ARWR - Arrowhead Pharmaceuticals: A High-Risk High-Reward Bet

2023-10-26 01:47:29 ET

Summary

- Arrowhead Pharmaceuticals presents a complex investment opportunity with substantial risks and significant growth prospects.

- Despite revenue volatility and escalating operational costs, the company has a strong cash reserve and partnerships for financial stability.

- The company's revenue growth has been slowing down recently.

- The company is trading at a high Price/Book multiple of 7.4x.

Investment Thesis:

Arrowhead Pharmaceuticals ( ARWR ) presents a complex investment opportunity, characterized by both substantial risks and significant growth prospects. Despite its innovative focus on RNAi technologies in a rapidly expanding market, the company grapples with revenue volatility and escalating operational costs, casting shadows on its long-term financial sustainability. Although the firm boasts a robust cash reserve that provides a financial cushion for the next 4-5 years, the increasing long-term liabilities indicate a riskier capital structure. While the promising RNAi market and the company's diversified product portfolio offer potential high rewards, the inherent risks in drug development and clinical trials add layers of complexity to the investment decision.

Moreover, the earnings forecast for Q4 2023 shows mixed signals. While the Average Revenue Forecast grew by about 3.4%, the Median Revenue Forecast contracted by 18.4%. Both Average and Median EPS Forecasts showed a contraction, adding another layer of complexity to the investment decision.

Given these dynamics, including the mixed Q4 earnings forecast, a "Hold" recommendation seems the right choice for investors, particularly those with a risk-tolerant, long-term investment strategy.

Overview

Arrowhead Pharmaceuticals has strategically positioned itself in the biotech industry with a concentrated focus on RNAi technologies. Arrowhead aims to have 20 clinically tested or commercially available products by 2025, which is an aggressive but achievable target considering the company's proprietary TRiM platform designed for expedited drug development.

Financially, Arrowhead has raised nearly $1 billion through partnerships over the past six years and has not raised equity capital in the last 3.5 years. Arrowhead Pharmaceuticals has forged strategic partnerships with GSK ( GSK ) and Takeda ( TAK ) to accelerate drug development and secure substantial funding. The company's collaboration with GSK led to the initiation of a Phase IIb clinical trial for GSK4532990, a drug aimed at treating Non-Alcoholic Steatohepatitis ((NASH)). This significant milestone resulted in a $30 million payment to Arrowhead Pharmaceuticals. The company's partnership with Takeda facilitated the launch of the Phase III REDWOOD trial for Fazirsiran, designed to combat Alpha-1 Antitrypsin Deficiency liver disease. This led to a $40 million milestone payment from Takeda to Arrowhead Pharmaceuticals. In total, these partnerships have brought in $70 million in milestone payments. In the biotech industry, the costs of R&D can be high, sometimes requiring upwards of $2.6 billion for a single drug's development , according to the Tufts Center for the Study of Drug Development. Therefore, the capital from these partnerships is crucial for long-term growth and viability. Moreover, the partnerships offer the advantage of shared R&D risks, which is especially crucial when 90% of drugs entering clinical trials fail , thereby contributing to Arrowhead's long-term financial stability and growth prospects.

Despite having cash reserves of $494.5 million, Arrowhead reported a net loss of $102.9 million in Q2 2023. While this may raise concerns, the cash reserves could provide a financial runway for approximately 4-5 more years, assuming a static burn rate. This runway is particularly valuable in the biotech sector, where companies often take between 10 and 15 years to turn a profit due to long R&D cycles and regulatory barriers.

In summary, Arrowhead Pharmaceuticals is a high-risk, high-reward stock. The company has made strategic choices that align with both current and anticipated industry trends, strengthened by financial backing and a diversified portfolio. While the company operates at a net loss, its strong cash reserves offer a degree of financial security, allowing for sustained R&D efforts. The upcoming Phase 3 trials present both a significant risk and potential reward, making them a crucial focal point for the company's future. Given these various factors, Arrowhead Pharmaceuticals presents an investment opportunity that requires close monitoring, especially of clinical trial outcomes and regulatory interactions. These will be key determinants in the company's long-term success or failure.

