AJG - Arthur J. Gallagher: Reiterate Buy Rating On Strong Earnings Growth Prospect

2023-08-01 08:27:10 ET

Summary

- I recommended a buy rating due to AJG's strong earnings growth prospects in FY23 and FY24.

- AJG reported strong Q2 results, with total revenue growth of 17.4% and organic revenue growth of 10.8%.

- The brokerage and risk management segments both exceeded expectations, and management anticipates continued growth in the near term.

Overview

My recommendation for Arthur J. Gallagher ( AJG ) stock is a buy rating as I expect earnings growth to remain strong in FY23 and FY24, which will continue to support the current 23x forward PE. Note that I previously gave AJG a buy rating due to my optimism about the business future as the insurance brokerage industry remained healthy and there were no visible hard catalysts that might slow growth in the near term.

Recent results & updates

AJG reported total revenue of $2.4 billion , adj EBITDAC of $676 million, and adj EPS of $1.90, 70c ahead of Consensus estimates. This strong performance was driven by strong organic growth. Total revenue growth rate reached 17.4%, 710bps higher than 1Q23 on a reported basis. Organic revenue growth rate was 10.8%, 110 bps higher than 1Q23. Adj. EBITDAC margin came in at 32.1%, a minor expansion sequentially.

I think this was a very strong quarter for AJG, with strong growth and margins that exceeded management’s own guidance. What’s even better is that management forward looking comments are supportive of growth in the near-term. I expect consensus and the market to react very positively to these results, increasing estimates and further supporting valuation.

Brokerage

Brokerage organic growth was 9.7%, 240 bps above management's 7-7.5% guidance midpoint. It's noteworthy that growth occurred across a wide range of offerings and geographic areas. The quarter ended on a high note for both the U.S. Retail and U.K. Specialty businesses, contributing to the beat against management's own guidance. Even more encouraging was the fact global renewal premium change (RPC) increased by 12% in the first two months of the quarter (indicating continuous momentum), exceeding the 11% guidance management had provided at the June Investor Meeting. For FY23 as a whole, including the 3Q/4Q, management now anticipates achieving the upper end of the 8-9% organic growth range previously discussed. Furthermore, management has indicated that they anticipate 2024 organic growth to be very strong and similar to 2023. Given the current rate environment, I anticipate that the upward trend in insurance and reinsurance premiums will continue through at least 2024.

The segment's adjusted EBITDAC margin increased by 50 basis points to 32.1%, which again exceeded management's margin expansion guidance of 10 basis points. Moreover, management noted that if organic growth were to be 9% in 2024, then 80bps of margin expansion would be achievable.

Risk management

Even more impressive was the 18.1% organic growth in the Risk Management segment. Rising claim numbers and sustained growth from recent new business wins were to key reasons to AJG achieving these results, which beat management guidance as well. Notably, new business wins have come from a diverse range of clientele, including governmental agencies, large corporations, and insurance companies and captives. Although growth is robust, I do not anticipate a repeat performance of this magnitude in 2H23 due to a challenging comparison to 2H22, which benefited from lumpy new business.

As a result of higher operating leverage, the profit margin of 19.4% also exceeded management's expectations for the quarter, which had been set at 19.0-19.5%. For 2H23, management anticipates a quarterly margin of greater than 19.5% and an annual margin of close to 20%

Valuation and risk

Author's valuation model

According to my model, AJG is valued at $268 in FY24, representing a 24% increase. This target price is based on growth rates similar to my previous model, except that I have increased my estimates for FY23 and FY24 by a modest margin to incorporate management's positive outlook.

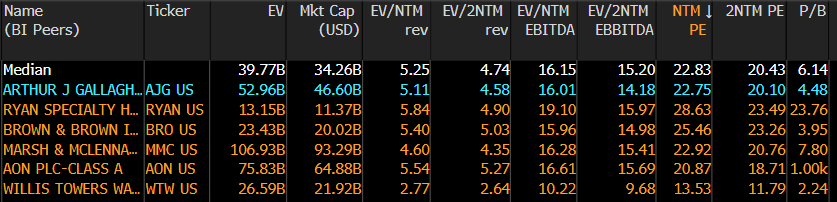

AJG is now trading at 23x forward PE, which I believe is well supported in the near-term as the earnings momentum and sentiment are very strong right now. Also, given the current rate environment, investors are likely to invest in assets that provide positive exposure to it, of which AJG is a prime candidate. I note that the industry is also trading at a similar level, so AJG is not an outlier here.

{kind=link}

Bloomberg

Summary

I reiterate a buy rating for AJG based on its strong earnings growth prospects. The recent results and updates indicate robust performance, exceeding expectations and management's guidance. The brokerage segment showed impressive organic growth, and the risk management segment also performed well. With positive forward-looking comments from management and a supportive rate environment, I anticipate continued growth in the near term.

For further details see:

Arthur J. Gallagher: Reiterate Buy Rating On Strong Earnings Growth Prospect