AHH - Armada Hoffler: Embedded Growth At Far Too Cheap Of A Price

Summary

- AHH has significant amounts of pent up growth as it waits for developments to come online.

- Thus what appears to be currently medium paced growth is about to accelerate.

- I think AHH's multiple is far too cheap for its quality and growth.

The Buy Thesis

Armada Hoffler ( AHH ) trades at the cheap multiple of an office/retail hybrid REIT as it has been incorrectly labeled as such. Quality and synergy result in its property portfolio drastically outperforming its underlying property types resulting in growth where peers are shrinking.

This quality differential should result in AHH trading at a substantial premium to its peers but it can still be bought at a discount. I see AHH as substantially undervalued with about 35% upside to fair value. As developments come online and the cashflows start hitting the bottom line I think the market will begin to see the growth engine here and start trading it closer to fair value.

Let me begin by addressing the nature of the discount at which AHH trades.

Lumped in with its category

Office real estate is radioactive right now. Investors will not go anywhere near it resulting in the sector trading at an average multiple of 10.5X forward FFO.

Retail is met with a similar skepticism, although to a lesser degree, with an average multiple of 13X.

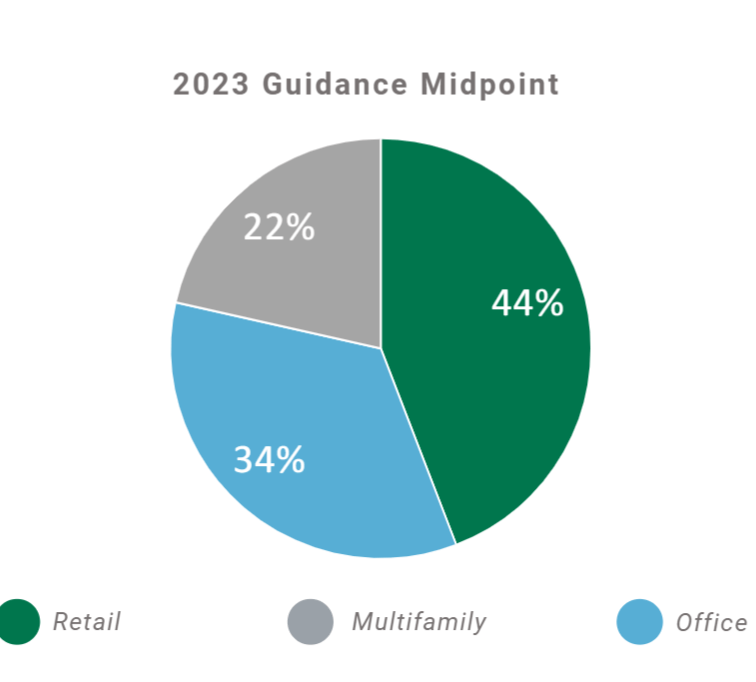

With this sector level viewpoint in mind, the market sees the following slide in AHH’s presentations.

{kind=link}

The slide itself is fine. It is just a factual report of their property types. The unfortunate side effect is that the market sees AHH as a mostly office and retail REIT.

Sure enough, it trades AHH at a multiple of 11X forward FFO. Right in the middle of the office and retail sector multiples.

That is a massive discount to the REIT average of 15.2X.

For office in general, I think the big discount is warranted. Occupancy is absurdly low and landlords are having to pay exorbitant incentives to tenants to induce them to stay. Thus, it is understandable as to why AHH would trade at such a discount given its property types. However, a deeper dive into Armada Hoffler suggests that superficial sector level analysis is not valid here.

