ARIS - Aris Water Solutions: Impressive Quarter And Scalability May Push The Stock Price

2023-08-07 05:28:53 ET

Summary

- Aris Water Solutions recently reported impressive quarterly earnings, benefiting from a new agreement with a major oil and gas corporation.

- The company offers water management solutions in the Permian Basin, reducing costs and pollution for energy companies.

- Expectations include positive free cash flow in 2024 and 2025.

Aris Water Solutions, Inc. ( ARIS ) recently delivered impressive quarterly earnings results a few months after the company signed a new agreement with a massive oil and gas corporation. I think that the company will most likely benefit from the production growth expected in the Permian Basin but may also experience FCF margin growth from promised scalability and cost management improvements noted recently. Yes, there are some risks, however I believe that demand for the stock and beneficial expectations may push the price up in the coming years.

Aris Water Solutions

With a presence in the service markets for the solution of environmental problems and focused on the management of the water and carbon footprint in industrial processes, Aris Water Solutions presents itself as a company with its activities focused on customers in the Permian Basin in the United States. The services offer a complete water management cycle, from use to waste, which significantly reduces costs and pollution for energy companies.

Aris has sufficient infrastructure to participate in large-scale processes and its own research and development areas to include high value-added technologies within its management processes. With this in mind, I believe that readers may understand why large corporations work with Aris. Some of its main clients in this region are ConocoPhillips ( COP ), Mewbourne Oil Company, Inc., and Chevron Corporation ( CVX ) or some of its subsidiaries.

The operations are organized via a single business segment, in which the activities of water solutions and management are distinguished. The management area is in charge of the collection, transport, and distribution of water produced through oil and petroleum processes. The company signs long-term contracts for these services, where a minimum amount is evaluated to maintain the appreciation margins on profit for the company.

On the other hand, the water solutions section develops and operates recycling infrastructures for its clients' energy production plants. Aris has its own pipes and supply circuit, which allows it to collect wastewater from several of its clients as well as to carry out large-quantity recycling processes, thus helping to reduce costs. In some cases, in order to meet the volumes agreed with its customers in the return, Aris mixes this recycled waste with non-potable water from underground, and in some more extreme cases, to complete these numbers, it buys water from third parties.

The company currently has more than 150 contracts open with 40 different clients. By the end of 2022, the average duration of the contracts was 8.3 years, ensuring operations in this regard for the next decade.

The Quarterly Income Statement Included A Significant Increase In The Operating Income As Well As Net Income Increase

I believe that the market appreciated quite a bit the most recent quarterly earnings release, so I took some time to understand what management gave to investment analysts. One day after the earnings, the stock price spiked up as analysts had a look at the new figures.

Source: SA

The new income statement included a significant increase in net sales in the quarter ended June 30, 2023. Quarterly net sales stood at $96.64 million, 26% more than that in the same period in 2022. Operating income also increased to close to $19 million from $11 million in the three months ended June 30, 2022. Finally, the quarterly net income attributable to Aris increased from about $1.3 million to about $4.6 million.

Source: 10-Q

I believe that it is fair to make a small comment about different share classes reported by Aris. Investors can buy class A shares from the market. However, there are also class B shares. With this in mind, analysts running FCF models will need to take into account that only a fraction of the future free cash flow will be received by class A shareholders. It is not ideal.

Source: 10-k

Expectations Include Positive FCF In 2024 And 2025

Considering the impressive results delivered in the last quarter, I took some time to review the expectations given by other market analysts. Experts in the field believe that Aris could deliver net sales growth in 2024 and 2025 along with positive net income. Besides, the company would deliver positive FCF in 2024 and 2025, which I think could bring significant attention from new investors. As a result, the demand for the stock could creep up.

Source: MarketScreener

Balance Sheet

As of June 30, 2023, the company reported cash worth $4 million, accounts receivable close to $66 million, accounts receivable from affiliates of close to $27 million, and total current assets worth $129 million. The ratio of total current assets/current liabilities stands at about 1x, so I would say that liquidity may not be an issue.

Long term assets included property, plant, and equipment close to $890 million, intangible assets of $250 million, goodwill worth $34 million, and total assets close to $1.332 billion. The asset/liability ratio stands at close to 2x, so I believe that the balance sheet of Aris stands in good shape.

Source: 10-Q

I would not be worried about the total amount of liabilities. Accounts payable would be close to $36 million, with payables to affiliates of close to $2 million, accrued and other current liabilities worth $73 million, and total current liabilities of $112 million.

Besides, with long-term debt of close to $423 million and asset retirement obligation of $18 million, total liabilities were equal to $663 million.

Source: 10-Q

I did review the amount of money paid for the debt because the net debt does not seem small. Aris pays close to 7.625% for senior notes. With this in mind, I felt comfortable using a WACC of 10% in my DCF model.

