AANNF - Aroundtown: Despite Depressed Valuation There Is No Rush To Buy

2023-03-30 01:08:06 ET

Summary

- Aroundtown suspended its annual dividend as expected, but its liquidity position is good and was a key reason for a positive share price reaction.

- Its operating performance and property valuations have been more challenging recently, a trend that is likely to maintain in the short term.

- Its depressed valuation seems to already reflect most of its headwinds and fundamental issues.

Aroundtown ( OTCPK:AANNF ) has suspended its dividend related to 2022 earnings as I’ve predicted, but this seems to be already reflected, among other issues, in its depressed valuation. While there is no rush to buy, Aroundtown is cheap enough for contrarian investors to consider entering a position.

As I’ve analyzed in previous articles , I was expecting Aroundtown to follow its peer’s footsteps and cut, or suspend, its annual dividend due to strong headwinds facing the European real estate sector, which the company did today.

Indeed, Aroundtown reported its 2022 financial results and announced a dividend suspension to preserve cash, a move that was not well received by the market initially, given that its share price started trading down by more than 10%, but recovered during the day and closed slightly higher on the day, to a share price of €1.36 in its domestic listing.

This shows that a dividend cut was already priced-in, as Aroundtown’s current valuation is clearly very depressed and is already discounting a lot of potential issues. In this article, I analyze its most recent financial figures and revisit Aroundtown’s investment case.

Earnings Analysis

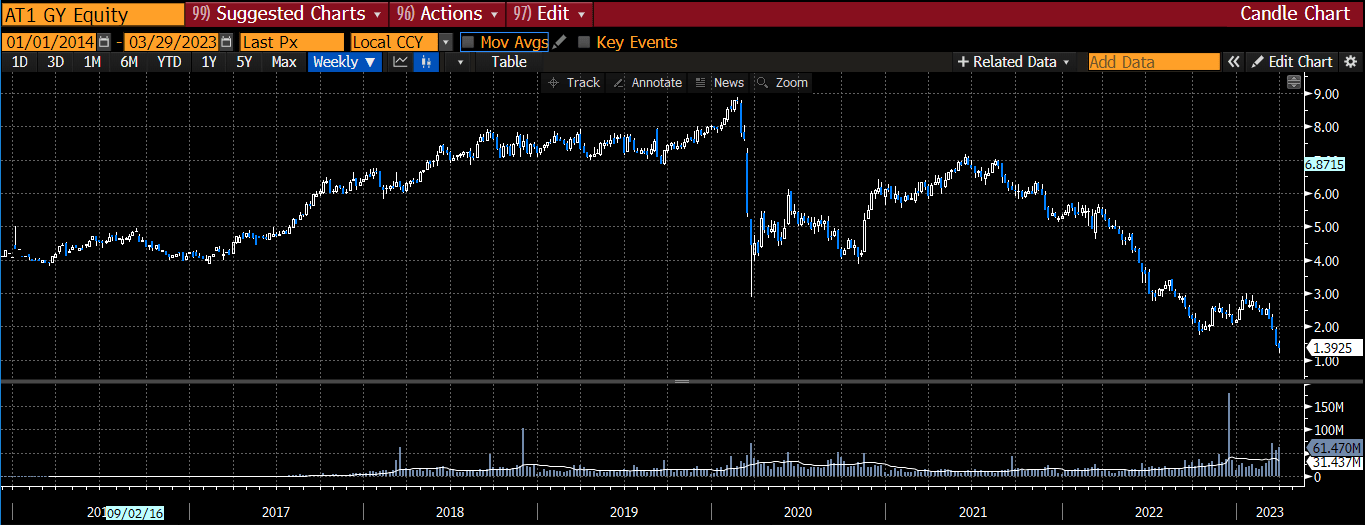

Aroundtown’s operating momentum has been somewhat resilient in recent quarters, even though the operating landscape has deteriorated considerably in recent months, as rising interest rates in Europe resulted in lower valuations, while higher borrowing costs and tighter funding conditions on the capital markets led to much lower transactions and demand for real estate assets. Moreover, investor sentiment was turned negative towards real estate stocks, explaining why Aroundtown’s share price has collapsed by more than 80% since its peak in 2020, and is currently trading near its all-time lows.