Financial Analysis

{kind=link}

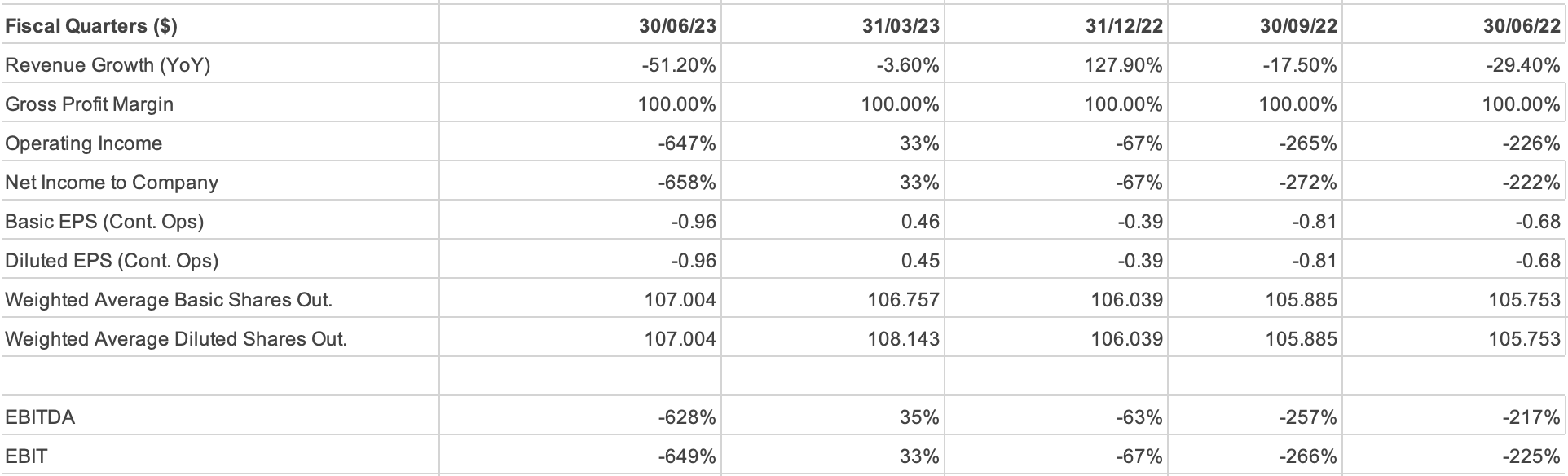

Starting with revenue, Q3 2023 saw a sharp drop to $15.825 million from $32.412 million in Q3 2022, translating to a 51.2% decrease. However, for the nine-month period ending in June 2023, revenue was $224.638 million, a 6.1% increase from the $211.656 million recorded in the same timeframe in 2022. This trend suggests that while revenue might be improving in the long term, the company faces considerable quarter-to-quarter volatility. On the expense side, operating expenses for Q3 2023 were $118.528 million, up by 12.5% from $105.321 million in Q3 2022. For the nine months, these expenses were $321.31 million, marking a 4.9% increase from the $306.333 million in 2022. This increase in operating expenses is a concern, as it outpaces the revenue growth, thereby contributing to higher net losses.

The company's R&D expenses for the third quarter of 2023 were $94.757 million, a 31.2% increase from the $72.180 million spent in Q3 2022. This trend continues when examining the nine-month period ending in June 2023, where R&D expenditures rose to $253.333 million from $213.930 million in the same period the previous year, marking an 18.4% hike. The data suggests two immediate red flags: First, the R&D spending is escalating at a high rate, especially in the most recent quarter. Second, this increase is not accompanied by a proportional rise in revenue, indicating an inefficiency in capital utilization. If this rate of growth in R&D expenses persists, based on the nine-month growth rate, the company could be looking at an R&D budget of around $332 million for the next year. However, this could balloon to $363 million if the Q3 growth rate continues unchecked. These figures bring forward key risks; notably, if these heightened R&D expenses do not yield profitable products, the financial health of the company could be jeopardized. Furthermore, as interest expenses have already started to appear on the financial statements, totaling $13.064 million, this could signify that the company is accruing debt to finance these escalating costs, which could pose solvency risks in the long term.

Specifically, the operating loss for Q3 2023 was $102.703 million, a 40.9% increase from the $72.909 million in Q3 2022. Net loss followed suit, standing at $102.946 million in Q3 2023, a 43% increase from the $72.046 million in Q3 2022. For the nine months, the net loss was $95.596 million, a 5.6% increase from $90.552 million in 2022. This trend of increasing losses, despite the slight revenue growth over nine months, raises questions about the company's ability to manage costs efficiently.

Looking forward, if current trends persist, Arrowhead Pharmaceuticals is likely to face deteriorating financial health with escalating operating expenses and net losses. For instance, if the 6.1% growth in revenue continues, we might expect approximately $238 million in revenue over the next 12 months. However, if operating expenses continue to grow at 4.9%, they could reach around $337 million, and the net loss could hit around $101 million, assuming a 5.6% increase. This raises red flags, such as revenue volatility and escalating expenses and losses.

The revenue growth over the nine-month period is a strength, but the increasing operating expenses and net losses are weaknesses that cannot be overlooked. Opportunities for revenue growth might exist, while the threats include the continual escalation of net losses and operating expenses.

Balance Sheet Analysis

The company experienced a 16% growth in total current assets, increasing from $405.3 million in September 2022 to $470.2 million in June 2023. This growth potentially signals better liquidity but could also hint at underutilized assets, especially when juxtaposed with the company's long-term assets, which also rose by 13.6% from $286.6 million to $325.7 million over the same period. In contrast, total current liabilities fell sharply by 49.4%, going from $138.9 million to $70.2 million. This significant reduction in liabilities drastically improved the company's current ratio from 2.9 to 6.7 and the quick ratio from 2.9 to 6.5. However, this positive change is counterbalanced by a concerning 154.8% hike in long-term liabilities, which surged from $134.8 million to $343.6 million.

This rapid accumulation of debt shifted the debt-to-equity ratio from 0.65 to 1.13, signaling a risky capital structure leaning more towards debt financing. The trend in operating expenses reveals a 4.9% increase, rising to $321.3 million in the nine months ending in June 2023 compared to $306.3 million for the same period in 2022. This operating expense trend, in the context of projected revenue of $238 million for the next 12 months (based on a 6.1% YoY growth), points towards a widening gap between revenue and expenses, which could further escalate the net loss from $95.6 million to an estimated $101 million if the trend persists.