Source: 10-Q

DCF Model

Aris Water Solutions directs its efforts towards the growth of its business flow within the region where it concentrates its operations. Regarding the expansion of its businesses, at the moment its sights are set on attracting clients in the area of ??transportation and water management. Considering that large clients already trust Aris, I assumed that management will easily find new customers, which may enhance future FCF growth.

In this sense, Aris's business strategy is to have close relationships with companies and regional communities, providing knowledge and dissemination services on the importance of its services. I believe that further investments in marketing and information about the services offered will most likely continue to bring revenue growth. It is also worth noting that Aris will most likely maintain great communication channels with other clients because the executive chairman and other members of the team are well connected to other boards.

Bill served on the boards of numerous portfolio companies, including Gulf Atlantic Operations, Kitimat LNG, Freebird Gas Storage, Cadre Proppants, MS Energy Services and Greene’s Energy Group. Previously, Bill held the role of Senior Vice President and General Manager at Dynegy Inc., building and managing the natural gas liquids business. Prior to that, he held the roles of Feedstock Trading Manager and Business Analyst at Dow Hydrocarbons and Resources. Source: Aris Water Solution Bill Zartler

With regards to agreements with large corporations, I believe that after the agreement signed with XOM in 2023, many other large players will be interested in Aris’ solutions.

In January 2023, Exxon Mobil Corporation ( XOM ) joined our strategic agreement with Chevron U.S.A. Inc. and ConocoPhillips to develop and pilot technologies and processes to treat produced water for potential beneficial reuse opportunities. Source: 10-Q

I am very optimistic about the words of management about new cost effective and scalable methods of treating produced water. Under my DCF model, I assumed that scalability and lower efficiency will most likely drive FCF margins north.

Our goal under the strategic agreement is to develop cost effective and scalable methods of treating produced water to create a potential water source for industrial, commercial and non-consumptive agricultural purposes. Source: Source: 10-Q

I also believe that the company will most likely benefit from the Permian Basin oil and associated water production growth, which is expected to outpace production growt h in other parts of the United States. Yes, Aris depends quite a bit on the development of the Permian Basin, however in my view, management is working in a very good spot for the coming years.

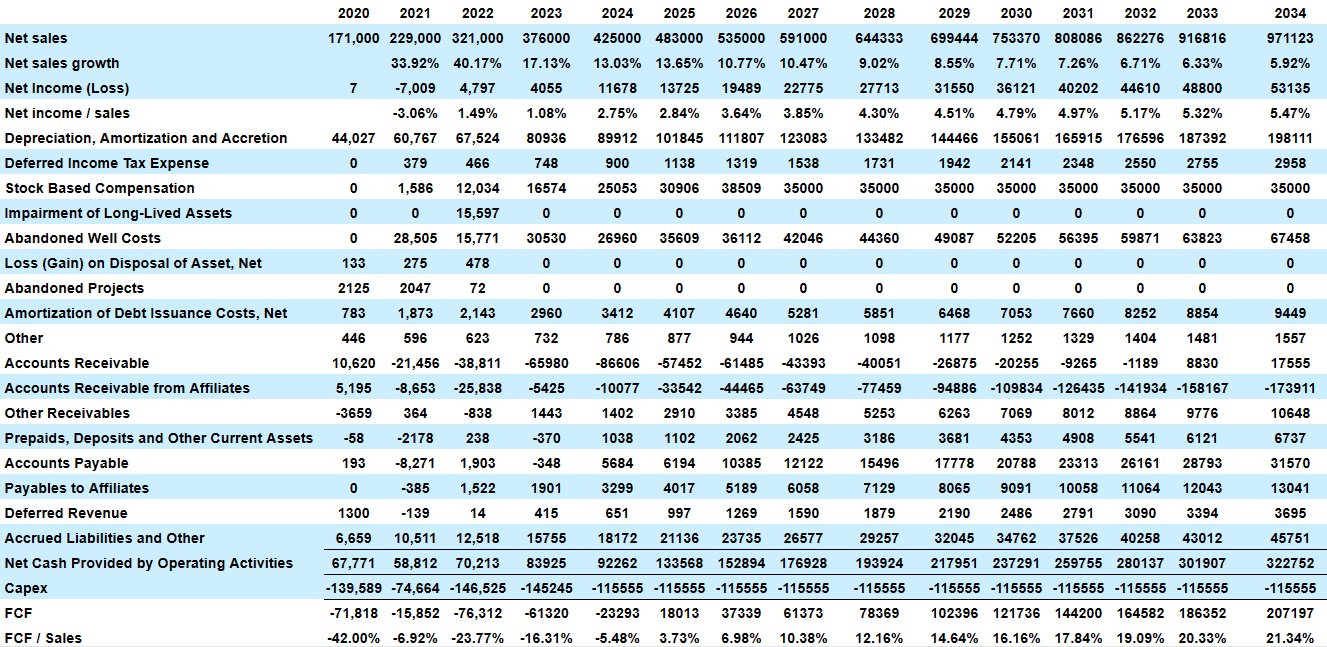

My expectations include net sales growth around 10% and 5% from 2026 to 2034 and net profit margin close to 2%-5%. 2034 Net sales would stand at about $971 million, with 2024 net income close to $53 million and net profit margin of 5.47%.

