AJG - Arthur J. Gallagher: Nice Growth But Trades At A Large Premium

2024-01-16 04:51:27 ET

Summary

- Arthur J. Gallagher & Company is the fourth largest insurance broker focusing on risk management globally. The company has three business units: brokerage, risk management, and corporate consulting.

- Over the years, AJG stock has beat the overall market in total returns by a large margin but this also created a high valuation premium.

- There has also been a lot of stock dilution in order to drive the company's aggressive acquisition policy.

- While the company has shown impressive growth, its current valuation suggests a large premium, and investors may want to wait for a correction before investing.

Arthur J. Gallagher & Co. ( AJG ) is an insurance company that focuses on insurance and reinsurance brokerage, consulting, risk-management solutions, claims settlement, and administration services to businesses, government institutions, and non-profit organizations globally. This is the world's fourth-biggest insurance broker focusing on risk management based on revenues. While the company offers an impressive growth rate and has a history of outperformance, it is probably trading at a pretty large premium right now and investors would be better off if they wait for a correction or pullback to get in.

The company has three business units that are called (1) brokerage, (2) risk management, and (3) corporate consulting. The brokerage segment is the largest one accounting for about 85% of the company's total revenues and it includes fees and commissions collected from customers.

The company's insurance products cover a wide variety of scenarios that can occur in many different industries such as casualty, disability, product liability, professional liability, property, natural disasters, healthcare, medical, fire, executive benefits and compensation. Some of the company's largest customers include automotive industry, restaurant industry, technology industry, healthcare industry and energy industry. The company also offers aviation-related insurance products for this particular industry which comes with its own set of risks and opportunities.

The company's stock performed very well over the years, outperforming the overall index ( SPY ) in total returns by a margin of more than 100% in the last decade. The stock's outperformance was mostly driven by the company's strong sustainable growth over the years.

In the last 10 years, the company's revenues rose by 182% while its net income rose by 310%. The reason the company's profits grew at a much faster rate than its revenues was due to cost cutting, better financial management, and synergies coming from its mergers and acquisitions over the years. However, keep in mind that while the company's net income grew by almost 310%, its EPS (earnings per share) only grew by about 150% during this period which indicates share dilution, some of which was also driven by the company's aggressive merger & acquisition policy.

The company is certainly not shy about making acquisitions in order to fuel its growth, which accounts for some of its share dilutions. Just in the last 10 days, it announced two acquisitions. First, it announced acquisition of Köberich Financial Lines on January 8th and then it announced the acquisition of MCMM Services Limited three days later on January 11th. Since both acquisitions were previously private companies, the transaction details such as the price paid were not announced. Typically this company likes to make a large number of small acquisitions that add up over time rather than making a few acquisitions that are very large. Each acquisition is hand-picked to ensure that it will meet the company's long-term growth rate by either supplementing its existing offerings, creating new markets for the company, or creating cross-selling opportunities for the company. We don't know how much the company is paying for most of these acquisitions but we can probably have an idea by looking at the company's diluted share count. It is also possible that a lot of these acquisitions were made using stock rather than cash as currency. In 2023 the company made close to 40 acquisitions and collectively those acquisitions added about $475 million to its annual revenues (estimated by the company).

In the last decade, the company's average diluted share count grew from 130 million to 220 million which indicates a growth of 62%. Some investors certainly won't like this because more diluted shares mean that each share becomes less valuable. Still, the fact that this stock outperformed the overall index by a margin of more than 100% despite all this dilution means that the company must be doing something right at least.

