ARHS - Arhaus Is A Good Long-Term Prospect

2023-07-31 01:38:39 ET

Summary

- Arhaus is a premium retailer of home furnishings, offering a range of products.

- ARHS stock has experienced impressive growth but is expected to stabilize its revenues in the current year.

- I believe that Arhaus has long-term growth potential that the stock's current price isn't pricing in.

Arhaus Inc. ( ARHS ) is a premium retailer in home furnishings. The company provides customers with furniture, lighting, textiles, décor, and outdoor assortments. Arhaus has had impressive growth in the last years, but with a cooldown after a Covid-spike in the furniture industry, Arhaus is set to stabilize its revenues in the current year. I still believe the company has potential to create shareholder value with long-term growth, which is why I have a buy-rating for the stock.

The Company

Founded in 1986, Arhaus sells furniture in a premium segment in the United States; for example, a sideboard sells for $2799 on sale on the company's website. The company offers a wide variety of products.

Currently Arhaus is trying to grow brand awareness through showrooms, as the company's CEO explains in their Q1 earnings call:

As we discussed with you when we reported last quarter, our focus in 2023 is investing in the long-term growth in showrooms and systems that will fuel that growth, while at the same time continuing to prioritize product, building brand awareness and putting our clients first."

This seems to be a rational decision by the company's management, as discussed in the next chapter through financials.

Financials

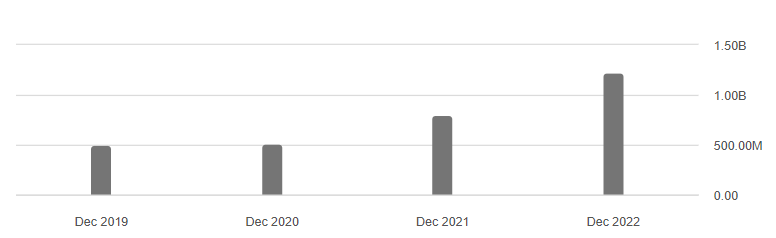

The company's public financial information only goes back to 2019, as the company had an IPO in November of 2021. Arhaus has had phenomenal growth in its recent history, as revenues have grown at a compounded annual rate of 35.4% from 2019 to 2022:

{kind=link}

For the current year the company has guided revenues of $1240 million to $1300 million, with the middle point representing a growth of 3% - growth seems to be tapering off at least for the current year. Arhaus wants to move cautiously through the currently turbulent macroeconomic environment, as they cement their brand and build a foundation for better brand awareness:

Our outlook reflects the expectation that we will continue delivering our backlog through 2023, achieve a demand comp range of negative 1% to up mid-single digits and carefully manage our expenses even as we continue to invest in growth, including new showroom, marketing, product development and investments to enhance omnichannel and technology capabilities including information technology and systems infrastructure, all of which are expected to accelerate brand awareness, support growth and generate efficiencies from scale."

I believe that the company's analysts underestimate Arhaus' long-term growth potential - consensus estimates only point towards a revenue growth of around six percent in both 2024 and 2025.

Due to being in the premium segment, Arhaus has a good gross margin, that has grown in the company's recent history. Currently Arhaus' trailing gross margin stands at 48.8% . As the company's revenues have scaled, their operating expenses have gotten smaller compared to gross profit, resulting in a trailing operating margin of around 16 percent. As the company has communicated, further development should generate a greater foundation for efficiency, boosting Arhaus' margins; I believe the current operating margin to be at a somewhat sustainable level considering the company's investments, although it could be lower going forward as the company tries to scale its operations.

On the balance sheet side Arhaus has a cash balance of around $145 million , with seemingly no interest-bearing debt - the balance sheet shows some current liabilities, but they seem to be operative in nature and not interest-bearing. The company also has over $400 million in capital leases, which are also operative in nature.

