EPAM - Argosy Investors Q2 2023 Letter

2023-08-09 10:00:00 ET

Summary

- Argosy Investors is a fee-only investment adviser seeking to earn above-average returns through a risk-conscious approach that allows us to maintain significant amounts of cash if the conditions warrant, and to deploy capital quickly and aggressively when opportunities are more plentiful.

- Argosy Investors will no longer report performance publicly due to new regulations.

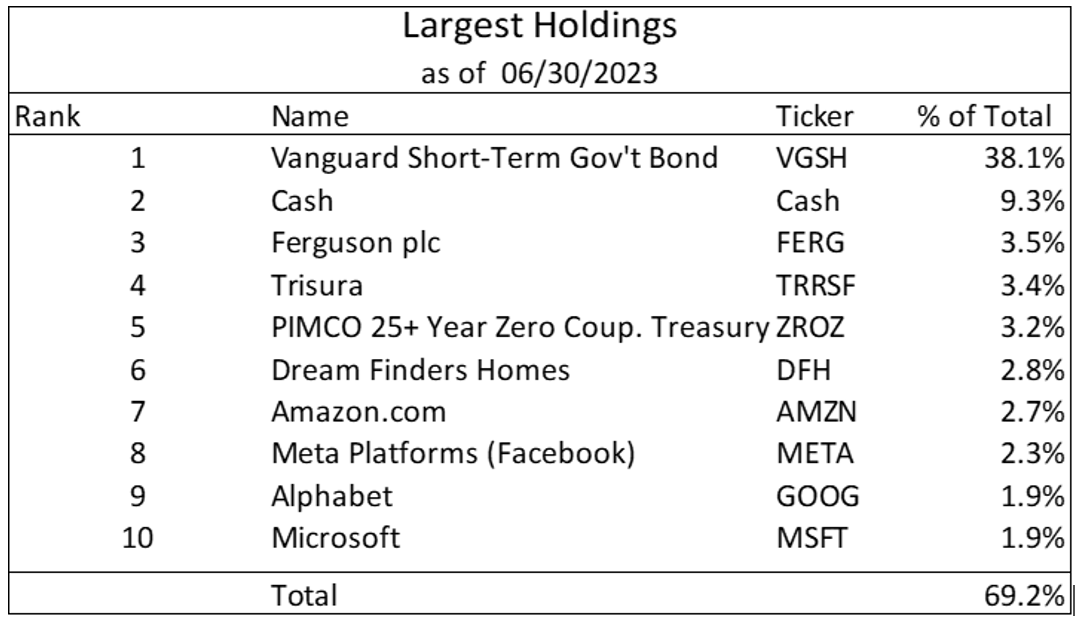

- The portfolio ended the quarter with 52% in cash and equivalents.

- Argosy sold positions in Torrid Holdings and Ollie's Bargain Outlet and bought a position in Endava.

Dear Investors,

I will no longer be reporting performance publicly based on recent marketing regulations issued by the state of NC. During the period, the S&P 500 ( SP500 , SPX ) returned 8.7%. We ended the quarter with 52% of the portfolio in cash and equivalents. The environment we’re in warrants a risk-conscious approach, and while no one will accuse me based on these letters of completely ignoring risk, the present moment feels like one in which to be especially conscious of the risks in the economy and market. We see some companies in industries we know fairly well that are seeing their prices severely dislocated, including one we purchased after the end of the quarter, and one we purchased during the quarter, Endava ( DAVA ). We will look to judiciously grow your wealth during the current period, but we think risk control will pay perhaps larger dividends, and enable us to invest much more aggressively when others can not or will not.

EXISTING PORTFOLIO ACTIVITY

Sold: TWKS , CURV , GDYN , OLLI

Bought: DAVA

During the quarter, I did mostly housekeeping, selling a couple of smaller positions in Torrid Holdings and Ollie’s Bargain Outlet. In other news, I essentially swapped the positions in Thoughtworks and Grid Dynamics for a position in Endava. First, Torrid Holdings was never a large position, but it performed horribly during my ownership of the position. Body positivity, as it turns out, was not a positive development for Torrid. Long operating somewhat alone in the plus size women’s apparel (that women actually want to wear) category, COVID and the advent of stars such as musical artist Lizzo shined a light on women who did not fit the traditional definition of beauty. As a result, every retailer from Victoria’s Secret ( VSCO ) to Sephora has embraced body positivity, featuring plus size models in their marketing content and making clothes for larger people. Torrid lost its differentiated position in the market, and I believe has been struggling to remain relevant when plus size women have so many more options than they used to. In any event, this women’s fashion has never been something I considered myself an expert in, so perhaps I should be a little more cautious next time I venture into this quixotic realm.