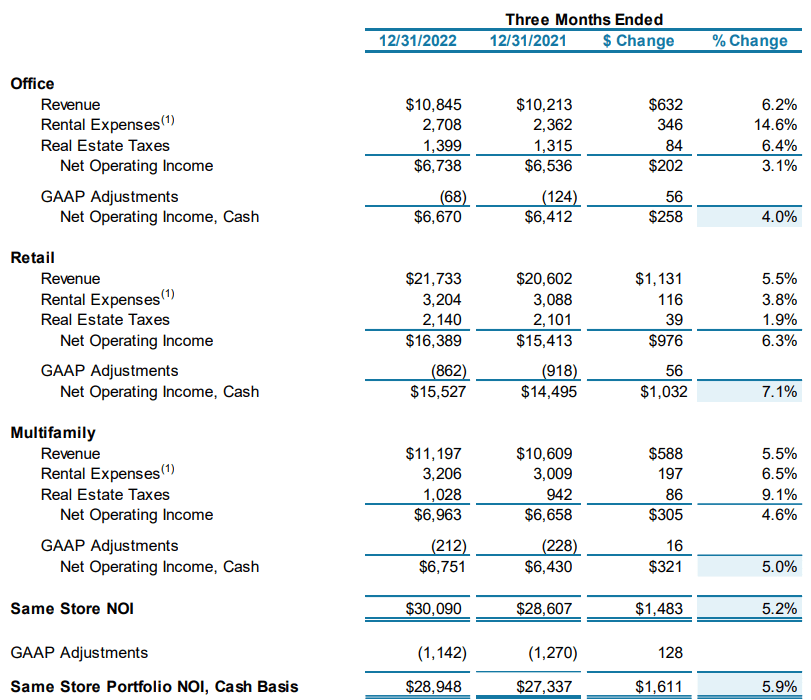

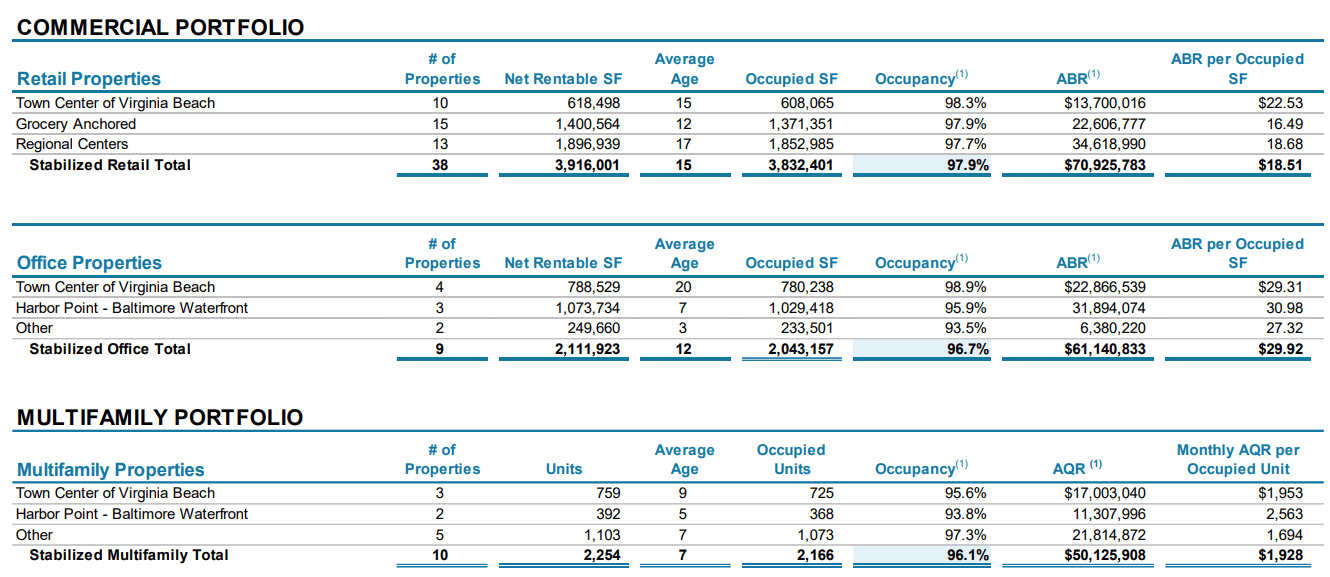

I posit that AHH is not an office REIT. It is not a retail REIT. It is something else entirely. Allow me to tease this notion by referencing the actual numbers just reported on 2/14/23. AHH’s office segment had positive 4.0% same store NOI growth. Its retail segment had positive 7.1% same store NOI growth and its apartments grew NOI by 5.0%.

