ARWR - Arrowhead Pharmaceuticals: Good Work In Progress

Summary

- Arrowhead is a strong biotech with unique and powerful attributes.

- The company has seen its share of recent struggles, including in share price.

- It leverages its RNAi technology to develop drugs with the potential to treat very serious diseases.

- Arrowhead has tightened its focus to achieve greater clarity for both drug development and test phase processes.

- I believe that the company is positioned to become a powerful pharma player.

Introduction

Since I last wrote about Arrowhead ( ARWR ), things have changed for this promising biotech company. Most changes have been positive, but not all. Weighing the elements on both sides of the scale depends on an investor’s outlook, as Arrowhead’s story has always been a long-term one.

It owns an innovative platform based on technology that applicable across disease categories. Positive results in FDA trials and increasing partnerships with established pharmaceutical companies support ARWR’s methodology and strategy.

Under the leadership of CEO Chris Anzalone, Arrowhead intends to be a major player in the pharmaceutical industry. This is a strategic ambition that's buttressed by the power of its pipeline and investigative drugs. However, the current pre-approval of these drugs requires investor patience.

ARWR has had its share of struggles. Some of these are internal, some are a byproduct of the biotech space, and some are macro-induced. It's no secret that the markets have received blow after blow from the effects of COVID and post- COVID realities, as well as from geopolitical events that have deepened the international economic malaise in the wake of the pandemic and the inflation that followed.

ARWR has not escaped these, while grappling with the challenges of drug development and associated trial phases. These include:

- The underperformance or misfire of specific drug trials, as with ARO-ENaC, the ARWR cystic fibrosis drug.

- ARO-HIF2, a promising entry for renal cancer, failing to attract a major pharma partner.

- JNJ-3989's mixed results in various clinical trials. This partnered Hepatitis-B drug, combined with another JNJ drug, has yet to deliver on its full promise in addressing this difficult disease.

- ARO-AAT ('Fazirsiran') for treatment of Alpha-1 liver disease and partnered with Takeda, now is likely to require full FDA Phase 3 trials before approval.

None of these developments objectively damages the ARWR story. ARO-ENaC has been replaced with a new version yielding solid trial results. JNJ may yet turn JNJ-3989 into a success that impacts ARWR’s bottom line through associated payments, while Fazirsiran is still in an excellent position to gain approval following Phase 3 trials.

The fundamental ability to develop drugs across disease categories and find willing large-pocket partners for some while others in-house is a practical, hybrid approach that also provides instrumental cash influxes to fund current and future development.

