REZI - Armstrong World Industries: Upgrade Warranted With Q3 Earnings On The Horizon

2023-10-11 17:53:52 ET

Summary

- Armstrong World Industries, Inc. stock has declined by 9.8% while the S&P 500 has risen 18.5% over the past year, prompting an upgrade of Armstrong from "hold" to "soft buy."

- Recent financial performance shows an increase in revenue and net income, but operating cash flow has weakened.

- Analysts have positive expectations for the upcoming third quarter results, with forecasted improvements in revenue and earnings per share.

Just over a year ago, I found myself taking a rather neutral stance on a company called Armstrong World Industries, Inc. ( AWI ). For those not familiar with the enterprise, it focuses on the production of ceiling systems and other similar offerings. Naturally, this means that the firm is heavily tied to the construction industry. Because of how the stock was priced back then, I was naturally drawn to it and its prospects. However, it was also around that time that I started to become truly worried about the residential construction industry. Only a small portion of the company's revenue comes from residential construction activities. However, I have also been incredibly worried about exposure to office properties.

The office space is facing some major headwinds. The last I checked, vacancy rates across the country were high and still rising . And there's no indication that this picture will get better at any point in the near future. Using the most recent data available , about 30% of sales generated by Armstrong World Industries come from the office vertical. Due to these concerns, I ended up rating the company a "hold" instead of the "buy" I normally would have rated it. Interestingly, the picture ended up being even worse than I thought from a share price perspective.

While recent financial performance for the company has been generally positive and the current outlook as provided by management is bullish, shares have actually declined by 9.8% at a time when the S&P 500 (SP500) has gone up 18.5%. In light of this decline and the impact that it has on the company’s valuation, as well as due to current guidance, I have decided to upgrade my rating on the company from a "hold" to a soft "buy," but that comes with a caveat that we aren't hit with any big surprises when management announces financial results for the third quarter later this month ( expected October 24th pre-market).

