ARKO - Arko: Improving Operating Metrics But Expensive Reiterate Neutral

2023-10-05 02:37:43 ET

Summary

- Arko has improved its operational profile driven by the outperformance of its merchandise portfolio.

- It has reported resilient earnings in Q2 with improving leverage metrics, which has remained a cause of concern.

- ARKO trades at a premium to larger peer CASY, which has a more robust network and outsized operating metrics. Reiterate Neutral.

Investment Thesis

In continuation with our previous coverage of Arko ( ARKO ), we rated ARKO as a Hold driven by its improving operational profile and deleveraging balance sheet post the Travel Centers of America (TA) deal fiasco while its expensive valuation compared to its larger peer Casey's General Stores ( CASY ) providing a limited margin of safety. The stock has largely remained flat since the publication of the article, down ~3% vs. S&P's 1.5% decline. It reported sustained earnings in Q2 2023 driven by continued outperformance of its merchandise portfolio offset by the fuel segment. ARKO trades at a premium to CASY despite CASY's strong network and outsized operating metrics on the back of investor anticipation of ARKO's acquisitive boost to EPS and management targeting higher repurchases and dividends to drive shareholder value. However, we believe it provides limited margin of safety at current levels and we reiterate at Neutral.

Improving Earnings

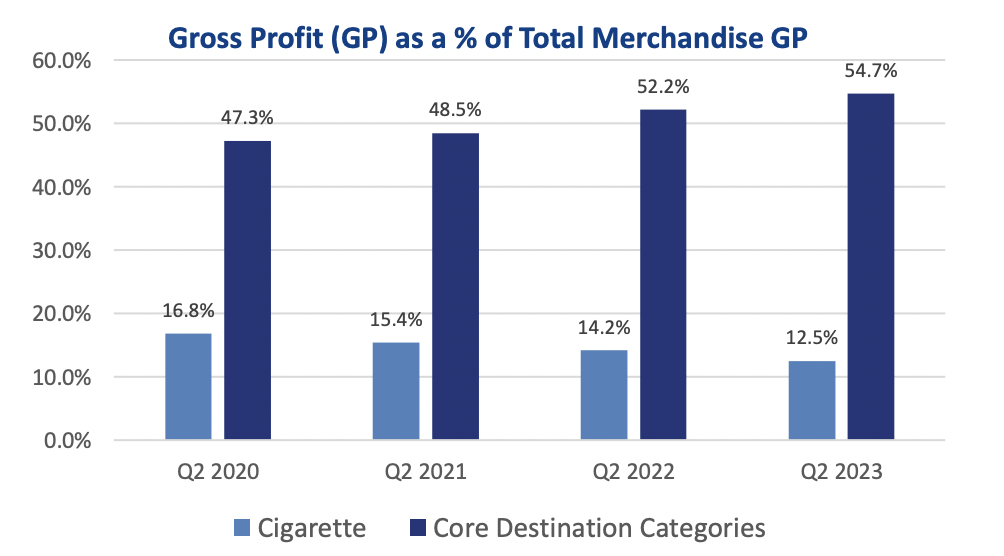

ARKO reported resilient Q2 earnings with same-store sales excluding cigarettes growing 3.8% YoY while same-store sales for cigarettes declined 5.7% YoY marking another quarter of resilient growth. The growth was driven by its continued growth was driven by outperformance in its core destination categories of candy and salty snacks which reported a double-digit growth while sweet snacks, beer, and alternative snacks reported mid-single digit growth. Sales from high-margin core destination categories continue to improve, contributing 64% of same-store sales growth excluding cigarettes.

Retail revenues decreased by 9.2% YoY primarily driven by a $0.95 decrease in average gas price per gallon along with 2.6% decline in same-store gas volumes, partially offset by the volumes from recently acquired entities which contributed ~$175 mn in revenues. Wholesale revenues decreased 16% YoY as a result of average fuel cost decline partially offset by an 11.5% jump in gas volumes sold which was driven by Quarles acquisition as legacy sites continue to lose volume share. Fleet fueling segment continues to drive sustained growth with sales of $121 mn, declining slightly from the $127 mn in revenue it posted last quarter.

Merchandise margin improved 150 bps YoY primarily driven by increasing contribution from the high-margin core destination categories, which now contributed 55% of total merchandise gross profits reaping the benefits of management's focus on the same.

