AHH - Armada Hoffler Series A Preferred Stock: 7.7% Yield And 14% Upside To Par

2023-04-26 15:37:24 ET

Summary

- AHH.PA offers a high yield and low risk profile, as it is issued by a REIT with a solid and diversified portfolio of quality real estate.

- The preferred dividend coverage is very high.

- AHH common stock may have more upside, but AHH.PA enjoys a higher and safer dividend yield.

The Armada Hoffler Properties Series A 6.75% Cumulative Perpetual Preferred Stock (AHH.PA) looks very interesting as a source of safe, high income with some upside.

Here are some key metrics for AHH.PA:

| Price as of 4/25/23 |

| $21.90 |

| Upside to $25 Par Value |

| 14% |

| Dividend Yield as of 4/25/23 |

| 7.7% |

| Capitalization At Par |

| $55m (+ Overallotment: $63.25m) |

| Call Date |

| 6/18/24 |

| Total Return Assuming Redemption At Call Date |

| 21.5% |

The real estate portfolio backing AHH.PA's dividend is strong and stable, the management team is well-aligned with common and preferred shareholders alike, and the preferred shares provide very nice total return prospects along with its high yield.

Thus, AHH.PA looks like an attractive opportunity for income investors.

Brief Overview Of Armada Hoffler Properties

I pitched the issuing company, Armada Hoffler Properties (AHH), in a recent article titled " 5 Quality REITs Yielding Over 5% ." It is a real estate investment trust focused on owning and developing various kinds of real estate on the East Coast.

{kind=link}

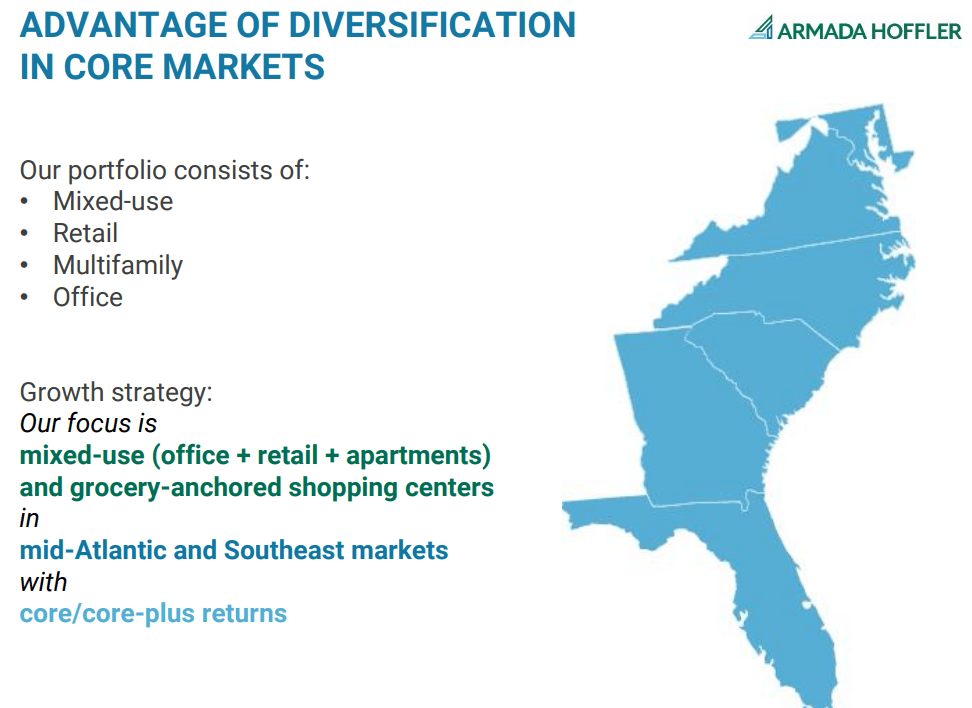

AHH specializes in developing and managing mixed-use centers in prime locations, such as its flagship Town Center of Virginia Beach property that also houses the company's headquarters.

The focus is on high-quality properties, whether they be trophy office buildings, grocery-anchored retail centers, or Class A apartments. The REIT also owns one industrial property.