{kind=link}

Those numbers look nothing like what is coming up in the rest of the office sector. Even in retail which generally had a decent 4Q22, AHH’s numbers came in much higher.

Something different is going on here.

Most REITs are financial vehicles, buying individual high quality assets that at the time of purchase they believe to have strong cashflow relative to their purchase price. It is an analytical process of asset selection where if an asset acquirer can get a good read on the future, they can obtain a nice return.

AHH is more of a value creator. There are two main processes by which they create value:

- In-house development of properties that allows them to obtain large properties for substantially cheaper than their market price. I would estimate they can build for about 80 cents on the dollar relative to buying an existing property.

- Strategic proximal placement of assets next to other assets they own such that they can be demand driver’s for each other.

Synergistic live-work-play environments

Town Center of Virginia beach is the matured example of how this process works. AHH buys up land in the premier location of a submarket and builds the highest end trophy properties within that submarket. In this case it is 500,000 square feet of retail, 800,000 square feet of office and 760 apartments. It becomes the premier destination of the submarket and businesses want to locate there.

This one has already worked and proved the concept as AHH has achieved high occupancy while commanding the highest rent per foot in the submarket.

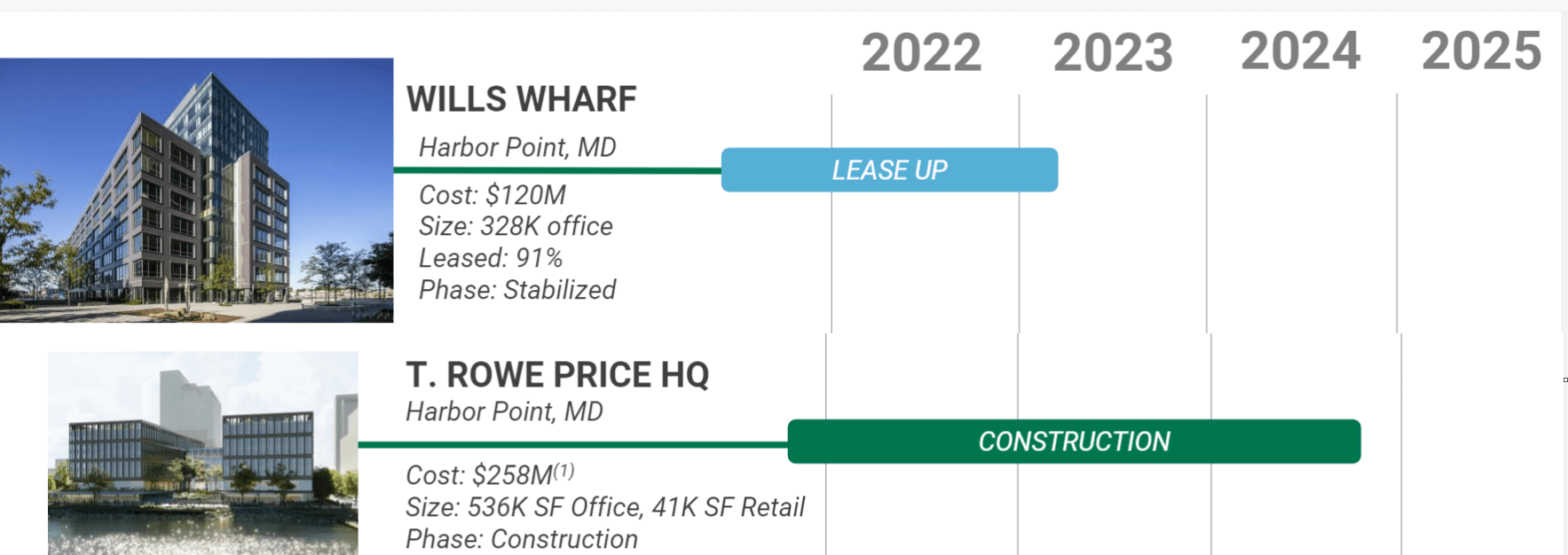

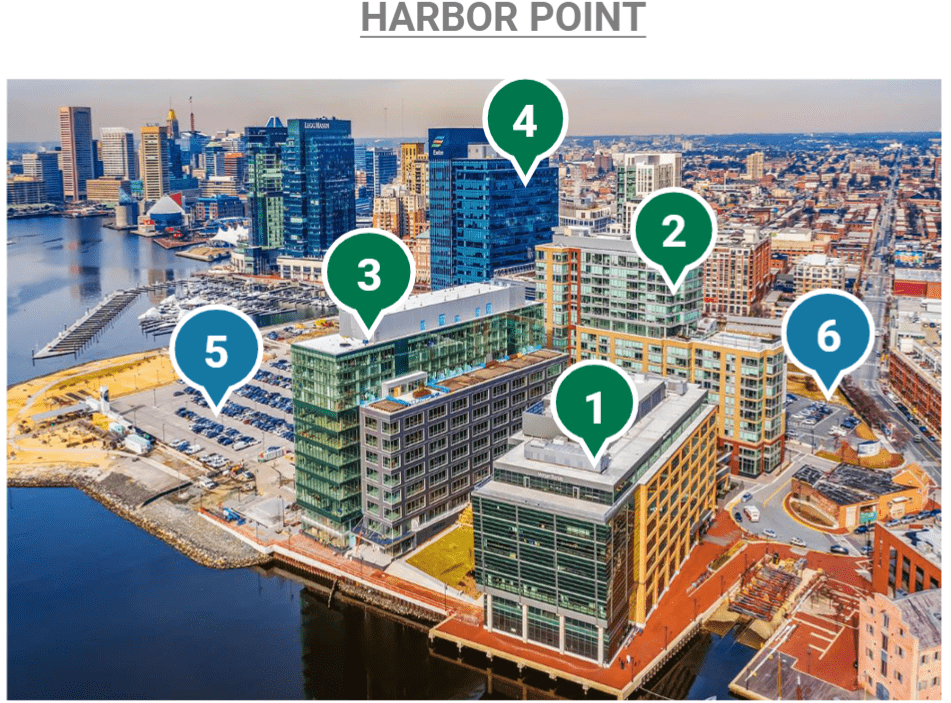

Harbor Point is coming up next. Wills Wharf is already 91% leased and the T. Rowe Price headquarters is of course pre-leased to T. Rowe and will finish construction in 2024.

{kind=link}

These assets are of course characterized as office, but fundamentally they are nothing like office. These are long term leased to high credit tenants and will cleanly cashflow for the foreseeable future. The in-place tenants provide high affluence workers that will live and shop at the adjacent Armada Hoffler owned retail and apartments. They will park in the adjacent Armada Hoffler JV owned parking lots.

{kind=link}

So I hope the point is clear. While technically office, these are not fundamentally anything like office.

These are luxury master planned communities and I think the market is making a big mistake in applying the superficial office label and trading AHH as such.