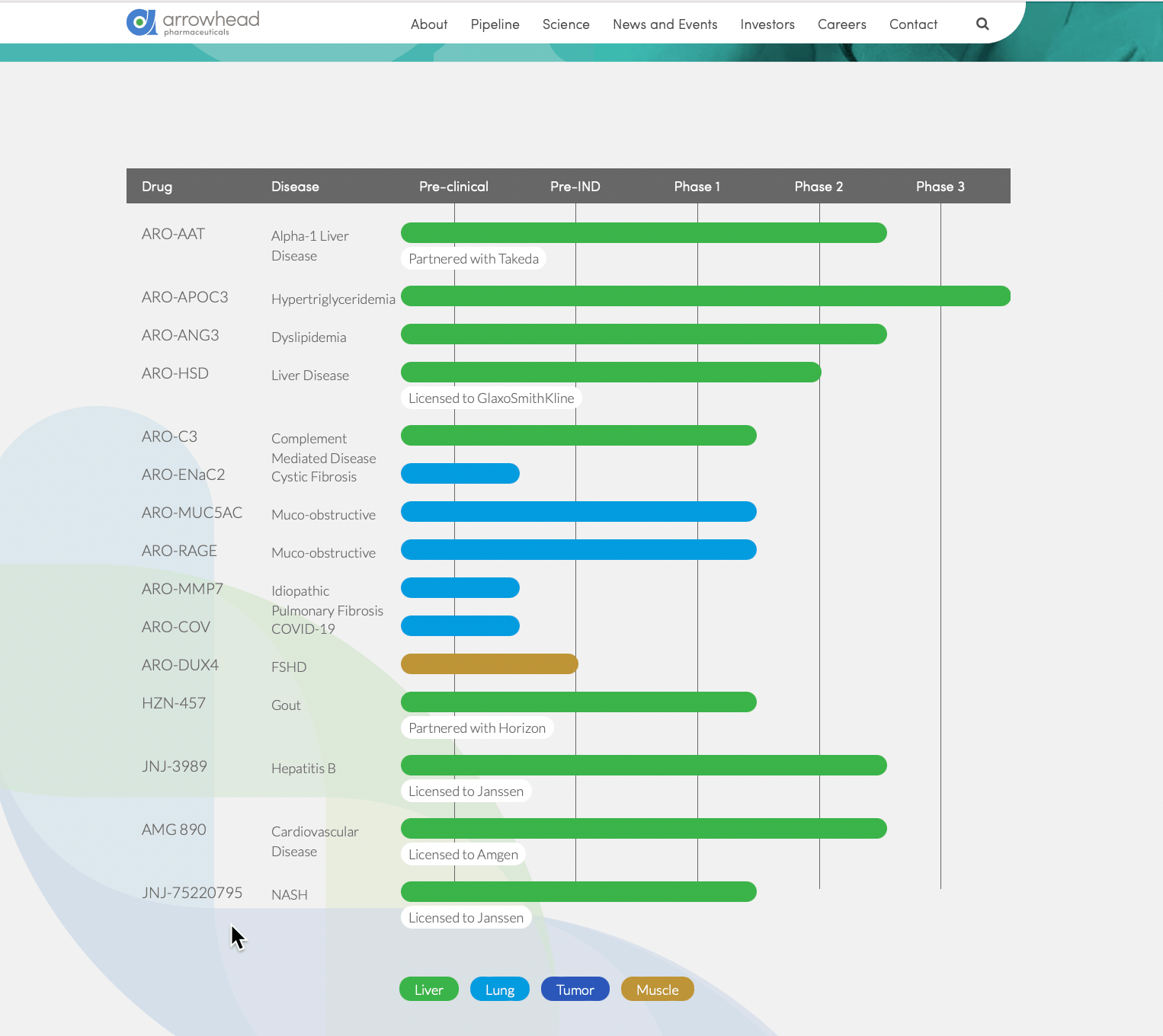

The Pipeline: Groups, Drugs, Partnerships And Timelines

The Arrowhead pipeline:

{kind=link}

Drugs in various phases from pre-clinical to Phase 3 number 15 in all. ARO-APOC3 is in FDA Phase 3, and four others have advanced to Phase 2 trials. Six drugs are partnered or licensed to one of five different partners (half of these are in Phase 2).

Despite the evidence of great progress, the setbacks described weigh both on the stock price and analyst/investor views of Arrowhead. CEO Anzalone addressed these concerns in the latest earnings report while emphasizing a focus clarity :

“We've seen clear progress across our large and balanced pipeline, large because it now includes 12 drug candidates in clinical trials and balanced because it spans in multiple therapeutic areas and includes six partnered programs and six that are wholly owned. It is a good representation of that which makes us different.”

Dr. Anzalone addressed the need to track drugs in development and trial phases - and for increased clarity :

“We have increased clarity as to the makeup of our multiple Phase 3 programs, increased clarity as to how we intend to use our late-stage drug candidates in different patient populations... we expect proof of concept from our earlier stage programs.. as to where we plan to go next with the expansion of our platforms into new cell types… as to how large we think our pipeline of clinical candidates will be over the next few years and...how we intend to finance our growing pipeline.”

Clarity is a code word for greater focus and attention to the business plan. Lessons have been learned from ARO-ENaC and ARO-HIF2 and JNJ-3989 — and from news that the FDA has put fast-tracked ARO-AAT (Fazirsiran) back on a standard Phase 3 schedule prior to any approval.

CEO Anzalone, in the Q3 earnings call , goes into further detail about shifting plans for specific drugs in different categories:

ARO-AAT (Takeda Fazirsiran)

Takeda submitted Phase 3 protocol information at end of Q3 and is expecting feedback. ARWR expects progress on AAT, and plans to provide top-line data from the Phase 2 SEQUOIA study while simultaneously giving guidance on Phase 3 study design.

Cardiometabolic Programs

“We are gaining a clearer understanding about how our cardiometabolic programs perform in different patient populations, and thus are better able to determine the positioning of each, and importantly the development paths and studies needed to seek approval for various indications…the interim analyses for the SHASTA-2 and MUIR studies of ARO-APOC3 and the ARCHES-2 study of ARO-ANG3. .. gave us some critical insights that are helping to accelerate the path to Phase 3 studies. We… expect to have further clarity, including from multiple anticipated regulatory interactions, in 2023.”

I believe that approval of one or two drugs in 2023 is essential to moving the ARWR share price up. The focus on practical patient population results, identifying paths/studies required as prerequisites to seeking approvals, and interim analyses as launch points for Phase 3 studies provide reassurance as well.