Recent performance is mixed but fine

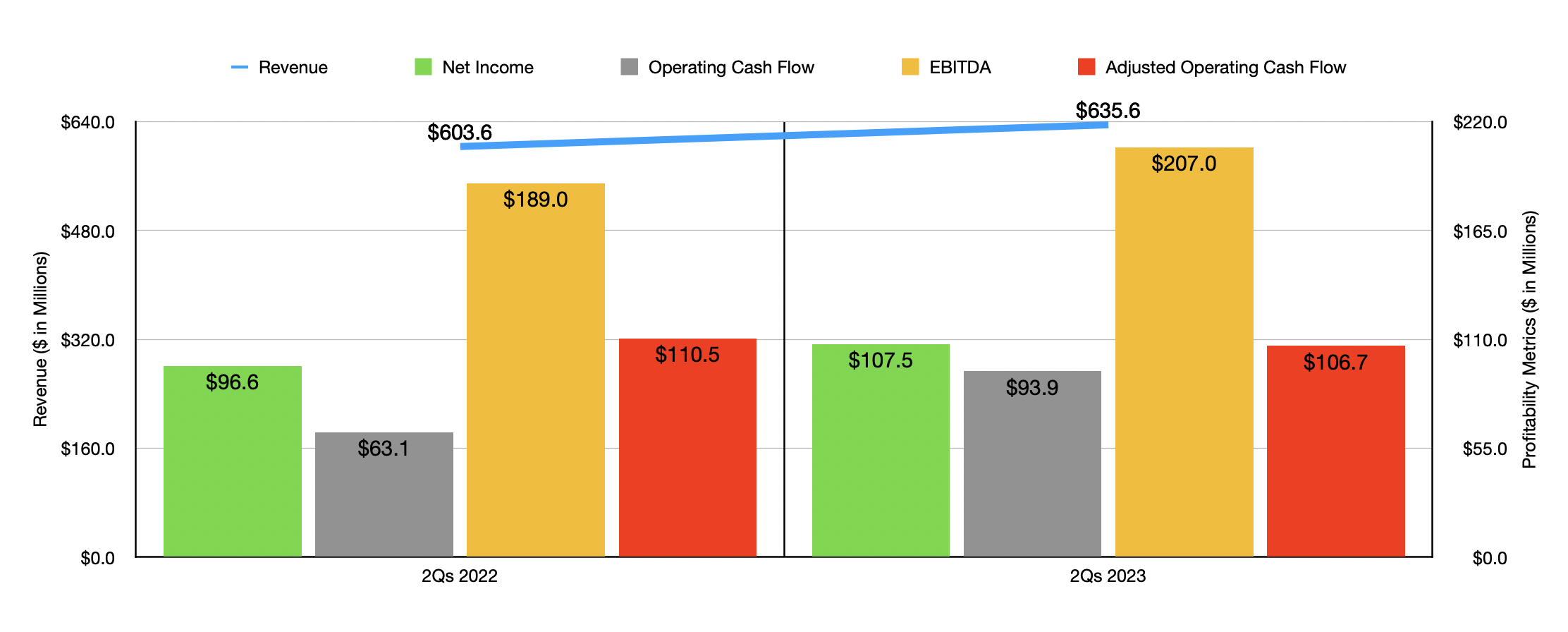

When evaluating Armstrong World Industries, it's likely best to focus on the most recent financial performance figures reported by management. Starting at the top line, revenue in the first half of 2023 came in at $635.6 million. That represents an increase of 5.3% over the $603.6 million the company reported only one year earlier. While the company did benefit from higher volumes of product sold, that increase year over year amounted to only $9 million. Most of the increase, about $23 million in all, came from higher average unit value, which basically means higher average prices on what the company did sell. Most of the improvement came from the larger Mineral Fiber segment, though the company did benefit to the tune of $7 million from the smaller Architectural Specialties segment.

{kind=link}

The bottom line has been a bit more problematic. Net income increased year over year, rising from $96.6 million to $107.5 million. The company was hit by increased costs. A jump in interest expense from $10.9 million to $17.9 million contributed to some of this pain, as did a rise in income tax expense from $30 million to $36.4 million. But these were more than offset by the benefit of higher revenue and a modest improvement in the company's gross profit margin. Operating cash flow also improved, growing from $63.1 million to $93.9 million. But if we adjust for changes in working capital, we get a decline from $110.5 million to $106.7 million. Meanwhile, EBITDA for the company grew from $189 million to $207 million. It would have been nice to see all of these increase across the board. But the adjusted operating cash flow, which is my favorite of the metrics, just had to show some signs of weakening.

