ARR - Armour Residential: ~50% Dividend Cut Expected By 2024 As Swaps Expire

2023-10-01 02:27:20 ET

Summary

- Long-term interest rates have increased significantly in Q3, defying expectations of bond market stability.

- Higher commodity prices threaten a rebound in inflation and encourage a parallel increase in the yield curve (both long-term and short-term).

- Residential mortgage REITs, like ARMOUR Residential, have negative exposure to inflation and interest rates, with higher interest rates creating book value and margin issues.

- This quarter's increase in long-term rates is expected to lower ARR's book value per share to around $5.9, given no significant portfolio positioning changes.

- As its interest swap positions expire soon, I expect that ARMOUR distributable income will likely be cut in half over the coming quarters, giving it an "adjusted yield" of ~10%.

As the third quarter ends, it is a good time for investors and analysts to take stock of significant events that have occurred this quarter, impacting financial markets. One of the most notable trends has been the relatively substantial increase in long-term interest rates, defying expectations of bond market stability after last year's record-breaking bond crash. The second key Q3 developed is likely the 30% rise in oil prices, threatening a rebound in inflation, thereby encouraging even higher long-term interest rates.

Most stocks have negative exposure to inflation and interest rates, but one of the most directly exposed is residential mortgage REITs. I've covered many residential mortgage REITs over the past three years, detailing their immense negative exposure to interest rates and inflation in 2020 . Since then, many, such as ARMOUR Residential REIT ( ARR ), have lost over half of their value as higher mortgage rates hamper their book value, and the inverted yield curve pressures their net interest margins.

I covered ARMOUR last in April with a bearish view because I expected that the inverted yield curve would slowly erode its profitability potential over the coming years as its swap positions expire. Since then, ARR has lost an additional 21% in value, mainly due to the recent spike in Treasury rates. Indeed, this trend is slightly surprising to me as interest rates seemed unlikely to rise much higher five months back. However, with the developments in the energy market pushing further stagflation, bond prices have taken yet another nosedive . Accordingly, it appears to be an excellent time to look at ARMOUR and the interest rate trends impacting its value.

Strategy Update and Interest Rate Pressure

Functionally , ARMOUR is a highly levered bond fund, given its assets have low credit risk but extremely high duration risk compared to the more credit-sensitive commercial mortgage REITs. Hence, investors should watch ARMOUR's book value trends, realizing its ~22.6% dividend yield is high due to extreme leverage. I believe far too many investors buy stocks with high dividend yields, overlooking solvency factors that could easily wipe out all potential gains from dividends. Historically, ARMOUR is a stock with an excellent dividend yield, but chronic book value declines have caused its total returns (which include dividends) to almost always be negative YoY. See below:

Over the past decade, ARMOUR's tangible book value per share has declined at around 18% per year annualized. Further, it has reduced almost every year, as has its share price. Before 2020, the chief cause of its decline was excessive refinancing or prepayment rates due to the meager mortgage rates over that period. Since 2020, the core cause of its decline has been the sharp increase in mortgage rates, lowering the value of its securities portfolio.

While managerial error, or poor positioning, could be stated as a cause of its chronic declines, indeed, ARMOUR has also been a bit unlucky because the mortgage market has gone from one extreme (record low mortgage rates) directly to the other (multi-decade high mortgage rates). Theoretically, if mortgage rates were stable around a historically average level that did not encourage refinancing, ARMOUR's book value would be stable. However, since the Federal Reserve began to wade into the mortgage-backed-security market, mortgage rates have become far more volatile. The Fed also buys essentially the same assets as ARMOUR, 30-year fixed-rate agency-backed residential mortgage-backed securities (mortgages lent to most homeowners).

Though the relationship is not direct, mortgage rates usually decline at the onset of Federal Reserve QE into the market and rise when the Federal Reserve sells MBS assets. The pattern is not direct because some investors (mainly banks) will often buy and sell MBS assets ahead of the Federal Reserve. See below:

Significant Federal Reserve and commercial bank inflows likely caused meager mortgage rates in 2020. Since 2022, both major institutions have become consistent net sellers of mortgage-backed-security assets, creating significant upward pressure in mortgage rates. Fundamentally, the MBS market has many buyers and very few sellers. Despite its high leverage, ARMOUR has increased its exposure to the market over the past year, pushing its total liabilities-to-assets up to nearly 90% as it purchases MBS securities at their now much higher rates. See below:

ARMOUR's decision to increase leverage over this tumultuous period should be seen with some concern for investors. The company is most likely looking to improve its yield by buying mortgage assets at much higher rates. However, should mortgage rates continue to rise, its solvency risk is more significant due to the increase in its leverage. Problematically, mortgage and treasury rates have increased again over Q3. See below:

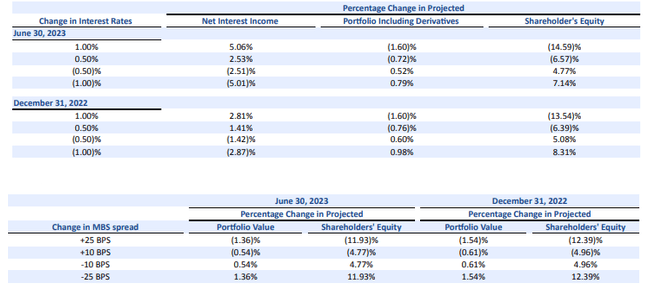

The 10-year Treasury rate has risen by about 80 bps over Q3, while average 30-year mortgage rates have increased by around 65 bps. Thus, the "mortgage spread" has fallen by potentially 15 bps, which is difficult to say because the mortgage rate data is not live. To estimate changes in book value, we can use ARMOUR sensitivity tables from its Q2 report:

ARMOUR Interest Rate Sensitivity (ARMOUR 10-Q Q2 2023)

{kind=link}

A 1% increase in interest rates is associated with a 14.6% decline in ARR's book value, so an 80 bps increase implies a ~11.7% book value decline. That said, the mortgage spread has likely declined over Q3, potentially by around 15 bps, implying a ~7.5% gain in ARR book value. This equates to a -4.2% equity loss; however, I will estimate it at 5% because I believe the mortgage rate data is slightly delayed, potentially failing to account for the rate spike over the past week.

Keep Management Fees in Mind

ARMOUR is externally managed, and, luckily, its fees are based on equity, not assets, so its increase in leverage should be a strategic decision (some other externally managed REITs have excess leverage potentially to increase AUM fees). Still, ARMOUR's management fee per year is currently ~2.95% of equity ( 10-Q pg. 19 ), which is certainly not a small amount. However, it has voluntarily waived a portion of that fee over recent years due to its significant losses. Including management fees and compensation, accounting for its fee waiver, annualized total fees equate to ~$36M. Including its own operating costs, which is also effectively a management fee, this figure would be closer to $45M. Thus, its total operating costs after waivers are about 3.5% of its current tangible book value per year. While its net operating income is well above that figure, I still believe this is a high cost, given its poor historical performance.

What is ARMOUR Worth Today?

Considering the estimated 5% in book value losses, I believe ARR's Q3 book value per share should be around ~$5.9. Its current price is $4.25, giving it an estimated price-to-book of ~0.72X. Historically, that is about the average valuation for the company. Of course, its price-to-book ratio is volatile, generally fluctuating with changes to its earnings per share. See below:

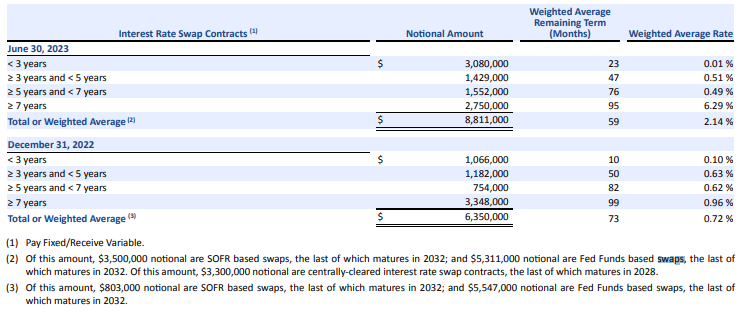

ARMOUR's EPS is negative TTM due to unhedged losses on its securities positions, but I believe it will be positive for at least the next year, as long as mortgage rates do not rise much faster than Treasuries. ARMOUR's net interest income should be negative because short-term borrowing costs are generally well above the fixed rate paid on its mortgage assets purchased before ~2022. However, it has also hedged a significant portion of its borrowing costs, as seen in its swap portfolio below:

ARMOUR Swap Portfolio Q2 2023 (ARR 10-Q Q2 2023)

{kind=link}

These swaps dramatically lower ARMOUR's borrowing cost. At the end of Q2, its weighted average asset yield was 4.24% compared to a 5.17% interest expense on repurchase agreements. After derivatives, its net cost of funds was just 2.49%, giving it a 1.75% net interest margin, in line with its historical average range (these data are seen on its 10-Q pg. 35. ). With a $11.75B securities portfolio, its annual net interest income (after derivatives) should be around $200M, or about $143M distributable after all other expenses and preferred dividends.

