ARR - Armour Residential: No Repo Play No Problem

2023-08-31 12:25:40 ET

Summary

- Armour Residential REIT, Inc.'s active portfolio is holding up well despite a lack of new repo trade opportunities.

- We are generally bearish on cyclical credit; however, we believe a heterogeneous opportunity exists in Armour due to its solid execution.

- A promising haircut line coupled with sound asset yields and receding prepayment risk provides encouragement.

- Proven tail risk and the fund's cyclical dividends are risk factors. Nonetheless, its current risk-return attribution seems solid.

I have to admit that Armour Residential REIT, Inc.'s ( ARR ) announced reverse stock split was the initial draw that led to today's analysis. Although the article discusses the event, I wanted to focus on the mortgage real estate investment trust's, or REIT's, repo model and prepayment risk as a baseline.

The topsy-turvy real estate credit market means Armour Residential provides an exciting talking point. Let's delve into a few of our recently discovered factors pertaining to Armour Residential REIT.

Portfolio Assessed

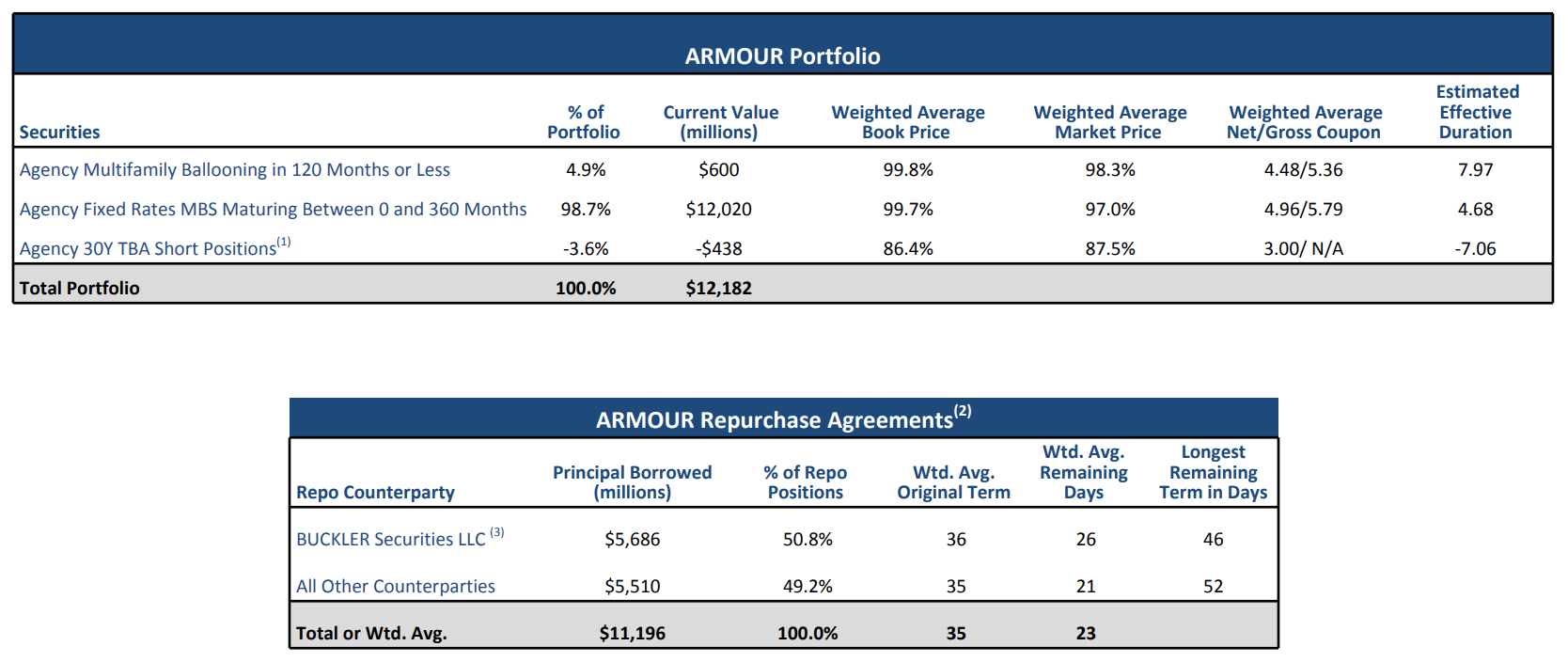

To start off, let's look at Armour's portfolio.