{kind=link}

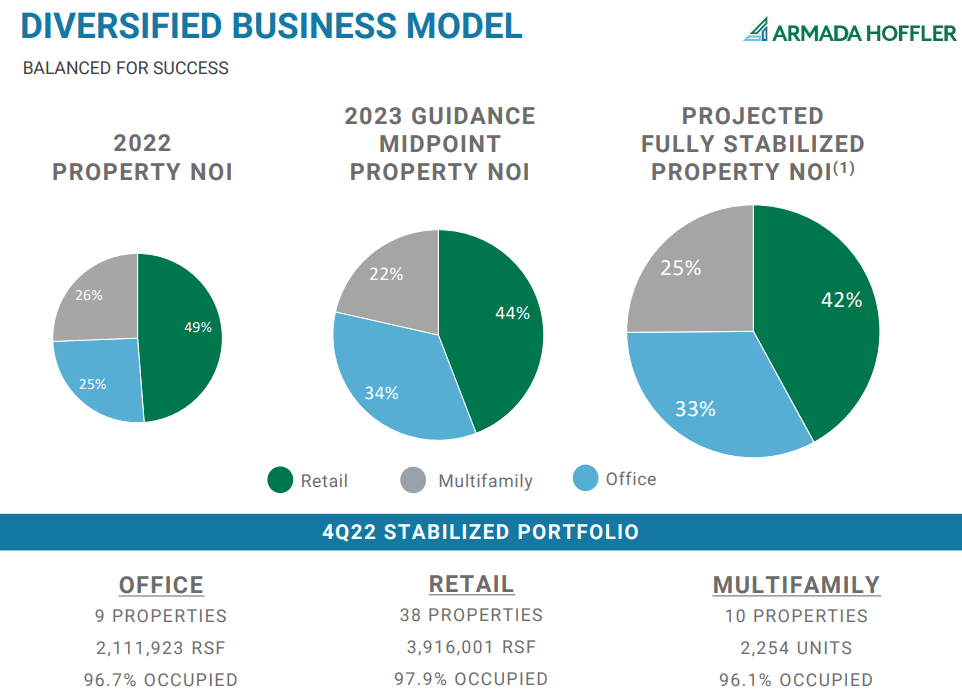

A plurality of NOI comes from retail properties, while about a third comes from office and the remainder from multifamily.

One measure of a property portfolio's quality is occupancy. Higher occupancy generally indicates higher demand for space from tenants. Notice that AHH's retail occupancy is nearly 98%, while office is almost 97% and multifamily is about 96%. These are strong metrics that demonstrate a fairly high degree of stability.

