AJG - Arthur J. Gallagher: Strong Growth And Margin Expansion Warrants A Premium Valuation

2023-10-31 09:31:59 ET

Summary

- I recommended a buy due to AJG expected growth in its brokerage segment and margin expansion.

- AJG's recent quarter performance in the Brokerage segment exceeded expectations, with organic growth of 9.3% driven by reinsurance and the U.K. Specialty businesses.

- Management expects sustained economic resilience, stable insurance pricing, and increasing renewal premiums, supporting a positive outlook for AJG's future performance.

Overview

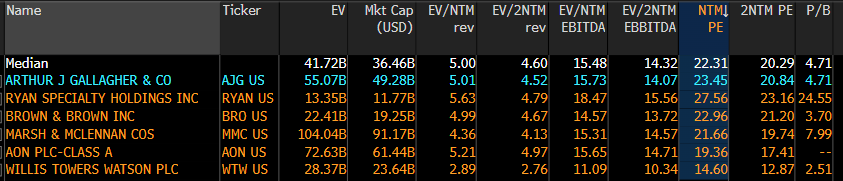

My recommendation for Arthur J. Gallagher ( AJG ) is a buy rating, as I gained more confidence in the business's ability to grow its brokerage segment and expand margins. The relative expected growth outperformance vs. peers should continue to support AJG trading at a premium valuation of 23x forward PE. Note that I previously rated the buy rating for AJG as I expect earnings growth to remain strong in FY23 and FY24, which will continue to support the current 23x forward PE.

Recent results & updates

AJG has recently announced another robust quarter performance in the Brokerage segment. This discussion will primarily concentrate on the latter segment (given that it is the majority of the business profits). The Brokerage segment experienced organic growth of 9.3%, surpassing management's projected growth rate of 9% by 30 basis points. Growth was widespread across product lines and geographic regions, with strong results in reinsurance and the U.K. Specialty businesses in particular driving the better-than-expected results versus management guidance in the previous investor meeting (September). The organic growth of the company was primarily driven by reinsurance, which experienced a significant increase of 20% due to a robust renewal process. Additionally, the U.K. specialty sector contributed to the organic growth with a growth rate of 18%, primarily attributed to the acquisition of new business opportunities. Furthermore, the AUS/NZ region witnessed a 13% organic growth, which is attributed to the acquisition of new business ventures and a substantial change in premium rates resulting from strong renewal activities.

Brokerage should remain a strong performer for AJG, as management has stated its expectation of sustained economic resilience. The crucial evidence here is that business activity among AJG's customers remains more robust than what news headlines suggest, and management has restated its characterization of business activity as strong. Management observed that the daily indicators during 3Q23 demonstrated annual growth in favorable mid-year policy endorsements and audits. Furthermore, it is worth mentioning that a significant disparity persists between the number of available job positions and the quantity of individuals who are unemployed, thereby exacerbating the prevailing conditions of a constrained labor market. In addition, I would like to emphasize that insurance and reinsurance pricing should be stable due to the fact that insurance companies are currently facing inflation, higher weather activity, and isolated areas of unfavorable casualty reserves. Another factor that has led me to have a positive outlook on future performance is the increase in global 3Q23 renewal premiums by 10%. This figure surpasses the previously reported range of 8–10% that the company had been reporting during FY22 and 1Q23. Furthermore, when adjusting for business mix, the 10% increase in 2Q23 suggests a level of stability that is consistent with the previous quarter. The management has observed that, after accounting for variations in business composition, there is no discernible indication of any shifts in the overall market trends. The trend of rising renewal premiums persisted across most product categories and all major regions.

Moving to our customers business activity, overall it continues to be more resilient than headlines would suggest, and we continue to characterize it as strong. From: 3Q2023 earnings call

The margin performance in 3Q23 was exceptional, with the adjusted EBITDAC margin expanding to 32.4%. This surpassed the management guidance of a 40 basis point margin expansion after adjusting for currency fluctuations. Upon deconstructing the margin expansion equation, it is evident that there exists a potential for further expansion of margins. The expansion of the margin was primarily attributed to two factors: organic growth, which accounted for 80 bps, and fiduciary investment income, which contributed 90 bps. However, this growth was partially offset by the impact of M&A, resulting in a decrease of 65 bps. Additionally, incremental technology investments of $7 million (equivalent to 35 bps) and travel and entertainment (T&E) inflation of $3 million (equivalent to 15 bps) also had a negative impact on the margin expansion. Of the negative headwinds, technology investments and T&E inflation should eventually taper off relative to growth, which means margins could’ve expanded much more. Management also indicated that they anticipate a potential adjusted margin expansion opportunity of 40–50 basis points in 4Q23. This information suggests that there is a likelihood of continued margin expansion in fiscal year 2024.

Valuation and risk

Author's valuation model

According to my model, AJG is valued at $278 in FY24, representing a 22% increase. The target price is derived from growth rates that align with the previous model, with the exception of slightly elevated estimates for FY23 to account for management's optimistic comments.

The current forward PE of AJG stands at 23x. I am of the opinion that this valuation is adequately justified in the short term due to the robust earnings momentum and positive market sentiment currently observed. Also, given the increased visibility of margin expansion, I expect investors to be more confident in their near-term estimates, which is positive for stock sentiment. Furthermore, it is justifiable for AJG to command a higher valuation compared to its industry peers due to its projected growth rate, which is anticipated to exceed 10%, while its counterparts are expected to achieve growth rates in the mid-to-high single digits.

{kind=link}

Risks

The company AJG stands to gain from increased interest rates, however, it also faces a dual risk that could potentially have negative consequences for its business operations and overall valuation in the long run. A change in interest rates on the operational front will have an adverse effect on premium growth, thereby reducing the generation of significant incremental profits. Consequently, AJG's fixed cost structure will lead to substantial decreases in earnings. While it is possible that there could be a rise in quantity, it is improbable that it would completely offset the decline in pricing. In light of valuation considerations, it is unlikely that AJG will be able to sustain its present elevated valuation multiples in the face of decelerating growth, primarily attributable to the influence of declining interest rates.

Summary

I recommend a buy rating for AJG based on its strong growth and margin expansion. The Brokerage divisions have performed exceptionally well, with significant organic growth across product lines and regions. The brokerage segment, in particular, has shown resilience and is expected to remain a strong performer. Management's outlook on economic resilience, pricing stability, and increasing renewal premiums further supports a positive view of AJG's future performance. Margin expansion has been impressive, with further potential indicated by management. Technology investments and travel expenses are expected to taper off relative to growth, offering room for margin improvement in fiscal year 2024.

Valuation remains justified with AJG trading at a forward PE of 23x, considering its strong earnings momentum and growth prospects. The company's expected growth rate exceeds industry peers, justifying a premium valuation. However, the company faces risks, including the potential negative impact of declining interest rates on premium growth and valuation.

For further details see:

Arthur J. Gallagher: Strong Growth And Margin Expansion Warrants A Premium Valuation