Moreover, the company seems to be investing heavily in infrastructure, as evidenced by a $121.1 million increment in property and equipment. This large capital expenditure indicates a focus on future growth but must be scrutinized against its revenue projections to assess its sustainability. The accounts receivable decreased from $1.41 million to $1.24 million, indicating an improvement in collections and a reduction in credit sales. Cash and cash equivalents also saw a slight dip from $108 million to $105.3 million, pointing to lower liquidity.

In terms of quality of earnings, the sharp spike in long-term liabilities alongside diminishing revenues raises red flags. If the trend of high debt continues, Arrowhead Pharmaceuticals might face solvency issues, casting doubts on its overall financial health. Additionally, the drop in current liabilities might temporarily inflate the current ratio, but the growing long-term liabilities are a concern. The SWOT analysis pinpoints the high current ratio as a strength and the increasing long-term liabilities as a weakness, with the increased CapEx offering potential growth opportunities. However, threats loom in the form of declining revenue and rising liabilities. Given these financial dynamics and potential risks, including a 51.2% drop in Q3 2023 revenue compared to Q3 2022, the investment recommendation for the company would be a "Hold" until more positive financial indicators emerge.

Free Cash Flow Analysis

{kind=link}

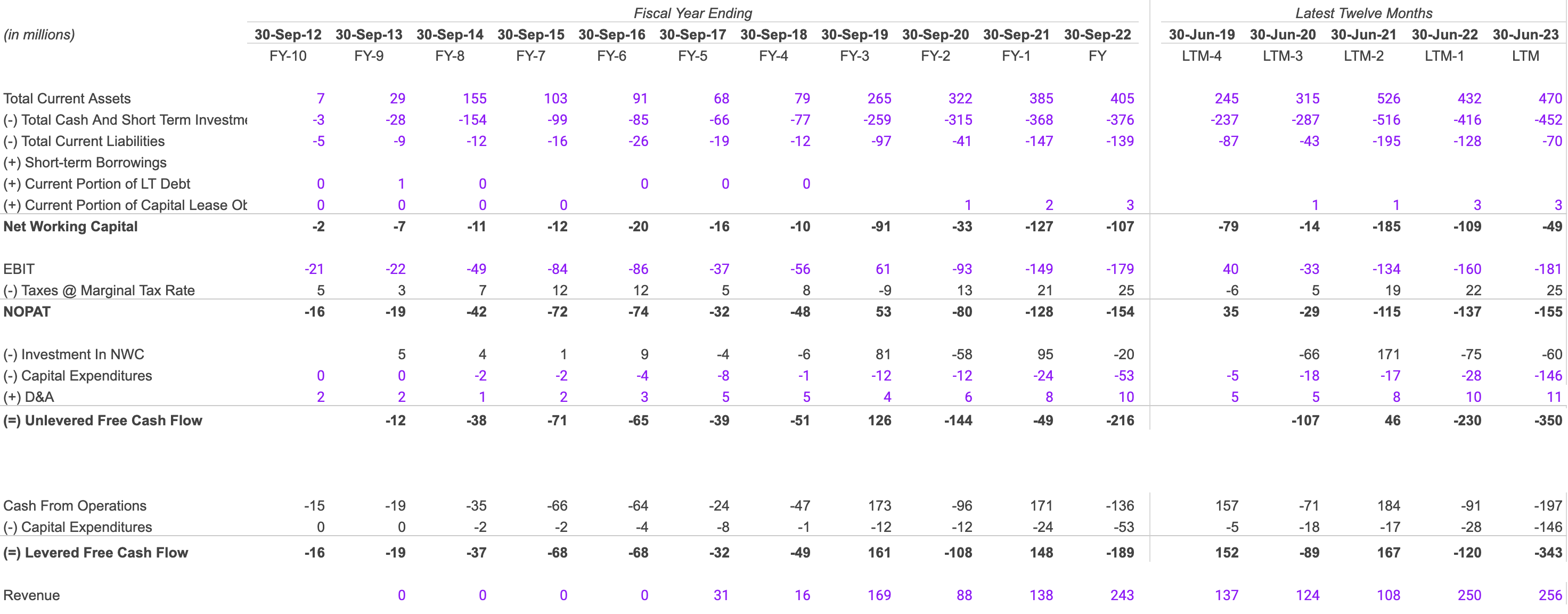

The Net Working Capital has improved over the last three years, from -$185 million in 2021 to -$49 million in 2023. This is a 55.05% improvement from 2022 to 2023, following a 40.54% improvement from 2021 to 2022. This increase in Net Working Capital is a good sign as it points to improved short-term financial health. However, EBIT fell by 19.40% from -$134 million in 2021 to -$160 million in 2022 and declined by another 13.13% to -$181 million in 2023. Similarly, NOPAT slid by 19.13% and 13.14% in 2022 and 2023, landing at -$137 million and -$155 million, respectively. This suggests less money is available for stakeholders and indicates a worsening operational performance.

The Unlevered Free Cash Flow plummeted from $46 million in 2021 to -$350 million in 2023, which is a 52.17% deterioration from the -$230 million in 2022. Levered Free Cash Flow also declined from $167 million in 2021 to -$343 million in 2023, marking a 185.83% decrease from -$120 million in 2022. These negative swings in free cash flows could affect the company's solvency and liquidity.

