-up) over the next 12 months in both instances. Of course, the risk of not being long the stock is that another producer comes in to acquire Argonaut at a large premium. However, I prefer to be disciplined and not bottom-fish mediocre stories, and this is the definition of a mediocre story at a time when the best names are trading at their most attractive valuations in years.

Summary

Argonaut Gold has paved a path to successfully constructing Magino without any major delays due to a funding shortfall, but in the process, it's more than doubled the share count and massively diluted many loyal shareholders. We've also seen a degradation in NPV (5%) at Magino and existing operations due to higher capex/inflationary pressures, weighing on the stock's net asset value. The result is that even after the 60% plus share price decline, Argonaut is not all that much more attractive, even if it is beginning to get oversold.

In my view, the bigger issue is that several other companies have become much more attractive, and when a fire sale has occurred, it makes sense to bet on the highest-quality stories rather than go dumpster-diving. This is because mediocre stories can go on sale once or twice a year, but obtaining a position in a high-quality company at multi-year low valuations only happens once or twice a decade. For this reason, I continue to see far more attractive ways to play the sector, and I would only become interested in Argonaut if we were to see clear signs of accumulation and a trend change from a swing-trading standpoint.

For further details see:

Argonaut Gold: Inflationary Pressures Dent Margins In Q2