The REIT hosts about $12.02 billion in fixed-rate Mortgage-Backed Securities Maturing Between 0 and 360 months, which comprises 98.7% of its portfolio.

In our view, Armour Residential probably locked in many fixed income opportunities at the substantially high mortgage rates experienced in the past year. In isolation, such opportunities might provide lucrative cash flows for years to come. Although it is not explicitly stated how many securities were purchased in the high-rate environment, we think the vehicle's high turnover (via its active management strategy) allowed it to circle into high cash flow trades in the past year.

{kind=link}

A noteworthy part of Armour's portfolio is its $600 million short position in Agency 30-year "To Be Announced" securities. I want to highlight that $500 million of the line items is a short position in Fannie Mae TBAs; however, it isn't a standalone short position as capital has been reallocated to commercial MBSs' under the DUS program with a horizon of 9.5/10 years (10-year underlying loan accompanied by a 9.5 year settlement period).

In my view, this is a down-duration move and not a speculative play. Therefore, I wouldn't say that additional risk has been onboarded by the majority of Armour's short positions.

Repo Trade

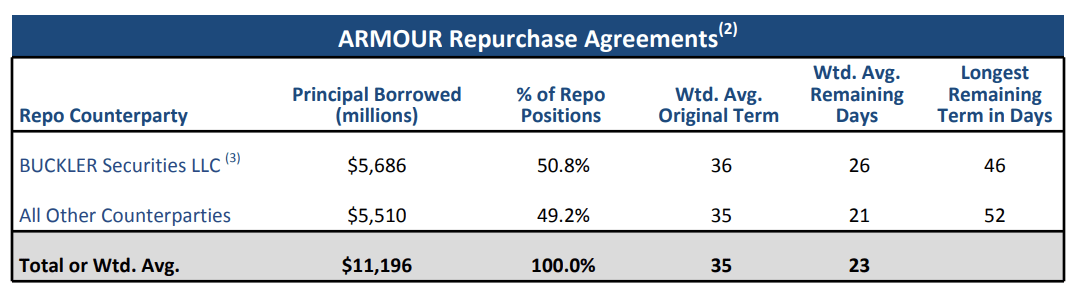

The repo trade, which involves investing in long-dated credit while borrowing (via short positions) in short durations, is a well-known active management technique that Armour has traditionally executed with efficiency.

Armour possesses $11.196 billion in repo borrowings with a weighted remaining days figure between 21 and 26, which is much shorter than its long positions, which possess effective durations between 4.68 and 7.97 years.

