ARKAF - Arkema: Entering Oversold Territory

2023-06-10 23:14:28 ET

Summary

- Arkema remains in the midst of a cyclical downturn.

- The stock has not been spared, underperforming by a wide margin over the last year.

- But with the valuation down to excessively cheap levels, investors willing to stick it out through the near-term headwinds could come out ahead.

Global specialty materials company Arkema SA (ARKAY) (ARKAF) has been punished this year amid fading China reopening hopes, as well as weakness across its key end markets. While Q1 outpaced a low bar, helped by relatively resilient results across its core divisions, the stock remains well off last year’s highs and, perhaps more importantly, has underperformed the broader French index (up mid-teens% over the last year). With the valuation now down to ~5x EV/EBITDA (~4x fwd), however, Arkema may be entering oversold territory. Besides delivering on its organic growth potential, the company is still levered to secular ESG themes like electric vehicle batteries, while its strong balance sheet allows for compelling M&A optionality. Expect more acquisitions like Ashland’s ( ASH ) Performance Adhesives unit (+2.2%pts contribution to Q1 2023 sales) in the coming years as management accelerates the transition into a pure-play specialty materials unit. And as the battery destocking cycle enters its final stages, investors willing to stick it out for a few quarters stand to be well rewarded, in my view. The well-covered ~4% yield means investors also get paid to wait.

Few Surprises as the Cyclical Downtrend Continues in Q1

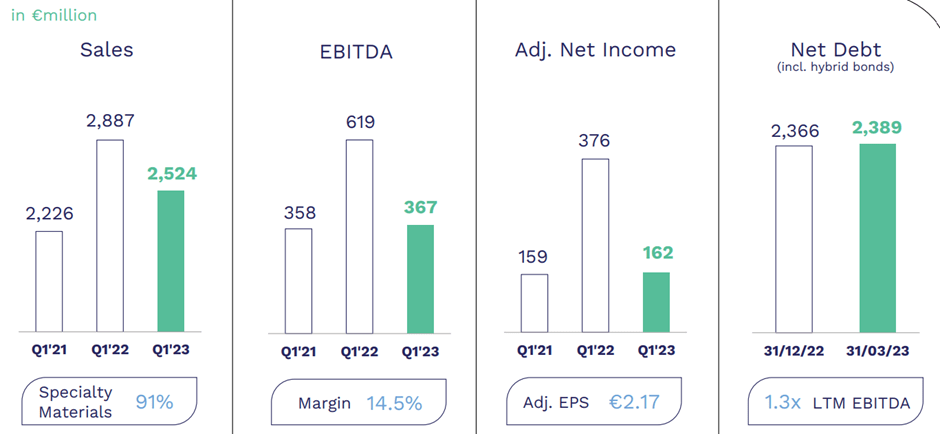

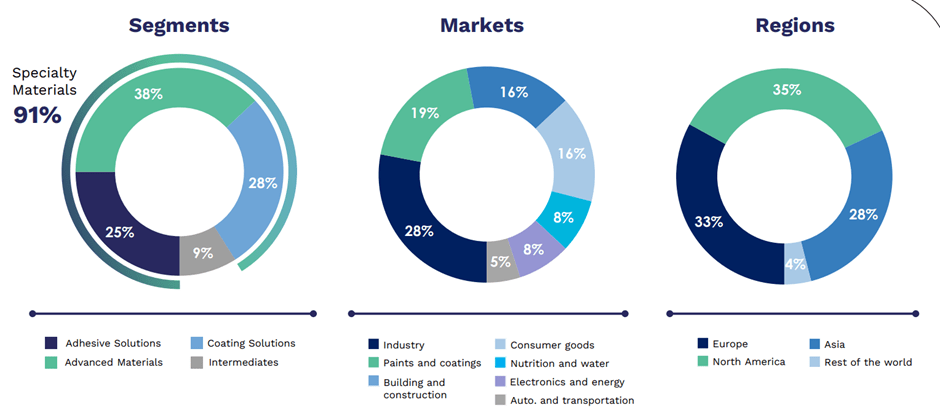

Arkema unsurprisingly reported another quarter of declining volumes across its core businesses, with the demand weakness from last year extending into Q1 2023 as well. Slower Europe construction activity was the main detractor, along with a slowdown in the US. By segment, adhesive solutions (28% sales contribution) was the outperformer at +4.2% revenue growth, helped by a +6.7% YoY price hike (-12.7% volumes; +10.0% scope from Ashland’s adhesives). A favorable mix shift towards more value-added solutions (“high-performance adhesive applications”) was the key revenue driver, helped by further synergy benefits from the Ashland Adhesive unit acquisition (integration on track with Arkema targets).

Elsewhere, the advanced materials segment saw a high-single-digit % price hike as well, though a 20.5% YoY decline in volumes more than offset any pricing gains. Like the >20% drop in volumes for the coating solutions segment, however, the headwinds were mostly related to temporary destocking activity in key end markets like Chinese batteries and should improve over time. Also weighing on volumes in advanced materials was the lack of a China reopening boost (recall management had previously hoped for some uplift in H1). As a result, overall EBITDA was down >40% YoY (~6.9%pt swing in margins to 14.5%), though the EUR367m in Q1 was still ahead of a low consensus bar.