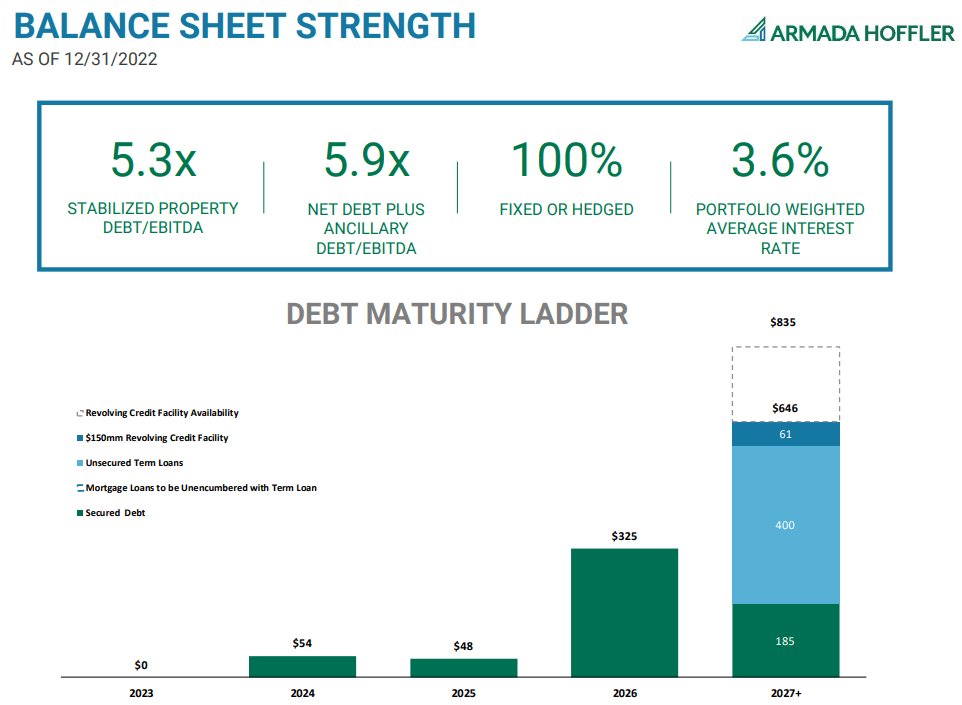

The REIT's balance sheet is in pretty good shape, with 100% of loans fixed or hedged at this point and very few maturities until 2026.

{kind=link}

Management had to pay some upfront fees in order to purchase caps for much of the ~40% of debt with floating interest rates, but now that those caps are in place, AHH's interest expenses are mostly fixed over the next few years. That results in safer common dividends and significantly safer preferred dividends.

When it comes to a preferred's dividend safety, it's important to keep in mind that preferred stocks generally have fixed share counts, while common stocks may see their shares outstanding increase over time as the company taps equity for investments. As such, growth in EBITDA and NOI translates directly into greater preferred dividend coverage, holding debt and interest expenses equal.

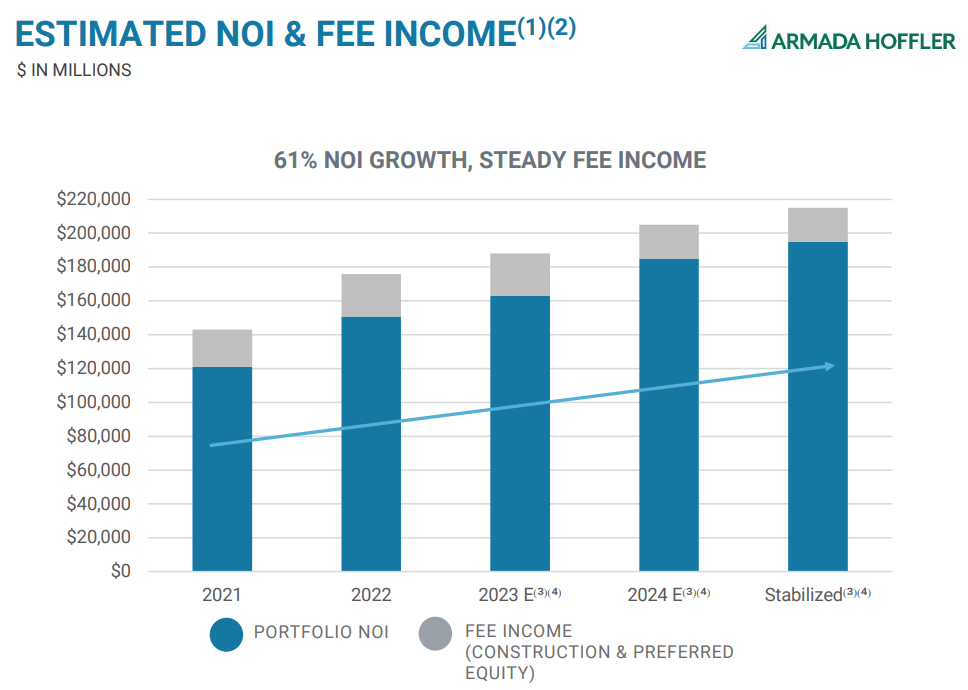

As we saw above, AHH's interest expenses should be mostly fixed over the next few years, while NOI growth should continue steadily increasing.

{kind=link}

That increasing portfolio NOI year after year steadily increases fixed charge coverage, which includes preferred dividends.

You can also look at EBITDA, which in the chart below is non-adjusted but still directionally accurate. In the past year, EBITDA has surged higher.

In the last twelve months, EBITDA has been 6.2x higher than interest payments and preferred dividends. And EBITDA after interest payments covers preferred dividends 16.5 times over.