{kind=link}

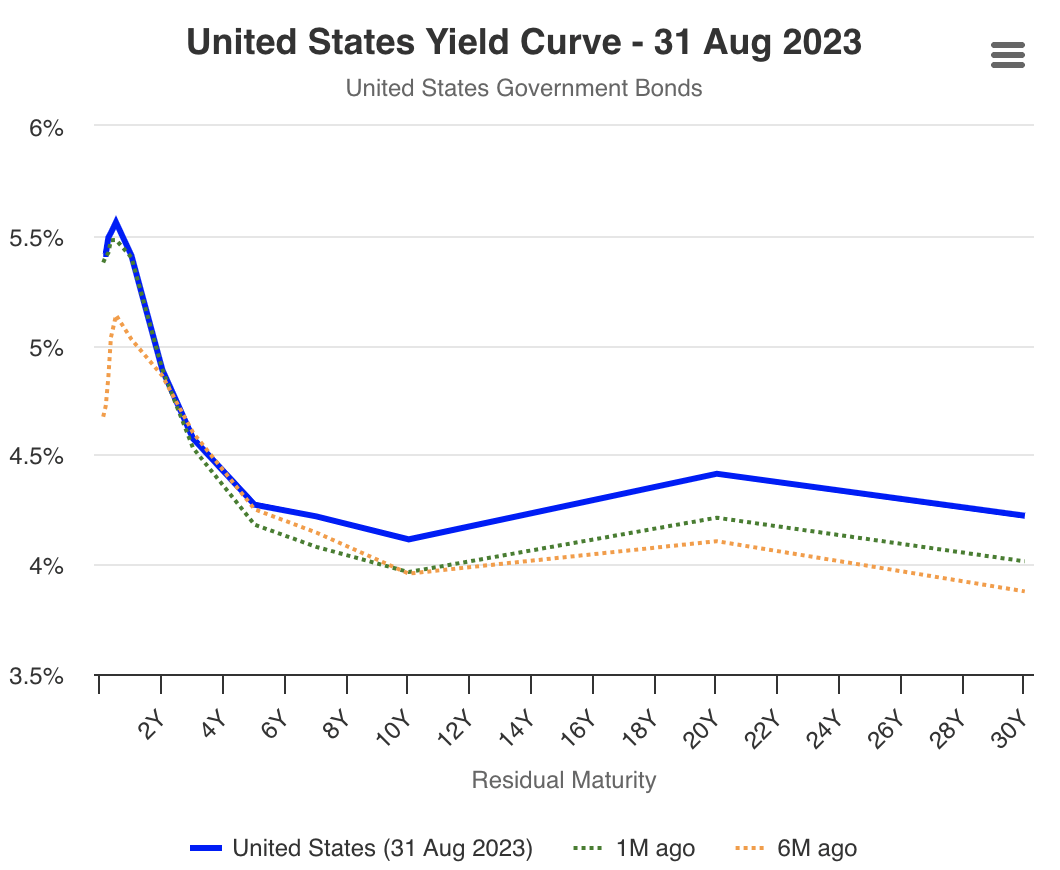

At face value, the repo trade possesses no real price gain opportunities for the time being, with the yield curve's slope and curvature being the main issue. As shown below, the curve is inverted, with risk premiums at the shorter end extremely high and medium-term premiums exceptionally low.

Sure, the curve's level is high relative to recent years. However, new positions will have to enter at the current level, which is what I am trying to get across.

