AMNF - Armanino Foods: Momentum Remains Strong But Getting Pricey

2024-01-16 15:42:24 ET

Summary

- Armanino's fundamentals have improved significantly since the pandemic, with a 30%+ gain in shareholder value over the past year alone.

- The company has focused on cost control, internal efficiencies, and growth drivers in its food service and retail segments.

- Despite sound profitability, Armanino's assets and sales appear overpriced, leading to a 'Hold' rating on the stock for now.

Intro

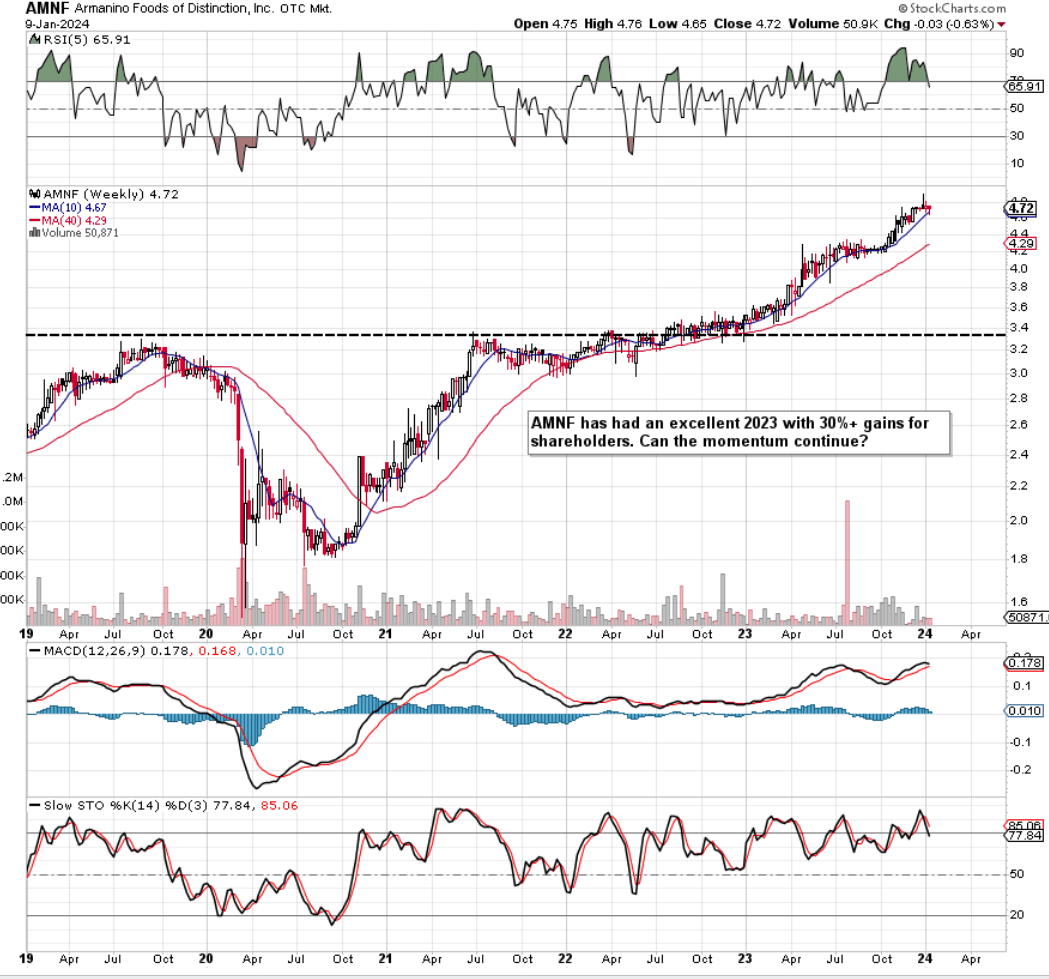

We wrote about Armanino Foods of Distinction, Inc. ( OTCPK:AMNF ) back in February 2020 when we delved through some of the key financial trends that make up the company's dividend. Shares were trading at $3.20 per share at the time. Although we saw no issues with the US frozen food producer at the time with trends in book value and EBIT being particularly strong, given that shares had topped out in September'2019 and were undergoing a sustained trend of lower lows at the time, we rated the stock a 'Hold' until we had confirmation that financial markets had bottomed out.