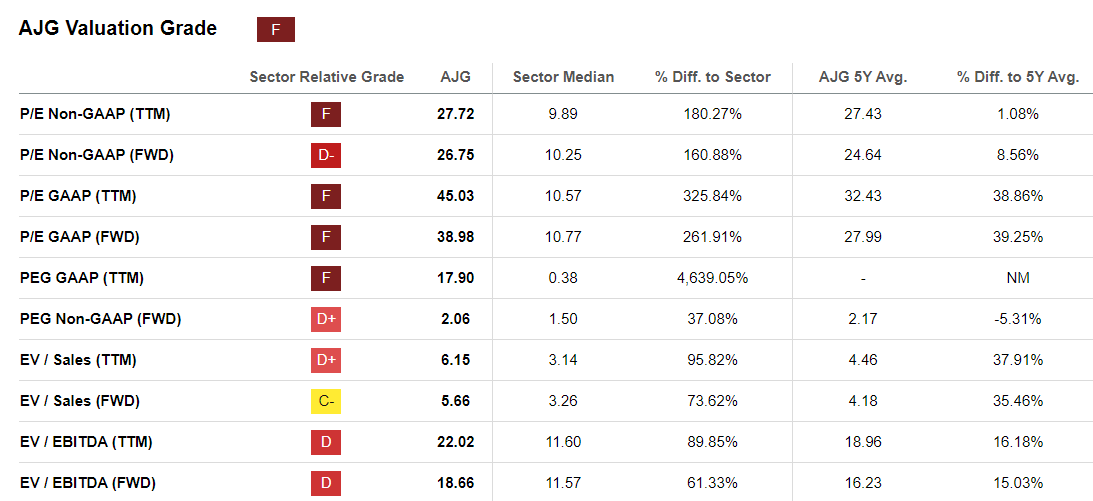

The company currently trades at a P/E of 45 which indicates a premium over its long-term valuation. In the last decade, the company's P/E ratio ranged from 16 to 48 and its current valuation is much closer to the top of its range than its bottom and much higher than its long-term average P/E of 27. One could even argue that some portion of the stock's multi-year outperformance came from P/E expansion as its P/E more than doubled in the last decade from 20 to 45. Then again, one could also make the same argument for the overall market (measured by S&P 500 index) since its P/E also expanded from 13 to 25 in the last decade.

Not only does the company's valuation look rich as compared to its own historical averages, but it also looks rich as compared to its peers. The company's non-GAAP P/E of 27 is almost triple the sector median of 9.8 and its GAAP P/E of 45 is more than quadruple the sector median of 10.77. The company's PEG (P/E divided by its growth rate) is almost 18 as compared to the sector average of 0.38 indicating that investors are overpaying for the company's growth by a large margin. Also, the company's EV/EBITDA ratio of 22 is twice the sector median of 11. It's clear that the company trades at a large premium against its peers. The big question is whether it deserves such premium or not. Having a premium over your peers in valuation is not a big deal if your growth rate justifies it as we've seen in companies like Nvidia ( NVDA ) but if it's not justified by robust growth, it becomes a problem.

Valuation Metrics (Seeking Alpha)

{kind=link}

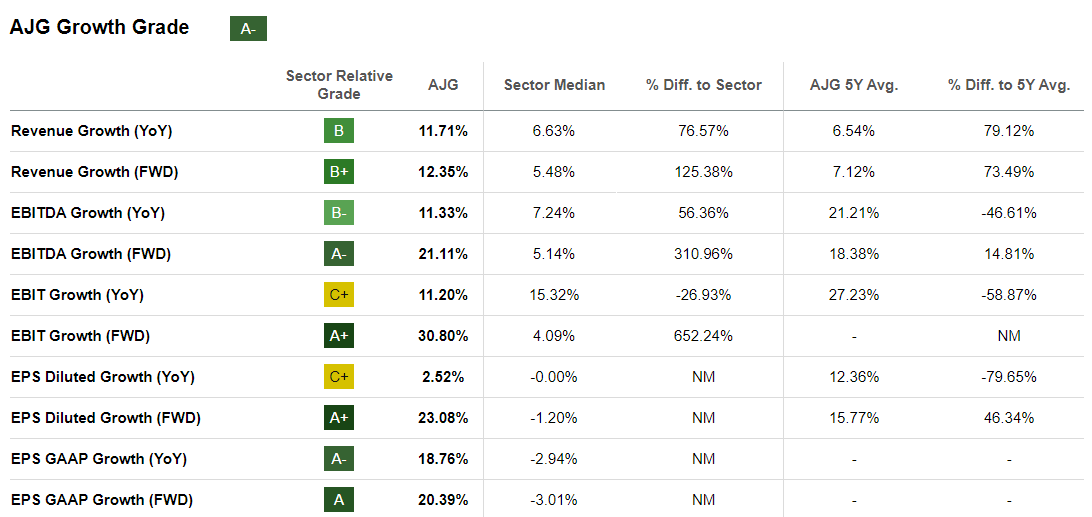

Then let us look at the company's growth rate as compared to its peers. At first look, it looks like the company has a pretty good growth rate. Its annual revenue growth came at 11.7% versus its peers having a growth rate of 6.6%. Its EBITDA growth came at 11% versus its peers which posted a 7% growth rate. But these are in nominal terms. When we look at per share metrics (accounting for share dilution), the numbers look less impressive as the company's EPS diluted growth rate came at only 2.52% (still better than its peers averaging 0% last year). Meanwhile, the company's "forward" metrics look impressive such as forward EBITDA growth rate of 21% forward EBIT growth of 30%, and forward EPS growth rate of 23% but these could be just analysts being overly optimistic about the company's prospects.