{kind=link}

This poor performance is largely explained by Aroundtown’s high leverage, as the company is among the players with higher debt levels in the sector, when including its hybrid bonds. Indeed, its loan-to-value ((LTV)) ratio, a key measure of indebtedness within the European real estate sector, was 40% when accounting only for its senior debt, a ratio that increases to 55% at the end of 2022 when also including hybrid bonds. This ratio is much higher than compared to its closest peers, which have LTVs ratios between 40-45%, putting pressure on Aroundtown to reduce debt during a difficult period.

LTV ratio (Aroundtown)

This means that Aroundtown’s balance sheet is not particularly solid and the company needs to retain cash, both for liquidity purposes and to reduce leverage, explaining its decision to suspend its annual dividend related to 2022 earnings.

This decision was not really a surprise, as I’ve analyzed in a previous article , given that other German real estate companies did the same in recent weeks, including its subsidiary Grand City Properties ( OTCPK:GRNNF ), in which Aroundtown holds 60% of its equity and naturally approved GCP’s decision to suspend its own dividend.

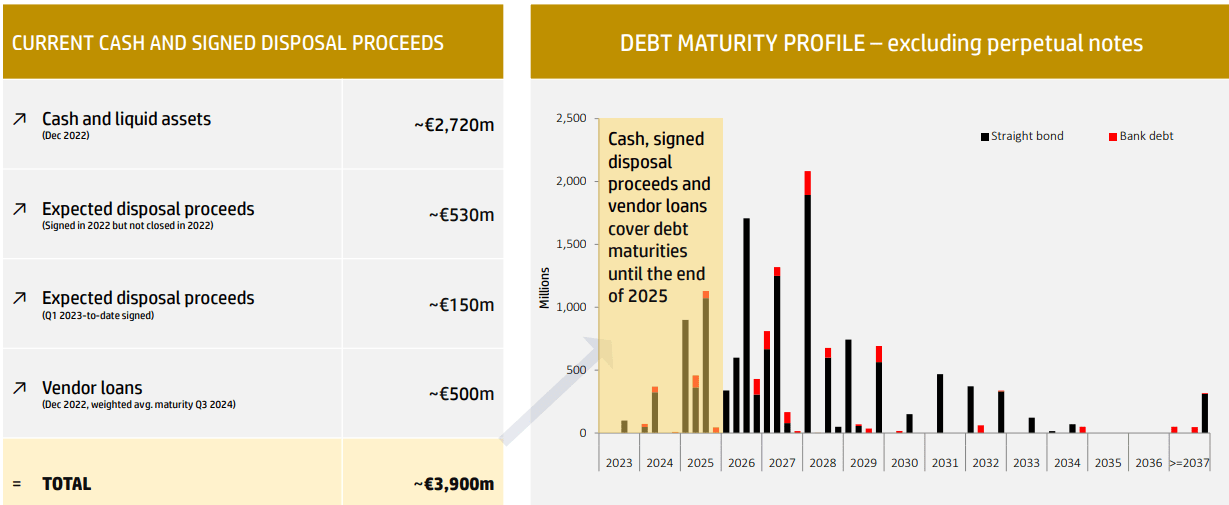

By suspending its annual dividend, Aroundtown saves about €250 million of cash outflow, which in the current operating environment of cash preservation is a considerable amount. Investors should note that its liquidity position at the end of 2022 was about €2.7 billion, thus during ‘normal times’ Aroundtown had plenty of capacity to maintain its dividend, but due to current uncertainties in the economic environment the company decided to be conservative.

This decision is justified by Aroundtown’s high balance sheet leverage and difficult funding conditions, plus a transaction market that is not easy for large transactions, putting its management's focus on cash preservation rather than growing the business.

Indeed, to raise cash and reduce its dependency on capital markets for financing, Aroundtown closed asset sales of €1.6 billion during 2022 , with a profit of about €351 million. Considering that the transaction market has been tough during the past year, this is a positive sign that Aroundtown’s valuations are conservative, and that its assets have good quality. Furthermore, the company was able to sell further properties during the first months of 2023, for a total amount of about €150 million at book value, which is also positive regarding its capability to monetize assets.

Transactions profit (Aroundtown)

Taking into account its €2.7 billion cash position at the end of 2022, plus close to €700 million of cash proceeds expected from pending transactions and €500 million of vender loans, Aroundtown has enough liquidity to cover its loan and bond maturities until the end of 2025. This gives some comfort that a cash crunch is not expected in the next couple of years, plus Aroundtown also announced today a tender offer for some of its bond maturing in 2025 and 2026. It will buy back some of its bonds at distressed prices, which will have a positive impact on its P&L account, and will reduce its refinancing needs in the next three years.