The sharp declines in EBIT and NOPAT, as well as the negative free cash flows are a red flag. These existing trends, if they persist, forecast a deterioration in EBIT, NOPAT, and negative free cash flows. Even though the revenue growth was robust at 131.48% in 2022 compared to 2021, the decline to a 2.4% growth in 2023 is a concern, potentially pointing to market saturation and increased competition.

The current ratio for 2023 stands at a healthy 6.71, but the quick ratio is a low 0.257. This low quick ratio suggests that, when disregarding inventories, the company might struggle to meet its short-term liabilities. Solvency is also a cause for concern, particularly given the negative EBIT and NOPAT figures. .

A SWOT analysis points out the high current ratio as a strength but underscores the negative EBIT, NOPAT, and cash flows as significant weaknesses. The opportunity lies in the improving Net Working Capital, whereas the threat is the declining operational performance.

Shareholder Yield

{kind=link}

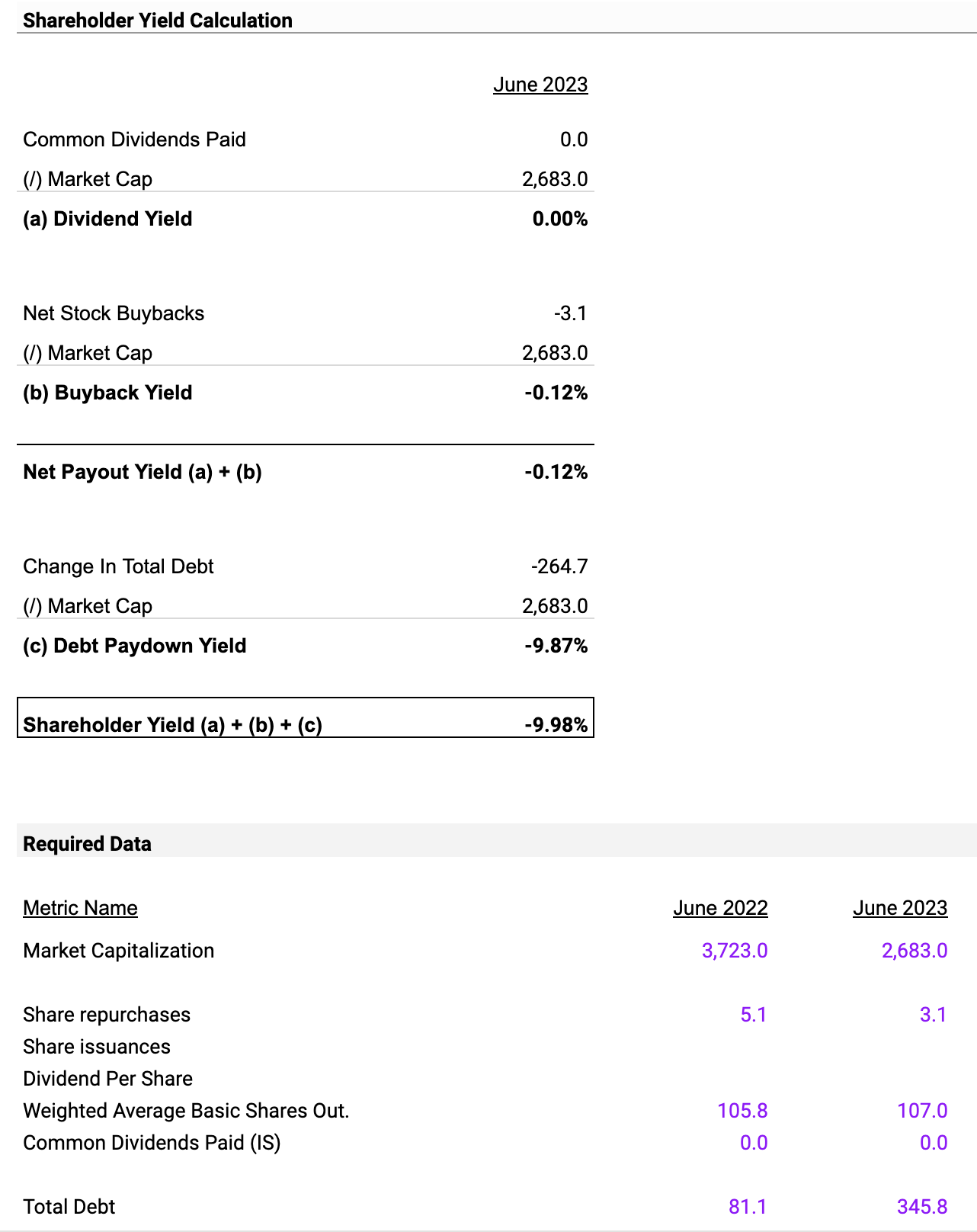

With a Dividend Yield of 0.00%, the company currently does not offer any dividends, making it unattractive for investors looking for dividend-based income. This zero percent yield could indicate that the company isn't generating enough profit to distribute dividends. The Buyback Yield stands at -0.12%, signaling that the company may have issued more shares than it has bought back. This is a direct form of dilution for existing shareholders, and it's crucial as it could lead to a decline in earnings per share, a key metric for company valuation.

The Debt Paydown Yield is at -9.87%, indicating that the company has added its total debt by $264.7 million. Such an uptick in debt levels is risky, as it adds financial burden on the company and could lead to solvency issues in the long run. The increased debt signals that the company is sourcing more capital, possibly to fund expansion, operational requirements and to meet short-term obligations.

