RVLV - Aritzia: Bringing Everyday Luxury To Your Portfolio

2023-12-21 07:32:53 ET

Summary

- Aritzia is a Canadian fashion house operating in the "everyday luxury" space, with revenue of over $1.64 billion and a market capitalization of $2.10 billion.

- The company has a combination of physical boutiques and a growing e-commerce presence, with online sales accounting for up to 50% of revenue during the pandemic.

- Despite attractive growth in recent years, slowing growth and rising costs are a concern, and Aritzia stock is reasonably priced compared to similar firms. A "hold" rating is recommended.

Generally speaking, I don't do much with the fashion space. It might have to do with the fact that I have been told many times that I have no sense of fashion. But it is also due definitely to my view of just how difficult and competitive the market is. Margins can be low and the companies in this space deal with a feast or famine lifestyle, with them feasting when consumers are happy and with them suffering famine when the hype around a brand declines. But every so often, a firm in this space will catch my eye and I will perform an analysis of it and gauge its potential. In this instance, the firm in question is Aritzia ( OTCPK:ATZAF ), a Canadian fashion house with sales both up there and down here in the US.

The company has achieved rather significant growth in recent years, though some of its profitability metrics have been a bit volatile. Growth is definitely slowing now, though management does have high hopes for what the next few years will bring. The stock is not particularly expensive. In fact, in many respects, I would consider it cheap. But because of how other shares are priced and the space in which it operates, I would argue that an additional margin of safety is needed. It's because of that thinking that I have decided to rate the business a ‘hold’ for now. Though if financial performance does pick up or if shares get cheaper, my mindset on the matter could change.

A necessary note

As I mentioned already, Aritzia is, first and foremost, a Canadian company. The firm’s financial statements are even quoted in Canadian dollars as opposed to US dollars. Given that my primary audience is based in the US and that a search for the company's stock price will likely yield the US listing, I have decided to convert all financial figures into their US equivalent using the current exchange rate. Any exceptions to this will be shown as CDN$ with the specific Canadian dollar amount attached to the end of that string.

An interesting firm that’s in fashion

{kind=link}

According to the management team at Aritzia, the company is not exactly a luxury provider of fashion products. In fact, it's not even in the sub luxury market. As you can see in the image above, the firm believes that it fits in what is known as the ‘everyday luxury’ space, right above the mid-market category and below the sub luxury market. Being true to itself has paid off in its life, as evidenced by the fact that, from 1984 through today, the company has grown to be a rather significant participant in this space. Revenue in the 2023 fiscal year was just over $1.64 billion and the company boasts a market capitalization of $2.10 billion.