ARO-APOC3 and ARO-ANG3, which Dr. Anzalone addresses in this comment, are key drugs for Arrowhead, with ARO-APOC3 in Phase 3 trials. They are critical drugs among the six in-house (non-partnered) drugs.

Regarding ARO-APOC3, now in Phase 3:

ARO-APOC3 first targets FCS patients. What is FCS ?

“FCS: Familial chylomicronemia syndrome - FCS - is a rare genetic disorder estimated to affect 1-2 individuals per million . It is a serious disease that prevents the body from breaking down fats consumed through the diet, or triglycerides. These triglycerides are carried in the blood by large structures called chylomicrons.”

“While several genetic causes have been associated with FCS, about 80% of people with FCS have a problem with lipoprotein lipase. Lipoprotein lipase is a digestive enzyme in the blood that helps the body break down chylomicrons. People who have FCS are either unable to make lipoprotein lipase or have a broken form of it. When lipoprotein lipase is absent or not working properly, chylomicrons build up in the blood, and triglyceride levels rise.”

It also targets severe hypertriglyceridemia : Individuals with severe hypertriglyceridemia (SHTG) have triglyceride levels more than three times the normal level . SHTG can lead to multiple serious conditions, including cardiovascular disease ((CVD)) and acute pancreatitis.

Pulmonary Drugs

Another category is pulmonary disease category. There are some dreadful diseases within this grouping, and Arrowhead is tackling them with several new and very promising drugs.

“We believe we’ve made a lot of progress with the platform since our generation one candidate ARO-ENaC, and gaining clarity on how the generation two candidates perform will be exciting. Importantly, we are performing various analyses to assess pharmacodynamics using different methods, so we are confident that we should be able to define knockdown and duration of effect at different dose levels and different timepoints. The ARO-MMP7 Phase 1 started later than ARO-RAGE and ARO-MUC5AC, but dosing in healthy volunteers should begin imminently.”

The ability to define knockdown effects based on doses and time targets adds meat to the bone. ARO-MMP7 has enormous potential, given that it's targeted at idiopathic pulmonary fibrosis - IPF, a terrible disease that, when contracted, sets an end-of-life date of about three years.

With 100,000 patients in the US alone and 30,000 new patients diagnosed yearly creating a relatively small patient population, IPF has been neglected despite identification of its gene target more than 20 years ago. Yet only now has an RNAi drug been presented.

The ability to identify/locate virtually all IPF patients means that approval will result in near-immediate enrollment of at least 75% of the patient population, with new patient count increasing constantly. This may create a very focused and practical profit center intensified by patients seeking out approved relevant drugs.

If this provider is Arrowhead, revenue estimates may approach $4 billion a few years following approval. If valuation is approximately 4x revenue, the enormous potential of pulmonary is clear. A last point about ARO-MMP7: if it passes Phase 2 it may be fast-tracked to approval because of the pressing public need.

ARWR may become a brand of sorts for pulmonary disease treatment.

Complementary Mediated Disease

What's complementary mediated disease and what are the drug therapies that can treat these diseases?

Complement-mediated disease : Relates to the function or malfunction of complement proteins (as produced by the liver) that attack invading bacteria or pathogenic host cells in order to attempt to destroy disease. Such infection-fighting proteins are produced by hepatocytes — an important cell type in parenchymal tissues of the liver.

Hepatocytes direct the battle against infection by secreting specific proteins, called bactericidal complement proteins , an essential element of human immunity. Hepatocytes also maintain high serum concentrations in these pathogen-fighting proteins.

Complements form chemical cascades that dig pores in the membranes of invading bacteria or pathogenic host cells and then lyse their targets. These complement proteins are carried by three different pathways "configured" to work with them: a classical pathway, an alternative pathway, and a lectin pathway.

Arrowhead has entered the complement-mediated space through ARO-C3. The program is progressing and is expected to yield interim knockdown and safety data in the first part of 2023. The company is familiar with hepatocyte targets and eager to attack the range of complement-mediated and associated diseases. The practical financial benefits of success would be significant.

’20 For 25’ - A Three-Year Strategic Plan

A corollary to Arrowhead’s clarity directive is systematically growing the pipeline so the company can develop into a biotech power.

CEO Anzalone also presented the "20 for 25" plan, designed to reach 20 drug candidates by 2025.

“Between our hepatocyte-directed programs, our pulmonary programs, potential skeletal muscle targeted programs, and new cell-types, we believe we will hit 20 in the year 2025 between wholly owned drug candidates and partnered programs. This will be a remarkable achievement that has the potential to touch millions of lives and create substantial value.”