I see these measures as positive for the company to alleviate market fears about potential liquidity issues in the coming years. Moreover, while issuing bonds don’t make much sense right now as the cost of debt is too high, Aroundtown maintains access to bank financing, which is a good sign. In 2022, the company was able to raise €480 million bank debt, plus about €160 million in the first months of 2023.

Additionally, the vast majority of its properties are unencumbered, thus Aroundtown has plenty of room to raise mortgage loans if needed, thus the probability of the company going bankrupt over the medium term seems rather low.

{kind=link}

Regarding its operating performance , it was somewhat mixed as rents continue to perform relatively well, while on the other hand property valuations turned south during the last months of 2022.

Aroundtown revalued its total portfolio at the end of the year, which was valued at closed to €28 billion including GCP, or €24 billion considering GCP at relative consolidation. This valuation represents a decline of 3.1% compared to the end of September 2022, explained by a 5% drop in office values, a 2.1% decline in residential assets, and stable hotel values. Lower valuations are mainly a result of rising interest rates, which increase the cap and discount rates, which were not offset by higher rents. Going forward, Aroundtown expects property values to remain under pressure, with a further decline of 5% expected over the next 12-18 months.

On a more positive note, the company’s rental income increased by 13% YoY during the past year to more than €1.2 billion, which is explained largely by the consolidation of GCP (vs. just one semester in 2021). Therefore, the like-for-like figure is the most relevant metric to use, which increased by 3.5% YoY supported by higher rents in the office and residential segments, while hotels were flat.

In the office segment, Aroundtown has been able to raise rents because the vast majority of its tenants are large corporates and governments, which can accommodate higher costs more easily than smaller companies. Despite that, the vacancy rate increased in this segment to 4.9% (+40 basis points in the year) and the company expects this ratio to increase to 5.5% in 2023, which will put some pressure on rental income. The residential segment is less exposed to economic cycles and reported a vacancy rate of 4.2%, among the lowest in its history, and is not expected to change much in the near future.

On the other hand, its hotel segment continues to be pressured by the effect of the pandemic, as tenants are still recovering from lower travel, especially related to business. While leisure travel has recovered to pre-Covid levels across Europe, the business travel market has not recovered in the same extent, plus Germany has lagged travel related to business, which is not positive for hotel chains.

This explains why its rent collection rate was only 69% in 2022, as collection rates increased throughout the year, from some 40% in Q1 to more than 80% in the last quarter. For 2023, it expects the rent collection rate to be between 85-90%, and a full recovery in 2024. This is positive for its earnings during the next two years, as it will decrease expenses for uncollected rent (€75 million in 2022 and €125 million in 2021).

However, higher expenses and lower capital gains compared to 2021, led to a strong decline in its operating profit (€361 million vs. €1.7 billion in 2021), plus a goodwill impairment of €404 million resulted in a net loss for the year of €457 million (vs. more than €1 billion profit in the previous year). More relevant for real estate companies, its free funds from operations ((FFO)), which strip out gains and losses from asset transactions and revaluations, amounted to €363 million (up by 3% YoY).

FFO (Aroundtown)

Going forward, Aroundtown’s guidance is to generate FFO between €300-330 million in 2023, a decline of 9% to 16% compared to 2023, due to higher financing costs and the effect of disposals, which is not offset by improving collection rates in the hotel segment and higher rents in other segments. Moreover, current economic forecasts expect a flat economy in Germany during 2023, which may be optimistic due to the recent banking crisis that is expected to lead to tighter lending conditions ahead, which will have a negative impact on economic growth over the coming quarters. If economic conditions become more negative than expected, Aroundtown’s guidance may be too optimistic as the office and hotel segments are more cyclical and could be under increased pressure.

Conclusion

Aroundtown has reported decent earnings considering the difficult operating environment and its liquidity position was a good surprise, which was a key reason in my opinion why the market reacted well today despite its decision to not pay a dividend related to 2022 earnings.

While there are many headwinds and an operating turnaround is not likely in the short term, its current depressed valuation of only 0.15x net asset value seems to be too harsh. This means Aroundtown stock may offer value for contrarian long-term investors right now, even though I think investors should continue to follow its equity story and there is no rush to buy.

For further details see:

Aroundtown: Despite Depressed Valuation, There Is No Rush To Buy