{kind=link}

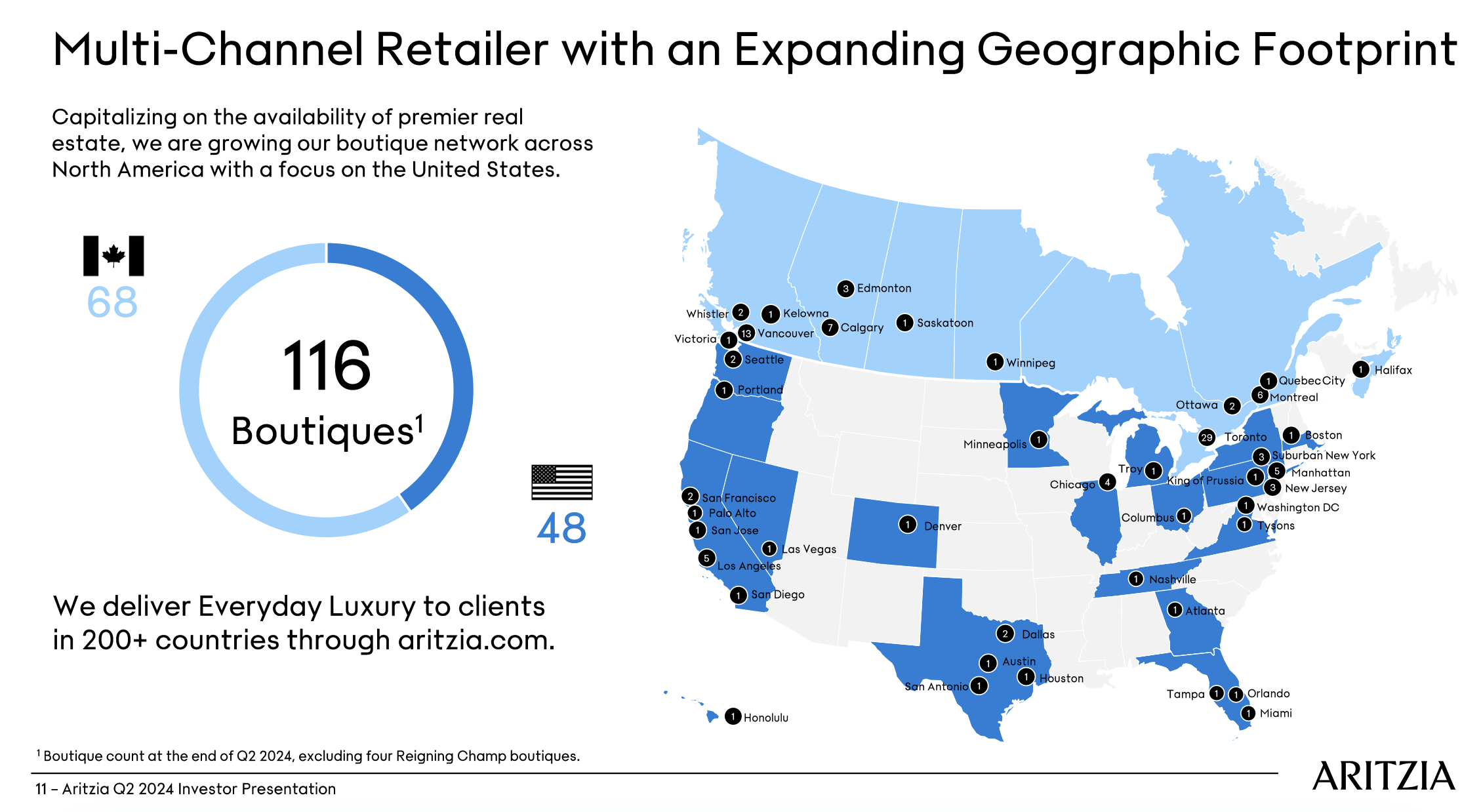

There are multiple ways in which management gets its product offerings to its customers. For starters, the firm has 116 boutiques in operation, 68 of which are located in Canada while the remaining 48 are here in the US market. Even though I came into analyzing the company with certain preconceived notions, those notions ended up being wrong. I figured that this would have been a strictly East Coast and West Coast sort of business so far as the US market is concerned. And it is true that the company does emphasize those regions. For instance, ten of its locations are spread throughout parts of California. It also has locations in Las Vegas, Portland, and Seattle. The firm has 8 locations between New York City and suburban New York. And it also has three in New Jersey as well as one in Boston. However, the firm also boasts five different locations in Texas, one in Denver, four in Chicago, and even one in my home state of Ohio. In Canada, it even boasts locations and areas that I wouldn't expect either, as the map above illustrates.

As with pretty much any company these days, or at least any company that sells a physical product in a retail setting, retail is not enough to truly capture fantastic growth. Management also has been working hard on establishing a meaningful ecommerce presence for the company. From 2016 through 2020, the company reported ecommerce revenue growth of 36% per annum. Growth has continued to be impressive since then, with as much as 50% of its revenue coming from online sales during the pandemic year of 2021. That number has since dropped as the company has seen a rise in the number of boutiques and as shoppers have returned to coming into the store to try on their items before buying. For the 2023 fiscal year, even though ecommerce revenue grew by 36% year over year, total ecommerce revenue dropped from 38% of sales the year prior to 35%.