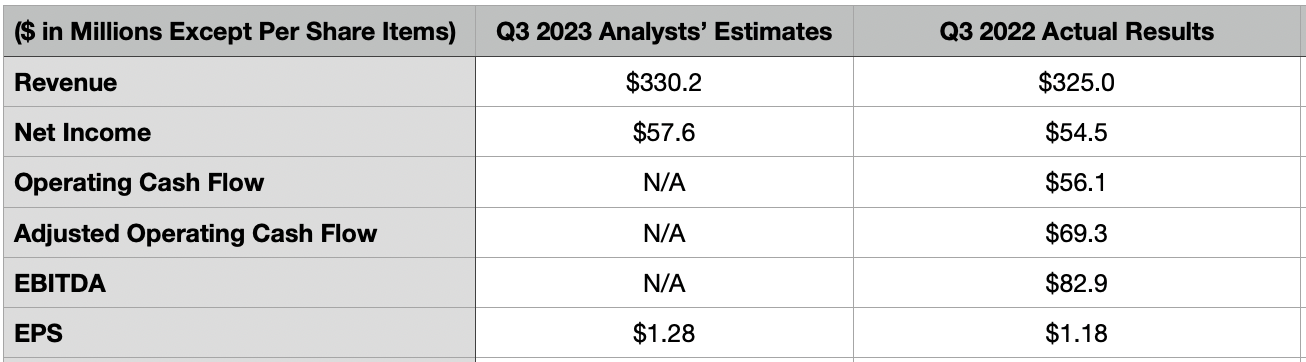

When it comes to the third quarter, which management is going to announce data for before the market opens on October 24th, analysts have generally positive expectations. They're currently anticipating revenue of $330.2 million. If this comes to fruition, it would translate to a 1.6% improvement over the $325 million the company reported in the third quarter of 2022. Earnings per share are forecasted to come in at $1.28. This would be favorable compared to the $1.18 in earnings from continuing operations and the $1.25 in total earnings reported in the third quarter of last year. This would translate to net profits of $57.6 million compared to the $54.5 million the company reported for the same time last year.

{kind=link}

Management has not provided guidance when it comes to other profitability metrics. But understanding what the picture looked like last year will help investors understand the company's performance this time around. During the third quarter of last year, operating cash flow was $56.1 million, while the adjusted figure for this was $69.3 million. And finally, EBITDA for the company came in at $82.9 million.

Investors should pay attention to all of these figures when earnings come out. But they should also be paying attention to the guidance provided by management. After all, current economic conditions are uncertain and the picture can change rather rapidly. Not only do we have economic conditions that can evolve over time, we also have a company that is truly dynamic and changing all the time on its own. As an example, in late July of this year, management completed its acquisition of BOK Modern for an undisclosed sum. That particular purchase will bring in around $12 million in annual revenue. But because we know nothing else about the transaction, we don't know how the firm will be impacted moving forward.

Also in July, management announced a new $500 million share buyback program, increasing its current program to $1.7 billion. With a market capitalization of only $3.19 billion as of this writing, this is a rather sizable maneuver if management ends up acting on it in any material way. And while this wouldn't change anything from a revenue or profit perspective, it could impact per share performance as time goes on.