{kind=link}

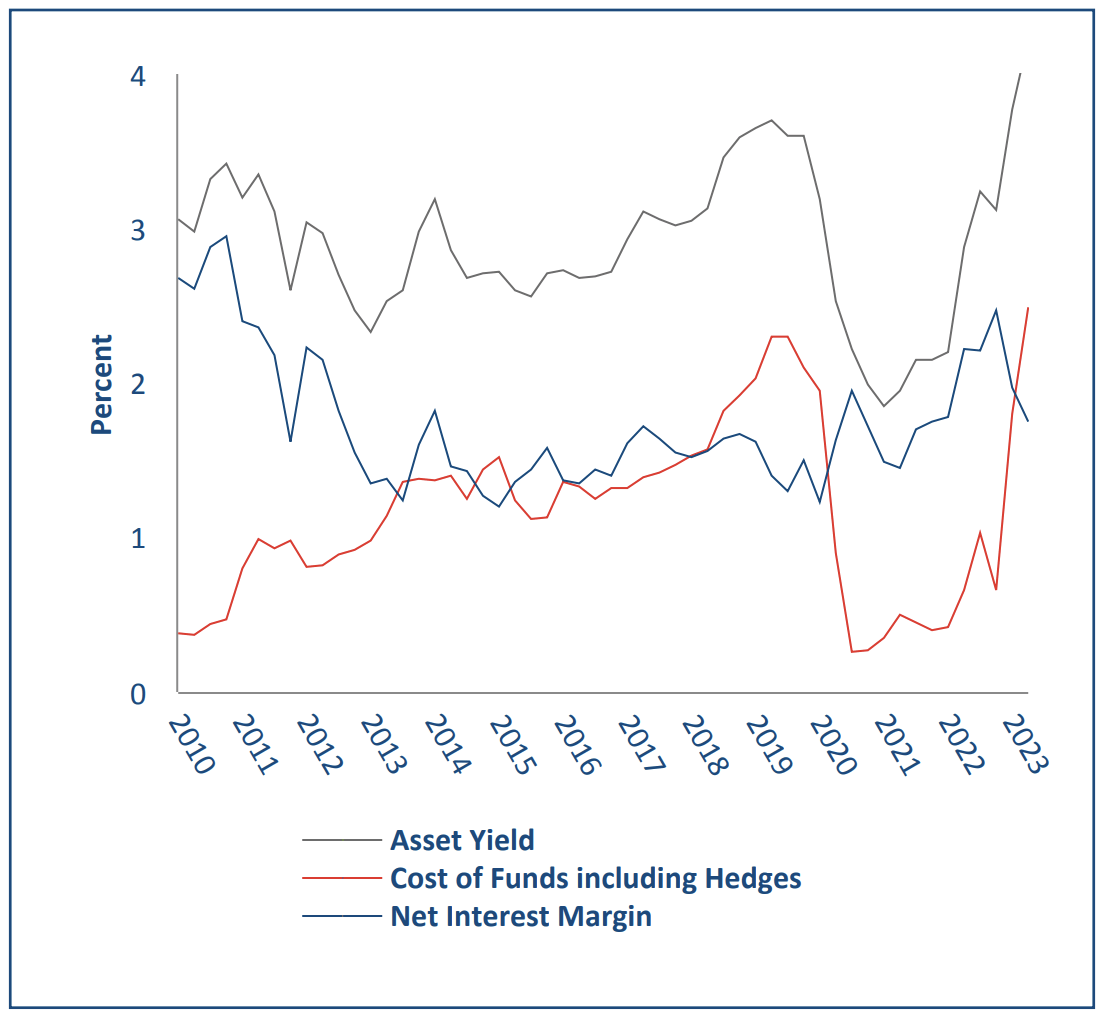

Despite the curve's ongoing inversion, Armour's weighted average haircut on its repo book maintains at a lowish 2.7% while it has been able to capture mortgage rates of as high as 6.8% to 7.2% between November 2022 and July 2023. According to the REIT's Co-CEO, Scott Ulm, assuming constant borrowing rates, Armour will not need to refinance unless mortgage rates fall below 5%.

The diagram below illustrates the divergence between the fund's asset yields and funding costs, which is highly impressive. In my view, a "higher for longer" interest rate environment might require further hedging until interest rates pivot and the curve steepens; nevertheless, although I anticipate most returns to derive from cash flows and not price gains, I think the arbitrage on ARMOUR's positions is in sound territory for the time being.