{kind=link}

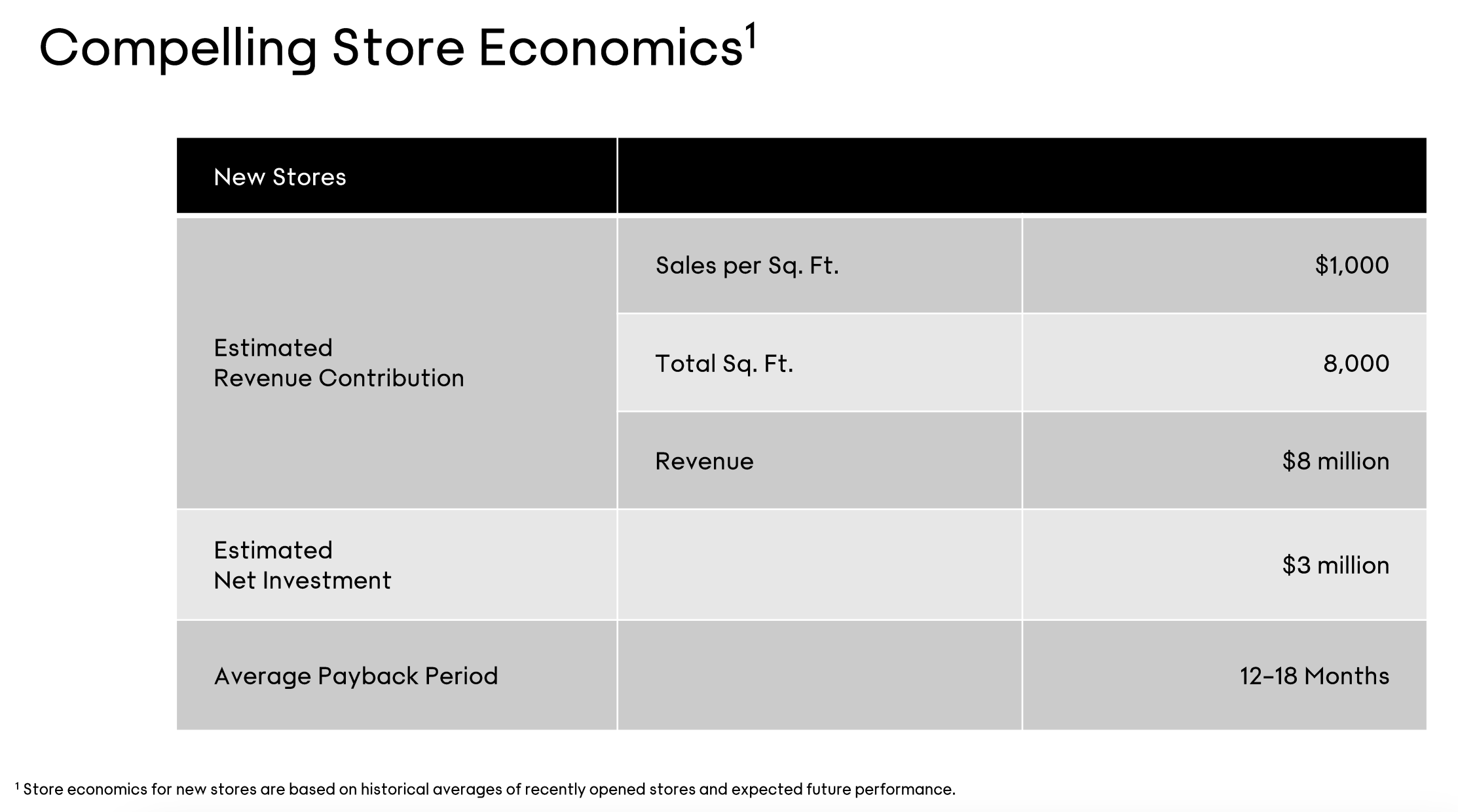

Even though ecommerce has proven to be a true boon for the company from a revenue growth perspective, management does not expect to stop building boutiques any time soon. In 2023, the firm added eight new boutiques to its network. And this year alone, it plans to add another eight. In addition to this, it also intends to make investments in order to expand for others. This is because the economics associated with physical stores makes sense for the company. The average new location costs about CDN$3 million to set up. They are about 8,000 square feet in size and generate around CDN$8 million a year in revenue. When all the math is said and done, the average store takes between 12 months and 18 months for the company to make its investment back on. So that implies profitability of between CDN$167,000 and CDN$250,000 each month.