{kind=link}

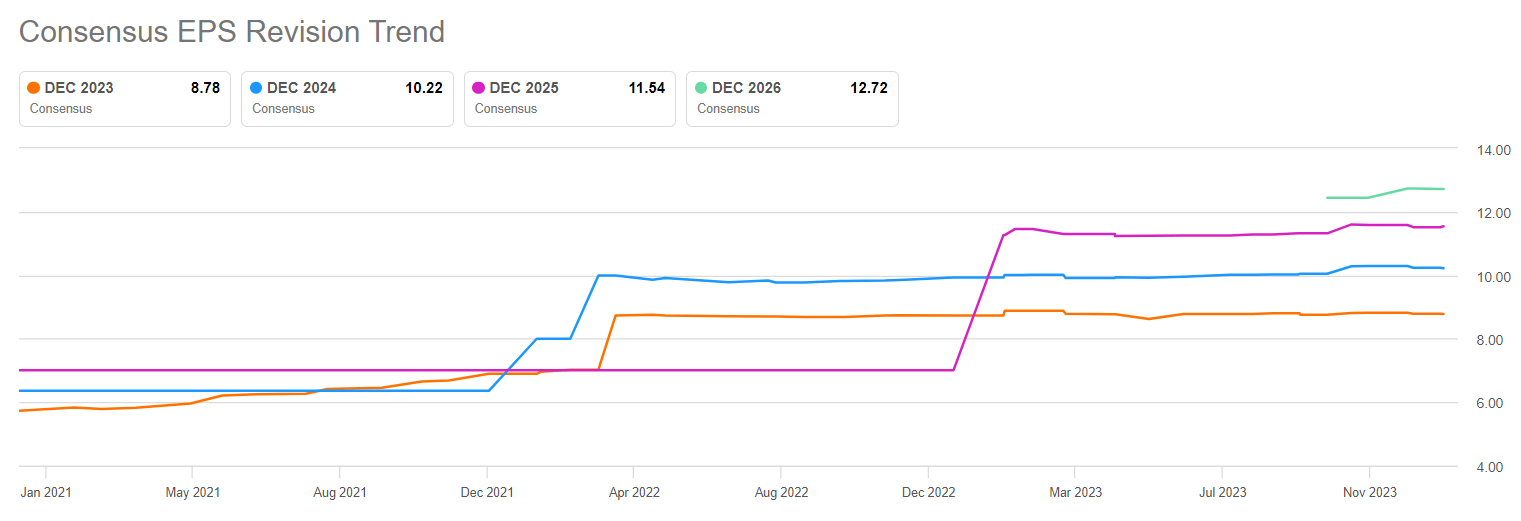

Speaking of analysts, they have been revising their estimates higher and higher for this company so they believe that the company's earnings growth will far outpace its share dilution. Analysts expect the company to grow its EPS to $10 in 2024, almost $12 in 2025 and almost $13 in 2026. If this happens, shares suddenly don't look as expensive with a forward P/E of 20 based on 2025 earnings estimates.

Analyst Estimates (Seeking Alpha)

{kind=link}

One word on dividends. The company has a long history of hiking dividends over the last 4 decades but keep in mind that its dividend yield is still less than 1% (about 0.9% to be exact) and dividends shouldn't be the main reason you are investing in this company. Most of this company's returns will come from share price appreciation in the long run as opposed to dividends. It's a good dividend growth stock but it will be many years before your dividends reach a meaningful number unless you bought many years ago and have been holding until now. For example, if you had bought 5 years ago your yield on cost would be 3% which is more than triple the current yield. If you had bought 10 years ago, your yield on cost would have been close to 5%. In that case, you are getting a nice yield in addition to dividend hikes year after year.

All in all, this is a good growth company but its valuation and constant share dilution keep me from rating it a "buy" at the moment. The company's current valuation suggests a large premium against its peers and its PEG ratio is dangerously high so it's up to each investor to decide if this premium is worth it or not.

For further details see:

Arthur J. Gallagher: Nice Growth But Trades At A Large Premium