AMNF - Armanino Foods: A Hidden Gem With A Bright Future

2023-09-08 11:00:01 ET

Summary

- Armanino Foods of Distinction is a small-cap producer of frozen Italian cuisine.

- The company has shown solid financial performance and navigated the COVID-19 pandemic well.

- While a potential takeover did not happen, Armanino remains an attractive target for larger food or food distribution companies.

Recap

In September 2021, I wrote an article about Armanino Foods of Distinction ( AMNF ), in which I praised the company for its financial discipline and the way in which it navigated the COVID-19 pandemic. Also, I wrote that I viewed the company as a potential takeover target, because of the potential synergies between Armanino and an acquirer, and also since changes in the board of Armanino were signaling a bigger emphasis on growth.

First of all, this potential takeover did not happen (at least not yet). In this article, I will show why I am quite satisfied with the way Armanino has performed during the past few years, and I will try to give an estimate where we can expect the company is heading during the next few years.

Performance

Let us take a look at the financial performance of Armanino in 2021 and 2022. In figure 1 below, I pasted the consolidated statements of operations as it can be found in Armanino's 2022 annual report.

otc markets Armanino report

Figure 1: Armanino Foods of Distinction consolidated statement of operations in annual report 2022

The first thing which stands out in this statement is the net sales figure, which increased by more than $14M from 2021 to 2022. This was partially caused by customers restocking in 2022 after being very cautious during the COVID-19 pandemic, which was still in full swing in 2021. Also, operating expenses have gone up by about 20%, but this seems to be more or less in line with the increase in sales.

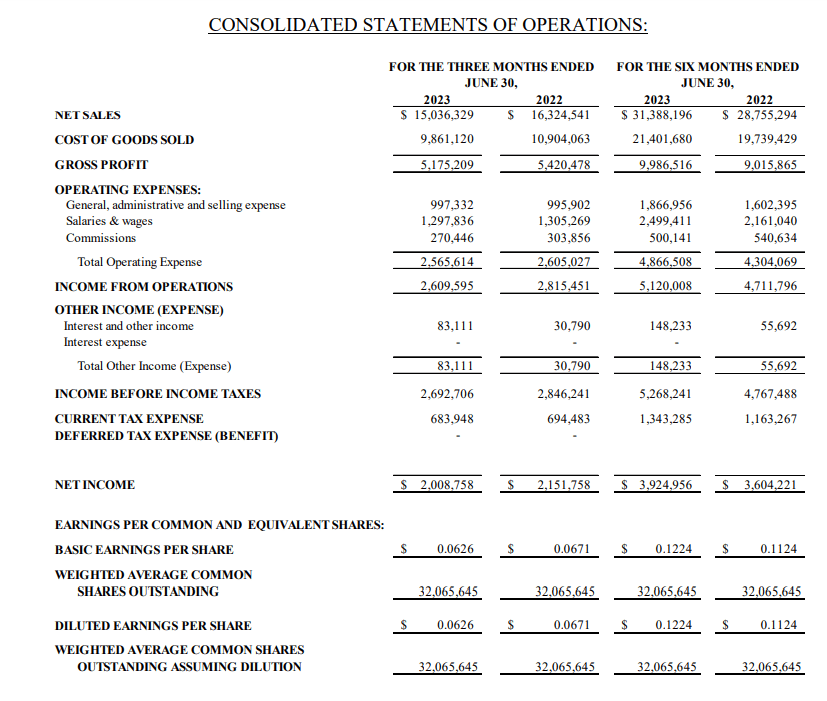

In total, this statement looks very solid. A nice increase in sales, net income and earnings per share. Now let us check their most recent financial report, of Q2 2023, which I inserted below.

{kind=link}

Figure 2: Armanino Foods of Distinction consolidated statement of operations in quarterly report Q2 2023

The figures of these two timespans are more easily comparable since 2022 was not impacted by the COVID-19 pandemic any more like 2021 was. There might have been a bit of restocking influencing the financial performance of Armanino in 2022, but still 2022 and 2023 will be a lot easier to compare.

Measured over the first half year of 2023, net sales increased by almost 10%, but this was only thanks to a very good performance in the first three months of the year. Sales during Q2 2023 were actually lower than in Q2 2022. In its report, Armanino states that 2023 Q2 sales were likely lower "due to economic headwinds and somewhat one-time prior year sales benefit", which sounds plausible.

The other listed items on the statement of operations seem to be influenced by the level of sales, and over the first 6 months of 2023, the company achieved a modest but decent growth in sales, income and earnings per share.

Now to conclude our short examination of their financial reports, let us take a look at the balance sheet of Armanino as listed in their Q2 report 2023.

otc markets report

Figure 3: Armanino Foods of Distinction balance sheet in quarterly report Q2 2023

This balance sheet looks about as clear as you would expect from a conservatively-run company with steady growth: some items are fluctuating a bit, for instance the categories inventories and accounts payable, but there are no out of the ordinary large items listed which could have a major future influence on the company.

About the item listed as investments, the company mentions: "At June 30, 2023, the Company held a mutual fund investment with a fair value totaling $5,085,458."