{kind=link}

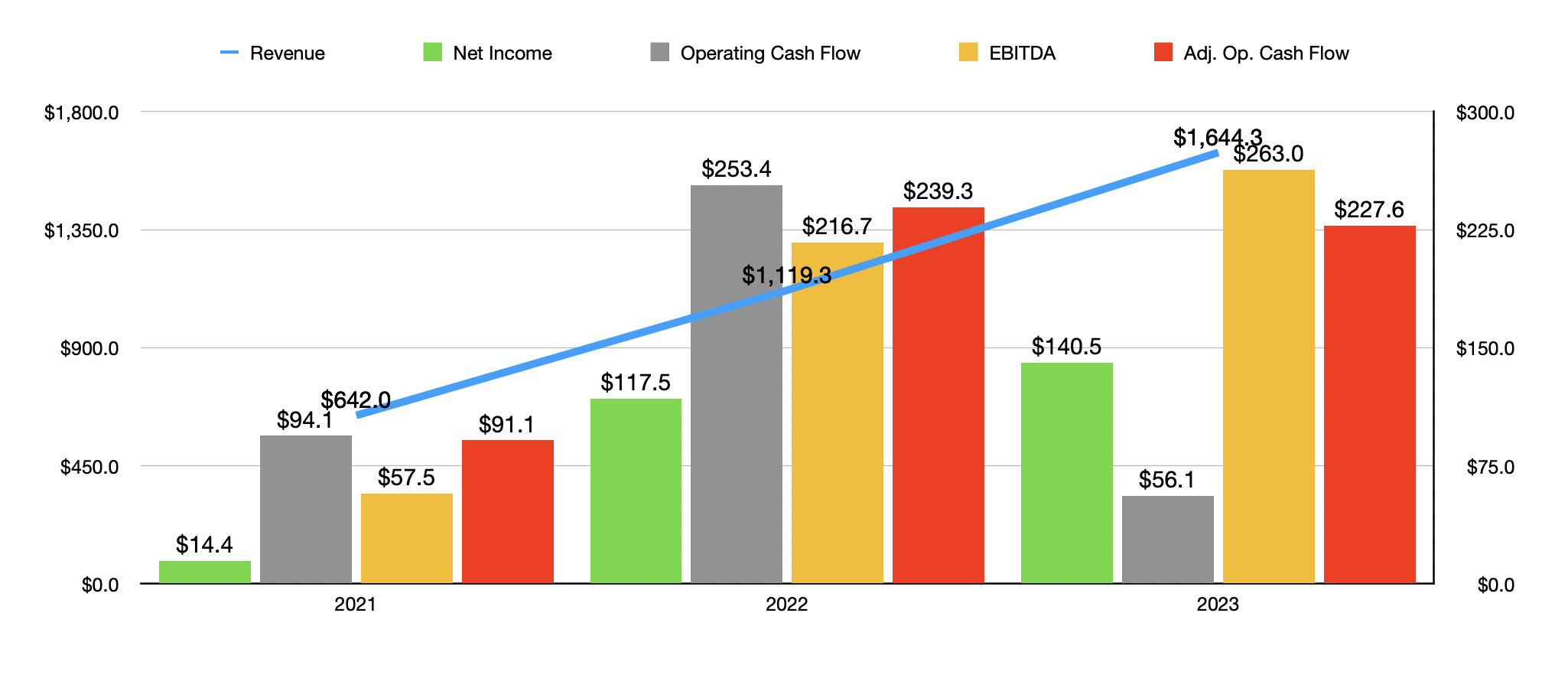

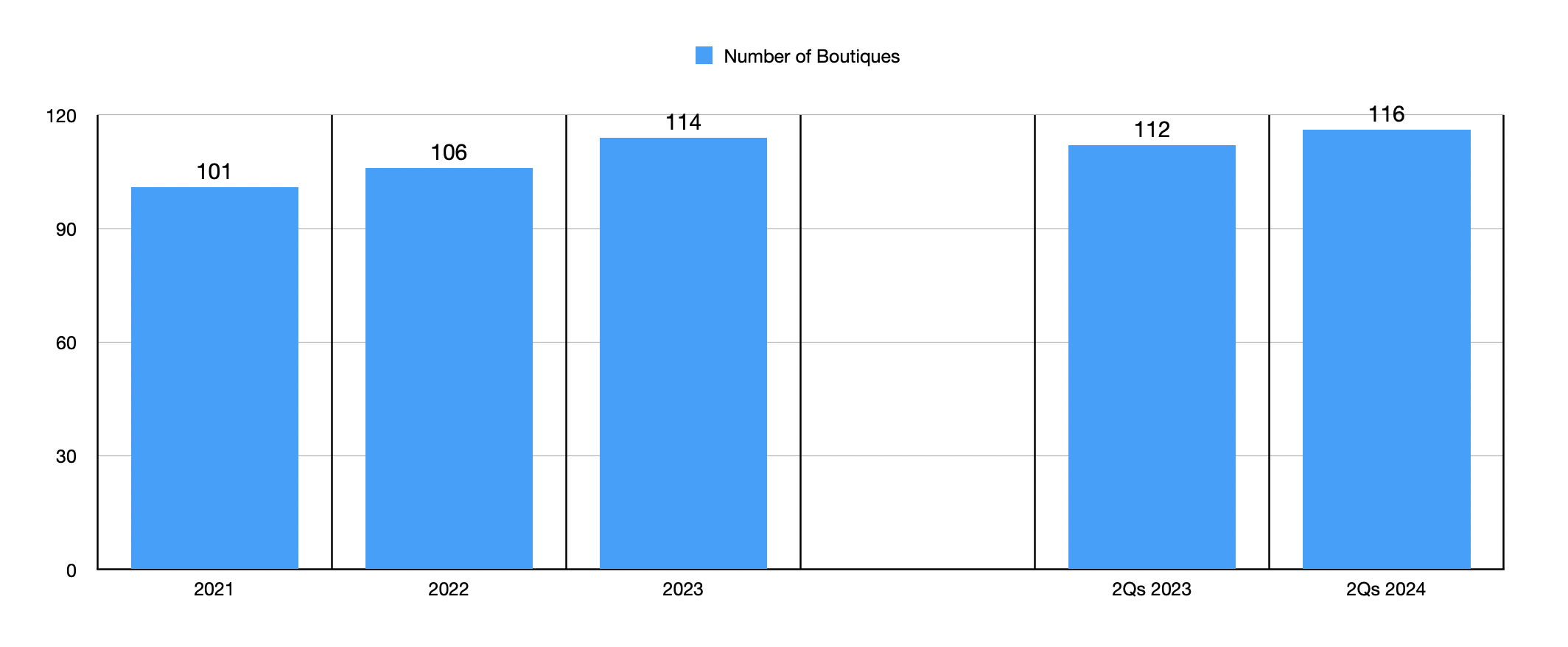

Using its omni-channel approach, Aritzia has grown from generating $642 million in revenue in 2021 to $1.64 billion in 2023. Again, some of this has been driven by a rise in the number of boutiques from 101 locations to 114. We also had a surge in activity back to the boutiques following the worst days of the pandemic. But on top of this, we have the aforementioned online sales that played a role in this expansion. As revenue rose, profitability followed suit. Net profits skyrocketed from $14.4 million to $140.5 million. As you can see in the chart above, operating cash flow has been very volatile. But if we adjust for changes in working capital, we would see an increase from $91.1 million to $227.6 million. Meanwhile, EBITDA for the company expanded from $57.5 million to $263 million.