Growth now and prefunded growth later

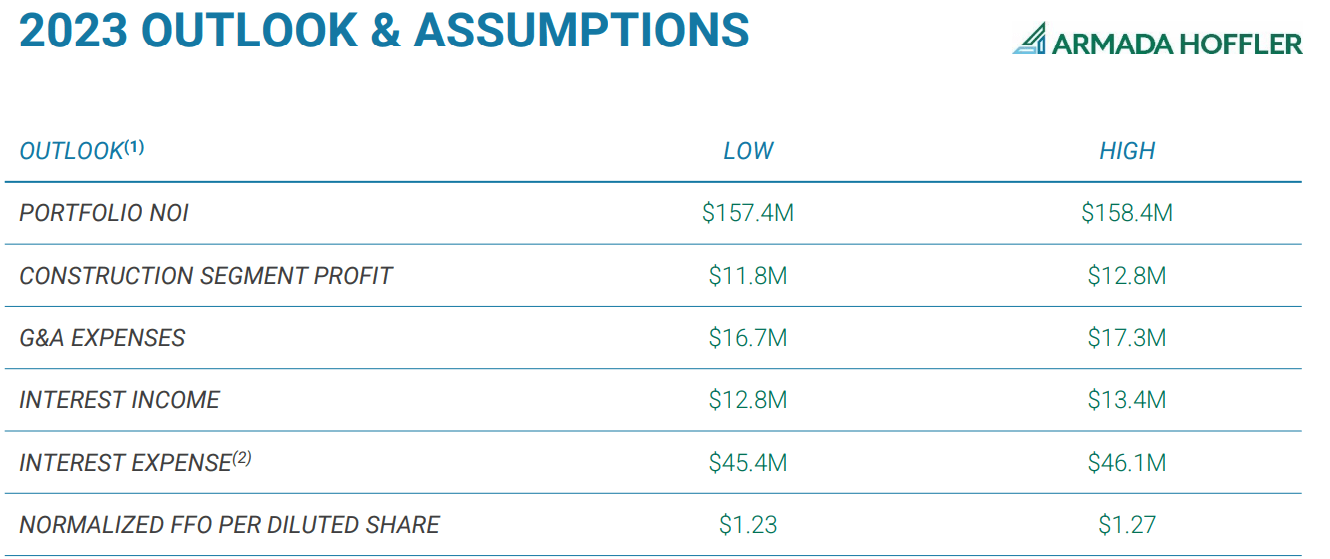

Along with the 4Q22 report on February 14 , AHH put out 2023 guidance calling for $1.23-$1.27 of FFO.

{kind=link}

This beats the 2022 FFO figure which came in at $1.22, but more importantly it is unexpectedly strong for 2023 which is supposed to be a down year. Consensus analyst estimates call for $1.21 in 2023.

{kind=link}

The reason 2023 is supposed to be a down year is timing of construction. The T. Rowe Headquarters is not going to be delivered until 2024, but it is incurring huge cost in 2023. Similarly, the Southern Post in Roswell, Georgia (suburb of Atlanta) costs $118 million but is not delivered until late 2023 with lease-up expected to take most of 2024. The Parcel 4 mixed use development is supposed to finish in early 2024 with lease-up into 2025.

There is all this pent up growth that will hit in 2024 and 2025 yet much of the costs are already being incurred in 2023. Given the magnitude of costs relative to the size of AHH 2023 almost certainly should be a down year - and yet they are calling for growth.

That means the pop in FFO/share that will happen upon delivery and lease up of these huge assets will not be off a trough number but rather a further increase off an already high FFO/share.

How is growth in 2023 possible?

Much of the strength in 2023 outlook comes from organic lease-up. Office occupancy is already high at 96.7%, but more leases are in the pipeline.

On the 4Q22 conference call Shawn Tibbetts ((COO)) discussed an upcoming lease:

“The company is facing issues with tenant expansion request given the lack of available space. We are working with one high credit tenant who we expect to take space at some point in 2023. This will result in yet another high-quality global firm located at Town Center in Virginia Beach”

The rest, presumably, is continued NOI growth in retail and apartments which is less surprising given that many of the REITs in these areas are calling for organic growth in 2023.

I think one of the main advantages AHH is having in leasing is the newness of its portfolio.

{kind=link}

Since they built most of these properties themselves rather than buying existing, the average age is very low compared to most peers.

Valuation

An 11X FFO multiple implies no growth as the ~9% cashflow yield would be sufficient to generate a good return for investors even if there was no growth.