The 'Hold' rating at the time was the right call as shares traded below $2 a share in the throes of the pandemic before finally bottoming out. As we see from the technical chart below, post the stock's rally out of the pandemic 2020 lows, shares did consolidate (limited share-price gains) between mid-2021 & late 2022. However, Armanino's fundamentals seemed to receive a significant boost once calendar 2023 started as since then, shares have never looked back. Shareholders (minus dividend distributions) have seen a 30% gain over the past 12+ months which demonstrates that the ramifications of the pandemic may have been a blessing in disguise.

{kind=link}

AMNF Technical Chart (Stockcharts.com)

Growth Triggers In Multiple Areas

We state this because Armanino is a much different company now than it was in 2020 in that the downturn forced management to get its costs under control, improve internal efficiencies & marketing efforts, and above all, double down on growth drivers to gain market share. After reviewing Armanino's most re cent earnings repor t (16th of October 2023) & investor presentation , management seems adamant that significant potential remains in its food service core business, retail as well as its new product platform.

In food service, restaurant penetration stands at only 30% demonstrating the long runway for growth Armanino has for the multitude of its frozen fresh offerings illustrated below. On the retail front, the success of the Armanino brand in the likes of Safeway in certain jurisdictions demonstrates that the company has an excellent product where the value case among customers is identified. Again, in the retail segment, there is a long runway for growth here given Armanino's limited presence in the South West, Texas & the East of the US. The 'Ready Meal' trend is another growth area where Armanino can take advantage of the present relationships it has with its retailers. The target market Armanino wants to hit here is the health-minded deli customer who wants healthy food out of a restaurant setting.

{kind=link}

Armanino Top-Selling Foodservice Items (Company Website)

Financial Trends

Evidence of Armanino's transformation can be seen in its recent quarterly numbers (ending September 2023) & corresponding 9-month (year-to-date) trends. Sales grew by 4% over the same period of 12 months prior and by 7.5% over the first three quarters of 2022. What was particularly noteworthy (alluded to earlier) is how the company continues to get its costs in order and thus improve its margins. Net profit of $2,263,972 in the September quarter was a 46% gain over the same period of 12 months prior while the first nine months of 2023 ($6,188,927) came in 20% higher compared to the same 9-month period of 2022.

Suffice it to say, the most glaring trend in the company's near-term financials is the pace at which bottom-line growth has been outpacing top-line growth. Although stocks are for the most part priced on Wall Street on their earnings growth, strong sales growth also has to be in the picture to ensure sustained EPS growth can indeed continue. In saying this, management remains confident that significant costs (concerning commodity pricing & capital improvements on its production facility) will continue to be seen over time in the company's financials. While this may be so, investors would prefer to see a more diversified customer base which consequently would bring less risk to the company's top-line sales numbers. We state this because Armanino's main customer continues to contribute well over 50% of the company's top-line sales at present.