{kind=link}

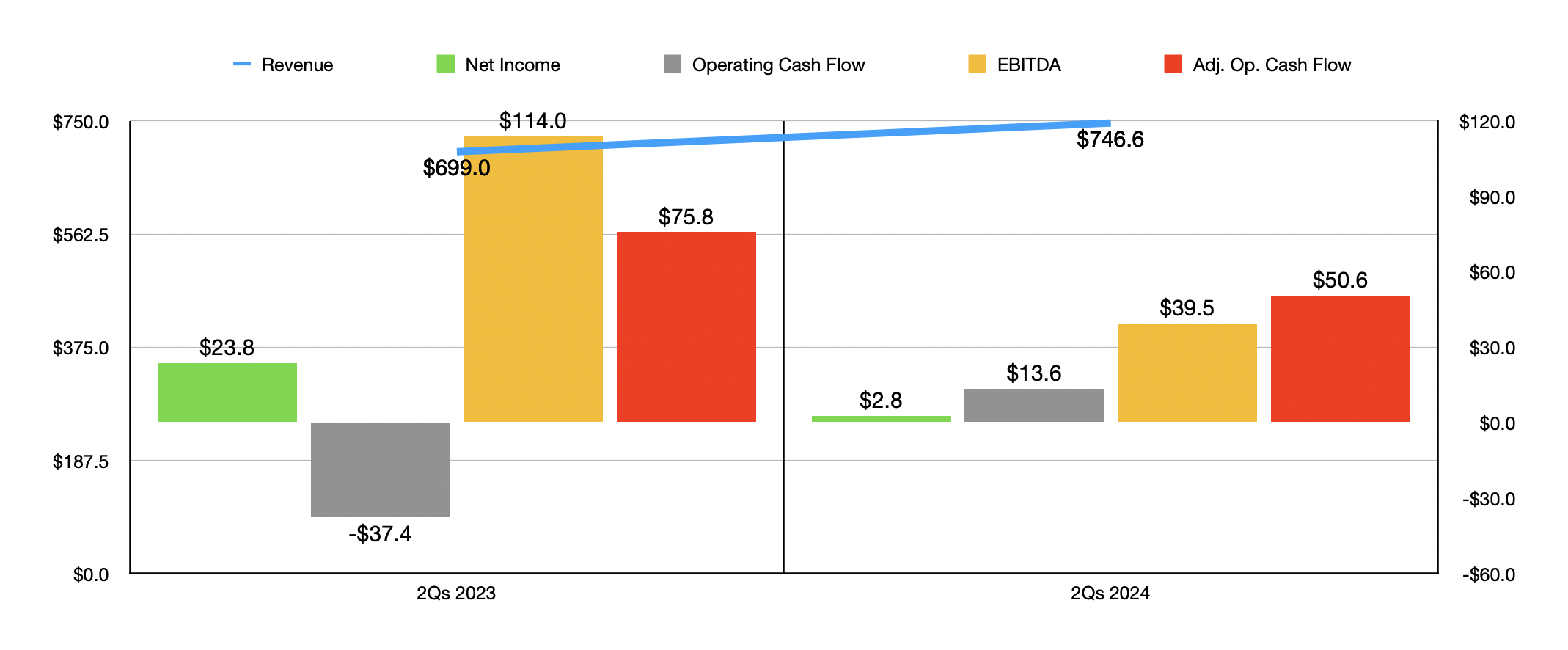

Financial growth has continued into the current fiscal year. Revenue in the first half of 2024 totaled $746.6 million. That's up nicely from the $699 million reported the same time of 2023. However, rising costs pushed net profits down from $23.8 million to $2.8 million. Despite the growth in sales, the company saw its gross profit margin contract from 43% to 36.8%. This was driven largely by inflation associated with the products that the company sells. A normalization of markdowns, as well as temporary warehousing costs associated with changes in inventory management, on top of expenses related to the firm’s new distribution center, on top of multiple other factors, all played a role in bringing this down. On top of all of this, selling, general, and administrative costs, skyrocketed 21.4% in the first half of 2024. Increased wages on the retail side of things, as well as ‘support’ for office labor, were largely responsible.

{kind=link}

Some of these costs, such as the labor related ones, look to be pretty sticky to me. That could be problematic for the company in the long run, though it is likely that some of these other costs are transitory. Regardless, they are problematic because they have also been responsible for bringing down other profitability metrics. Operating cash flow for the company improved during this window of time, but both the adjusted figure for that and EBITDA reported significant weakening year over year. This also brings into question, especially when looking at sales forecasts for next year, whether the company can come even remotely close to its near-term growth target.

You see, management's goal that was set out in October of 2022 was to see the company expand to generate between $2.62 billion and $2.85 billion in revenue in 2027. That implies an annualized growth rate of between 15% and 17%. To put this in perspective, management is now forecasting revenue for 2024 of between $1.69 billion and $1.76 billion. At the midpoint, this would be $1.72 billion, which would be only 4.6% above what was seen in 2023. What's more, management is targeting an EBITDA margin of 19%, which, at the midpoint, would translate to EBITDA of $519.7 million by 2027. That's a near doubling from what was seen in 2023.