How Likely Is AHH.PA To Be Redeemed?

Finally, it would be fair to ask how likely it is that AHH.PA will be called on or near its call date of June 18th, 2024.

The preferred coupon yield at par of 6.75% does seem significantly higher than the weighted average interest rate of 3.6%. But with what money would AHH redeem the $55 million of AHH.PA shares?

Given that AHH is trading at a normalized FFO yield (NFFO/market cap) of 10.7% and an AFFO yield of 8-8.5%, trading the preferreds for common stock would not seem like a good idea, if AHH's share price remained around its current price in June 2024. I can't see management issuing common stock to redeem the preferreds.

AHH does have $233.5 million available on its credit facility (as of 12/31/22), and the facility is priced at SOFR plus about 1.5%. Today, that would be around a 6.3% effective borrowing rate, but if the Fed lowers interest rates below their current level at some point between now and June 2024, the cost of using the revolver will fall and make it at least somewhat tempting to eliminate AHH's most expensive source of capital - AHH.PA.

As of now, AHH does have an interest rate hedge on the credit facility keeping the interest rate effectively fixed, but by next year that hedge will expire. It's unknown if management will secure another one, or if such a hedge could be extended to the full amount needed to redeem the preferred stock.

So, in short, I don't know if AHH.PA is likely to be redeemed at its call date, but it does seem plausible that it could be.

Perhaps more importantly, notice that AHH.PA has traded above its call price for a significant portion of its lifespan. As such, if interest rates fall from here, I find it likely that AHH.PA will achieve at least 14% upside based on its status as a bond proxy alone.

Change Of Control Clause

You can read about AHH.PA's change of control provisions in its prospectus or in this SEC filing summarizing the prospectus. Readers are welcome (and encouraged!) to read through these documents themselves, as I readily admit to being maladroit at divining their legalese. What follows is my non-expert understanding of the buyout scenario.

First, what exactly counts as a "change of control"? Two conditions must be met:

- AHH is wholly acquired by a third party entity

- That third-party acquirer is not publicly traded on any US stock exchange

If AHH is acquired by a non-publicly traded company, AHH.PA shareholders also have the right to convert their shares into the lesser of $25 plus unpaid preferred dividends divided by the common stock price or 2.97796 common stock shares prior to the change of control conversion date, unless the company first announces a redemption of shares for cash (which would be at the $25 par value). The company can also redeem its AHH.PA shares at $25 per share up to 120 days after the change of control date.

So, what happens if the acquirer is publicly traded? In this case, the provision triggering liquidation-at-par of the acquiree's preferred stocks doesn't occur, and the acquirer can simply leave the acquiree's preferred stocks in place.

This is exactly what happened with Wheeler REIT's ( WHLR ) acquisition of Cedar Realty (CDR). CDR's preferred stock series B and C continue to trade publicly, albeit at a severe discount to par value.

They trade at that discount because, even though preferred dividends continue to be paid now, WHLR could cease payment of these preferred dividends at any time. WHLR already does not pay a common stock dividend, nor has it paid dividends for its own preferred stocks in quite some time.

Note, however, that even in this worst-case scenario, it appears that the publicly traded acquirer is still required to pay the acquiree's preferred dividends before it can pay its own common stock dividend.

Perhaps most telling, though, is the fact that company insiders own shares of AHH.PA themselves.

According to Nasdaq , for example, former CFO Michael O'Hara owns 8,900 shares of AHH.PA (purchased above $26, I might add). While O'Hara retired from his post in March 2022, and thus we can't know if he has since sold these shares, the fact that the former CFO owns or owned them himself is notable.

Bottom Line

I like AHH and believe it has around 50% upside potential after a Fed pivot and the beginning of a new falling interest rate environment.

But I also like AHH.PA for a different reason: it's safer and higher-yielding dividend. While AHH currently offers a dividend yield of about 6.6%, AHH.PA's yield of 7.7% sits a full point above that.

For income investors who want to lock in a 7.7% yield for at least another year, along with 14% probable upside, take a look at AHH.PA.

For further details see:

Armada Hoffler Series A Preferred Stock: 7.7% Yield And 14% Upside To Par