The overall Shareholder Yield totals up to -9.98%, which is a concern. It reveals that not only is the company not returning any value to its shareholders through dividends or buybacks, but it is also taking on more debt. This could indicate a riskier financial strategy and should prompt investors to question the company's long-term sustainability and growth plans.

Earnings Preview For Q4 2023

{kind=link}

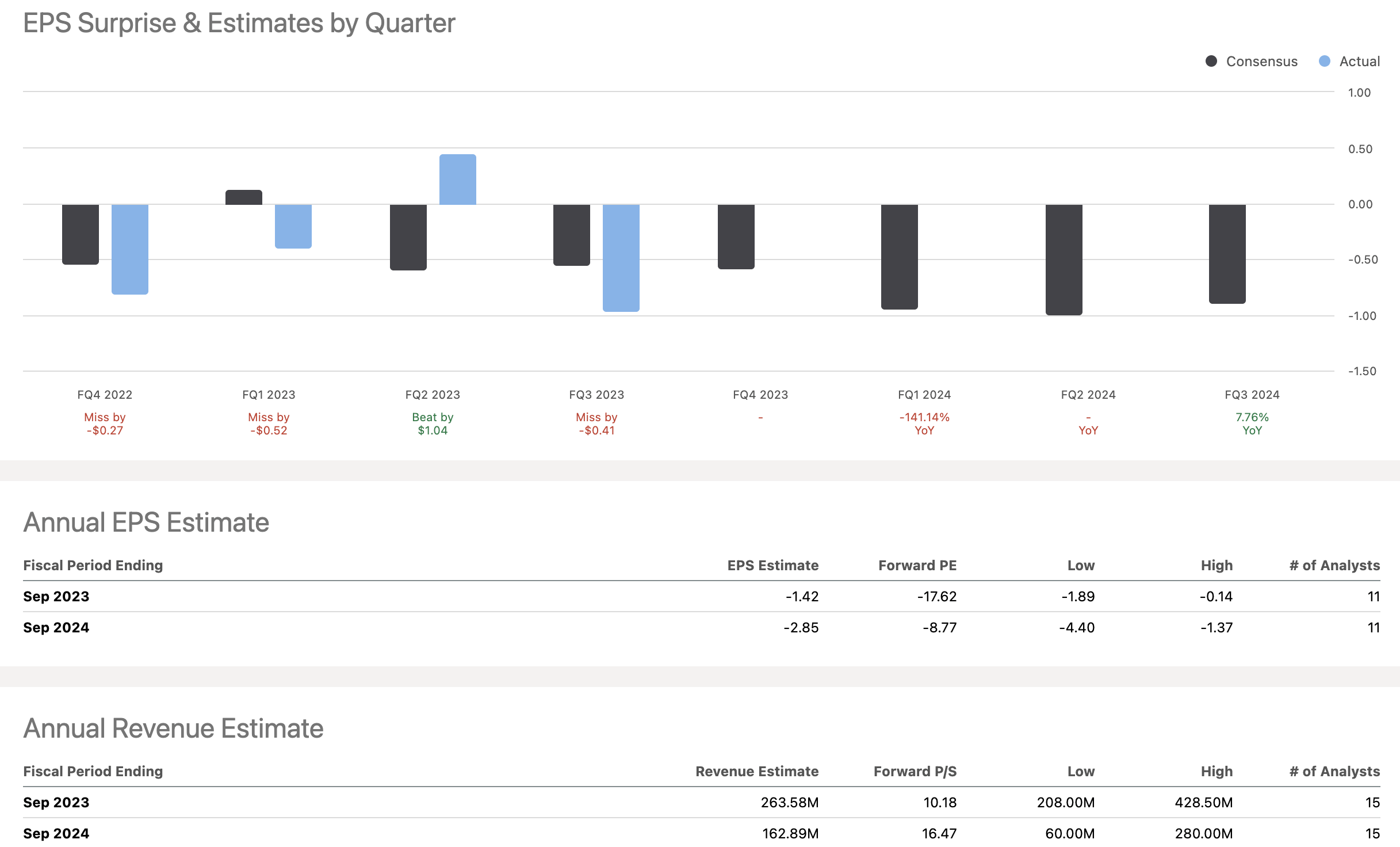

The Average Revenue Forecast saw a minor increase from $45.423 million in June to $46.967 million in September, representing a growth of approximately 3.4%. On the other hand, the Median Revenue Forecast decreased from $40 million in June to $32.65 million in September, marking a contraction of approximately 18.4%.

In terms of Earnings Per Share estimates, the Average Forecast slightly deteriorated from -$0.55 in June to -$0.58 in September, showing a contraction of about 5.5%. The Median EPS Forecast also saw a dip from -$0.69 in June to -$0.73 in September, signifying a contraction of about 5.8%.

To summarize, the period from June to September 2023 shows mixed signals for Arrowhead Pharmaceuticals. While the Average Revenue Forecast grew by 3.4%, the Median Revenue Forecast contracted by 18.4%, suggesting varied outlooks among analysts. Concurrently, both the Average and Median EPS Forecasts contracted by 5.5% and 5.8%, respectively. The revenue and EPS forecasts imply that investors should exercise caution.