Benefits Of Partnerships

Arrowhead’s partnerships with reputable pharmaceutical companies make a critical contribution to operations and the consolidation of its profile and credibility. In practical terms, ARWR receives infusions of cash as milestones are reached for its partnered or licensed drugs. I laid out some of this in a previous piece on ARWR .

Another example is in the $25 million payment from Amgen announced this week. This milestone payment was triggered by Amgen reaching Phase 3 for Olpasiran. Separate from these Amgen-contracted milestone-dependent payments, Arrowhead recently negotiated sale of royalties from the drug to Royalty Pharma , receiving $250 million in cash and up to $160 million in additional payments (again, milestone dependent).

The partnerships have become an important piece of Arrowhead’s strategy and ability to fund the drugs I described earlier in this article. Splitting pipeline drugs between in-house and licensed is a smart and practical way to drive the company forward.

The Wisconsin Site: Facts and Implications

Arrowhead is building a multi-purpose facility in Wisconsin that includes manufacturing, laboratory and office facilities. Laboratory and office construction is targeted for Q1 2023 completion, while the manufacturing facility is scheduled for a Q4 2023 finish date.

Built on 13 acres of land, the campus will feature the 140,000 square foot drug manufacturing facility and a three-story laboratory and office space.

Reports indicate that construction is proceeding. While this project can be considered a form of essential housekeeping, it's an essential aspect of growth and evidence of Arrowhead’s confidence in its future.

Risks

A number of risks may threaten the Arrowhead story. Some relate to the company’s specific position, while others are functions of biotech industry realities.

- The RNAi technology that underpins the platform and drives the associated pipeline is found to be flawed. This would be a derailing event if it occurred.

Risk: Very Low. If such a flaw were a substantive threat, we would have seen evidence for it already. Instead, setbacks in individual drug candidate trials were specific and unique. The consistent progress of multiple drugs through demanding pre-trial and trial phases shows the strength of Arrowhead’s foundational technologies.

2. Competitors beat the company to market in multiple categories and in regard to multiple target diseases. Risk: Low. While certain competitors have gained approval for drugs that have similar purposes to ARWR drugs or have others in investigative phases, these are limited in number. Trial/test results with patient populations have consistently demonstrated the empirical superiority of Arrowhead drugs’ therapeutic results.

3. Financial issues slow or halt the company’s ability to pursue its strategic goals such as the enunciated "20 for 25" program.

Risk: Low. I see a practical approach to financial management. While it would be nice to know more about how financial decisions are made, especially in the 50-50 in-house development versus partnering/offloading of specific drugs, the methodology appears to be working. Given that ARWR is still in pre-approval stages for every drug in its pipeline, the financial numbers are reasonable.

The partnership/licensing/royalty agreements are positioned to finance development and trial phases. Depleting working cash before looks to be a remote possibility.

4. There is a management shakeup or key C-suite exodus.

Risk: Very Low.

The length and continuity of service of CEO Anzalone and other key scientific and business personnel looks very solid. While surprises can happen because of professional or personal considerations, key players appear committed to the company’s strategic success.

Summary

My view of Arrowhead remains resolutely positive despite the precipitous drop in share price from the highs of mid-2021, when it reached about $90 per share. The descent has been sharp and fairly consistent:

{kind=link}

The effect on shareholders is real and stress-inducing. Yet, the greatest investors always remind us that we don’t buy shares of a company (though we also do that). We are buying small pieces of a business when we purchase shares. Investing in my view means holding shares of those businesses until the story changes or until personal financial circumstances intervene.

When projecting performance for the company and its shares, I think we need to consider these factors: Company history, leadership, sector characteristics and Arrowhead’s own strengths and weaknesses. I see mostly positives, though prospective investors are right to factor in the volatility of relatively small pharmaceutical companies playing in a large, very competitive space. Survival requires skill, smart strategy and execution. If Arrowhead has struggled in the past few years, it has been in executing certain aspects of its strategy. More specifically, it has not executed as well as it might have.

I also see the company directly addressing these challenges, honing its strategy and giving greater attention to detail as investigative drugs are tested and tried. I also think that its platform is proven and its pipeline growing in strength.

Fixing price targets for ARWR at this stage of its development is directly related to how quickly several of its leading drugs can achieve approval. Looking ahead one year, I believe that at least one approval can trigger a share price rise to $60-$70 per share. Two in that same time frame would send the share price to the region of $90-$120. I think the same logic applies when viewing things two or three years out. I personally believe that Arrowhead will win a series of approvals for enough of its drugs to become a powerful pharmaceutical company and a potential "multi bagger."

For further details see:

Arrowhead Pharmaceuticals: Good Work In Progress