{kind=link}

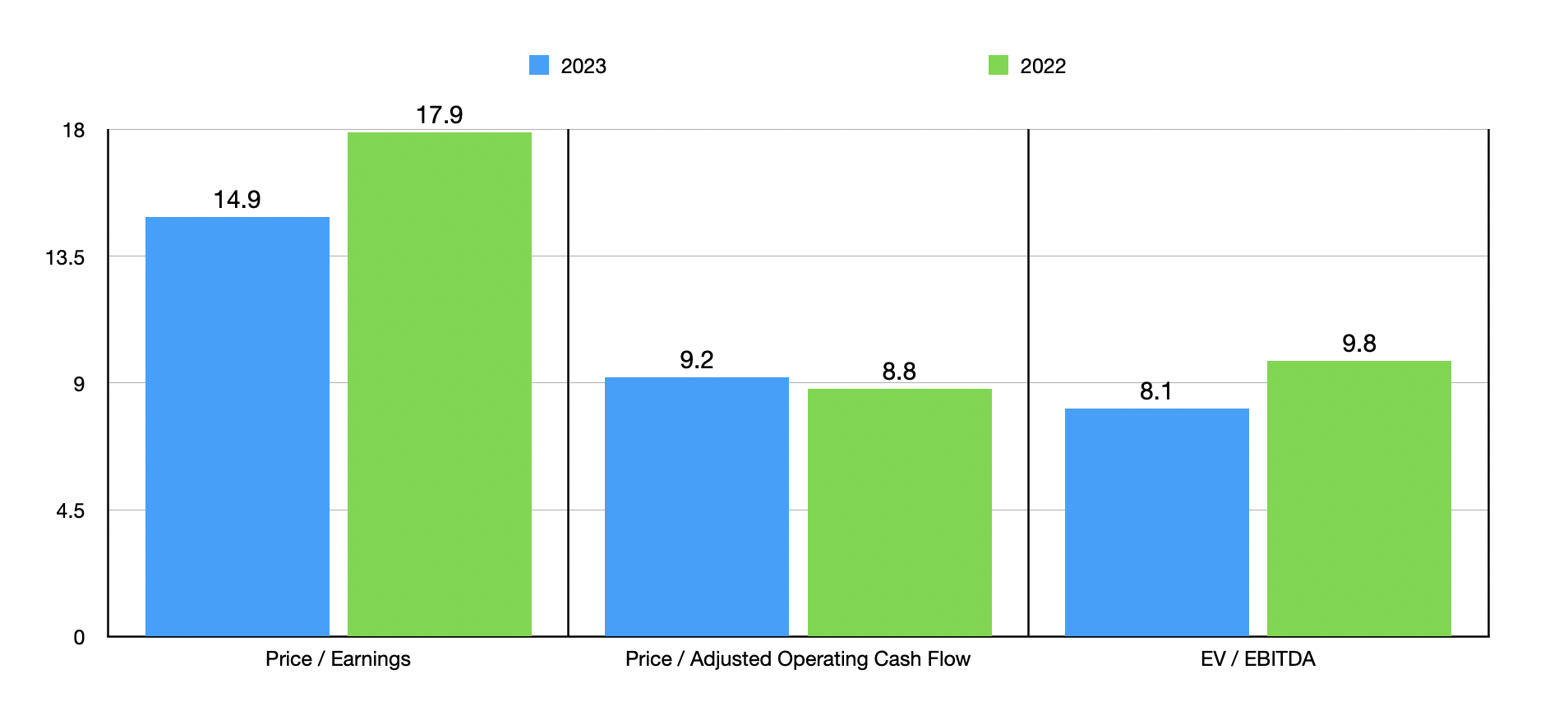

Using the results from 2023 and from 2022, I was able to value the company as shown in the chart above. Although the stock looks a bit lofty perhaps from a price to earnings perspective, it looks considerably more reasonable when it comes to the cash flow metrics. If we take the 2023 figures and compare the business to five similar firms, however, we see that shares are not priced at levels that are all that impressive. Using both the price to earnings approach and the EV to EBITDA approach, I found that two of the five companies that I compared it to are cheaper than it. This number increases to three of the five using the price to operating cash flow approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Aritzia |

| 14.9 |

| 9.2 |

| 8.1 |

| Victoria's Secret & Co. ( VSCO ) |

| 22.3 |

| 4.0 |

| 6.9 |

| Buckle ( BKE ) |

| 10.0 |

| 9.1 |

| 6.5 |

| Boot Barn Holdings ( BOOT ) |

| 14.3 |

| 7.8 |

| 8.7 |

| Foot Locker ( FL ) |

| 38.2 |

| 28.1 |

| 9.0 |

| Revolve Group ( RVLV ) |

| 40.9 |

| 36.8 |

| 30.2 |

Takeaway

As things stand right now, I definitely think that Aritzia is an interesting business. But I certainly am not going to buy any shares at this point in time. Management has achieved attractive growth in recent years, but growth looks to be slowing and costs are proving to be problematic. The stock looks reasonably priced on an absolute basis, but is closer to fair value when it comes to similar firms. Given these facts, I do believe that a ‘hold’ right hand makes the most sense for the business at this point in time. However, if we can see some nice progress on achieving those 2027 goals, particularly on the bottom line, it wouldn't take much for me to upgrade the stock to a ‘buy’.

For further details see:

Aritzia: Bringing Everyday Luxury To Your Portfolio