Given the growth in 2023 and significantly larger growth coming in 2024 and 2025 I think this multiple is inappropriately low for AHH. In my opinion, 15X would be correct. This implies a fair value of $18.45 or about 35% above current price.

Risks to investment in AHH

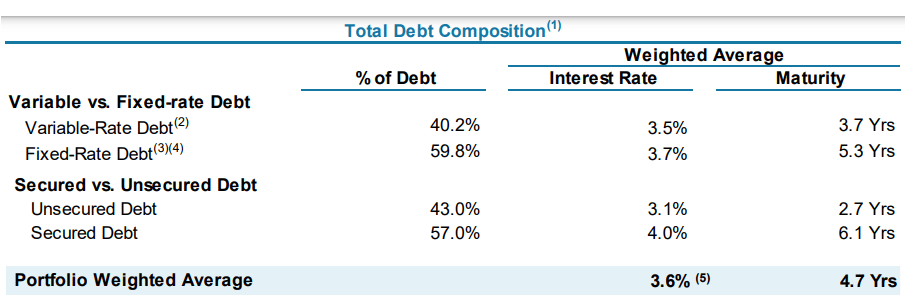

I think the biggest risk for AHH is its heavy reliance upon floating rate debt in this rising rate environment. Roughly 40% of their debt is variable rate and the weighted average maturity is somewhat short at 4.7 years.

{kind=link}

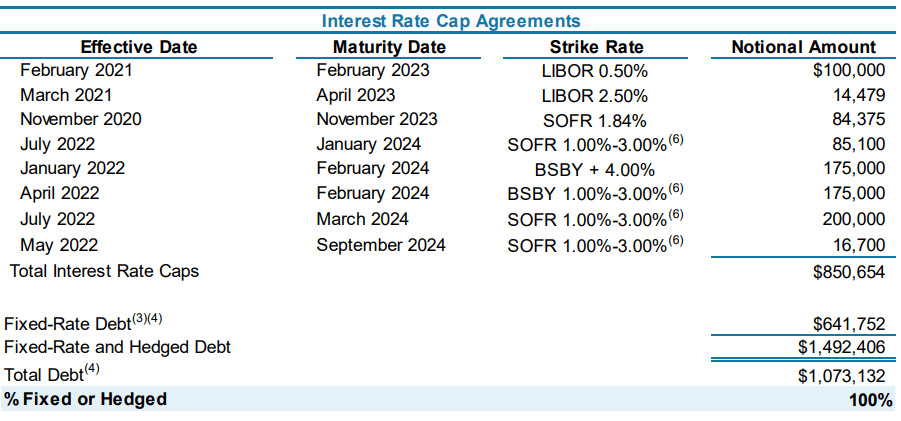

AHH has put in place a series of hedges such as swaps and cap agreements to functionally fix their floating rate debt.

{kind=link}

This temporarily shelters them from the impact of rising rates, but you may notice in the table above that many of these hedges expire in 2023 and 2024.

As such, AHH will have to refinance its currently cheap debt at the now higher market rates.

Partially offsetting this is the fact that AHH just earned its first investment grade rating. So while prevailing market interest rates have risen, the premium that AHH has to pay over treasuries is likely smaller than it has been in the past.

As a result, cost of capital will rise for AHH as they refinance over the next few years, but it will not rise by as much as the parallel shift in the yield curve would imply. Further, it is worth noting that rising interest expense is already embedded in AHH’s guidance.

The other risk to AHH is one common to all developers; the uncertainty of the environment upon completion. The outlook for these developments looks great now, but 2024 and 2025 could be an entirely different environment. Pre-leasing mitigates this risk somewhat, but there is a portion of space that still needs to be leased.

Overall thoughts

I have long owned AHH and have been continually pleased with the way the company is run and its fundamental performance. Over the past decade it has had times in which it was overvalued and times when it was cheap. This is one of those times where it is cheap.

For further details see:

Armada Hoffler: Embedded Growth At Far Too Cheap Of A Price