Valuation

The Enterprise Value to Revenue (EV/Revenue) metric is a useful valuation tool for a company like Arrowhead Pharmaceuticals, which currently shows a strong focus on revenue growth. Arrowhead has a 5-Year Compound Annual Growth Rate of 50.6% and a 3-Year CAGR of 12.9% in revenue. Given this growth rate, it's logical to evaluate the company based on its revenue-generating capabilities rather than profitability metrics like EBIT, especially since its latest fiscal year EBIT Profit Margin is -73.4%.

{kind=link}

We chose five companies as benchmarks: Inovio Pharmaceuticals, Alnylam Pharmaceuticals, Moderna, Ligand Pharmaceuticals, and Johnson & Johnson. These companies were selected based on their relevance to the biotechnology and pharmaceutical sectors. Additionally, they offer a mix of growth profiles:

-

Inovio Pharmaceuticals ( INO ) : Known for its work in DNA medicines, Inovio has a negative 5-Year CAGR of -24.6%, making it an interesting contrast to Arrowhead.

-

Alnylam Pharmaceuticals ( ALNY ) : Specializing in RNAi therapeutics, Alnylam has a robust 5-Year CAGR of 63.1%, comparable to Arrowhead's growth profile.

-

Moderna ( MRNA ) : Known for its mRNA technology, Moderna has a staggering 3-Year CAGR of 584.7%, which provides an upper limit on growth rates.

-

Ligand Pharmaceuticals ( LGND ) : With a 5-Year CAGR of 6.8%, Ligand offers a more moderate growth profile.

-

Johnson & Johnson ( JNJ ) : As a diversified healthcare giant, J&J provides the large-cap perspective with a 5-Year CAGR of 4.4%.

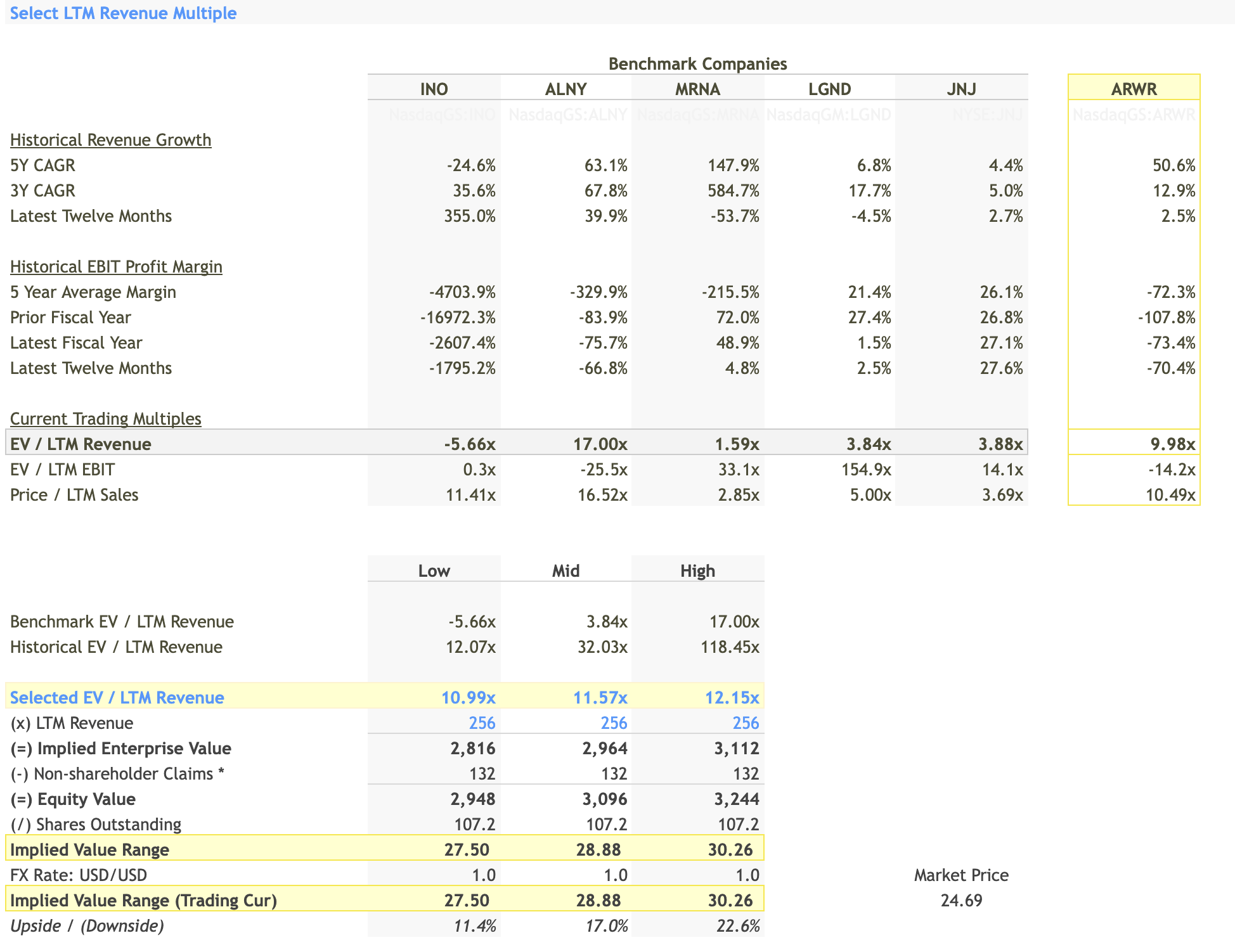

Select LTM Revenue Multiple

{kind=link}

The EV/LTM Revenue multiples for the benchmark companies range from -5.66x for Inovio to 17.00x for Alnylam. For the Last Twelve Months (LTM) Revenue Multiple, Arrowhead’s EV/LTM Revenue is at 9.98x. Given Arrowhead’s strong 5-Year revenue CAGR of 50.6%, this high multiple could be warranted. We selected a range of 10.99x to 12.15x for calculating the fair value. This implies an enterprise value of between $2,816 million to $3,112 million, leading to a stock price range of $27.50 to $30.26.