{kind=link}

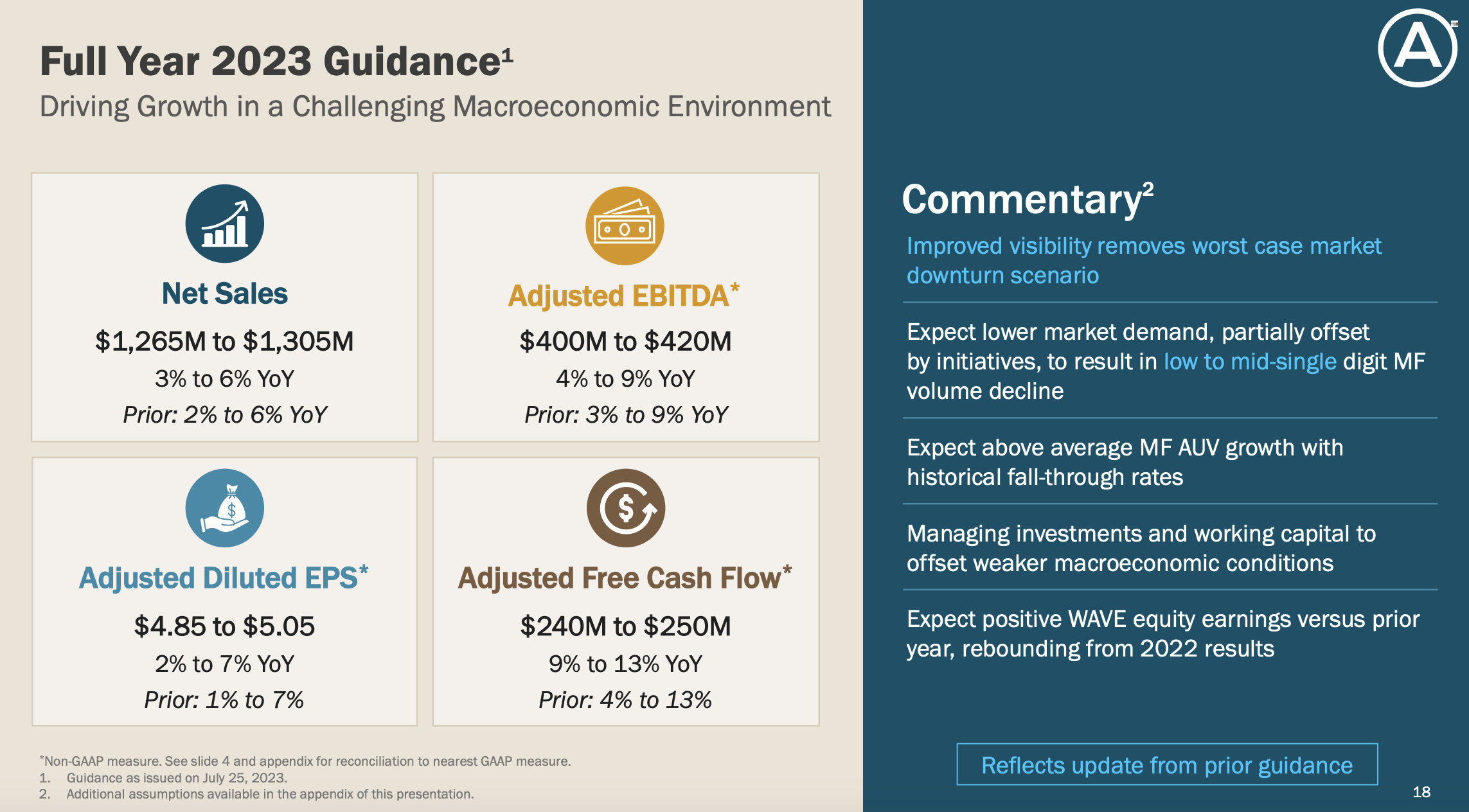

Assuming that we don't see any major changes in guidance, it's likely that Armstrong World Industries we'll generate between $1.265 billion and $1.305 billion in revenue for 2023 in its entirety. Management is forecasting earnings per share of between $4.85 and $5.05, with midpoint guidance implying net profits of $222.8 million. Meanwhile, EBITDA should come in somewhere between $400 million and $420 million. No guidance was given when it came to adjusted operating cash flow. But I estimate that would be around $307.4 million.