Ollie’s Bargain Outlet ended essentially at the same price I bought it more than 3 years ago, compared to a ~27% gain for the S&P, ex-dividends. A quirky off-price retailer after my own heart, I bought a gift for a White Elephant (a Christmas gift exchange) at one of their stores in rural Georgia that consisted of a bathroom rug and a pizza-shaped miniature piñata. They inventory all kinds of interesting things, like poor-selling romance novels, shelf-stable food, an oddly large assortment of carpets and rugs, many kids toys, and much more. It seemed like a great business for an uncertain economy and widening income inequality when I purchased in January 2020. Then COVID happened. People are locked inside and people from ages 2 to 92 are downloading Amazon ( AMZN ) and DoorDash ( DASH ) for the first time, not able or willing to venture out to physical stores. Additionally, off-price inventory became more scarce as some categories, such as shelf-stable foods and the all-important roll of TP (toilet paper), experienced a rush of demand from the same people locked down at home. In the end, Ollie’s remains priced about as expensively on a P/E basis as it did when I bought it, and despite all of the retail bankruptcies that have occurred recently, Ollie’s has not been able to effectively take advantage of it. Based on their execution and no desire to scale up the position, I decided to sell to simplify the portfolio.

Finally, Endava is one of the better-managed IT outsourcers among its peers, with perhaps only EPAM being better managed among at least the US-listed stocks. The very tangible (for some) chill that has befallen the tech sector’s once-rapid employment growth seems to be also impacting projects that Endava and other outsourcing companies were working on. As a result, the entire sector has fallen rather significantly. Given the indiscriminate selling of quality companies in the space, I decided to sell Thoughtworks, a slower-growing outsourcer with some suspicious foreign ties I wasn’t previously aware of, and Grid Dynamics, a much smaller company that I bought during the COVID pandemic after it went public via SPAC.

One of the challenges with former SPAC companies is that their incentives were poorly aligned when they went public, so there is the possibility that they won’t behave any better once public. When Grid Dynamics went public, it went public as a $100MM revenue company with significant growth opportunities ahead of it. Because of this, I looked past the significant stock-based compensation when I initially bought because oftentimes newly-public companies will issue a large amount of stock-based compensation (SBC) as a reward for a successful IPO and to incentivize the management team. We’re now 3 years past their IPO via SPAC, and the SBC issue remains.

In 2022, SBC is nearly 20% of revenue, the same % the year the company went public, and the company remains unprofitable on a GAAP basis but is conveniently profitable on a non-GAAP (I.e. adjusted for outrageous SBC) basis. At >$300MM of revenue, Grid Dynamics has no excuse for not achieving GAAP profitability. EPAM at a similar revenue level was significantly profitable with 15% operating margins and >20% annual growth. I grew tired waiting for GDYN to scale and generate real profits and instead will entrust Endava to treat my hard-earned money with more respect.

NEW PORTFOLIO ACTIVITY

Bought: ZROZ

Thanks to a pitch made on Value Investors Club, I decided to act on purchasing ZROZ, an ETF that holds long-government discount bonds, meaning they are issued at a discount to par, do not pay interest over time, but instead increase in value until they mature at par. While I have been hesitant historically to own long-term bonds, but since interest rates have increased, the risk-reward to owning long-term bonds makes a little more sense. There is still significant risk if interest rates continue to increase significantly from here. With that said, this investment has the potential to act as a good hedge for the rest of the portfolio, and the insurance doesn’t cost anything up front. In fact, we earn a nearly 4% yield while we wait. Essentially, because this instrument has a ~25 year duration, it is most sensitive to changes in interest rates. The upward pressure on rates would be due to continued inflation, while rates would decline if the economy were to fall into recession and the Fed began reducing rates again. Obviously, if the economy were to decline, the remainder of the portfolio would be negatively impacted, and this investment would serve as a hedge. However, if the economy does not fall into recession and if inflation continues to increase, this investment could result in a negative return.

CONCLUSION

Ever the “pessimist”, there are things happening right now, mostly related to interest rates, that will take time to make their way into the economy, but when they do, I’m not sure the real economy or the stock market are ready for the drop in profits and multiples that is possible. Of course, Jerome Powell could step in and provide relief by cutting rates, but that possibility seems less likely given the still-high inflation the US is facing. Most companies were very smart to refinance their debt for record-long time periods at the lowest rates on record, so the pain of higher interest rates is likely to be delayed, much as it will be in housing, since so many people took advantage of low interest rates during the pandemic. It would take a recession and job losses for those people who financed at the best possible time in the last 50 years to give up their homes and realize the unrealized losses they might face if they sold today. Companies will face a reckoning if this interest rate environment holds, which most market participants seem content to ignore. Just make sure you’re accounting for higher interest rates on existing debt when underwriting new investments.

Until October,

Argosy Investors

Appendix

{kind=link}

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Argosy Investors Q2 2023 Letter