{kind=link}

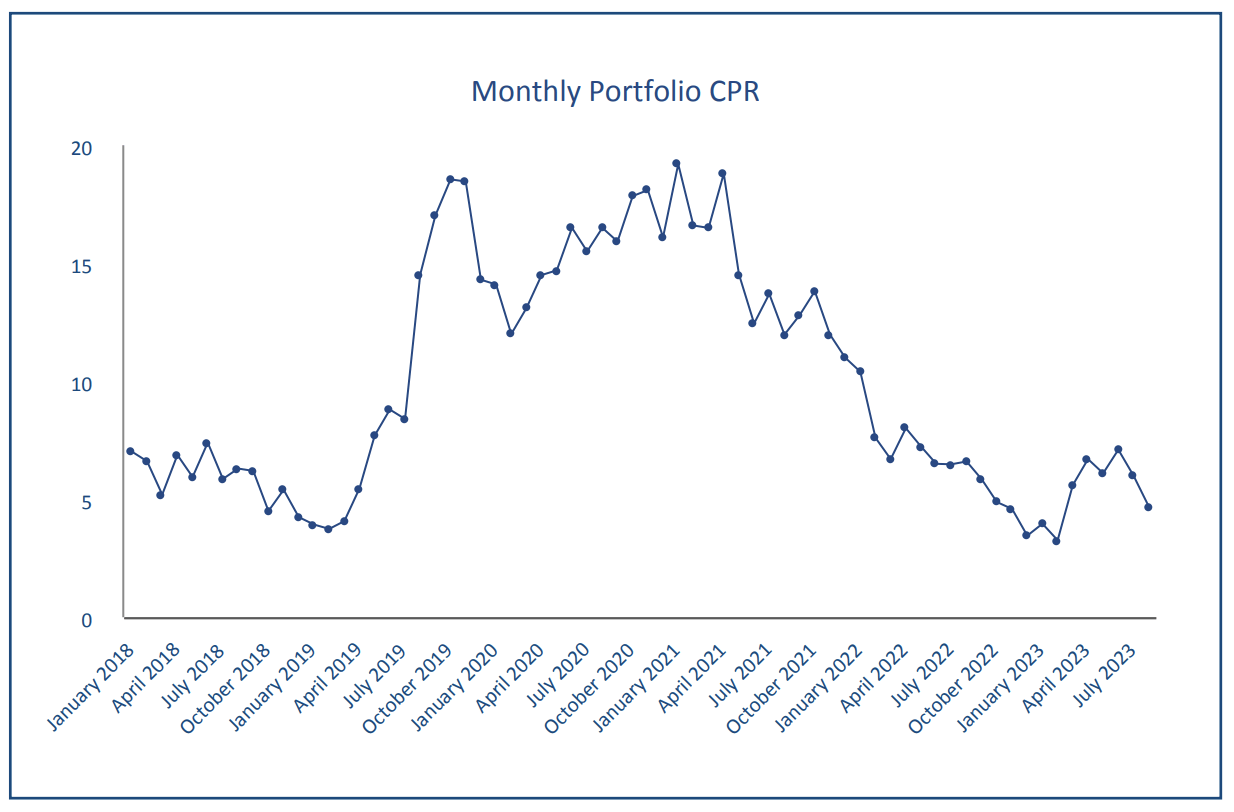

Prepayment and Credit Risk Abating

As shown in the following diagram, Armour's prepayments have receded significantly since the turn of 2021. Lower prepayments make it easier for the fund to project cash flows and concurrently determine its optimal asset-liability exposure. However, investors must consider that lower prepayments can be due to economic risk, which raises counterparty risk.

However, for the time being, we think the lower prepayment risk is well situated, especially as credit risk has started to fade (credit risk is discussed later in the article).

{kind=link}

In my view, the possibility of a hard economic landing shouldn't be overlooked. However, I also believe that much of the U.S.'s recession risk stems from sentiment instead of the nation's production functions. As such, consumers are likely holding back on cyclical spending instead of being unable to spend.

Key data metrics suggest U.S. households are coping with higher inflation and elevated borrowing rates. As such, I believe Armour's counterparty risk will remain within range for now.