{kind=link}

Arkema SA

Reaffirmed Guidance Implies a Better H2 Ahead

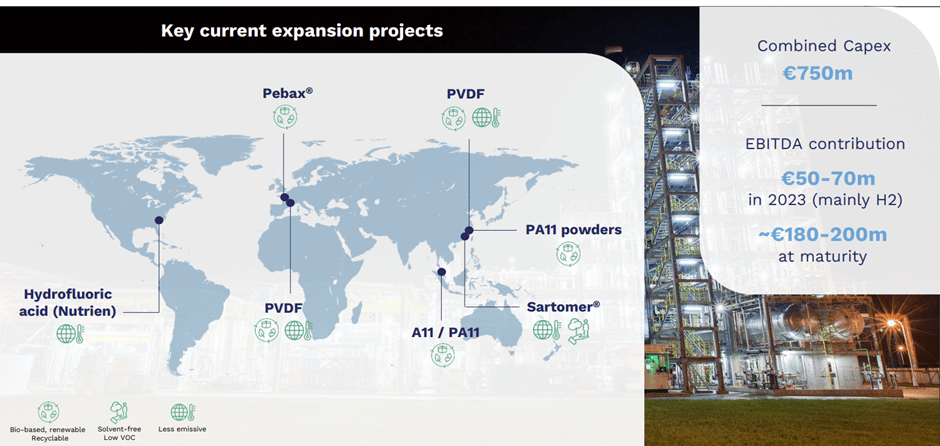

Arkema expects some reprieve from the macro weakness in Q2, though a meaningful upturn is only guided to kick in from H2 onward. Still, the company has kept full-year EBITDA guidance within the EUR1.5-1.6bn range (assuming no unforeseen macro disruptions ahead) and a relatively high EBITDA conversion ratio of >40%. The assumptions underlying this view seem reasonable - for instance, management expects the Chinese battery destocking cycle to wind down by H2 before a restocking cycle begins later in the year to boost volumes. Also in the pipeline are potentially high-return projects such as the polyvinylidene fluoride (abbreviated to PVDF, a key input for lithium-ion batteries due to its thermal stability and adhesive properties) capacity expansion in China and France. Alongside the ongoing Polyamide 11 capacity expansion in Singapore and Sartomer photocure resins capacity expansion in China, the EUR50-70m incremental EBITDA benefit (up to EUR200m at maturity) poses upside to the full-year numbers.

{kind=link}

Arkema SA

Another potential source of near-term upside is raw material costs. As management outlined in its outlook statement, costs have been easing for some time now, along with energy prices (though sanctions have kept these relatively high in Europe). The post-Q1 path for energy prices appears to be to the downside - aggregate demand in Europe remains weak, as economic growth has slowed amid an extended ECB monetary tightening cycle and elevated consumer inflation. The US is relatively better positioned on growth and inflation, but recent PMI reports indicate its manufacturing activity is slowing. Also weighing on energy prices is the lack of a meaningful ex-consumption rebound in China, though management expects a broader recovery in H2, along with the end of its battery destocking cycle. Alongside supply-side headwinds (e.g., oil-producing nations like Russia and Nigeria have pushed back on cuts at last week’s OPEC+ meeting , while the UAE will be raising output), any near-term volume weakness could well be offset by easing cost pressures at the EBITDA line.

Long-Term Growth Intact Despite the Near-Term Headwinds

Since outlining its long-term goal of transitioning into a higher-margin specialty chemical materials company in 2020, the company has made several positive steps, including non-core divestments, to rebalance its portfolio. As of 2022, specialty materials now contribute 91% of business revenue (vs. 79% in 2019), but with margin expansion still in its early stages (18.1% margin for specialty materials vs. 30% for intermediates), the earnings growth runway remains extensive.

{kind=link}

Arkema SA

Backed by a strong balance sheet and ample M&A optionality following the YTD de-rating in the space, Arkema should easily complete the transition in 2024. The question from here is where margins eventually land once scale benefits fully kick in. With Arkema’s recent acquisitions placing the company in a better position to capture the electrification tailwind globally (accelerated by US and EU policies), I see more upside than downside over the long run. But in the meantime, the company will need to navigate the cyclical downturn amid global demand weakness and destocking in China. Pending visibility into an H2 recovery and China’s reopening broadening out beyond consumption, investor sentiment is likely to stay downbeat, presenting long-term patient investors with a compelling entry point at ~4x fwd EV/EBITDA and ~9x fwd P/E.

Entering Oversold Territory

Arkema closed out Q1 stronger than expected, with resilient results across its core divisions pushing EBITDA over consensus expectations. Progress on unlocking post-acquisition synergies from Ashland’s (Performance Adhesives unit) has also been encouraging. Equipped with ample liquidity to ride out the near-term volatility, along with more balance sheet headroom for M&A, the company looks poised to deliver on its long-term strategic shift toward specialty chemicals. While near-term headwinds from destocking and global demand weakness are material, the stock has likely priced in these negatives at ~4x EBITDA. Alongside the low valuation bar, investors also get a well-covered low to mid-single-digit % dividend yield; hence, the risk/reward on Arkema screens attractively here.

For further details see:

Arkema: Entering Oversold Territory