{kind=link}

Retail cents per gallon on same-store basis came in at $0.403 from $0.414 last year, continuing to normalize from the outsized margins recorded last year, however, staying above the $0.4 mark. Wholesale gross profit margins declined by 20 bps primarily due to lower gas prices and underperformance of its legacy stores partially offset by contribution from acquisitions. Fuel margin in its proprietary cardlock locations came in at 43.9 vs. 44.5 cents in Q1 as a result of Arko's focus on further strengthening its position in high margin fleet fueling segment.

Adj. EBITDA grew 9% YoY at $86.2 with EBITDA margins improving 60 bps YoY to 4.4% driven by strong contribution from high margin merchandise segment partially offset by declining retail cents per gallon. Interest expenses shot up 36% YoY primarily as a result of higher debt at an increase in average interest cost.

While the company's leverage position continues to be a concern for rating agencies and investors, its leverage ratios have remained stable despite the continued acquisition spree observed in the past year demonstrating the company's value focus and synergistic opportunities. Its interest-paying ability has also improved over the past year with Interest Times Earned coming at 2.3x vs. average 3x over the past year.

We continue to believe that the growth in H2, and in particular, Q3 2023 would be driven by continued growth in its high-margin core destination categories partially offset by a decline in fuel margins primarily due to tough compared which were at record $0.448 in Q3 2022 as the price per gallon shot above $5 mark. ARKO ended up with total liquidity of ~$2 bn including $220 mn cash in hand and $600 mn of undrawn line of credit along with the amended Oak Street program agreement worth $1.5 bn through 2024. We believe the company would continue to fuel further growth through acquisitions and with an enhanced liquidity post the Oak Street agreement, we await further steps from the management on the potential targets.

How the Earnings Stack up?

ARKO has been a relative underperformer compared to its larger peer CASY (CASY has ~2,500 stores compared to ARKO's 1,500+) in terms of operating parameters as a result of CASY's strong brand resonance amongst its consumers compared to ARKO's umbrella of brands operating about 30 brands within the company. We believe it would be imperative for Arko to consolidate brands under one roof which would enable them to drive growth organically through brand building along with its inorganic approach. In terms of merchandise growth, it reported a robust growth of 3.8% vs. 5.4% of CASY, however, underperforming on all fronts from same-store fuel gallons sold to retail fuel margins and lower Adj. EBITDA margins.

| Particulars |

| ARKO |

| CASY |

| SSS Merch growth |

| 3.8% |

| 5.4% |

| SSS Fuel gallons growth |

| (2.6%) |

| 0.4% |

| Retail fuel margin per gallon |

| 40.3 cents |

| 41.6 cents |

| Gross Margin |

| 13.7% |

| 22.7% |

| Adj. EBITDA Margin |

| 4.4% |

| 8.1% |

Valuation

Arko trades at a forward PE ratio of 26.8x at a premium to its larger peer CASY, despite CASY's larger scale and outsized margins. Investors are looking to apply a premium for its growth-driven inorganic boost along with continued steps to drive shareholder value creation by management from increasing its original share repurchase program from $50 mn to $100 mn and increasing dividends (dividend yield of 1.7% currently since it started dividend payouts last year)

However, we believe, despite its aggressive approach to growth through acquisitions and improving earnings profile driven by sustained outperformance of its merchandise portfolio on the back of robust growth in core destination categories, the fuel segment remains an underperformer. In addition, the current valuation multiple offers a balanced risk-reward and we reiterate a Neutral rating.

Risks to Rating

Risks to rating include

1) Volatility in gas prices can significantly impact the gross margins as witnessed during the early part of last year when the company had record margins due to higher gas prices which soon normalized leading to decline in margins in recent quarters

2) Its inorganic growth is fraught with risks as the company may end up overpaying or not be able to realize anticipated synergies or benefits

Final Thoughts

ARKO continues on its acquisition-fueled growth journey and has also shown improvement in its operational profile driven by sustained growth in its merchandise portfolio. Debt metrics also remain comfortable as the company continues to vet their acquisitions diligently to drive synergies and not overpay for growth. However, the fuel business still remains a concern with legacy sites in its wholesale business underperforming and organic recovery in the retail business still away compared to its peers. We believe the valuation premium at which the company is trading compared to CASY, despite its acquisitive growth-led boost to earnings, provides balanced risk reward. Reiterate at Neutral.

For further details see:

Arko: Improving Operating Metrics But Expensive, Reiterate Neutral