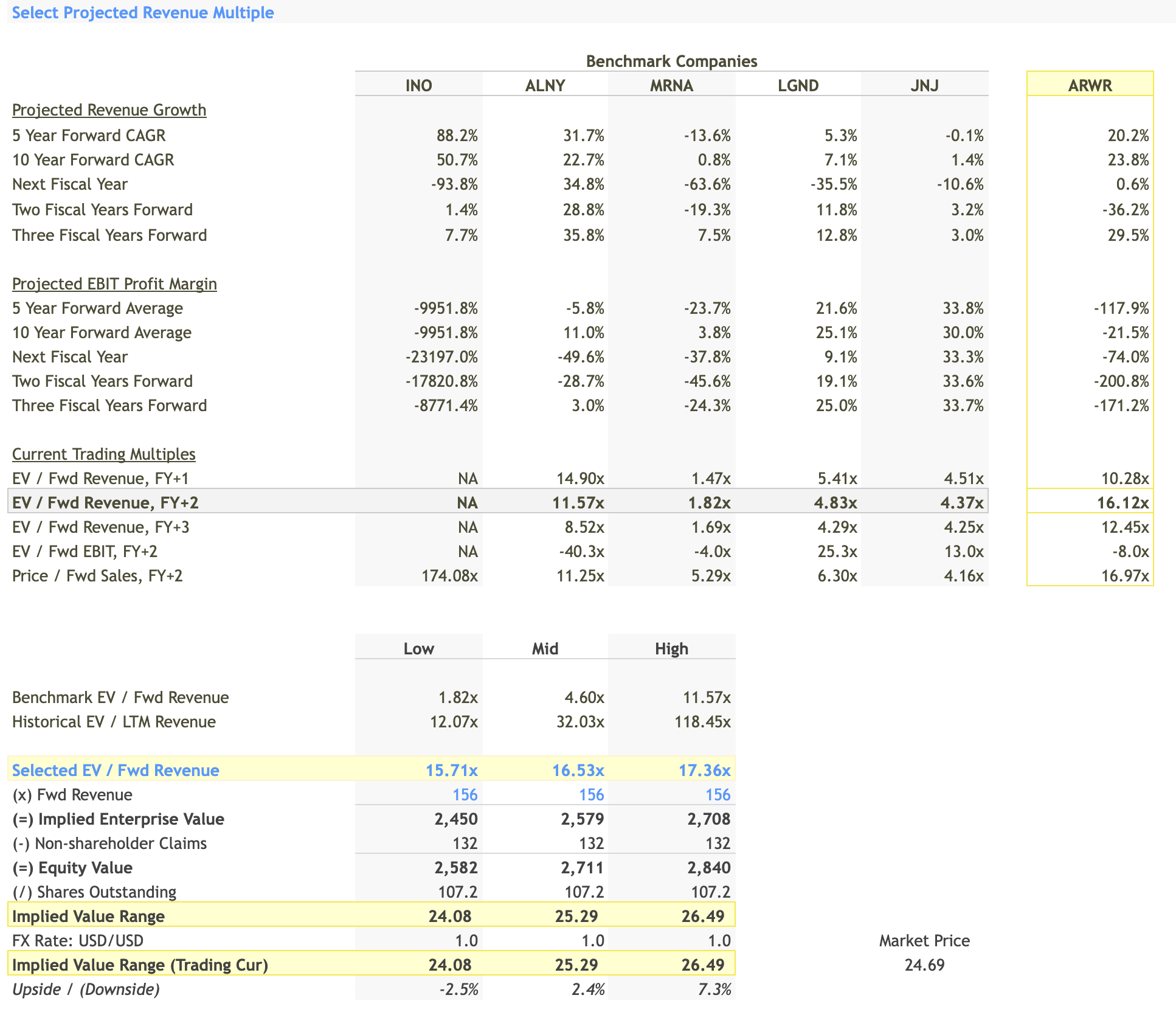

Select Forward Revenue Multiple

{kind=link}

For Arrowhead Pharmaceuticals, the 5-Year Forward CAGR is 20.2%, indicating solid growth prospects. In comparison, the benchmark companies have forward CAGRs ranging from a decrease of 13.6% (Moderna) to an increase of 88.2% (Inovio), giving us a diverse set of growth scenarios to consider.

To calculate the fair value, we selected a forward EV/Revenue multiple range of 15.71x to 17.36x. This range is notably higher than the benchmark range of 1.82x to 11.57x but is justified given Arrowhead's robust growth prospects. By applying these multiples to the projected forward revenue of $156 million, we arrive at an implied enterprise value range of $2,450 million to $2,708 million. Subtracting the non-shareholder claims of $132 million, we get an equity value range of $2,582 million to $2,840 million. Dividing by the total outstanding shares (107.2 million), we find an implied stock price range of $24.08 to $26.49.