Valuation

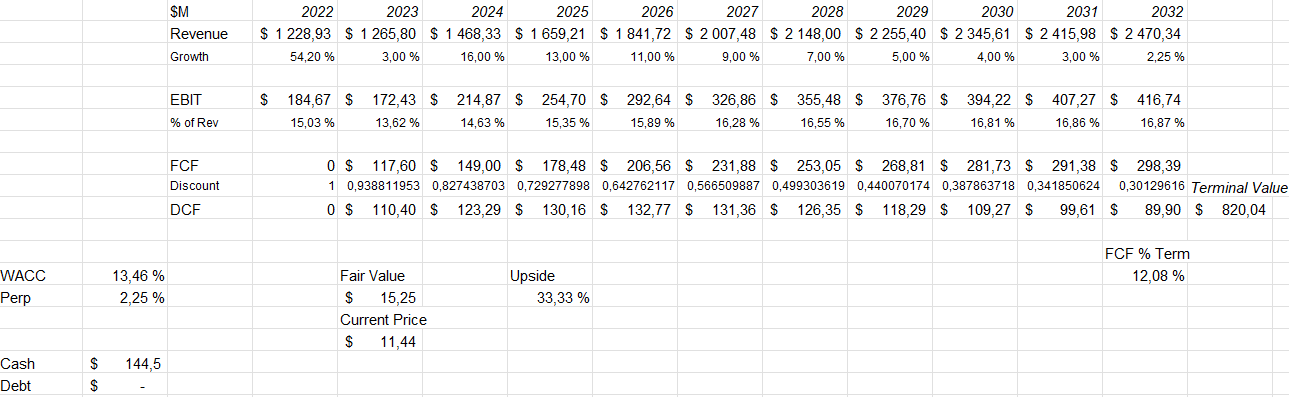

With trailing numbers Arhaus has a price-to-earnings ratio of 10.2, which I believe to not price in a big amount of growth. Taking a look at the company's valuation in terms of a discounted cash flow model, my estimates have the stock's estimated fair value at $15.23 - a 33% upside from its current price.

For the estimates, I have the current year's revenue in line with Arhaus' guidance. Going forward, though, I believe the company should grow its revenues faster than analysts currently expec t - with a historical CAGR of 35.4% and a temporary slowdown due to macroeconomic factors, the company's growth should in my opinion continue faster in 2024, which is why I'm estimating a growth of 16% instead of analysts' 6.2%. Going forward, I expect the growth to slow down slowly into a perpetual growth of 2.25% - a slightly higher growth than my usual expectation, as the company could still be growing.

On the margin side, I believe that Arhaus should have falling margins for the current year due to the current macroeconomic situation - I expect an EBIT margin of 13.62%, with that being around 1.41 percentage points lower than in the previous year. This margin should scale with time, though, as growth investments show themselves in gross profit and the company realizes scale benefits.

{kind=link}

The high weighed average cost of capital of 13.46% is derived from a capital asset pricing model:

CAPM of Arhaus (Author's Calculation)

The company currently has no interest-bearing debt as the company is still in a growing phase, and equity financing is a safer option. I estimate their potential interest for debt to be around six percent, with a debt-to-equity of 15% in the long-term.

I use the United States' 10-year bond yield as the risk-free rate, with the yield being at 3.84% at the time of writing. The used equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate made in July. Tikr estimates the company's beta to be at 1.81, a high figure due to the company's cyclical nature. Finally, I add a 0.5% liquidity premium into the cost of equity to compensate for possibly low liquidity. These estimates craft a cost of equity of 15.04% and a WACC of 13.46%.

Risks

Arhaus operates at a highly cyclical segment - furniture sales in general are quite cyclical in nature, and Arhaus itself operates in a premium segment - as customers' purchasing power falls, the company could be hit with rough times. This cyclical nature is also represented in the company's beta, as Tikr estimates the figure to be at 1.81.

As investors don't currently have visibility into the company's future growth rate, the company could be a significantly worse investment if future growth doesn't materialize; as showroom installations take up capital and grow expenditures, the company needs to have growth in order to cover the costs associated with these investments.

Takeaway

At $11.44, I believe Arhaus to be an investment that is worth looking into. As the company targets long-term growth with historically high margins, the company's valuation seems to have upside as my estimated DCF model presents. Although the company could be hit with a rough period due to macroeconomic headwinds, this doesn't concern me too much in the long run.

For further details see:

Arhaus Is A Good Long-Term Prospect