Source: My DCF

My financial model also included 2034 depreciation, amortization, and accretion worth $198 million, with deferred income tax expense worth $2 million and 2034 stock based compensation of $35 million.

If we also include accounts receivable close to $17 million, accounts receivable from affiliates of about -$174 million, and changes in accounts payable worth $31 million, net cash provided by operating activities would stand at about $322 million. Finally, with capital expenditures of -$116 million, 2034 FCF would be close to $207 million.

Note that my figures include FCF/Sales close to 3%-21%, which I believe is conservative. I also did not include extraordinary items like abandoned projects, gains on disposal of assets, and impairment of assets for the calculation of the CFO.

{kind=link}

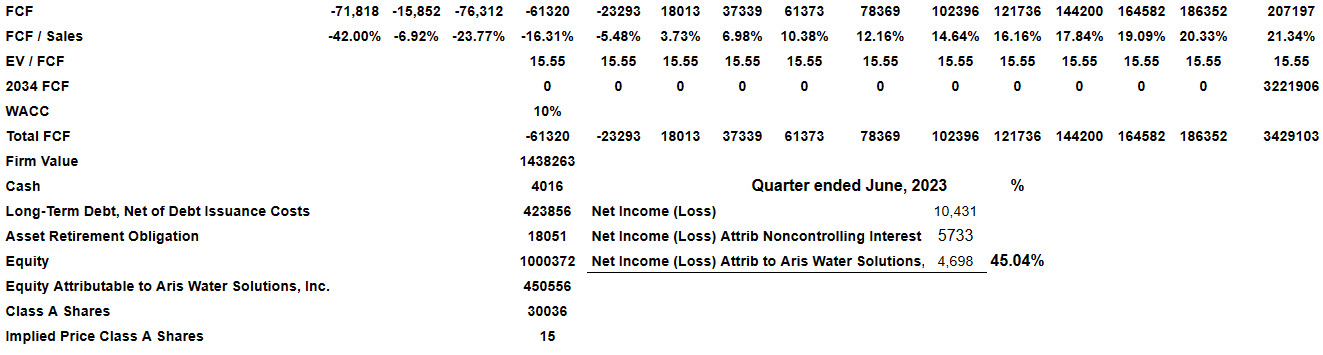

Most analysts are expecting EV/FCF close to 19x-16x in 2024 and 2025, so I tried to be a bit conservative than other investment analysts and used a terminal EV/FCF close to 15.55x.

Source: MarketScreener

With a WACC of 10%, the implied firm value would be close to $1.438 billion. If we add cash of about $4 million, and subtract long-term debt of $423 million and asset retirement obligation worth $18 million, the implied equity would be about $1000 million. Now, taking into account the equity attributable to Aris and the total number of class A shares, the implied price per Class A share would be $15 per share.

{kind=link}

Competitors

Competition in this region is given by public or private companies with similar activities, internal developers in their client companies, and the possibility that they develop their own management and recycling cycles. In this sense, the competition is given by the ease of the facilities, the price of the services, and the recognition of the brand support within the market. In any case, Aris's quest to grow the waste management and water transport sector may lead to new competitive instances for which the company has not yet developed forecasts.

Risks

Aris's business depends directly on the development and capital expended by the energy industry within the region where it operates. The volatility of market prices as well as the lack of updating of rates in contracts signed in the past are also risks.

Regarding the development of its infrastructure and managing its growth in the short term, Aris encounters a series of group and individual rejections mainly coming from the nearby communities regarding the expansion of its pipelines. This could directly affect the strategy regarding wastewater management and transport area.

Regarding the risk associated with the concentration of its clients, it is necessary to mention that the three main clients concentrated more than 55% of Aris's activities in 2022. Specifically, ConocoPhillips accounted for around 35% of the company's such revenues in recent years. Due to the risk of termination of contracts, the risks that directly affect its clients, and the geographical concentration of its operations, these data are not very encouraging for new investors, resultantly reducing access to financing lines for future business and infrastructure developments.

Ultimately, although not directly, Aris is conditioned by a series of laws that fall on its clients in relation to contamination and waste traces. If the operations of some of its main clients suffer due to the enactment of new laws, the company's capital circuit could be altered.

Conclusion

Aris recently delivered impressive quarterly net income growth, a few months after Exxon Mobil Corporation joined Aris’ strategic agreement with Chevron U.S.A. Inc. In my view, the company will most likely benefit from production increases in the Permian Basin in the United States. Also, with improvements in scalability and efficiency promised by management, I think that we can expect significant FCF margin improvements in the coming years. Even assuming risks from the geographical concentration of its operations or the total amount of debt, my DCF implied that Aris appears undervalued.

For further details see:

Aris Water Solutions: Impressive Quarter And Scalability May Push The Stock Price