{kind=link}

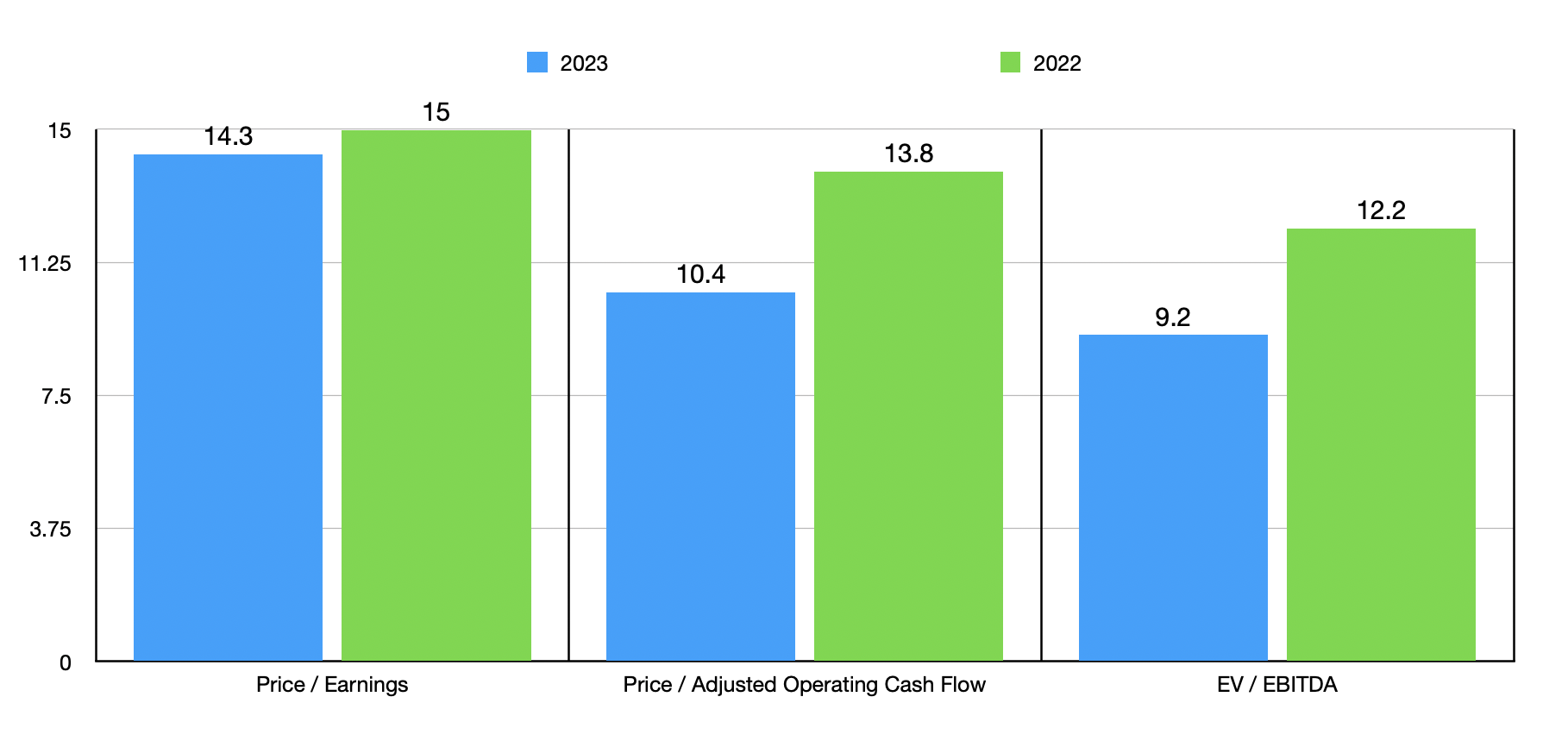

If these numbers do come to fruition, shares of the company look fairly attractive. As you can see in the chart above, the stock does look cheaper on a forward basis than if we were to use data from last year. And in the table below, I compared the enterprise to five similar firms. Using all three metrics, it was cheaper than three of the five companies across the board, while being more expensive than two of them. This makes it slightly on the cheap side relative to similar firms.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Armstrong World Industries |

| 14.3 |

| 10.4 |

| 9.2 |

| Simpson Manufacturing Co. ( SSD ) |

| 18.0 |

| 13.3 |

| 11.5 |

| UFP Industries ( UFPI ) |

| 11.3 |

| 5.9 |

| 6.5 |

| Zurn Elkay Water Solutions ( ZWS ) |

| 89.4 |

| 23.7 |

| 24.7 |

| AAON Inc. ( AAON ) |

| 32.4 |

| 39.2 |

| 21.5 |

| Resideo Technologies ( REZI ) |

| 11.2 |

| 7.9 |

| 6.6 |

Takeaway

Based on the data provided, I must say that Armstrong World Industries strikes me as an interesting prospect. In the past, I was worried about it. But recent performance, continued attractive guidance provided by management, and the fact that shares have fallen, all leave me with a sense of bullishness. Because of economic uncertainty, I wouldn't be surprised to see more volatility in the days, weeks, and months ahead. But for those buying for the long haul, I would say that this is a decent prospect to consider.

For further details see:

Armstrong World Industries: Upgrade Warranted With Q3 Earnings On The Horizon