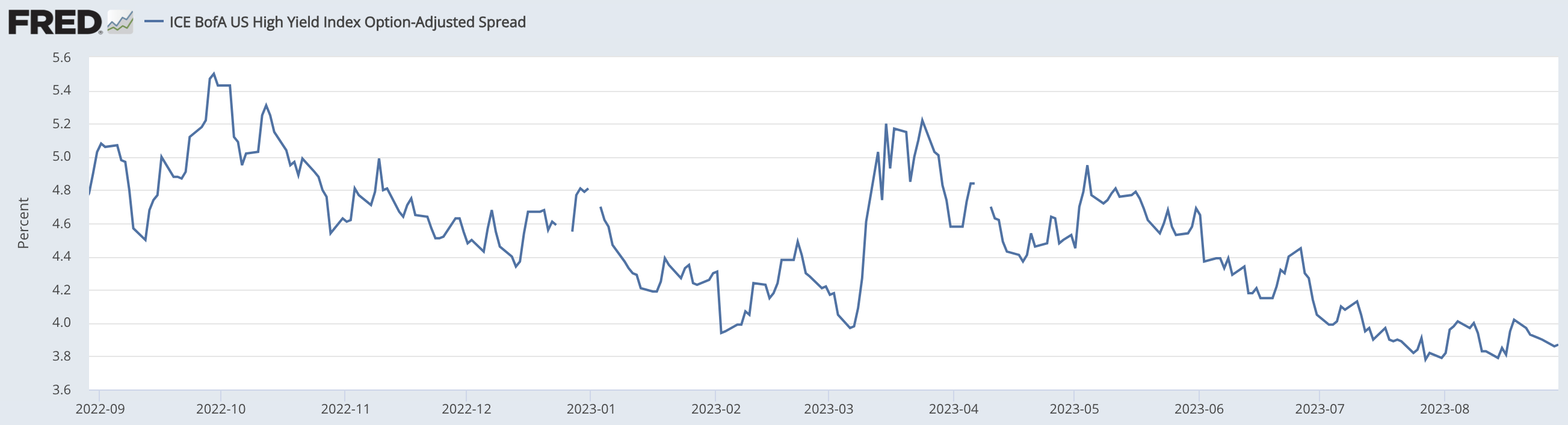

Furthermore, U.S. credit risk is diminishing after a steep rise in Mark after fears of a credit event surfaced due to the Silicon Valley Bank bankruptcy. As an active bond investor, you want to position yourself on expected risk premiums instead of realized risk premiums; however, a continued downtrend in credit risk premiums is highly possible, which might elevate the weighted average valuation of Armour's asset base.

{kind=link}

Shareholder Return Prospects

Returns In-Store and Risks

As shown in the introduction, much of Armour's returns stem from dividends. Thus, cash flow returns are critical.