Please also note that the number of shares issued did not increase by a single share. Let us now check whether share performance and dividend development of Armanino matched their stellar performance as listed in their financial reports:

Graph 1: Armanino Foods of Distinction share price and dividend development over the last 5 years (source: YCharts)

The short answer is yes, it did. Share price rose by about 30% between the end of 2021 and now. Dividend was increased twice after it was restored to pre-pandemic levels, amounting to a total increase of almost 20% over 2 years. What's not to like?

Well, the most obvious risk in Armanino's operations is their dependency on a single large distributor. From their Q2 2023 financial report:

The Company had one distributor customer who accounted for 61% of outstanding receivables at June 30, 2023, and accounted for 56% of outstanding receivables as of December 31, 2022.

During the three months and six months ending June 30, 2023, 49% and 51% of the Company’s total gross sales, respectively, were handled by a non-exclusive national distributor. This distributor is a master consolidator who buys various products in large quantities, stores them, and then ships consolidate products, primarily to other distributors from one of their twelve distribution centers located throughout the US.

Armanino's outstanding receivables and sales are dominated by a single distributor, which is responsible for about half of their entire sales. Being only a small food producer, this might be difficult to avoid, and this concentration has not posed problems for Armanino in the past. But still, this risk deserves mentioning again.

Implications for investors

As we can see in both the financial results of Armanino and the graphs of their share price and dividend development, the company has successfully regained their path to growth after a brief setback caused by the COVID-19 pandemic. Growth has returned and the company restored its dividends to pre-pandemic levels in 2021. After this, dividend growth has picked up again with two very healthy dividend increases of 9% and 10% during the last 2 years. Armanino's share price responded accordingly, rising from around $3.30 a share at the end of 2021 to $4.25 nowadays, an almost 30% increase in a bit more than 1.5 years!

Let us take a look at Armanino's price to earnings ratio to see whether the stock would still be worth buying:

Graph 2: Armanino Foods of Distinction price to earnings ratio over the last 10 years (source: YCharts)

As we can see in the PE graph, which I intentionally took over the last 10 years, the company's current price to earnings ratio of 18.2 looks to be in a normal realm for the company. During the years 2020 and 2021, the PE metrics were heavily influenced by the COVID-19 pandemic and as such this bottom and peak cannot be used to assess the normal range.

A PE ratio of 18.2 might be a bit on the high side for Armanino, since there were a couple of instances in the past between 2014 and 2019 where the stock traded for a PE of around 15, during a time when they were also growing steadily. But still, I would not call the company overvalued by any means. Based on qualitative and quantitative factors, I still rate the company as a buy.

Estimates about the future

In their press release, the board expressed the following thoughts about the future and the way in which Armanino will mitigate future economic headwinds:

Going forward, the Company anticipates continued success in executing its long-term strategies as well as lower prices on key commodities which drive COGS. In addition, the Company expects to complete soon the capital improvements to its production facility. As such, the Company expects ongoing benefits from operational efficiencies that should help mitigate the impact of potential future economic headwinds.

A couple of thoughts about this statement:

- Lower prices of key commodities are anything but certain. So whether this will become a factor in lowering the cost on goods sold is a big question mark in my opinion.

- The capital improvements to the production facility of Armanino are however a real factor which is very likely to help the company benefit in the near future.

- For the future a bit further away, Armanino will probably need to expand their facilities to a greater extent or make them more efficient to continue its current growth rate. This means ongoing capital expenditure.

As far as I can tell, Armanino still has space to run and continue its growth. If they are able to lower their production costs, earnings might be able to grow faster than sales but I view this as an uncertain factor, although I am happy with the focus of the company on this topic. At this moment, it looks reasonable to assume that Armanino should be able to continue or slightly increase (by lowering COGS) its current growth rate.

What about the potential takeover?

In my previous article in 2021 I wrote that I thought the company would be an attractive takeover target for a larger food or distribution company. As illustrated by the sound financial figures over the last couple of years, I am happy a takeover did not happen. The company looks solid as a rock and as an investor I hope that this nice performance can continue into the future.

On the other hand, if I were on the board of a food or food distribution company, I would love to own Armanino for exactly these reasons. Especially food distribution companies would have good synergies with Armanino since one of the main weaknesses of Armanino is that they are quite dependent on a couple of food distribution companies. A takeover from a food distribution company would potentially increase the total addressable market and provide some certainty with regard to distribution.

From Armanino's perspective though, the situation is fine as it is. The company is growing in a steady, controlled way and financial discipline is stellar. A potential acquirer would have to offer very significant synergies in order for it to be worth it from the companies' (and investors') perspective. Still, I believe a takeover is not out of the question, simply because Armanino looks so attractive.

Conclusion

In my previous article about the company, I rated Armanino a strong buy. As I discussed in this article, the stock has rallied almost 30% since then, decreasing future potential gains, which changes my rating to buy. The company continues to be very robust financially, while also continuing its steady but modest growth. If their endeavors to lower production costs bear fruit, their earnings might be able to grow quicker than their sales in the near future.

I would be happy adding to my position for the current share price, since I believe the company is not overvalued and has very decent prospects. Armanino Foods of Distinction is a company which possesses some interesting characteristics which are rare in combination with one another: small, steadily growing and financially robust. I believe Armanino remains a true gem for dividend growth investors looking to add a smaller company to their portfolio.

For further details see:

Armanino Foods: A Hidden Gem With A Bright Future