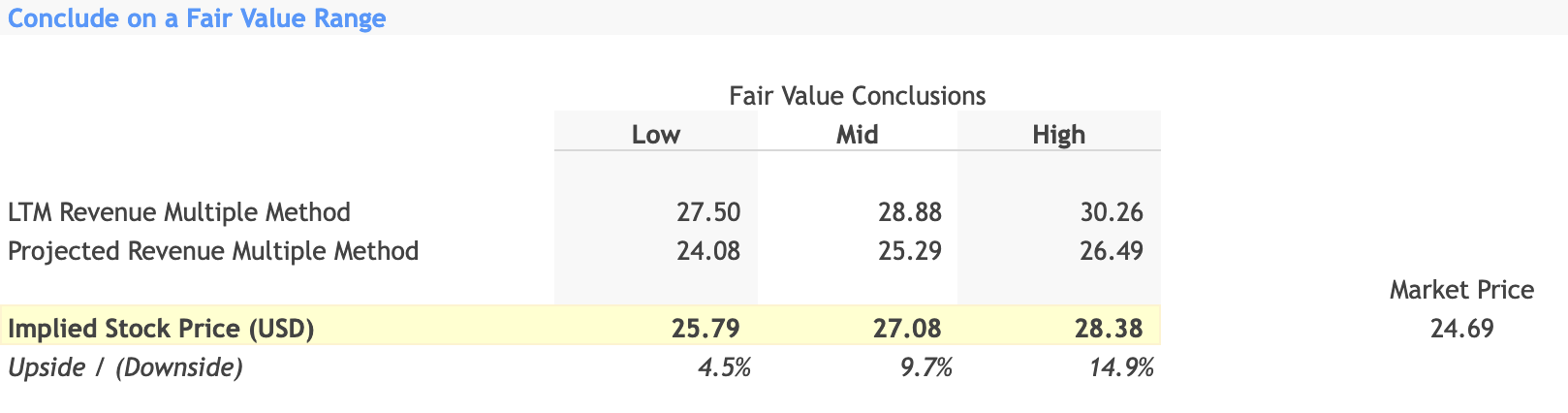

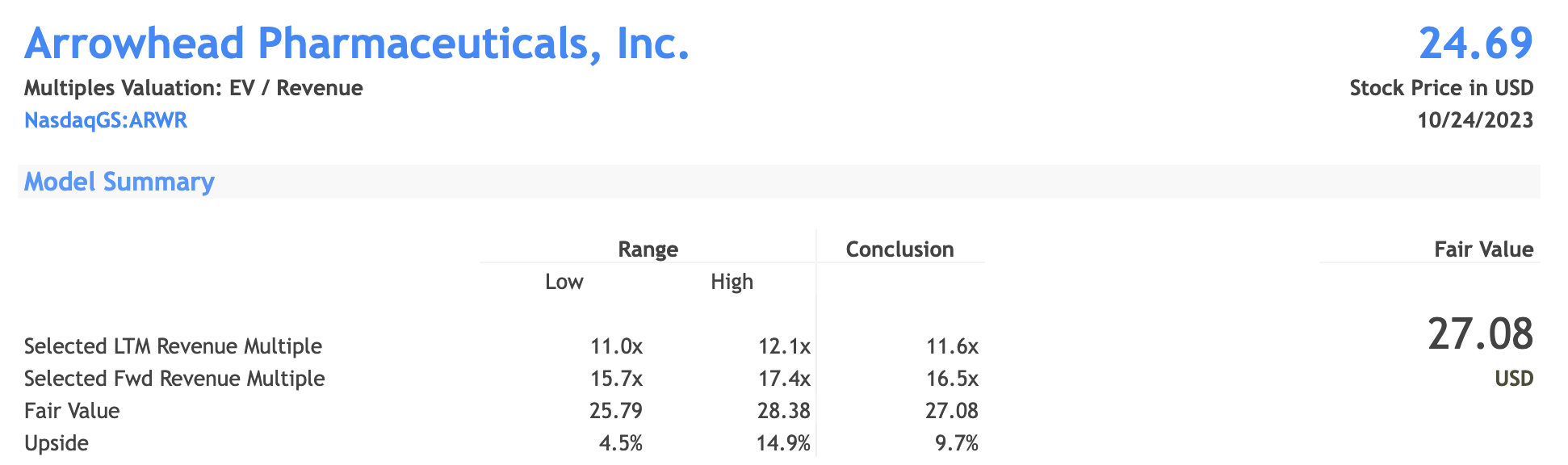

Fair Value Range

{kind=link}

By considering both LTM and projected revenue multiples, we derive an implied stock price range of $25.79 to $28.38. This range is based on Arrowhead's strong growth profile and its comparison to the industry benchmarks.

Investment Recommendation

{kind=link}

Considering the above, the mid-point of this fair value range is approximately $27.08, which presents an upside potential of about 9.7% from the current market price of $24.69. This implies that the stock is currently undervalued, which would usually suggest a "Buy" recommendation. However, it's essential to factor in potential risks, such as market volatility or any unforeseen negative news affecting the pharmaceutical industry.

Therefore, the most balanced investment recommendation for Arrowhead Pharmaceuticals at this time would be a "Hold." This is because while the stock appears to have upside potential based on our valuation, the recommendation accounts for the associated risks.

For further details see:

Arrowhead Pharmaceuticals: A High-Risk, High-Reward Bet