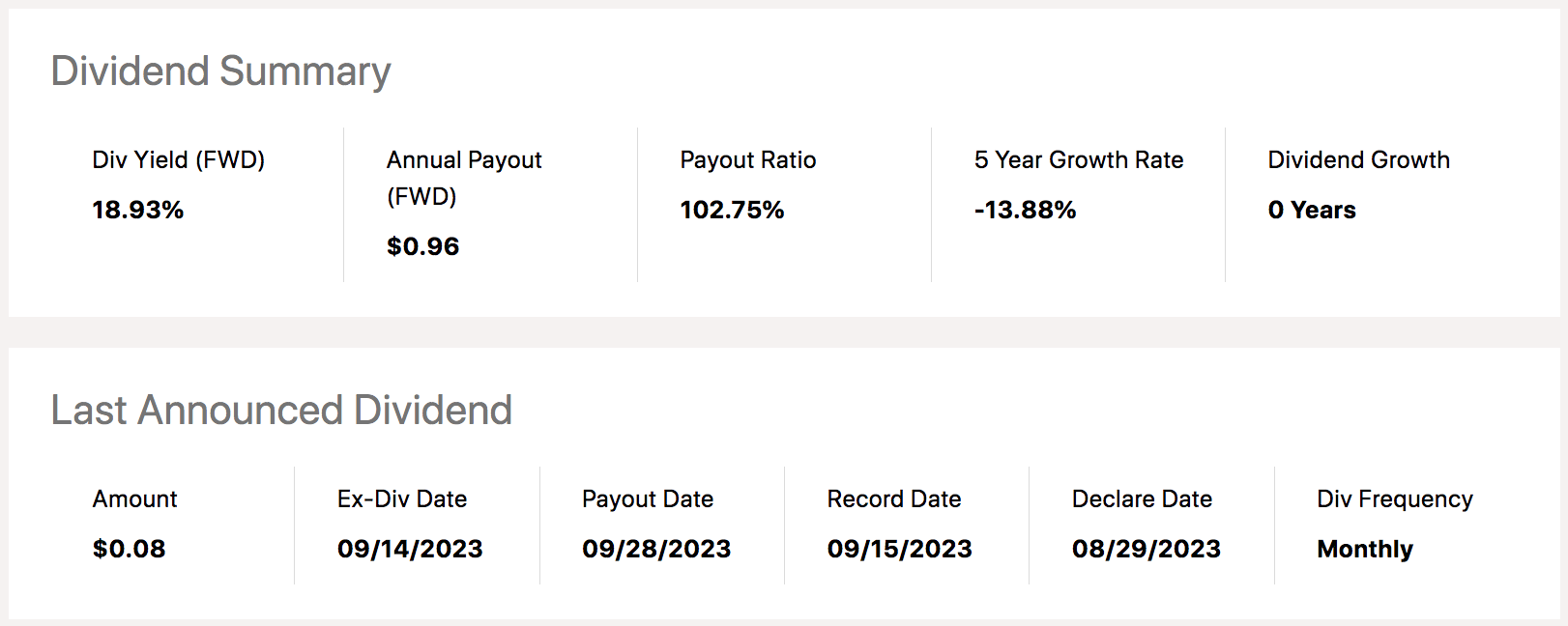

Armour's forward dividend yield of 18.93% and 5-year average yield-on-cost of 4.54% suggest that Armour provides solid dividends throughout the business cycle. Nevertheless, as shown by its realized data, Armour's dividends are cyclical, which is a factor income-seeking investors should consider.

{kind=link}

As also illustrated in the introduction, Armour has achieved negative returns since inception; however, substantial cyclical upticks have occurred. As such, I believe Armour is a dynamic (maybe tactical) play more than anything else.

Considering the earlier fundamental analysis, I believe Armour is set for solid total returns within the next few years; however, I wanted to point out a few systemic risks.

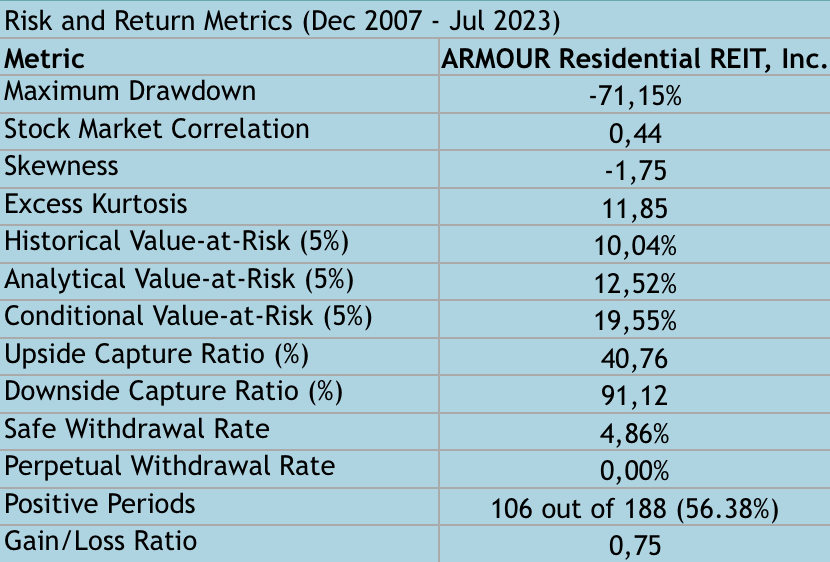

Based on my regression analysis, Armour's net negative returns stem from tail risk. The asset's historical return is negatively distributed, meaning its severe drawdowns are, in most instances, larger than its breakouts. Additionally, the asset has a conditional Value-at-Risk figure that exceeds its historical VaR by an excess of 9.51%; therefore, it is evident that Armour's tail risk is substantial.

{kind=link}

All in all, key indicators suggest Armour presents a solid risk-return profile in the current interest rate environment. As mentioned, it is a risky bet, yet it often provides its investors with lucrative rewards.

DRIP and Reverse Stock Split

In addition to announcing its latest monthly dividend of 8 cents per share , Armour Residential announced a one-for-five reverse stock split as part of its internal value creation plan.

The firm's dividend reinvestment program is used to repurchase stock and reinvest dividends in order to enhance investors' tax efficiency. However, note that you do not have to subscribe to the plan as it is optional.

In addition, keep in mind that the reverse stock split is unlikely to have any economic effect on existing shareholders. It has likely been executed to make the stock more investable and to stem investor interest.

Final Word

Our analysis shows that Armour Residential REIT might present investors with significant upside as a pivot in the credit market is en route. In our view, Armour isn't as homogenous (versus other mortgage REITs) as it seems at face value, as its repo trades haven't suffered from an inverted yield curve as many would have anticipated. Moreover, its fixed cash flow exposure presents lucrative income opportunities.

We believe the asset will provide solid returns to investors willing to ride out temporary economic headwinds.

For further details see:

Armour Residential: No Repo Play, No Problem