Now, estimating a year forward, we can assume that about 60% of its $3.08B swaps with <3 year maturities will mature (current weighted-average term 20 months - subtracting three months from 23 months in Q2); that change will cause ~$1.85B of its existing swaps to see payment rates rise to the current short-term rate of ~5.5% (assuming no rate cuts by then), adding about $100M in interest costs. This should lower its net interest income after derivatives from around $200M to about $100M annualized. This equates to about $53M in estimated distributable annual funds.

Moving two years forward, all of its zero-rate swaps will have expired, meaning ~$3.08B of its liabilities will cost 5.5%, assuming the Federal Reserve has not cut interest rates by then. The 2-year Treasury rate is 5.05% today, implying minor interest rate cuts by then. I will use that to estimate its future interest costs, as it may be unreasonable to assume no rate cuts. A 5.05% rate on $3.08B in debt would add ~$156M in realized costs for ARMOUR. That would push its distributable income to below zero by around mid-2025.

After that point, if the Federal funds rate remains high, ARMOUR should have chronically negative income after its derivative swap positions. Still, I expect ARMOUR will need to reduce its dividend in Q4 of this year or Q1 of 2024. At the end of 2022, its <3 year swaps had a maturity of 10 months, implying a solid amount of swaps are expiring around today. Thus, my "forward year estimate" of $65M in distributable annual income is more weighted toward the next quarter or two than later in 2024. So, its net income should fall in Q3-Q1 2024, stabilize for most of 2024, and then decline again in 2025.

Obviously, this estimate assumes no change in ARMOUR's portfolio. ARMOUR's managers may sell equity to buy higher-yielding assets; however, I doubt that because its equity is below its book value. Of course, ARMOUR may also sell its securities and repurchase newer ones at higher yields, but that should not change the outlook for its net income too dramatically. Still, my estimates should not be viewed as concrete, as I am not privy to all the necessary data to give a very detailed outlook; however, what is clear to me is that ARMOUR's distributable income should fall by around $25M per quarter from Q3 2023 to sometime in 2024. This change should cut its dividend in half (~$50M quarterly today), assuming ARMOUR changes its dividend with its income level, as is usually the case for REITs due to their tax structure.

The Bottom Line

Investors today should not purchase ARMOUR, assuming it will pay a 22.5% dividend yield over the next year. After we adjust its net income outlook for the estimated maturity of its swap portfolio, it appears that its net income payable to shareholders should fall by over half over the coming quarters. Thus, I believe its forward dividend yield is likely closer to 10% , based on the net interest cost outlook from above. Roughly 20 months from now, I estimate that ARMOUR's distributable income will reach zero unless the Federal Reserve reduces interest rates below 5%. If we assume the yield curve predicts future Fed funds rates accurately, then it is clear that ARMOUR's net interest margin (after derivatives) will be chronically negative by ~2025.

Now, does this necessarily make ARMOUR a future bankruptcy? Not necessarily. For one, declining mortgage spreads or Treasury rates could rapidly restore its book value. That would not fix its net interest margin issue and would likely worsen it. However, a rapid reduction in the Federal funds rate, ideally below 4%, would restore ARMOUR's long-term potential. The best outcome for ARMOUR would be a decline in long-term and short-term interest rates, improving its book value and net margin outlook. Significantly, reducing mortgage rates should not increase prepayment pressures on ARMOUR as long as it does not reallocate into higher-yielding MBS securities created this year. That change would improve its NIM outlook to an extent but increase its prepayment risk because homeowners borrowing at 7% today will likely race to refinance their rates fall back below 4%.

Overall, I remain bearish on ARR but am now slightly bearish instead of "very bearish." To me, ARMOUR's ability to survive past 2024 is very questionable as long as the Fed funds rate is above 4-5%, and there are no indications that it will fall below that level quickly enough. Of course, in a standard disinflationary recession, it is common for the entire yield curve to shift lower, a potential that would likely save and restore ARMOUR. Conversely, a rebound in oil prices that increases the inflation outlook pushing the entire yield curve up, could cause ARMOUR to fail sooner than expected. Finally, with no change in the yield curve, I expect ARMOUR will need to cut its dividend dramatically sometime in the coming quarters, making it a relatively weak value investment. Still, its price-to-book ratio is low, and its recent decline seems to overestimate book value losses, so, to me, ARR certainly does not appear overvalued on a short-term basis.

For further details see:

Armour Residential: ~50% Dividend Cut Expected By 2024 As Swaps Expire