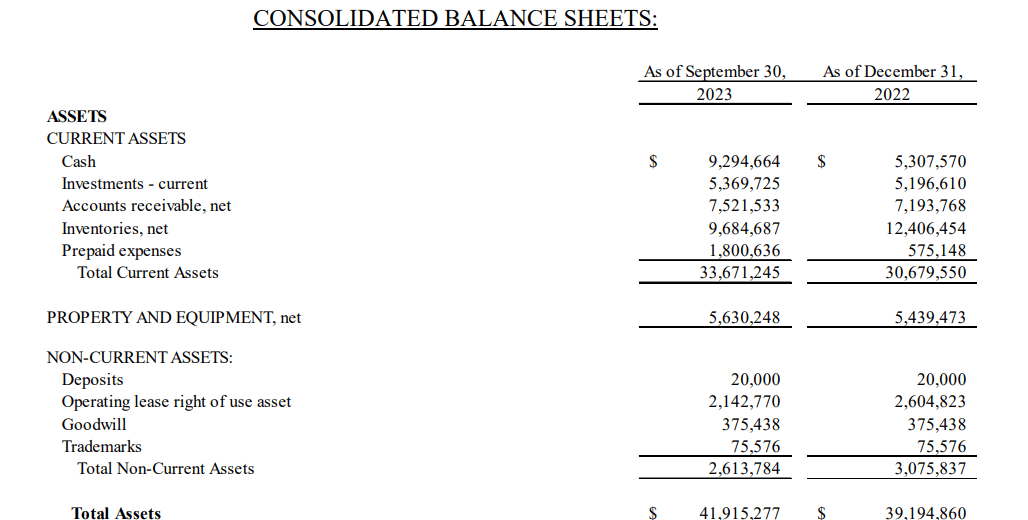

Concerning the balance sheet, considering the company's strong liquidity (current ratio of 3.04 in the latest quarter) & absence of interest-bearing debt (strong solvency), it is not surprising to see strong trends in its assets as we see below. A big reason however for the significant jump in the company's cash balance over the past three quarters was the $2.7+ million drop in inventory over this period. A lower inventory count on higher sales is excellent for cash-flow generation so it will be interesting to see if this trend can continue over time. Accounts receivables have remained in check at just over $7.5 million.

Armanino Balance Sheet (Assets) (www.otcmarkets.com/otcapi/company/financial-report/386290/content)

{kind=link}

Forward-Looking Expectations

Therefore, with a debt -free balance sheet and earnings growth most certainly taking place in 2023, the question is whether Armanino is cheap enough to warrant long exposure at present. In effect, the value of Armanino as an investment is based on its future earnings but since forward-looking growth rates are impossible to predict, we will go to the company's traditional valuation multiples to see how they stack up against the sector in general.

To get a sense of the growth path Armanino is currently undertaking, we will annualize the year-to-date 2023 numbers to get a read on how cheap the company's sales, earnings & cash flow are from a forward-looking basis. When we annualize fiscal-2023 year-to-date top-line sales, net earnings & operating cash flow, we get adjusted annual sales of $63.29 million, adjusted net profit of $8.25 million & adjusted annual operating cash flow of $10.55 million. Using the present market cap of $152.24 million, we get the following adjusted multiples

| Valuation Multiple |

| Adjusted 12-Month |

| Sector Median |

| Price To Sales |

| 2.4 |

| 1.15 |

| Price To Earnings |

| 18.45 |

| 21.26 |

| Price To Cash/Flow |

| 14.43 |

| 12.25 |

Although Armanino's sales are more expensive than the consumer staples median, its earnings are currently trailing the average. However, when we look at the company's balance sheet ($28.994 million reported at the end of Q3), we see that Armarino's assets are overextended as the company's trailing book multiple comes in at 5.25 as opposed to a sector average of 2.4.

What can we learn from the above-adjusted multiples? Well, assets & sales are the key metrics that drive a company's earnings & sales over time. Therefore, for the value-minded long-term investor, it makes sense to buy a company's assets & sales as cheaply as possible as valuation multiples many times revert to their long-term mean. Although short-term upside looks on the cards here due to the strength of the stock's technicals, the company's assets look a tad pricey which is why we reaffirm our 'Hold' rating in this play.

From a fundamental standpoint, Armanino remains a strong buyout target due to the growth triggers mentioned above and strong financials. If indeed a bigger player were to come onto the scene, then you would feel that the company would be able to achieve much better economies of scale and increase the company's addressable market more quickly. If a buyout were not to take place. What we see playing out is that if strong sales growth remains absent in upcoming quarters, we will see the stock consolidate until its key valuation multiples catch up or 'revert' over time.

Conclusion

Therefore, to sum up, despite Armanino's sound profitability, well-covered dividend & multiple growth triggers, the company's assets & sales look a tad overpriced at this point. Furthermore, one would believe that higher levels of revenue growth will be needed over time to keep those strong double-digit bottom-line growth rates intact. The stock remains a 'Hold' for us at present. We look forward to continued coverage.

For further details see:

Armanino Foods: Momentum Remains Strong But Getting Pricey